Endpoint Security Market

Endpoint Security Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703252 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

Endpoint Security Market Size

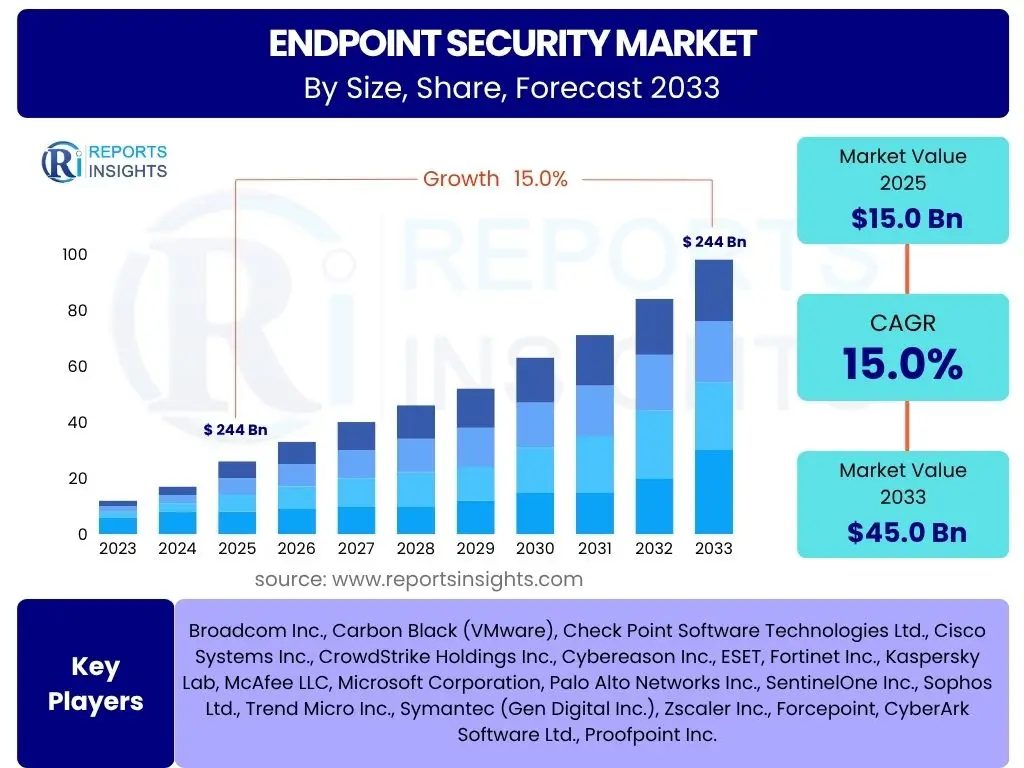

According to Reports Insights Consulting Pvt Ltd, The Endpoint Security Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 15.0% between 2025 and 2033. The market is estimated at USD 15.0 Billion in 2025 and is projected to reach USD 45.0 Billion by the end of the forecast period in 2033.

Key Endpoint Security Market Trends & Insights

The endpoint security market is undergoing rapid evolution, primarily driven by the escalating sophistication of cyber threats, the widespread adoption of remote work models, and the accelerated pace of digital transformation across industries. Organizations are increasingly recognizing that traditional perimeter-based security is insufficient in a distributed environment, leading to a strong demand for advanced endpoint protection solutions that can detect and respond to threats at the device level.

A significant trend involves the shift from standalone security products to integrated platforms that offer comprehensive visibility and control. This includes the convergence of Endpoint Protection Platforms (EPP) and Endpoint Detection and Response (EDR) capabilities, often augmented with Extended Detection and Response (XDR) for broader telemetry. The focus is moving towards proactive threat hunting, behavioral analytics, and automated response mechanisms to minimize dwell time and mitigate potential damage.

Furthermore, the proliferation of Internet of Things (IoT) devices and operational technology (OT) endpoints presents new attack surfaces, necessitating specialized endpoint security approaches. Compliance requirements and data privacy regulations are also compelling enterprises to invest in robust security frameworks that ensure data integrity and confidentiality, making endpoint security a foundational component of their overall cybersecurity strategy.

- Convergence of Endpoint Protection Platforms (EPP) and Endpoint Detection and Response (EDR) into unified solutions.

- Increased adoption of Extended Detection and Response (XDR) platforms for integrated visibility across multiple security layers.

- Growing emphasis on Zero Trust Network Access (ZTNA) principles, extending least-privilege access to endpoints.

- Rise in demand for cloud-native endpoint security solutions for scalable and flexible deployment.

- Integration of advanced threat intelligence and behavioral analytics for proactive threat detection.

- Expansion of endpoint security scope to include IoT and OT environments.

- Demand for security solutions that support hybrid work models and Bring Your Own Device (BYOD) policies.

- Focus on data loss prevention (DLP) capabilities at the endpoint to comply with privacy regulations.

AI Impact Analysis on Endpoint Security

Artificial Intelligence (AI) and Machine Learning (ML) are profoundly transforming the landscape of endpoint security, enabling a paradigm shift from reactive defense to proactive threat prevention and rapid response. Users frequently inquire about AI's ability to detect novel threats, reduce false positives, and automate security operations. AI algorithms can analyze vast datasets of endpoint activity, identifying anomalies and malicious patterns that would be imperceptible to human analysts or traditional signature-based systems. This capability is crucial for combating sophisticated, polymorphic, and zero-day attacks.

AI's influence extends to enhancing predictive capabilities, allowing security solutions to anticipate potential threats based on evolving attack trends and historical data. This leads to more intelligent threat prioritization and resource allocation. While AI significantly boosts efficiency and accuracy, concerns exist regarding adversarial AI, where attackers employ AI to evade detection, and the potential for AI models to inherit biases or generate false positives if not properly trained and monitored. The industry is actively working on explainable AI (XAI) to build trust and transparency in AI-driven security decisions.

The integration of AI also facilitates the automation of routine security tasks, such as incident triage, vulnerability management, and policy enforcement, thereby freeing up security analysts to focus on more complex strategic challenges. This automation is vital in addressing the persistent cybersecurity talent gap and improving the scalability of security operations. Overall, AI is positioned as a critical enabler for next-generation endpoint security, offering unparalleled capabilities for threat detection, response, and operational efficiency.

- Enhanced threat detection and identification of zero-day exploits through behavioral analytics and anomaly detection.

- Reduced false positives by intelligently differentiating between benign and malicious activities.

- Automated incident response, enabling quicker containment and remediation of threats.

- Predictive threat intelligence, anticipating future attacks based on learned patterns.

- Improved vulnerability management through AI-driven prioritization of patches and security configurations.

- Optimization of security operations by automating routine tasks and reducing manual effort.

- Emergence of adversarial AI techniques, posing new challenges for AI-driven defense systems.

- Continuous learning and adaptation of security models to evolving threat landscapes.

Key Takeaways Endpoint Security Market Size & Forecast

The endpoint security market is poised for robust and sustained growth throughout the forecast period, driven by an ever-intensifying cyber threat landscape and the imperative for organizations to protect their diverse digital assets. The projected Compound Annual Growth Rate (CAGR) underscores a significant expansion, reflecting the foundational role endpoint protection plays in modern cybersecurity strategies. Key questions from users often center on the primary growth catalysts and the longevity of this market expansion.

A critical takeaway is the shift towards comprehensive, integrated security solutions that offer advanced threat detection, rapid response, and proactive threat hunting capabilities. Simply preventing malware is no longer sufficient; enterprises require solutions that can identify sophisticated, file-less, and insider threats. This market evolution is further accelerated by the widespread adoption of cloud computing, remote work models, and the proliferation of IoT devices, all of which expand the attack surface and necessitate robust endpoint controls.

The forecasted growth highlights significant investment opportunities for solution providers developing innovative AI/ML-driven security technologies and for organizations looking to fortify their defenses. Strategic alliances, mergers, and acquisitions are anticipated as companies seek to expand their portfolios and market reach. The market's resilience and consistent growth trajectory are clear indicators of its critical importance in safeguarding digital infrastructures globally.

- Endpoint security market projected for strong double-digit CAGR from 2025 to 2033, reaching substantial market valuation.

- Growth is primarily fueled by increasing sophistication of cyber threats, expansion of attack surfaces, and stringent regulatory compliance.

- Shift towards integrated, AI-driven EPP and EDR solutions, with a focus on proactive threat hunting and automated response.

- Significant opportunities exist in cloud-native solutions, IoT security, and the integration of Zero Trust principles.

- Market expansion is global, with particularly high growth rates anticipated in emerging economies.

Endpoint Security Market Drivers Analysis

The endpoint security market's robust growth is propelled by several critical factors that have amplified the need for comprehensive protection at the device level. The pervasive digital transformation initiatives across industries have led to an explosion in connected devices, from traditional laptops and smartphones to IoT and OT endpoints, each representing a potential entry point for attackers. This expanded attack surface necessitates robust and adaptive endpoint defenses. Concurrently, the increasing sophistication and volume of cyber-attacks, including ransomware, phishing, and advanced persistent threats, create an urgent demand for solutions capable of detecting and mitigating these evolving threats.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Sophistication of Cyber Threats and Attacks | +3.5% | Global | 2025-2033 |

| Proliferation of Remote Work and Hybrid Work Models | +2.8% | North America, Europe, APAC | 2025-2030 |

| Growing Adoption of Cloud-Based Solutions and Digital Transformation | +2.5% | Global | 2025-2033 |

| Strict Regulatory Compliance and Data Privacy Mandates | +2.0% | Europe (GDPR), North America (CCPA), APAC | 2025-2033 |

| Rise in Endpoint Devices (BYOD, IoT, OT) | +1.5% | Global | 2025-2033 |

Endpoint Security Market Restraints Analysis

Despite significant growth drivers, the endpoint security market faces several restraints that could impede its expansion. One primary challenge is the high cost associated with implementing, maintaining, and continuously updating advanced endpoint security solutions. This is particularly burdensome for small and medium-sized enterprises (SMEs) with limited IT budgets and resources. The complexity of integrating new endpoint security solutions with existing IT infrastructures and legacy systems also poses a significant hurdle, leading to deployment challenges and potential operational disruptions.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Cost of Implementation and Maintenance | -2.0% | Global, particularly SMEs | 2025-2033 |

| Complexity of Managing Diverse Endpoint Environments | -1.5% | Global | 2025-2030 |

| Lack of Skilled Cybersecurity Professionals | -1.2% | Global | 2025-2033 |

| Integration Challenges with Legacy Systems | -1.0% | Developed Regions | 2025-2030 |

| Increased Alert Fatigue and False Positives | -0.8% | Global | 2025-2028 |

Endpoint Security Market Opportunities Analysis

The endpoint security market presents substantial opportunities for innovation and growth, driven by emerging technological advancements and evolving enterprise needs. A significant opportunity lies in the continued integration of Artificial Intelligence (AI) and Machine Learning (ML) to enhance threat detection, automate responses, and provide predictive insights, moving beyond traditional signature-based methods. The accelerating adoption of cloud-native architectures creates a demand for cloud-based endpoint security solutions that offer scalability, flexibility, and simplified management, catering to organizations transitioning their infrastructure to the cloud.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Integration of AI/ML and Automation in Endpoint Solutions | +3.0% | Global | 2025-2033 |

| Growing Demand for Unified Security Platforms (XDR, SASE) | +2.5% | North America, Europe | 2025-2033 |

| Expansion into Emerging Markets and Untapped Sectors | +2.0% | APAC, Latin America, MEA | 2025-2033 |

| Development of Specialized IoT and OT Endpoint Security | +1.8% | Global | 2025-2033 |

| Rise in Managed Security Service Provider (MSSP) Offerings | +1.5% | Global, particularly SMEs | 2025-2033 |

Endpoint Security Market Challenges Impact Analysis

The endpoint security market faces several inherent challenges that demand continuous innovation and strategic adaptation from solution providers and organizations. The primary challenge is the relentlessly evolving and increasingly sophisticated cyber threat landscape, including advanced persistent threats (APTs), file-less malware, and polymorphic viruses, which often bypass traditional signature-based defenses. This necessitates constant updates and integration of advanced detection techniques. Another significant challenge is securing the vast and diverse array of endpoints, which now include not only traditional laptops and desktops but also mobile devices, IoT sensors, and operational technology (OT) systems, each with unique vulnerabilities and management complexities.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapidly Evolving and Sophisticated Threat Landscape | -2.5% | Global | 2025-2033 |

| Securing Diverse and Distributed Endpoints (IoT, Cloud) | -2.0% | Global | 2025-2033 |

| Balancing Security Effectiveness with User Experience | -1.5% | Global | 2025-2030 |

| Budget Constraints and Resource Limitations for SMEs | -1.2% | Global | 2025-2033 |

| Cybersecurity Talent Shortage and Skill Gap | -1.0% | Global | 2025-2033 |

Endpoint Security Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global Endpoint Security Market, covering historical data from 2019 to 2023, current market estimates for 2024, and future projections from 2025 to 2033. It offers insights into market size, growth drivers, restraints, opportunities, and challenges, alongside a detailed segmentation analysis by component, deployment, organization size, and industry vertical. The report also highlights regional dynamics and profiles key players shaping the competitive landscape.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 15.0 Billion |

| Market Forecast in 2033 | USD 45.0 Billion |

| Growth Rate | 15.0% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Broadcom Inc., Carbon Black (VMware), Check Point Software Technologies Ltd., Cisco Systems Inc., CrowdStrike Holdings Inc., Cybereason Inc., ESET, Fortinet Inc., Kaspersky Lab, McAfee LLC, Microsoft Corporation, Palo Alto Networks Inc., SentinelOne Inc., Sophos Ltd., Trend Micro Inc., Symantec (Gen Digital Inc.), Zscaler Inc., Forcepoint, CyberArk Software Ltd., Proofpoint Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Endpoint Security Market is comprehensively segmented to provide a granular understanding of its diverse components and applications across various sectors. This segmentation highlights key growth areas and varying adoption patterns based on technological preferences, deployment models, organizational scale, and specific industry requirements. Analyzing these segments helps identify niche opportunities and tailor solutions to address distinct market needs, reflecting the market's complexity and dynamism.

The "By Component" segmentation differentiates between various types of solutions and accompanying services, illustrating the shift towards integrated platforms and the increasing reliance on managed security offerings. "By Deployment" distinguishes between on-premise and cloud-based solutions, reflecting the industry's strong move towards cloud adoption. "By Organization Size" highlights the distinct security needs and budget considerations of SMEs versus large enterprises, while "By Industry Vertical" showcases the varied threat landscapes and compliance demands across different economic sectors. This detailed breakdown facilitates targeted market strategies and product development.

- By Component: This segment includes a wide array of solutions such as Endpoint Protection Platforms (EPP), Endpoint Detection and Response (EDR), Data Loss Prevention (DLP), Network Access Control (NAC), Unified Endpoint Management (UEM), Mobile Threat Defense (MTD), Cloud Access Security Broker (CASB), encryption tools, firewalls, anti-malware, antivirus software, and vulnerability management systems. It also covers crucial services like Managed Security Services and Professional Services, which support the implementation and ongoing management of these solutions.

- By Deployment: Divided into On-Premise deployments, where software is installed and managed locally, and Cloud-Based (SaaS) solutions, which offer greater scalability, accessibility, and reduced infrastructure overhead.

- By Organization Size: Categorizes the market based on the scale of businesses, distinguishing between Small and Medium-sized Enterprises (SMEs) and Large Enterprises, each with unique security budgets, infrastructure complexities, and threat profiles.

- By Industry Vertical: Encompasses various sectors including Banking, Financial Services, and Insurance (BFSI), IT & Telecom, Healthcare, Government & Public Sector, Retail & E-commerce, Manufacturing, Energy & Utilities, Education, and Other industries, reflecting the tailored security needs of each domain.

Regional Highlights

- North America: Expected to hold the largest market share due to the early adoption of advanced security technologies, the presence of major cybersecurity vendors, and stringent regulatory frameworks like HIPAA and CCPA. High incidence of cyber-attacks also drives demand.

- Europe: Characterized by strong regulatory compliance (e.g., GDPR, NIS Directive) driving robust cybersecurity investments. Significant focus on data privacy and sovereign cloud solutions.

- Asia Pacific (APAC): Projected to exhibit the highest growth rate owing to rapid digital transformation, increasing internet penetration, growing cyber threat landscape, and rising awareness about cybersecurity among SMEs and large enterprises. Countries like China, India, and Japan are key contributors.

- Latin America: Emerging market with increasing adoption of cloud services and digital payments, leading to a rising need for endpoint protection. Economic development and growing cybersecurity awareness are key growth factors.

- Middle East and Africa (MEA): Growth driven by government initiatives to digitize public services, increasing investment in critical infrastructure, and rising awareness of cyber threats. Cybersecurity spending is increasing across key sectors like oil & gas, finance, and telecommunications.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Endpoint Security Market.- Broadcom Inc.

- Carbon Black (VMware)

- Check Point Software Technologies Ltd.

- Cisco Systems Inc.

- CrowdStrike Holdings Inc.

- Cybereason Inc.

- ESET

- Fortinet Inc.

- Kaspersky Lab

- McAfee LLC

- Microsoft Corporation

- Palo Alto Networks Inc.

- SentinelOne Inc.

- Sophos Ltd.

- Trend Micro Inc.

- Symantec (Gen Digital Inc.)

- Zscaler Inc.

- Forcepoint

- CyberArk Software Ltd.

- Proofpoint Inc.

Frequently Asked Questions

Analyze common user questions about the Endpoint Security market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is endpoint security?

Endpoint security refers to the practice of securing endpoint devices such as laptops, desktops, mobile phones, and servers from cybersecurity threats. It protects these devices and the networks they connect to from malware, phishing attacks, ransomware, and other cyber threats, acting as the last line of defense.

Why is endpoint security important in today's digital landscape?

Endpoint security is crucial because endpoints are often the primary entry points for cyber-attacks. With the rise of remote work, cloud adoption, and BYOD policies, traditional network perimeters have diminished, making robust endpoint protection essential to safeguard sensitive data and prevent unauthorized access or system compromise.

How does AI impact endpoint security solutions?

AI significantly enhances endpoint security by enabling advanced threat detection through behavioral analysis, reducing false positives, and automating incident response. AI algorithms can identify unknown threats, zero-day exploits, and sophisticated attacks that signature-based methods might miss, improving overall security posture and operational efficiency.

What are the key trends shaping the endpoint security market?

Key trends include the convergence of EPP and EDR functionalities, the increasing adoption of XDR for unified visibility, the shift towards cloud-native security platforms, the integration of Zero Trust Network Access (ZTNA) principles, and a growing focus on securing IoT and OT endpoints due to their expanding presence.

What are the primary challenges in implementing endpoint security?

Major challenges involve the high cost of advanced solutions, the complexity of managing diverse endpoint environments, the persistent shortage of skilled cybersecurity professionals, integration difficulties with legacy IT systems, and the constant need to adapt to a rapidly evolving and sophisticated threat landscape.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted