Epoxy Encapsulant Material for Automotive Market

Epoxy Encapsulant Material for Automotive Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701395 | Last Updated : July 29, 2025 |

Format : ![]()

![]()

![]()

![]()

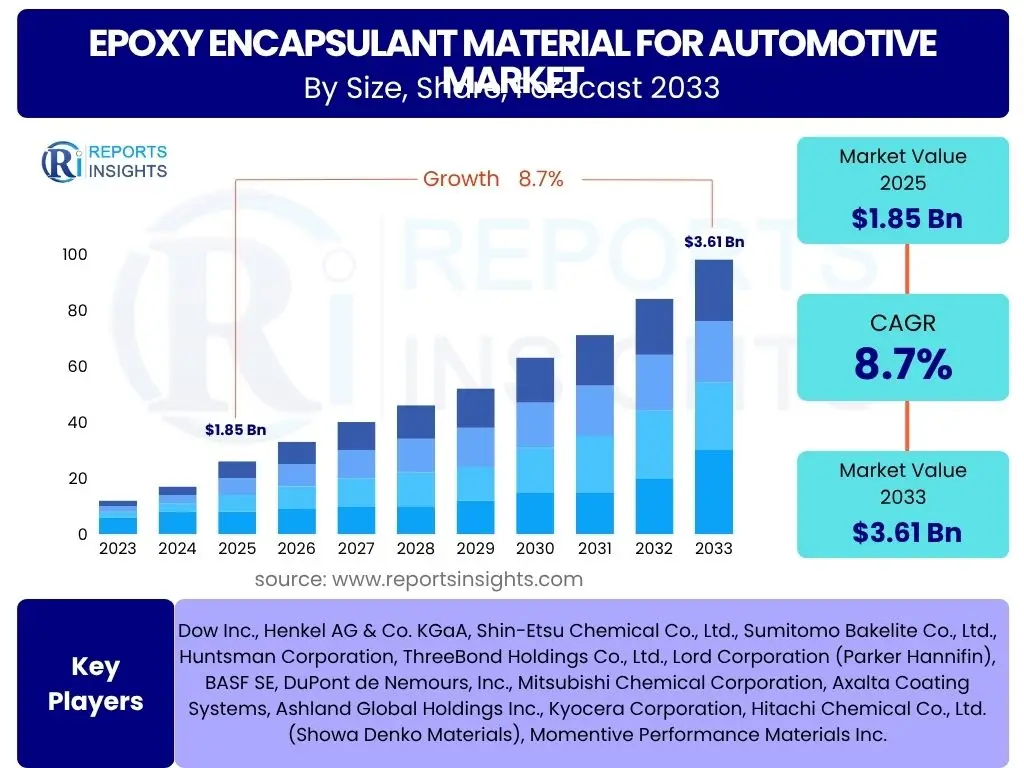

Epoxy Encapsulant Material for Automotive Market Size

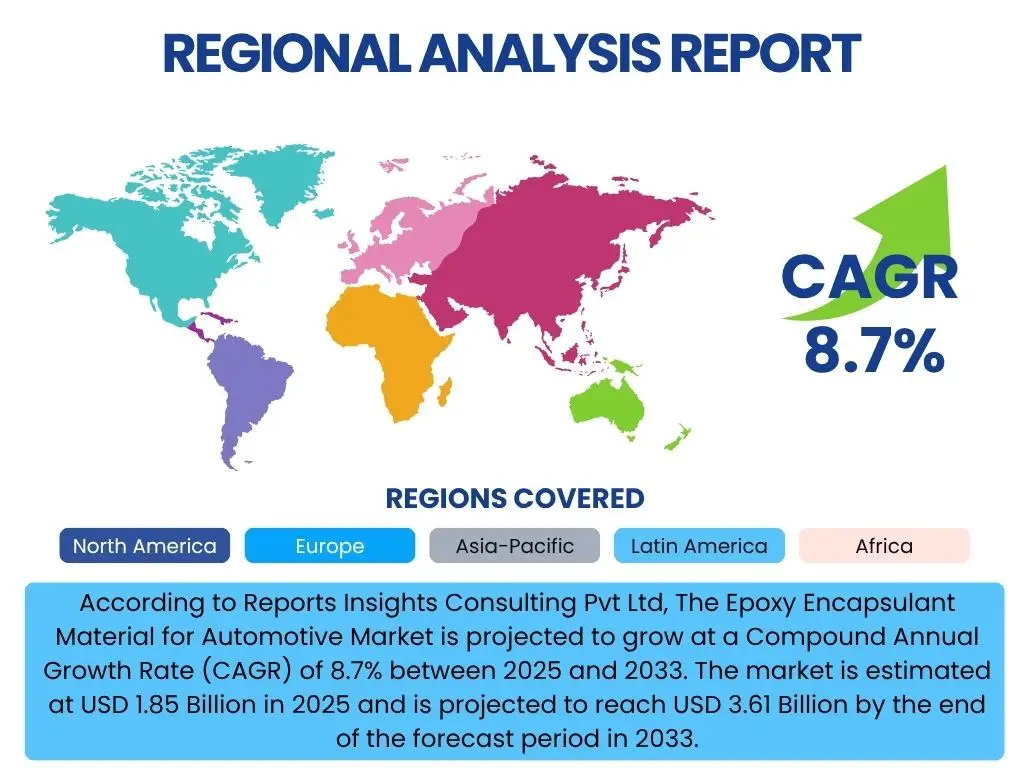

According to Reports Insights Consulting Pvt Ltd, The Epoxy Encapsulant Material for Automotive Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.7% between 2025 and 2033. The market is estimated at USD 1.85 Billion in 2025 and is projected to reach USD 3.61 Billion by the end of the forecast period in 2033.

Key Epoxy Encapsulant Material for Automotive Market Trends & Insights

The Epoxy Encapsulant Material for Automotive market is currently shaped by several transformative trends driven by advancements in vehicle technology and evolving consumer demands. A significant shift towards electric vehicles (EVs) and hybrid electric vehicles (HEVs) is fueling the demand for high-performance encapsulation solutions that can protect sensitive electronic components from harsh operating conditions. This includes the need for enhanced thermal management capabilities and superior dielectric properties to ensure the reliability and longevity of power electronics, battery management systems, and on-board chargers.

Furthermore, the proliferation of advanced driver-assistance systems (ADAS) and autonomous driving technologies is accelerating the adoption of epoxy encapsulants. These systems rely on numerous sensors, cameras, and LiDAR units, all requiring robust protection against moisture, vibration, and extreme temperatures. Miniaturization of electronic components, coupled with the increasing complexity of vehicle architectures, necessitates encapsulants that offer excellent adhesion, low stress, and compatibility with various substrates, paving the way for advanced formulations tailored for specific applications.

- Growing demand for electric and hybrid vehicles driving encapsulant use in power electronics and battery modules.

- Integration of advanced driver-assistance systems (ADAS) and autonomous vehicle technologies increasing the need for robust sensor encapsulation.

- Emphasis on thermal management solutions for high-power density automotive electronics.

- Development of bio-based and sustainable epoxy formulations to meet environmental regulations and corporate sustainability goals.

- Miniaturization of electronic control units (ECUs) and components demanding precise and low-stress encapsulating materials.

AI Impact Analysis on Epoxy Encapsulant Material for Automotive

Artificial intelligence (AI) is poised to significantly impact the Epoxy Encapsulant Material for Automotive market by revolutionizing material design, manufacturing processes, and quality control. AI-driven algorithms can analyze vast datasets of material properties, performance characteristics, and processing parameters, enabling chemists and engineers to rapidly identify optimal epoxy formulations for specific automotive applications. This accelerates the research and development cycle, leading to the creation of novel encapsulants with enhanced thermal conductivity, improved adhesion, and superior dielectric strength, addressing critical performance gaps in next-generation vehicles.

In manufacturing, AI can optimize production lines by predicting equipment failures, refining curing profiles, and ensuring consistent material mixing, thereby reducing waste and improving overall efficiency. AI-powered vision systems can perform real-time quality inspections, detecting microscopic defects or inconsistencies in encapsulated components that might be missed by human inspection, ensuring higher product reliability. Furthermore, AI can aid in supply chain management, predicting demand fluctuations and optimizing inventory, which is crucial for managing the complex raw material procurement for epoxy resins.

- Accelerated material discovery and optimization through AI-driven predictive modeling for novel epoxy formulations.

- Enhanced quality control and defect detection in manufacturing processes using AI-powered vision systems and analytics.

- Optimized production parameters and curing cycles for improved efficiency and reduced material waste.

- Predictive maintenance for manufacturing equipment, minimizing downtime and ensuring consistent encapsulant production.

- AI-driven supply chain optimization for raw materials, enhancing resilience and responsiveness.

Key Takeaways Epoxy Encapsulant Material for Automotive Market Size & Forecast

The Epoxy Encapsulant Material for Automotive market is experiencing robust growth, primarily propelled by the widespread adoption of electric and hybrid vehicles, alongside the increasing sophistication of automotive electronics. The market’s expansion is indicative of the critical role these materials play in ensuring the reliability, safety, and longevity of complex electronic systems within modern vehicles. Anticipated growth figures highlight a sustained demand trajectory, driven by technological advancements and stringent performance requirements across various automotive applications.

A key insight from the market forecast is the pronounced shift towards high-performance encapsulants capable of withstanding extreme temperatures, vibrations, and harsh environmental conditions, especially prevalent in power electronics and ADAS modules. The market is also witnessing a trend towards sustainable and lightweight solutions, reflecting broader industry efforts towards environmental responsibility and vehicle efficiency. Strategic investments in research and development by key players, focusing on innovative formulations and processing techniques, will be pivotal in shaping the competitive landscape and unlocking new opportunities within this evolving sector.

- Significant growth primarily driven by the electrification of vehicles and the proliferation of advanced electronics.

- Demand surge for high-performance encapsulants suitable for harsh automotive environments, including high temperatures and vibration.

- Increasing focus on thermal management properties of encapsulants due to rising power densities in electronic components.

- Emergence of Asia Pacific as a dominant region due to expanding automotive manufacturing and EV adoption.

- Strategic importance of research and development in sustainable and specialized epoxy formulations for future automotive needs.

Epoxy Encapsulant Material for Automotive Market Drivers Analysis

The global automotive industry's rapid transition towards electrification is a primary catalyst for the Epoxy Encapsulant Material for Automotive market. Electric Vehicles (EVs) and Hybrid Electric Vehicles (HEVs) inherently contain a significantly higher number of sophisticated electronic components compared to traditional internal combustion engine (ICE) vehicles, including battery packs, inverters, converters, and on-board chargers. These components demand robust protection from environmental factors such as moisture, dust, vibrations, and thermal cycling, which epoxy encapsulants are uniquely positioned to provide, ensuring their operational reliability and extending their lifespan.

Additionally, the burgeoning adoption of Advanced Driver-Assistance Systems (ADAS) and the progression towards autonomous driving further amplify the demand for high-performance encapsulants. ADAS features like adaptive cruise control, lane-keeping assist, and automatic emergency braking rely on an array of sensors, cameras, and radar units that must function flawlessly under diverse conditions. Encapsulants offer vital protection to these sensitive electronic modules, preventing failures due to physical stress, thermal shock, or moisture ingress, thereby underpinning the safety and efficacy of these critical automotive technologies.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Surge in Electric Vehicle (EV) and Hybrid Electric Vehicle (HEV) Production | +2.5% | Global, particularly Asia Pacific, Europe, North America | Short to Long-term (2025-2033) |

| Increasing Adoption of Advanced Driver-Assistance Systems (ADAS) | +2.0% | Global, particularly Developed Markets | Short to Mid-term (2025-2029) |

| Miniaturization and Integration of Automotive Electronics | +1.5% | Global | Mid-term (2027-2033) |

| Stricter Automotive Safety and Reliability Standards | +1.0% | Global | Ongoing |

Epoxy Encapsulant Material for Automotive Market Restraints Analysis

Despite the robust growth drivers, the Epoxy Encapsulant Material for Automotive market faces notable restraints, primarily concerning raw material price volatility and the complexities associated with their processing. The primary raw materials for epoxy resins, such as epichlorohydrin and bisphenol A, are petroleum-derived, making their prices susceptible to fluctuations in crude oil markets and geopolitical instability. This volatility can directly impact the manufacturing costs of encapsulants, potentially leading to higher end-product prices and impacting profit margins for manufacturers within the automotive supply chain.

Furthermore, the high precision and specialized equipment required for processing epoxy encapsulants, particularly for advanced automotive applications, can pose a significant barrier. Achieving optimal thermal management, dielectric strength, and mechanical properties often necessitates precise mixing ratios, controlled curing temperatures, and specialized dispensing equipment. These stringent processing requirements can increase manufacturing complexity, lead to higher operational costs, and limit the scalability of production, especially for smaller or emerging players in the market.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility in Raw Material Prices (e.g., petroleum derivatives) | -1.2% | Global | Short to Mid-term (2025-2028) |

| Complexities in Processing and Curing Techniques | -0.8% | Global | Ongoing |

| Competition from Alternative Encapsulation Materials | -0.7% | Global | Mid to Long-term (2027-2033) |

| Thermal Management Challenges for High-Power Components | -0.5% | Global | Ongoing |

Epoxy Encapsulant Material for Automotive Market Opportunities Analysis

Significant opportunities exist in the Epoxy Encapsulant Material for Automotive market, particularly in the development of advanced formulations tailored for specific, high-growth applications. The continuous innovation in electric vehicle battery technology, including solid-state batteries and improved thermal management systems, creates a fertile ground for novel epoxy encapsulants that can provide enhanced thermal conductivity, improved fire retardancy, and superior mechanical protection. These advancements will be crucial for improving battery safety, extending lifespan, and optimizing overall EV performance, offering a substantial avenue for market expansion.

Furthermore, the increasing complexity of infotainment systems, connectivity modules, and sensor arrays in next-generation vehicles presents additional avenues for growth. As vehicles become more akin to mobile computing platforms, the demand for reliable and durable encapsulation of these sophisticated electronic units intensifies. Opportunities lie in developing low-dielectric-constant encapsulants for high-frequency communication modules, transparent encapsulants for optical sensors, and highly flexible materials for bendable electronic circuits, aligning with the industry's drive towards integrated and seamless user experiences within the vehicle cabin.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Advanced Thermal Management Encapsulants for EV Batteries | +1.8% | Global | Short to Mid-term (2025-2030) |

| Growth in Autonomous Vehicle Sensor & LiDAR Encapsulation | +1.5% | North America, Europe, Asia Pacific (e.g., China, Japan) | Mid to Long-term (2027-2033) |

| Demand for Sustainable and Bio-based Epoxy Resins | +1.0% | Europe, North America | Mid to Long-term (2028-2033) |

| Expansion in Automotive LED Lighting Encapsulation | +0.8% | Global | Short to Mid-term (2025-2029) |

Epoxy Encapsulant Material for Automotive Market Challenges Impact Analysis

The Epoxy Encapsulant Material for Automotive market faces significant challenges, particularly related to meeting stringent performance requirements for thermal management and long-term durability in increasingly demanding automotive environments. Modern automotive electronics, especially in EVs and ADAS, generate substantial heat, requiring encapsulants with exceptionally high thermal conductivity to dissipate heat efficiently and prevent component failure. Developing cost-effective epoxy formulations that can consistently achieve these advanced thermal properties while maintaining other crucial characteristics like mechanical strength and chemical resistance remains a complex engineering hurdle, impacting material selection and adoption rates.

Another critical challenge lies in ensuring the long-term reliability and aging performance of encapsulated components under harsh operating conditions, including continuous exposure to wide temperature fluctuations, high humidity, and vibration. Automotive applications demand materials that can maintain their integrity and protective properties over the vehicle's entire lifespan, often exceeding 10-15 years. Issues such as delamination, cracking, or degradation of dielectric properties over time can lead to costly recalls and compromise vehicle safety. Addressing these durability concerns requires extensive research into material science and robust validation processes, adding to development timelines and costs.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Meeting Stringent Thermal Management Requirements in EVs | -1.0% | Global | Ongoing |

| Ensuring Long-term Reliability and Durability in Harsh Environments | -0.9% | Global | Ongoing |

| High Research and Development Costs for Specialized Formulations | -0.7% | Global | Short to Mid-term (2025-2030) |

| Regulatory Compliance and Material Recyclability Concerns | -0.6% | Europe, North America, Asia Pacific | Mid-term (2027-2033) |

Epoxy Encapsulant Material for Automotive Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global Epoxy Encapsulant Material for Automotive market, offering a detailed understanding of its size, growth trajectories, and future outlook. The scope encompasses a thorough examination of market drivers, restraints, opportunities, and challenges that shape the industry landscape, alongside a detailed segmentation analysis across various types, applications, and regional markets. The report also features a competitive analysis, profiling key players and their strategic initiatives, to offer actionable insights for stakeholders and market participants.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.85 Billion |

| Market Forecast in 2033 | USD 3.61 Billion |

| Growth Rate | 8.7% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Dow Inc., Henkel AG & Co. KGaA, Shin-Etsu Chemical Co., Ltd., Sumitomo Bakelite Co., Ltd., Huntsman Corporation, ThreeBond Holdings Co., Ltd., Lord Corporation (Parker Hannifin), BASF SE, DuPont de Nemours, Inc., Mitsubishi Chemical Corporation, Axalta Coating Systems, Ashland Global Holdings Inc., Kyocera Corporation, Hitachi Chemical Co., Ltd. (Showa Denko Materials), Momentive Performance Materials Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Epoxy Encapsulant Material for Automotive market is meticulously segmented to provide a granular view of its diverse applications and material types, reflecting the industry's complex structure and varied demands. This segmentation allows for a detailed analysis of market dynamics within specific niches, identifying high-growth areas and informing strategic decisions for manufacturers and suppliers. Understanding these segments is crucial for stakeholders to tailor their product offerings and market approaches effectively.

By type, the market is broadly divided into thermosetting and thermoplastic epoxy encapsulants, each possessing distinct properties and suitable for different performance requirements. Application-wise, the market encompasses critical automotive systems such as power electronics, ADAS sensors, battery management systems, and lighting, highlighting the ubiquitous need for robust component protection across the vehicle. Further segmentation by vehicle type and end-use industry clarifies the demand landscape, differentiating between the needs of electric vehicles versus traditional ICE vehicles, and original equipment manufacturers versus the aftermarket.

- By Type: Thermosetting Epoxy Encapsulants, Thermoplastic Epoxy Encapsulants.

- By Application: Power Electronics, Battery Management Systems (BMS), On-Board Chargers (OBC), Advanced Driver-Assistance Systems (ADAS) Sensors, Infotainment Systems, Lighting Systems, Engine Control Units (ECUs), Other Electronic Components.

- By Vehicle Type: Passenger Electric Vehicles, Commercial Electric Vehicles, Hybrid Electric Vehicles, Internal Combustion Engine (ICE) Vehicles.

- By End-use Industry: Original Equipment Manufacturers (OEMs), Aftermarket.

Regional Highlights

- North America: This region demonstrates steady growth, driven by increasing adoption of electric vehicles and significant investments in autonomous driving technologies. The presence of major automotive OEMs and a strong focus on automotive electronics innovation contribute to the demand for advanced epoxy encapsulants. Stricter safety regulations and the development of charging infrastructure further bolster market expansion.

- Europe: A leading region in automotive electrification and ADAS integration, Europe exhibits a robust demand for high-performance epoxy encapsulants. Stringent environmental regulations and a strong emphasis on sustainable manufacturing practices are driving the adoption of bio-based and eco-friendly encapsulant solutions. Germany, France, and the UK are key markets within this region.

- Asia Pacific (APAC): Positioned as the largest and fastest-growing market, APAC's dominance is attributed to high automotive production volumes, particularly in China, Japan, South Korea, and India. The rapid expansion of electric vehicle manufacturing, coupled with burgeoning consumer electronics integration in vehicles, significantly fuels the demand for epoxy encapsulants. Government initiatives supporting EV adoption and local manufacturing capabilities further accelerate market growth.

- Latin America: While a developing market, Latin America shows nascent growth in automotive electronics and EV adoption, presenting future opportunities for epoxy encapsulant manufacturers. Investment in manufacturing infrastructure and increasing vehicle parc will gradually contribute to market demand.

- Middle East and Africa (MEA): The MEA region is expected to experience gradual growth, primarily driven by increasing vehicle sales and infrastructure development in key countries. The shift towards diversifying economies and investments in smart city projects may indirectly boost demand for automotive electronics and, consequently, encapsulants.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Epoxy Encapsulant Material for Automotive Market.- Dow Inc.

- Henkel AG & Co. KGaA

- Shin-Etsu Chemical Co., Ltd.

- Sumitomo Bakelite Co., Ltd.

- Huntsman Corporation

- ThreeBond Holdings Co., Ltd.

- Lord Corporation (Parker Hannifin)

- BASF SE

- DuPont de Nemours, Inc.

- Mitsubishi Chemical Corporation

- Axalta Coating Systems

- Ashland Global Holdings Inc.

- Kyocera Corporation

- Hitachi Chemical Co., Ltd. (Showa Denko Materials)

- Momentive Performance Materials Inc.

- Elantas GmbH

- Nitto Denko Corporation

- Hexion Inc.

- Sika AG

- Altana AG

Frequently Asked Questions

Analyze common user questions about the Epoxy Encapsulant Material for Automotive market and generate a concise list of summarized FAQs reflecting key topics and concerns.

The market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.7% between 2025 and 2033, driven by increased adoption of electric vehicles and advanced automotive electronics. Key drivers include the surge in Electric Vehicle (EV) and Hybrid Electric Vehicle (HEV) production, the increasing integration of Advanced Driver-Assistance Systems (ADAS), and the continuous miniaturization of automotive electronic components. AI significantly impacts the industry by enabling accelerated material discovery, optimizing manufacturing processes for efficiency, enhancing quality control through predictive analytics, and improving supply chain management for raw materials. Major challenges include meeting stringent thermal management requirements for high-power components, ensuring long-term reliability and durability in harsh automotive environments, and managing the high research and development costs for specialized formulations. Asia Pacific (APAC) currently holds the largest market share due to its high volume of automotive production, particularly in electric vehicles, and robust growth in automotive electronics manufacturing across countries like China, Japan, and South Korea.

What is the projected growth rate for the Epoxy Encapsulant Material for Automotive Market?

Which factors are primarily driving the growth of this market?

How does AI impact the Epoxy Encapsulant Material for Automotive industry?

What are the main challenges faced by the market?

Which region holds the largest market share and why?

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted