Defense Cyber Security Market

Defense Cyber Security Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703403 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

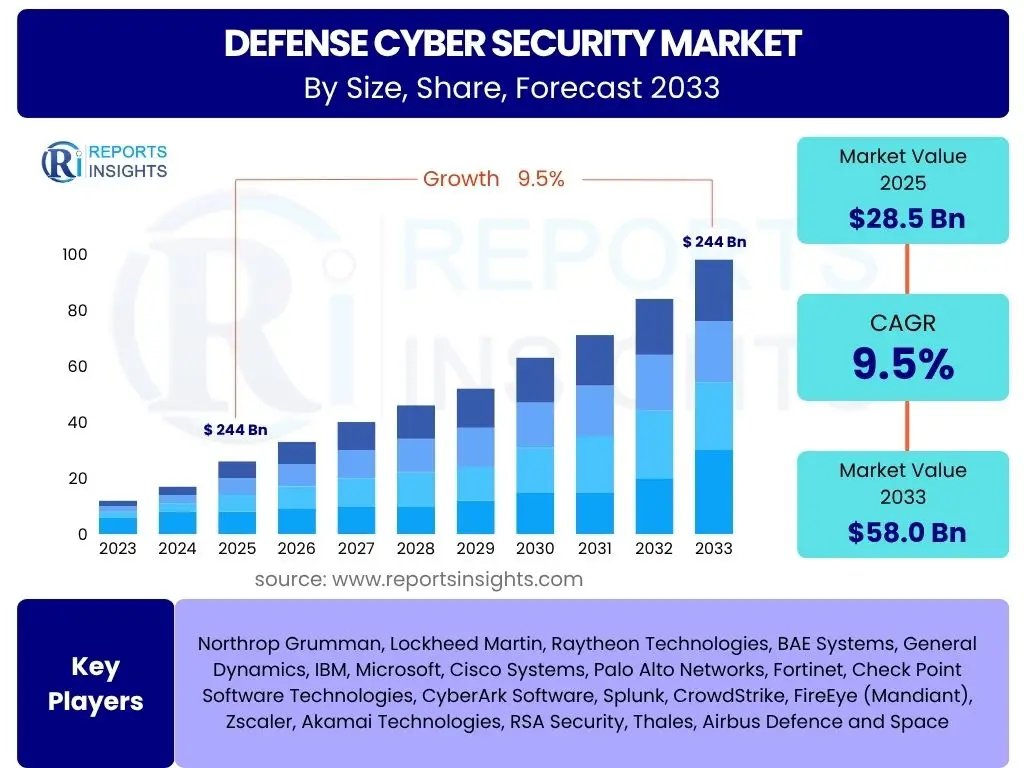

Defense Cyber Security Market Size

According to Reports Insights Consulting Pvt Ltd, The Defense Cyber Security Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.5% between 2025 and 2033. The market is estimated at USD 28.5 billion in 2025 and is projected to reach USD 58.0 billion by the end of the forecast period in 2033.

Key Defense Cyber Security Market Trends & Insights

User inquiries frequently revolve around the evolving nature of cyber threats, the increasing sophistication of state-sponsored attacks, and the imperative for defense organizations to adopt proactive and resilient cybersecurity postures. There is a clear interest in understanding how geopolitical tensions translate into cyber warfare strategies and the impact of emerging technologies on traditional defense frameworks. Furthermore, the emphasis on supply chain security and the integration of cybersecurity at every operational level are frequently highlighted themes, underscoring a shift towards a more holistic security approach.

Another significant area of user concern relates to the integration of advanced analytics, artificial intelligence, and machine learning into cybersecurity solutions. Users are keen to know how these technologies are enhancing threat detection, response capabilities, and predictive analysis within the defense sector. The ongoing talent gap in specialized cybersecurity skills and the need for continuous training and development are also recurring points of interest, reflecting a critical challenge in maintaining effective cyber defenses amidst a rapidly changing threat landscape.

- Proliferation of Advanced Persistent Threats (APTs) and state-sponsored cyber warfare.

- Increased adoption of zero-trust architectures across defense networks.

- Growing emphasis on supply chain cybersecurity and software bill of materials (SBOMs).

- Integration of Artificial Intelligence (AI) and Machine Learning (ML) for enhanced threat detection and autonomous response.

- Development of quantum-safe cryptography to counter future quantum computing threats.

- Expansion of cloud-based security solutions for defense data and applications.

AI Impact Analysis on Defense Cyber Security

Common user questions regarding AI's impact on defense cybersecurity center on its dual nature: both as a powerful tool for defense and a potent weapon for adversaries. Users seek to understand how AI can enhance threat intelligence, automate incident response, and identify novel attack patterns that evade traditional security measures. There is considerable interest in AI's role in predictive analysis, allowing defense organizations to anticipate and neutralize threats before they materialize, and in optimizing resource allocation for cybersecurity operations.

Conversely, significant concerns are raised about the potential for AI-powered offensive capabilities, such as automated vulnerability exploitation, sophisticated social engineering, and the creation of highly realistic deepfakes for disinformation campaigns. Users are also apprehensive about the ethical implications of autonomous decision-making in cyber warfare and the challenges of securing AI systems themselves from adversarial attacks. The need for robust AI governance frameworks and explainable AI (XAI) in defense applications is a recurring theme.

- Enhanced threat detection and analysis through AI-driven anomaly identification and behavioral analytics.

- Automated incident response and remediation, significantly reducing reaction times.

- Predictive threat intelligence, leveraging AI to forecast attack vectors and adversary tactics.

- Optimization of security operations and resource allocation through AI-powered insights.

- Development of AI-powered offensive tools by adversaries, increasing attack sophistication.

- Challenges in securing AI models from adversarial machine learning attacks (e.g., data poisoning, model evasion).

- Ethical considerations and governance frameworks for autonomous AI in defense contexts.

Key Takeaways Defense Cyber Security Market Size & Forecast

The core insights derived from the Defense Cyber Security market size and forecast consistently highlight a period of sustained and robust growth, driven by an escalating global threat landscape. Users frequently ask about the primary drivers behind this expansion, with the increasing sophistication of cyber warfare, rising defense budgets allocated to cybersecurity, and the pervasive digital transformation across military operations being central themes. The market's resilience against economic fluctuations underscores its criticality as a national security imperative, rather than a discretionary expenditure.

Another key takeaway is the imperative for defense entities to move beyond reactive security measures towards a proactive, threat-informed defense posture. This involves continuous investment in advanced technologies such as AI, quantum-safe solutions, and zero-trust architectures. The forecast also emphasizes the growing importance of public-private partnerships and international collaboration to share intelligence and develop resilient, interoperable cyber defenses, reflecting a collective recognition that cyber threats transcend national borders.

- The market exhibits sustained strong growth, fueled by increasing geopolitical tensions and advanced cyber threats.

- Significant investment is being channeled into AI, quantum computing defense, and supply chain security.

- Defense organizations are rapidly adopting zero-trust frameworks to enhance network resilience.

- A shift towards proactive defense strategies and continuous threat intelligence is becoming standard.

- International collaboration and public-private partnerships are crucial for effective cyber defense.

Defense Cyber Security Market Drivers Analysis

The defense cyber security market is profoundly influenced by a confluence of geopolitical and technological drivers. The escalating frequency and sophistication of state-sponsored cyber attacks and cyber warfare are primary catalysts, compelling nations to significantly bolster their digital defenses to protect critical infrastructure, intelligence assets, and military operations. Furthermore, the pervasive digital transformation across all branches of the armed forces, encompassing networked combat systems, cloud adoption, and IoT integration, inherently expands the attack surface, thereby necessitating robust cybersecurity solutions.

Increased national defense budgets, often with specific allocations for cyber capabilities, coupled with stringent regulatory requirements for data protection and operational resilience, provide significant impetus for market growth. The imperative to safeguard sensitive military intelligence, ensure operational continuity, and maintain information superiority in modern conflict zones further solidifies the demand for advanced defense cyber security solutions, driving innovation and adoption across the sector.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Escalating Cyber Warfare and State-Sponsored Attacks | +1.2% | Global, particularly North America, Europe, Asia Pacific | Short to Long-term |

| Rapid Digital Transformation in Defense Sector | +0.9% | Global, especially US, UK, China, India | Medium to Long-term |

| Increased Defense Budget Allocations for Cybersecurity | +0.8% | North America, Europe, Middle East | Short to Medium-term |

| Growing Adoption of Cloud and IoT in Military Operations | +0.7% | Global | Medium-term |

| Stringent Regulatory Compliance and Data Protection Directives | +0.6% | Europe (GDPR), US (NIST), Asia Pacific | Short to Medium-term |

Defense Cyber Security Market Restraints Analysis

Despite robust growth drivers, the defense cyber security market faces several significant restraints that can impede its expansion. One prominent challenge is the persistent issue of budgetary constraints, particularly in smaller defense economies or during periods of fiscal austerity. While cybersecurity is critical, it often competes with other essential defense expenditures, leading to prioritization dilemmas and potentially slower adoption of cutting-edge technologies.

Another key restraint is the acute shortage of highly skilled cybersecurity professionals within defense organizations. The specialized nature of military cyber operations requires a unique blend of technical expertise and strategic understanding, which is difficult to recruit and retain amidst fierce competition from the private sector. Furthermore, the inherent complexity of integrating new, advanced cybersecurity solutions with existing legacy IT infrastructure, which is prevalent in many defense environments, can lead to significant technical hurdles, prolonged deployment times, and interoperability issues, thereby slowing market progression.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Shortage of Skilled Cybersecurity Professionals | -0.8% | Global, particularly North America, Europe | Long-term |

| Integration Complexities with Legacy IT Systems | -0.6% | Global, especially mature defense markets | Medium-term |

| Budgetary Constraints and Procurement Cycles | -0.5% | Global, varying by economic stability | Short to Medium-term |

| Ethical and Legal Hurdles of Autonomous Systems | -0.3% | Global, particularly Western nations | Long-term |

| Over-reliance on Traditional Security Approaches | -0.4% | Global, particularly less agile defense organizations | Medium-term |

Defense Cyber Security Market Opportunities Analysis

Significant opportunities abound in the defense cyber security market, driven by the continuous evolution of technology and the imperative for enhanced national security. The emergence of quantum computing presents a dual challenge and opportunity; the need for quantum-safe cryptography to secure future communications and data offers a substantial new market segment for innovative solutions providers. Similarly, the increasing adoption of cloud services and the expansion of the Internet of Military Things (IoMT) within defense operations create a burgeoning demand for specialized cloud security and IoT security solutions tailored to military-grade requirements.

The growing emphasis on advanced analytics, Artificial Intelligence, and Machine Learning for predictive threat intelligence, automated response, and anomaly detection also represents a fertile ground for market expansion. Furthermore, the increasing recognition of supply chain vulnerabilities highlights a critical need for robust vendor risk management and software supply chain integrity solutions. International collaboration and information sharing initiatives among allied nations also open doors for joint ventures, cross-border technology transfer, and the development of interoperable cyber defense frameworks, fostering global market growth.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Quantum-Safe Cryptography Solutions | +1.0% | Global, particularly leading technological nations | Long-term |

| Expansion of Cloud and Internet of Military Things (IoMT) Security | +0.9% | Global | Medium to Long-term |

| Increased Demand for Advanced Analytics and AI/ML Security | +0.8% | Global | Short to Medium-term |

| Focus on Supply Chain Cybersecurity and Vendor Risk Management | +0.7% | Global, especially critical infrastructure nations | Short to Medium-term |

| Growing International Collaboration and Intelligence Sharing | +0.6% | North America, Europe, Asia Pacific alliances | Medium-term |

Defense Cyber Security Market Challenges Impact Analysis

The defense cyber security market is continually navigating a complex landscape of challenges that demand agile and innovative responses. The most formidable challenge is the persistently evolving nature of the cyber threat landscape, characterized by increasingly sophisticated attack vectors, polymorphic malware, and zero-day exploits. Adversaries, particularly state-sponsored groups, constantly adapt their tactics, techniques, and procedures (TTPs), making it difficult for defense systems to keep pace and requiring continuous investment in research and development.

Another critical challenge is the pervasive vulnerability of global supply chains. Defense organizations rely on a vast network of third-party vendors for hardware, software, and services, each representing a potential point of entry for malicious actors. Ensuring the integrity and security of this intricate ecosystem is complex and resource-intensive. Furthermore, the insider threat, whether malicious or unintentional, remains a significant concern, requiring robust access controls, behavioral analytics, and comprehensive training programs to mitigate risks to sensitive information and critical systems.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapidly Evolving and Sophisticated Threat Landscape | -0.9% | Global | Continuous |

| Vulnerabilities in Global Supply Chains | -0.7% | Global, particularly nations reliant on international supply chains | Medium to Long-term |

| Insider Threats (Malicious and Accidental) | -0.6% | Global | Continuous |

| Maintaining Data Privacy and Confidentiality | -0.5% | Global, especially nations with strict privacy laws | Short to Medium-term |

| Compliance with Fragmented International Cybersecurity Regulations | -0.4% | Global, particularly multi-national operations | Medium-term |

Defense Cyber Security Market - Updated Report Scope

This market report provides an in-depth analysis of the Defense Cyber Security market, covering historical performance from 2019 to 2023 and offering a comprehensive forecast from 2025 to 2033. It details market size estimations, projected growth rates, and a thorough segmentation across various components, types, deployment models, applications, and end-users. The report also highlights key market trends, analyzes drivers, restraints, opportunities, and challenges, and profiles leading market participants to provide a holistic view of the industry landscape. It serves as a vital resource for strategic planning and informed decision-making within the defense sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 28.5 Billion |

| Market Forecast in 2033 | USD 58.0 Billion |

| Growth Rate | 9.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Northrop Grumman, Lockheed Martin, Raytheon Technologies, BAE Systems, General Dynamics, IBM, Microsoft, Cisco Systems, Palo Alto Networks, Fortinet, Check Point Software Technologies, CyberArk Software, Splunk, CrowdStrike, FireEye (Mandiant), Zscaler, Akamai Technologies, RSA Security, Thales, Airbus Defence and Space |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Defense Cyber Security market is meticulously segmented to provide a granular understanding of its diverse components and applications. This comprehensive breakdown allows for a detailed analysis of spending patterns, technological adoption, and strategic priorities across various facets of defense operations. Understanding these segments is crucial for identifying specific growth opportunities and tailoring solutions to meet the unique security demands of different defense stakeholders.

Each segment, from the foundational components like hardware and software to specialized types of security and their deployment models, reflects distinct market dynamics and investment trends. The application and end-user segments further highlight where defense cyber security efforts are most concentrated and which entities are driving demand, enabling a precise evaluation of market potential and strategic positioning.

- By Component

- Hardware (e.g., Secure Routers, Firewalls, HSMs)

- Software (e.g., Antivirus, Encryption, SIEM, IDS/IPS, Threat Intelligence Platforms)

- Services (e.g., Managed Security Services, Consulting, Training & Education, Incident Response)

- By Type

- Network Security (e.g., VPN, Firewalls, IDS/IPS)

- Endpoint Security (e.g., Antivirus, EDR, Mobile Device Security)

- Application Security (e.g., Web Application Firewall, Code Analysis)

- Cloud Security (e.g., CASB, Cloud Workload Protection)

- Data Security (e.g., Encryption, DLP, Data Masking)

- Identity Management (e.g., IAM, PAM)

- Security Analytics (e.g., SIEM, UEBA)

- Others (e.g., Quantum Cryptography, SCADA Security)

- By Deployment

- On-Premise

- Cloud (Public, Private, Hybrid)

- Hybrid

- By Application

- Critical Infrastructure Protection (e.g., Energy Grids, Communications)

- Intelligence Gathering and Analysis

- Battlefield Management and Command & Control Systems

- Training & Simulation Systems

- Logistics & Supply Chain Management

- Weapon Systems and Platforms Security

- Others (e.g., Personnel Security, R&D Security)

- By End-User

- Government and Defense Departments

- Military Forces (Army, Navy, Air Force)

- Intelligence Agencies

- Aerospace & Defense Contractors

- Critical Infrastructure Operators (Private Sector, but Defense-related)

Regional Highlights

- North America: Dominates the defense cyber security market due to significant defense budgets, advanced technological infrastructure, and the presence of leading cybersecurity solution providers. The United States, in particular, drives substantial investment in research and development, integration of AI and machine learning, and stringent cybersecurity mandates for government and defense contractors.

- Europe: Exhibits robust growth, driven by increasing geopolitical tensions, the implementation of stringent data protection regulations such as GDPR, and collaborative efforts through NATO and the European Union. Countries like the United Kingdom, France, and Germany are at the forefront of adopting sophisticated cyber defense capabilities and fostering public-private partnerships.

- Asia Pacific (APAC): Emerging as a high-growth region propelled by rapid military modernization, escalating regional conflicts, and a growing recognition of cyber threats from state and non-state actors. Nations such as China, India, Japan, and South Korea are significantly increasing their defense cybersecurity spending and investing in indigenous capabilities.

- Latin America: Shows steady growth as countries increasingly recognize the importance of protecting critical national infrastructure and enhancing their defense capabilities against evolving cyber threats. Investment is primarily focused on foundational cybersecurity measures and capacity building.

- Middle East and Africa (MEA): Experiencing considerable market expansion driven by increased defense spending, ongoing conflicts, and a strategic focus on diversifying economies and protecting critical oil and gas infrastructure. Countries like Saudi Arabia, UAE, and Israel are investing heavily in advanced cyber defense technologies and developing regional cybersecurity hubs.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Defense Cyber Security Market.- Northrop Grumman

- Lockheed Martin

- Raytheon Technologies

- BAE Systems

- General Dynamics

- IBM

- Microsoft

- Cisco Systems

- Palo Alto Networks

- Fortinet

- Check Point Software Technologies

- CyberArk Software

- Splunk

- CrowdStrike

- FireEye (Mandiant)

- Zscaler

- Akamai Technologies

- RSA Security

- Thales

- Airbus Defence and Space

Frequently Asked Questions

What is the projected growth rate for the Defense Cyber Security Market?

The Defense Cyber Security Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.5% between 2025 and 2033.

How large is the Defense Cyber Security Market expected to be by 2033?

The market is projected to reach USD 58.0 billion by the end of the forecast period in 2033, up from an estimated USD 28.5 billion in 2025.

What are the primary drivers of the Defense Cyber Security Market?

Key drivers include escalating cyber warfare and state-sponsored attacks, rapid digital transformation in the defense sector, increased budget allocations for cybersecurity, and the growing adoption of cloud and IoT in military operations.

How is AI impacting defense cybersecurity?

AI is enhancing threat detection, automating incident response, providing predictive threat intelligence, and optimizing security operations. However, it also presents challenges from AI-powered offensive tools and ethical considerations for autonomous systems.

What are the main challenges facing the Defense Cyber Security Market?

Major challenges include the rapidly evolving and sophisticated threat landscape, vulnerabilities in global supply chains, the pervasive insider threat, and the complexities of integrating new security solutions with existing legacy IT systems.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted