Thermal Conductive Material Market

Thermal Conductive Material Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703590 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

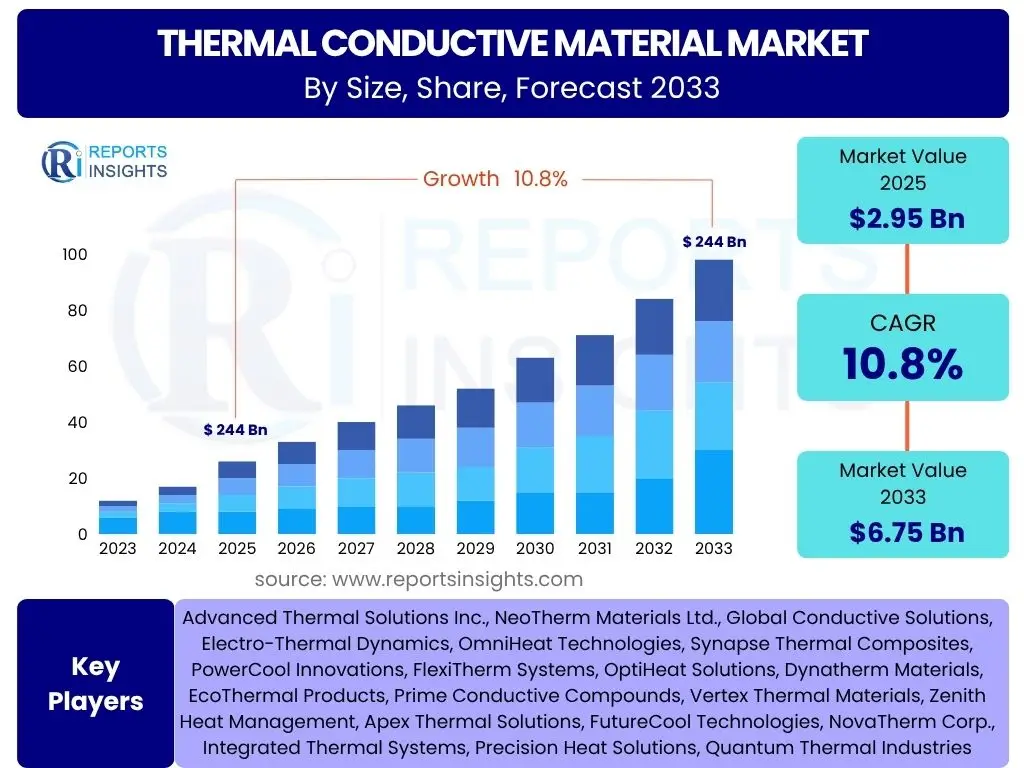

Thermal Conductive Material Market Size

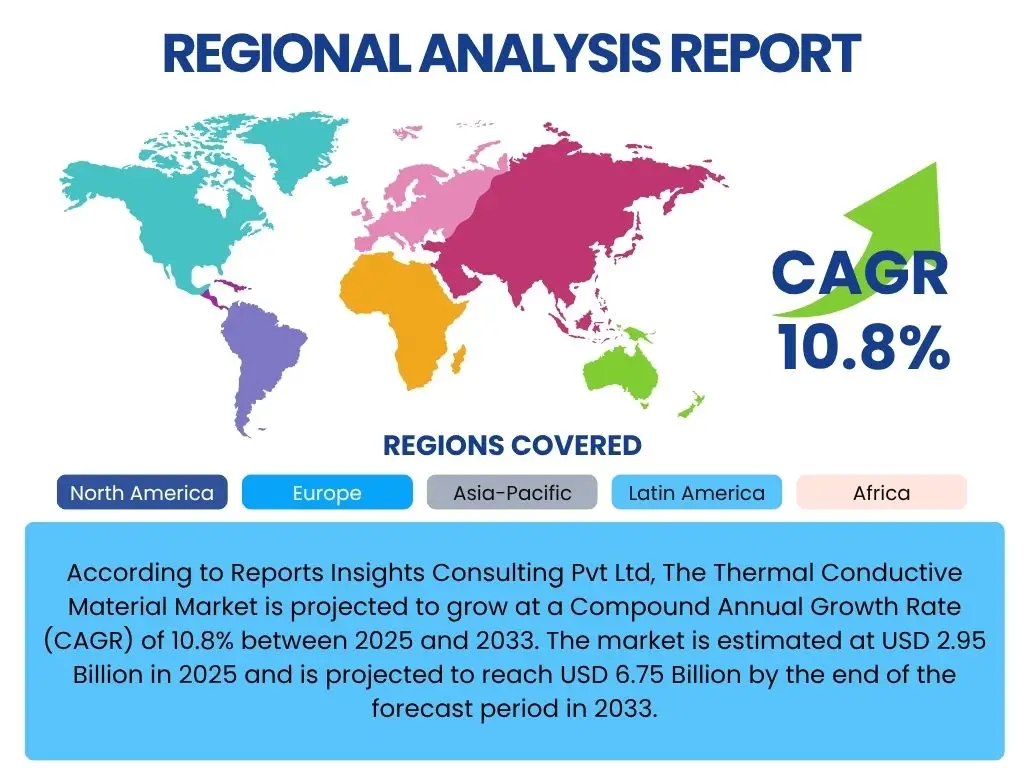

According to Reports Insights Consulting Pvt Ltd, The Thermal Conductive Material Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 10.8% between 2025 and 2033. The market is estimated at USD 2.95 Billion in 2025 and is projected to reach USD 6.75 Billion by the end of the forecast period in 2033.

Key Thermal Conductive Material Market Trends & Insights

User inquiries frequently highlight the imperative for enhanced thermal management in increasingly compact and high-performance electronic devices, reflecting a critical trend towards miniaturization and higher power densities. There is significant interest in how evolving technological landscapes, such as the rollout of 5G infrastructure and the proliferation of electric vehicles, are shaping demand for advanced thermal conductive materials. Furthermore, questions arise regarding the adoption of novel materials and eco-friendly solutions, underscoring a shift towards sustainable and efficient thermal management practices.

The market is witnessing a strong drive towards materials with superior thermal conductivity, lower thermal resistance, and improved mechanical properties, which are essential for managing heat dissipation in next-generation electronics. This trend is particularly evident in applications requiring stable performance under demanding conditions, such as automotive power electronics and high-frequency communication systems. The integration of thermal solutions earlier in the design phase is also becoming a standard practice, moving beyond traditional heat sinks to incorporate advanced interface materials and composite structures.

- Miniaturization of electronic devices driving demand for ultra-thin, high-performance thermal interface materials.

- Increasing adoption of electric vehicles (EVs) necessitating advanced thermal management solutions for batteries and power electronics.

- Expansion of 5G infrastructure and data centers requiring efficient heat dissipation for high-density components.

- Growing emphasis on sustainable and eco-friendly thermal materials and manufacturing processes.

- Advancements in material science leading to the development of novel composites and phase change materials.

- Integration of thermal management solutions early in product design for optimal performance and reliability.

AI Impact Analysis on Thermal Conductive Material

Common user questions regarding AI's impact on the thermal conductive material market primarily revolve around how artificial intelligence can optimize material design, predict performance, and streamline manufacturing processes. Users are keen to understand if AI can accelerate the discovery of new materials with superior thermal properties, and how it might influence the demand for existing materials. The potential for AI to enhance quality control and reduce development cycles for complex thermal solutions is also a recurring theme.

AI is poised to revolutionize the thermal conductive material sector by enabling sophisticated simulations and predictive modeling that can drastically reduce the time and cost associated with material discovery and optimization. Machine learning algorithms can analyze vast datasets of material properties and performance characteristics, identifying optimal compositions and structures for specific thermal management applications. This capability is particularly valuable for designing bespoke thermal solutions for highly specialized electronic systems or for predicting material behavior under extreme operational conditions.

Beyond material design, AI's influence extends to manufacturing efficiency and quality assurance. AI-powered analytics can monitor production lines in real-time, detecting anomalies and ensuring consistent material quality, thereby minimizing waste and improving yield. Furthermore, the increasing complexity and power density of AI hardware itself, such as specialized processors for deep learning, are directly driving the demand for more effective and efficient thermal conductive materials to ensure their stable and reliable operation.

- AI-driven material discovery and design optimization accelerating the development of novel thermal conductive materials.

- Predictive modeling and simulation capabilities enhancing the efficiency of material testing and performance validation.

- Automated quality control systems in manufacturing, leveraging AI for defect detection and process optimization.

- Increased demand for high-performance thermal solutions specifically for AI hardware and data center cooling.

- AI contributing to more efficient supply chain management and inventory forecasting for thermal materials.

Key Takeaways Thermal Conductive Material Market Size & Forecast

User inquiries into key takeaways from the Thermal Conductive Material market size and forecast consistently highlight the market's robust growth trajectory, driven primarily by the relentless demand for higher performance and greater power efficiency in electronic devices across various sectors. There is keen interest in identifying the fastest-growing application areas and the regions poised for significant expansion, indicating a focus on strategic investment and market entry points. The underlying message from these questions points to a recognition that thermal management is no longer an afterthought but a critical design consideration, directly impacting device reliability and longevity.

The forecast indicates a sustained high growth rate, propelled by macro trends such as the proliferation of 5G technology, the electrification of the automotive industry, and the increasing density of data centers. These sectors demand advanced thermal solutions that can handle extreme heat loads and ensure optimal operational performance. Furthermore, the shift towards sustainable manufacturing and eco-friendly materials is influencing product development, with companies investing in R&D to meet evolving regulatory standards and consumer preferences. The market's resilience is also attributed to its diverse application base, mitigating risks associated with reliance on a single industry.

- Significant market expansion anticipated, driven by pervasive digitalization and electronics proliferation.

- Automotive and data center sectors identified as primary growth engines for advanced thermal solutions.

- Technological advancements in material science are crucial for meeting future performance demands.

- Sustainability and environmental considerations are increasingly influencing material selection and design.

- Strategic partnerships and mergers are common as companies seek to expand product portfolios and regional reach.

Thermal Conductive Material Market Drivers Analysis

The Thermal Conductive Material Market is predominantly propelled by the escalating demand for efficient heat dissipation in a wide array of electronic devices and systems. As electronic components become more compact and powerful, the generation of heat increases exponentially, necessitating advanced thermal management solutions to prevent overheating, ensure reliable operation, and extend product lifespan. This is particularly evident in high-performance computing, consumer electronics, and specialized industrial applications where failure due to thermal stress is a significant concern.

Another significant driver is the rapid global expansion of the electric vehicle (EV) market. EV batteries, motors, and power electronics generate substantial heat, requiring sophisticated thermal conductive materials to maintain optimal operating temperatures, enhance energy efficiency, and ensure safety. Similarly, the rollout of 5G networks and the proliferation of data centers are creating immense demand for effective thermal management solutions for high-density servers, base stations, and other telecommunications infrastructure. These sectors critically rely on materials that can efficiently transfer heat away from sensitive components to maintain performance and reliability.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for High-Performance Electronics | +1.8% | Asia Pacific (China, South Korea), North America, Europe | 2025-2033 |

| Growth in Electric Vehicle (EV) Adoption | +1.5% | Europe, Asia Pacific (China, Japan), North America | 2025-2033 |

| Expansion of 5G Networks and Data Centers | +1.2% | North America, Asia Pacific (China, India), Europe | 2025-2030 |

| Miniaturization of Electronic Components | +1.0% | Global, particularly consumer electronics manufacturing hubs | 2025-2033 |

| Rising Applications in LED Lighting | +0.8% | Asia Pacific, Europe | 2025-2031 |

Thermal Conductive Material Market Restraints Analysis

Despite the robust growth prospects, the Thermal Conductive Material Market faces several significant restraints that could impede its expansion. One primary challenge is the high cost associated with advanced thermal conductive materials, particularly those incorporating exotic fillers or requiring complex manufacturing processes. This elevated cost can deter widespread adoption, especially in cost-sensitive applications or emerging markets where budget constraints dictate material selection. The specialized nature of these materials often necessitates significant research and development investments, which further contributes to their premium pricing.

Another notable restraint is the volatility in the prices of raw materials, such as metals (e.g., copper, aluminum) and specific ceramics or polymers, which are integral to the composition of many thermal conductive solutions. Geopolitical instability, supply chain disruptions, and fluctuating global demand can lead to unpredictable material costs, making it difficult for manufacturers to maintain stable pricing and profit margins. Furthermore, the inherent limitations in the thermal conductivity of certain widely used, cost-effective materials can restrict their application in ultra-high performance scenarios, forcing reliance on more expensive alternatives that might not be economically viable for all projects.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Cost of Advanced Thermal Materials | -0.7% | Global, particularly emerging economies | 2025-2033 |

| Volatility in Raw Material Prices | -0.5% | Global | 2025-2030 |

| Complexity in Manufacturing Processes | -0.4% | Global, impacting specialized manufacturers | 2026-2033 |

Thermal Conductive Material Market Opportunities Analysis

The Thermal Conductive Material Market presents numerous opportunities driven by ongoing technological advancements and the emergence of new application areas. The continuous innovation in material science is paving the way for the development of novel thermal solutions with enhanced properties, such as lighter weight, greater flexibility, and superior thermal performance at extreme temperatures. This includes advancements in graphene-based materials, boron nitride, and advanced composite structures, which offer significantly improved thermal conductivity compared to traditional materials, opening doors for their integration into next-generation devices.

The burgeoning fields of wearable electronics, IoT devices, and flexible displays represent significant growth opportunities for thermal conductive materials. These applications require ultra-thin, highly flexible, and efficient thermal management solutions that can conform to irregular shapes and operate effectively in compact spaces without compromising device aesthetics or functionality. Furthermore, the growing focus on energy efficiency and sustainability across industries is creating demand for thermal materials that not only manage heat but also contribute to overall system energy savings and environmental footprint reduction, stimulating innovation in eco-friendly and recyclable thermal solutions.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Advancements in Material Science and Nanotechnology | +1.3% | Global, especially R&D intensive regions | 2025-2033 |

| Emergence of Wearable and IoT Devices | +1.0% | North America, Europe, Asia Pacific | 2026-2033 |

| Growing Demand for Sustainable Thermal Solutions | +0.9% | Europe, North America, Asia Pacific | 2025-2033 |

| Integration in Advanced Driver-Assistance Systems (ADAS) | +0.7% | North America, Europe, Asia Pacific (Japan, South Korea) | 2025-2032 |

Thermal Conductive Material Market Challenges Impact Analysis

The Thermal Conductive Material Market faces several critical challenges that require innovative solutions and strategic adaptation. One significant challenge is achieving optimal performance at extremely high or low operating temperatures, which is increasingly demanded by specialized applications in aerospace, defense, and industrial processes. Many conventional thermal materials experience degradation in performance or mechanical properties under such extreme conditions, necessitating the development of highly resilient and stable alternatives, which often come with higher manufacturing complexities and costs.

Another major challenge is the integration complexity of thermal conductive materials into various electronic assemblies and diverse product designs. Ensuring seamless adhesion, precise thickness control, and long-term reliability of thermal interfaces within compact and intricate device architectures can be difficult. This requires advanced manufacturing techniques and rigorous testing, adding to the overall cost and development time. Furthermore, the market faces intense competition from alternative cooling methods, such as liquid cooling systems and active cooling technologies, particularly in high-power applications, compelling thermal conductive material manufacturers to continuously innovate and demonstrate superior cost-effectiveness and performance benefits.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Achieving Performance at Extreme Temperatures | -0.6% | Global, particularly aerospace & industrial sectors | 2025-2033 |

| Integration Complexities in Device Design | -0.5% | Global, across all electronics industries | 2025-2030 |

| Competition from Alternative Cooling Methods | -0.4% | Global, especially in high-power applications | 2025-2033 |

Thermal Conductive Material Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global Thermal Conductive Material market, offering detailed insights into market dynamics, segmentation, competitive landscape, and regional outlook. It covers key trends, drivers, restraints, opportunities, and challenges influencing market growth, with a forward-looking forecast up to 2033. The scope includes an assessment of AI's impact, a breakdown by material type, application, and end-use industry, alongside profiles of leading market participants to provide a holistic understanding of the market's current state and future potential.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 2.95 Billion |

| Market Forecast in 2033 | USD 6.75 Billion |

| Growth Rate | 10.8% |

| Number of Pages | 265 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Advanced Thermal Solutions Inc., NeoTherm Materials Ltd., Global Conductive Solutions, Electro-Thermal Dynamics, OmniHeat Technologies, Synapse Thermal Composites, PowerCool Innovations, FlexiTherm Systems, OptiHeat Solutions, Dynatherm Materials, EcoThermal Products, Prime Conductive Compounds, Vertex Thermal Materials, Zenith Heat Management, Apex Thermal Solutions, FutureCool Technologies, NovaTherm Corp., Integrated Thermal Systems, Precision Heat Solutions, Quantum Thermal Industries |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Thermal Conductive Material Market is extensively segmented across various dimensions to provide a granular understanding of its composition and growth drivers. These segments include classifications by material type, such as thermal grease, pads, adhesives, and more advanced phase change materials, reflecting the diverse range of solutions available for heat management. Further segmentation by application highlights the key industries leveraging these materials, including consumer electronics, automotive, LED lighting, and telecommunications, each with unique thermal performance requirements. The market is also analyzed by the form in which these materials are supplied and by end-use industries, providing a comprehensive view of market demand patterns.

Each segment presents distinct growth dynamics and technological preferences. For instance, the consumer electronics segment is driven by the need for miniaturization and high power density, favoring thin and efficient thermal interface materials. In contrast, the automotive sector demands materials with high durability and reliability under harsh environmental conditions for electric vehicle battery and power electronics thermal management. Understanding these segment-specific nuances is crucial for identifying targeted opportunities and developing tailored product strategies that address the precise thermal challenges of different industry verticals.

- By Type:

- Thermal Grease & Pastes: Commonly used for their ease of application and excellent gap-filling capabilities.

- Thermal Pads & Gaskets: Preferred for consistent thickness, non-wetting properties, and electrical isolation.

- Thermal Adhesives & Tapes: Offer bonding capabilities in addition to thermal conductivity, simplifying assembly.

- Phase Change Materials (PCMs): Provide enhanced thermal management by absorbing and releasing latent heat.

- Gap Fillers: Used for irregular surfaces, offering compliance and effective heat transfer across gaps.

- Encapsulants: Protect sensitive components while providing thermal dissipation.

- Metallic Materials (Copper, Aluminum, Graphite): High thermal conductivity for heat spreaders and heat sinks.

- Ceramic Materials (Alumina, Aluminum Nitride): Offer electrical insulation combined with good thermal conductivity.

- Polymer Matrix Composites: Engineered for specific thermal and mechanical properties.

- By Application:

- Consumer Electronics: Smartphones, laptops, gaming consoles, tablets, and wearables.

- Automotive Electronics: EV batteries, power control units, engine control units, LED headlights, infotainment systems.

- LED Lighting: High-brightness LEDs, streetlights, automotive lighting.

- Industrial Electronics: Power supplies, motor drives, automation equipment, industrial control systems.

- Telecommunications: 5G base stations, data center servers, networking equipment, optical modules.

- Medical Devices: Diagnostic equipment, imaging systems, surgical instruments.

- Aerospace & Defense: Avionics, radar systems, satellite components, thermal management for spacecraft.

- Energy: Solar inverters, wind turbine converters, power modules.

- By Form:

- Liquid: Gels, potting compounds, liquid gap fillers.

- Solid: Pads, sheets, films, pre-formed shapes.

- Paste: Compounds, non-curing greases.

- Sheet/Film: Thin thermal interface materials, graphite sheets.

- By End-Use Industry:

- Electronics & Electrical: All general electronic devices and electrical systems.

- Automotive: Vehicle manufacturing, including passenger cars and commercial vehicles.

- Telecommunications: Infrastructure and devices for communication networks.

- Industrial: Manufacturing, heavy machinery, and industrial automation.

- Aerospace & Defense: Aircraft, spacecraft, military equipment.

- Healthcare: Medical equipment and devices.

- Energy & Power: Renewable energy systems, power generation, and distribution.

Regional Highlights

- Asia Pacific: This region stands as the largest and fastest-growing market for thermal conductive materials, primarily driven by its dominance in electronics manufacturing and assembly. Countries like China, South Korea, Japan, and Taiwan are global hubs for smartphones, laptops, automotive electronics, and LED production, generating immense demand for efficient thermal solutions. The rapid expansion of 5G infrastructure and data centers, coupled with significant investments in electric vehicle manufacturing, further propels market growth in this region. Government initiatives supporting local electronics industries and technological advancements also contribute significantly to the market's dynamism.

- North America: Characterized by strong innovation in high-performance computing, advanced automotive technologies, and a robust aerospace and defense sector, North America represents a mature yet continually growing market. The region is a key adopter of advanced thermal management solutions for data centers, AI hardware, and electric vehicle components. Investments in research and development, coupled with a focus on stringent performance and reliability standards, drive the demand for premium and specialized thermal conductive materials. The presence of major technology companies and automotive manufacturers ensures sustained growth.

- Europe: The European market for thermal conductive materials is significantly influenced by its strong automotive industry, particularly in the development and production of electric vehicles, and its leadership in industrial automation and renewable energy. Countries like Germany, France, and the UK are at the forefront of adopting advanced thermal solutions for power electronics and energy-efficient systems. The region's emphasis on environmental regulations and sustainability also drives demand for eco-friendly and energy-efficient thermal management products, fostering innovation in materials and applications.

- Latin America: This region is an emerging market for thermal conductive materials, with growth driven by increasing industrialization, expanding electronics manufacturing, and developing automotive sectors, particularly in Brazil and Mexico. The rising adoption of consumer electronics and the gradual rollout of telecommunications infrastructure contribute to the demand. While smaller in market share compared to other regions, Latin America offers significant untapped potential as its economies continue to develop and industrialize.

- Middle East and Africa (MEA): The MEA region is witnessing growth in thermal conductive materials demand, primarily from investments in telecommunications infrastructure, especially the deployment of 5G networks, and the burgeoning construction of data centers. Increased focus on smart city initiatives and diversification of economies away from oil dependency are also fostering the adoption of advanced electronics, thereby driving the need for thermal management solutions. Countries like UAE and Saudi Arabia are leading these developments.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Thermal Conductive Material Market.- Advanced Thermal Solutions Inc.

- NeoTherm Materials Ltd.

- Global Conductive Solutions

- Electro-Thermal Dynamics

- OmniHeat Technologies

- Synapse Thermal Composites

- PowerCool Innovations

- FlexiTherm Systems

- OptiHeat Solutions

- Dynatherm Materials

- EcoThermal Products

- Prime Conductive Compounds

- Vertex Thermal Materials

- Zenith Heat Management

- Apex Thermal Solutions

- FutureCool Technologies

- NovaTherm Corp.

- Integrated Thermal Systems

- Precision Heat Solutions

- Quantum Thermal Industries

Frequently Asked Questions

Analyze common user questions about the Thermal Conductive Material market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the projected growth rate of the Thermal Conductive Material Market?

The Thermal Conductive Material Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 10.8% between 2025 and 2033, indicating robust expansion driven by increasing demand for efficient heat management in electronics.

Which applications are driving the demand for thermal conductive materials?

Key applications driving demand include consumer electronics miniaturization, the rapid growth of the electric vehicle (EV) sector, expansion of 5G networks and data centers, and advanced LED lighting solutions, allrequiring superior heat dissipation.

How does AI impact the thermal conductive material industry?

AI significantly impacts the industry by enabling faster material discovery, optimizing design and manufacturing processes, enhancing quality control, and driving demand for advanced thermal solutions in AI hardware and data centers.

What are the primary challenges faced by the market?

Major challenges include achieving optimal performance at extreme temperatures, managing complex integration requirements in diverse device designs, and facing competition from alternative cooling methods, necessitating continuous innovation.

Which region holds the largest market share and why?

Asia Pacific holds the largest market share due to its dominant position in global electronics manufacturing, extensive 5G deployment, significant investments in EV production, and rapid industrialization across countries like China, South Korea, and Japan.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted