Electrolyte Additive Market

Electrolyte Additive Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701935 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

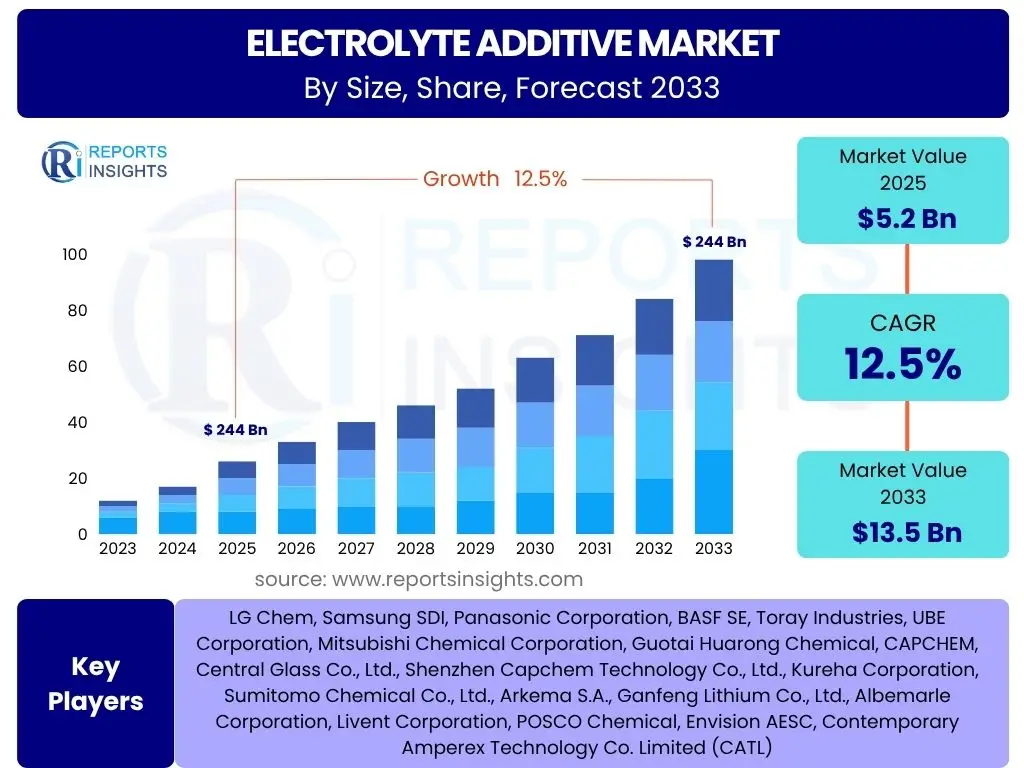

Electrolyte Additive Market Size

According to Reports Insights Consulting Pvt Ltd, The Electrolyte Additive Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.5% between 2025 and 2033. The market is estimated at USD 5.2 billion in 2025 and is projected to reach USD 13.5 billion by the end of the forecast period in 2033. This robust growth trajectory is primarily driven by the escalating global demand for high-performance batteries across various sectors, including electric vehicles, consumer electronics, and grid-scale energy storage systems.

The consistent expansion of the electric vehicle industry, coupled with the increasing adoption of renewable energy sources requiring efficient storage solutions, significantly propels the electrolyte additive market forward. These additives are crucial for enhancing battery lifespan, improving safety, and boosting overall performance, which are critical factors for mass adoption and technological advancement in the energy sector. The market's valuation reflects the intricate balance between technological innovation in battery chemistry and the growing imperative for sustainable energy solutions worldwide.

Key Electrolyte Additive Market Trends & Insights

The electrolyte additive market is currently experiencing dynamic shifts driven by advancements in battery technology and an increasing emphasis on safety and performance. Users frequently inquire about the emerging trends that are shaping battery development, particularly concerning how new materials can enhance energy density, extend cycle life, and mitigate safety risks. A significant area of interest revolves around additives that facilitate higher voltage operation and fast charging capabilities, addressing key limitations of existing battery chemistries. Furthermore, there is considerable focus on sustainable and environmentally friendly additives, reflecting a broader industry push towards green manufacturing and responsible material sourcing.

Another prominent trend gaining traction is the development of multi-functional additives that can simultaneously address several performance parameters, such as improving anode/cathode interface stability, reducing gas generation, and enhancing low-temperature performance. The advent of solid-state battery technology also presents a unique set of challenges and opportunities for electrolyte additives, as traditional liquid electrolytes are replaced by solid-state alternatives. This necessitates the creation of novel additives compatible with solid electrolytes to ensure efficient ion transport and robust interfacial contact. Understanding these evolving trends is crucial for stakeholders aiming to innovate and maintain a competitive edge in the rapidly transforming battery landscape.

- Development of multi-functional additives for enhanced performance across various parameters.

- Increased focus on sustainable, bio-derived, and environmentally friendly electrolyte components.

- Growing demand for additives that improve battery safety, particularly against thermal runaway and overcharge.

- Innovations in additives for high-voltage and fast-charging battery systems.

- Research and development of specific additives compatible with solid-state and next-generation battery chemistries.

- Integration of advanced analytics and AI for designing and testing novel additive formulations.

- Expansion of applications beyond traditional lithium-ion batteries, including sodium-ion and flow batteries.

AI Impact Analysis on Electrolyte Additive

The integration of Artificial intelligence (AI) is set to profoundly transform the electrolyte additive market, with common user questions centering on how AI can accelerate research and development, optimize material discovery, and streamline manufacturing processes. Users are keen to understand AI's role in predicting the properties of novel additive chemistries, identifying optimal formulations, and simulating battery performance under various conditions, thereby significantly reducing the time and cost associated with traditional experimental methods. There is also considerable interest in AI-driven quality control and supply chain optimization, as these aspects directly impact product consistency and market responsiveness.

AI's influence extends to enabling more sophisticated data analysis from battery testing, allowing researchers to uncover complex relationships between additive structure, electrolyte composition, and overall battery degradation mechanisms. This capability empowers manufacturers to fine-tune additive formulations for specific applications, achieving unprecedented levels of performance and longevity. Furthermore, AI can aid in the discovery of entirely new classes of materials that could serve as revolutionary electrolyte additives, pushing the boundaries of what is currently possible in battery technology. The long-term expectation is that AI will democratize access to advanced material science, fostering a more agile and innovative electrolyte additive market.

- Accelerated discovery and design of novel electrolyte additive molecules through AI-driven simulations.

- Optimization of additive formulations and concentrations for specific battery chemistries and applications.

- Enhanced quality control and predictive maintenance in electrolyte additive manufacturing processes.

- Improved understanding of degradation mechanisms and battery lifespan through AI-powered data analysis.

- Streamlined supply chain management and demand forecasting for raw materials used in additives.

- Development of intelligent robotic systems for automated synthesis and testing of new additive compounds.

- Personalized electrolyte solutions for diverse battery requirements, enabled by machine learning algorithms.

Key Takeaways Electrolyte Additive Market Size & Forecast

Common user inquiries regarding the electrolyte additive market size and forecast frequently revolve around understanding the primary growth drivers, the longevity of current trends, and the potential impact of disruptive technologies. A key takeaway is the consistent and substantial growth projected for this market, underpinned by the insatiable global demand for advanced energy storage solutions. The forecast indicates a transition towards higher-performance and safer battery chemistries, directly increasing the reliance on specialized electrolyte additives that can meet stringent industrial and consumer requirements. This growth is not merely incremental but reflective of a fundamental shift towards electrification across transportation, industrial, and residential sectors.

Another crucial insight is the direct correlation between battery technology advancements and the market for electrolyte additives. As battery energy density increases and charging times decrease, the stress on electrolyte components intensifies, necessitating more robust and sophisticated additive solutions. Furthermore, the market's trajectory is heavily influenced by regulatory frameworks promoting clean energy and reducing carbon emissions, particularly in regions with ambitious electric vehicle targets. Stakeholders should recognize that investment in research and development of novel, multi-functional, and environmentally benign additives will be paramount for securing future market share and capitalizing on the evolving energy landscape.

- The electrolyte additive market is poised for significant and sustained growth, driven by global electrification trends.

- Innovation in battery chemistry directly fuels the demand for advanced and specialized electrolyte additives.

- Safety and performance enhancement remain critical factors influencing additive development and adoption.

- Electric vehicles and grid-scale energy storage systems are the primary application segments propelling market expansion.

- Sustainable and environmentally friendly additive solutions represent a growing area of focus and opportunity.

- The market is dynamic, requiring continuous R&D investment to address evolving battery technology challenges.

- Regulatory support for clean energy and emissions reduction will continue to bolster market demand.

Electrolyte Additive Market Drivers Analysis

The electrolyte additive market is significantly propelled by several powerful forces that collectively drive demand for advanced battery components. A primary driver is the accelerating adoption of electric vehicles (EVs) worldwide, necessitating batteries with higher energy density, longer cycle life, and enhanced safety features. Electrolyte additives play a critical role in achieving these performance metrics, preventing degradation, and ensuring stability under demanding conditions. Concurrently, the increasing deployment of renewable energy sources such as solar and wind power creates a strong demand for grid-scale energy storage systems (ESS) to balance intermittency. These large-scale applications require durable and efficient batteries, where specialized additives contribute significantly to longevity and operational reliability.

Beyond EVs and ESS, the pervasive growth of consumer electronics, including smartphones, laptops, and wearable devices, continues to fuel the market. Consumers expect faster charging, longer battery life, and enhanced safety in these portable devices, all of which are enabled by sophisticated electrolyte additive formulations. Furthermore, advancements in battery technology itself, such as the transition to higher nickel content cathodes or silicon-based anodes, create specific needs for new additives to stabilize these novel materials and prevent undesirable side reactions. The global imperative for energy transition and decarbonization positions the electrolyte additive market as a foundational element in achieving sustainable energy ecosystems.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid growth of the Electric Vehicle (EV) industry globally. Additives enhance range, safety, and battery lifespan, crucial for mass EV adoption. | +3.5% | North America, Europe, Asia Pacific (China, Japan, South Korea) | 2025-2033 (Long-term) |

| Increasing deployment of grid-scale energy storage systems. Additives improve cycle stability and performance of batteries for renewable energy integration. | +2.8% | Asia Pacific (China, India), Europe (Germany, UK), North America (USA) | 2025-2033 (Long-term) |

| Technological advancements in battery chemistry (e.g., higher energy density cathodes, silicon anodes). New chemistries require specialized additives for stability and performance. | +2.2% | Global, particularly leading battery R&D hubs | 2025-2033 (Mid to Long-term) |

| Expanding demand for consumer electronics with enhanced battery performance. Longer battery life, faster charging, and improved safety are driven by additive innovation. | +1.5% | Global, major consumer markets like North America, Europe, Asia Pacific | 2025-2030 (Mid-term) |

| Stringent safety regulations and performance standards for batteries. Additives are essential for meeting safety certifications and ensuring robust battery operation. | +1.0% | Global, particularly highly regulated markets | 2025-2033 (Long-term) |

Electrolyte Additive Market Restraints Analysis

Despite robust growth, the electrolyte additive market faces several notable restraints that could temper its expansion. One significant challenge is the high cost associated with developing and producing highly specialized additives. Many advanced additives require complex synthesis processes and expensive raw materials, which can contribute to the overall manufacturing cost of batteries, potentially hindering their widespread adoption, especially in cost-sensitive applications. Furthermore, the inherent complexity of battery chemistry means that even small changes in additive formulations can have unforeseen effects on battery performance or safety, leading to extensive testing and validation periods that delay market entry for new products.

Another key restraint involves the supply chain vulnerabilities of critical raw materials. Some unique chemical precursors for advanced additives are sourced from a limited number of suppliers or specific geographical regions, making the market susceptible to geopolitical tensions, trade disputes, or natural disasters. This can lead to price volatility and supply disruptions. Additionally, the increasing scrutiny over environmental impact and sustainability concerns related to certain chemical additives could lead to tighter regulations, potentially restricting the use of some existing compounds and necessitating costly re-formulation or the development of entirely new, compliant alternatives. Balancing performance enhancement with cost-effectiveness and environmental considerations remains a persistent challenge for market participants.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High cost of advanced electrolyte additives and complex synthesis processes, impacting overall battery cost-effectiveness. | -1.8% | Global, particularly emerging markets | 2025-2030 (Mid-term) |

| Supply chain vulnerabilities and volatility of raw material prices for key additive precursors. | -1.5% | Global, impacting regions reliant on specific imports | 2025-2028 (Short to Mid-term) |

| Stringent regulatory approvals and lengthy validation processes for new chemical formulations, extending time-to-market. | -1.2% | Europe, North America, Japan | 2025-2033 (Long-term) |

| Potential environmental and toxicity concerns related to certain chemical additives, leading to regulatory restrictions. | -0.9% | Europe, parts of Asia Pacific (China) | 2028-2033 (Mid to Long-term) |

| Technological limitations in balancing multiple performance parameters (e.g., safety vs. energy density) simultaneously. | -0.7% | Global, impacting R&D efforts | 2025-2033 (Long-term) |

Electrolyte Additive Market Opportunities Analysis

Significant opportunities are emerging within the electrolyte additive market, primarily driven by the continuous evolution of battery technology and the increasing demand for enhanced performance. One major avenue for growth lies in the development of additives specifically designed for next-generation battery chemistries, such as solid-state batteries, lithium-sulfur batteries, and sodium-ion batteries. These technologies require entirely new classes of electrolyte components to overcome their unique challenges related to interface stability, dendrite suppression, and overall efficiency, presenting a fertile ground for innovation and new market entrants. The pursuit of higher energy density and faster charging capabilities in existing lithium-ion platforms also opens doors for novel additives that can push these limits safely and effectively.

Furthermore, the growing emphasis on sustainability and circular economy principles presents an opportunity for developing eco-friendly and bio-derived additives. Companies that can offer additives with a reduced environmental footprint, either through sustainable sourcing, less toxic synthesis, or improved recyclability of battery components, stand to gain a competitive advantage and appeal to environmentally conscious manufacturers and consumers. The expansion into niche applications, such as medical devices, aerospace, and specialized industrial equipment, which demand exceptionally reliable and long-lasting power sources, also offers premium market segments for highly specialized and performance-optimized additives. Leveraging advanced materials science and computational chemistry to rapidly screen and design these next-generation additives will be crucial for capitalizing on these burgeoning opportunities.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of specialized additives for next-generation batteries (e.g., solid-state, Li-S, Na-ion). | +2.5% | Global, particularly battery R&D hubs | 2028-2033 (Long-term) |

| Growing demand for sustainable and eco-friendly electrolyte additives, including bio-derived options. | +2.0% | Europe, North America, Asia Pacific (Japan, South Korea) | 2025-2033 (Mid to Long-term) |

| Expansion into new high-value, niche applications requiring ultra-high performance and reliability (e.g., medical, aerospace). | +1.8% | Global, targeting specialized industries | 2025-2033 (Long-term) |

| Integration of AI and machine learning for accelerated discovery and optimization of new additive chemistries. | +1.5% | Global, particularly technologically advanced regions | 2025-2030 (Mid-term) |

| Enhanced focus on circular economy principles and battery recycling, creating demand for additives that aid in material recovery. | +1.0% | Europe, North America | 2028-2033 (Long-term) |

Electrolyte Additive Market Challenges Impact Analysis

The electrolyte additive market faces several significant challenges that require strategic navigation to sustain growth and innovation. One pervasive challenge is the technical complexity involved in developing additives that are effective, safe, and compatible with diverse battery chemistries without introducing new failure modes. Achieving the optimal balance between enhancing performance parameters like cycle life and energy density while simultaneously ensuring thermal stability and preventing gas generation is an intricate scientific and engineering hurdle. This often leads to prolonged research and development cycles and high investment costs, increasing the risk associated with new product introductions.

Another critical challenge is intellectual property protection and intense competition. The market is characterized by a relatively small number of highly specialized players, leading to fierce competition over patented technologies and market share. Developing proprietary additive formulations that offer a distinct competitive advantage is paramount, yet the landscape of chemical synthesis and application is increasingly crowded. Furthermore, scaling up production of novel, complex additives from laboratory to commercial volumes while maintaining consistent quality and cost-effectiveness presents significant manufacturing challenges. Ensuring global regulatory compliance across different jurisdictions, each with unique chemical safety and environmental standards, adds another layer of complexity for market participants striving for international presence.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Technical complexity in developing multi-functional additives that enhance performance without compromising safety or stability. | -1.9% | Global, particularly R&D intensive regions | 2025-2033 (Long-term) |

| Intense competition and the need for robust intellectual property protection for proprietary additive formulations. | -1.6% | Global, impacting competitive landscapes | 2025-2033 (Long-term) |

| Scaling up production of novel additives from laboratory to commercial volumes while maintaining quality and cost-effectiveness. | -1.4% | Global, particularly for new market entrants | 2025-2030 (Mid-term) |

| Ensuring global regulatory compliance amidst varying chemical safety and environmental standards across different regions. | -1.0% | Europe, North America, parts of Asia Pacific | 2025-2033 (Long-term) |

| Managing the long product development and validation cycles inherent in battery material innovation. | -0.8% | Global | 2025-2030 (Mid-term) |

Electrolyte Additive Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global electrolyte additive market, offering critical insights into its current dynamics, historical performance, and future growth trajectories. The scope encompasses detailed market sizing, segmentation analysis by various parameters, examination of key market drivers, restraints, opportunities, and challenges, along with a thorough competitive landscape assessment. The report also highlights the profound impact of emerging technologies like Artificial Intelligence on material discovery and manufacturing processes within this sector, providing a holistic view for strategic decision-making and investment planning.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 5.2 Billion |

| Market Forecast in 2033 | USD 13.5 Billion |

| Growth Rate | 12.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | LG Chem, Samsung SDI, Panasonic Corporation, BASF SE, Toray Industries, UBE Corporation, Mitsubishi Chemical Corporation, Guotai Huarong Chemical, CAPCHEM, Central Glass Co., Ltd., Shenzhen Capchem Technology Co., Ltd., Kureha Corporation, Sumitomo Chemical Co., Ltd., Arkema S.A., Ganfeng Lithium Co., Ltd., Albemarle Corporation, Livent Corporation, POSCO Chemical, Envision AESC, Contemporary Amperex Technology Co. Limited (CATL) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The electrolyte additive market is intricately segmented to reflect the diverse applications, specific chemical requirements, and functional enhancements these additives provide across the battery landscape. Understanding these segmentations is crucial for identifying precise market opportunities and tailoring product development to meet specific industry needs. The market is primarily segmented by type of additive, which encompasses film-forming agents, cathode/anode protectors, and specialized additives for safety and performance. Further segmentation by battery type differentiates demand based on the unique chemistries of lithium-ion, solid-state, and other emerging battery technologies, each with distinct additive requirements for optimal functioning.

Segmentation by end-use application highlights the critical role of these additives in high-growth sectors such as electric vehicles, consumer electronics, and large-scale energy storage systems, demonstrating the market's reliance on broad industry adoption. Additionally, the market is analyzed by the form of the additive (liquid or solid) and its primary function, whether it's enhancing performance, ensuring safety, extending lifecycle, or reducing costs. This multi-dimensional segmentation provides a granular view of the market, allowing for targeted strategies in research, manufacturing, and distribution, ultimately supporting the continuous evolution and widespread commercialization of advanced battery technologies.

- By Type:

- Film-forming Additives

- Cathode Protection Additives

- Anode Protection Additives

- Lithium Salt Additives

- Flame Retardant Additives

- Overcharge Protection Additives

- Redox Shuttle Additives

- Others

- By Battery Type:

- Lithium-ion Batteries

- LiCoO2

- LiFePO4

- LiMn2O4

- LiNiMnCoO2

- Others

- Sodium-ion Batteries

- Solid-state Batteries

- Lead-acid Batteries

- Nickel-Cadmium Batteries

- Others

- Lithium-ion Batteries

- By End-Use Application:

- Electric Vehicles (EVs, HEVs, PHEVs)

- Consumer Electronics (Smartphones, Laptops, Tablets, Wearables)

- Energy Storage Systems (Grid-scale, Residential, Commercial)

- Industrial (Forklifts, UPS, Power Tools)

- Medical Devices

- Aerospace & Defense

- Others

- By Form:

- Liquid

- Solid

- By Function:

- Performance Enhancers

- Safety Enhancers

- Life Cycle Extenders

- Cost Reducers

Regional Highlights

The global electrolyte additive market exhibits significant regional disparities, driven by varying levels of industrialization, technological adoption, and governmental support for battery manufacturing and electric vehicles. Asia Pacific (APAC) currently dominates the market, largely due to the presence of major battery manufacturers and burgeoning electric vehicle production hubs in countries like China, South Korea, and Japan. China, in particular, leads in terms of battery production capacity and EV adoption, creating immense demand for electrolyte additives. The region benefits from robust supply chains and extensive investments in battery R&D, making it a pivotal growth engine for the market.

North America and Europe also represent substantial markets, propelled by increasing investments in electric vehicle infrastructure, stringent emission regulations, and a growing focus on grid modernization through energy storage systems. Countries such as the United States, Germany, and France are actively promoting battery Gigafactories and supporting research into advanced battery chemistries, thereby stimulating demand for innovative additives. While Latin America, the Middle East, and Africa (MEA) currently hold smaller market shares, they are expected to witness gradual growth as urbanization accelerates and initiatives for renewable energy integration and electric mobility gain momentum. Regional market dynamics are continuously evolving, influenced by national energy policies, raw material availability, and technological partnerships aimed at fostering self-sufficiency in battery component manufacturing.

- Asia Pacific (APAC): Dominant market share driven by leading battery manufacturers, high EV adoption rates, and robust governmental support in countries like China, South Korea, and Japan.

- North America: Significant growth propelled by increasing EV sales, grid-scale energy storage projects, and governmental incentives for battery production and research in the United States and Canada.

- Europe: Strong market expansion fueled by ambitious decarbonization goals, rapid development of battery Gigafactories, and stringent environmental regulations in Germany, France, and the UK.

- Latin America: Emerging market with increasing interest in electric mobility and renewable energy integration, though currently smaller in scale.

- Middle East and Africa (MEA): Nascent market with potential for growth driven by future investments in renewable energy and developing electric vehicle infrastructure.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Electrolyte Additive Market.- LG Chem

- Samsung SDI

- Panasonic Corporation

- BASF SE

- Toray Industries

- UBE Corporation

- Mitsubishi Chemical Corporation

- Guotai Huarong Chemical

- CAPCHEM

- Central Glass Co., Ltd.

- Shenzhen Capchem Technology Co., Ltd.

- Kureha Corporation

- Sumitomo Chemical Co., Ltd.

- Arkema S.A.

- Ganfeng Lithium Co., Ltd.

- Albemarle Corporation

- Livent Corporation

- POSCO Chemical

- Envision AESC

- Contemporary Amperex Technology Co. Limited (CATL)

Frequently Asked Questions

What is the projected growth rate for the Electrolyte Additive Market?

The Electrolyte Additive Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.5% between 2025 and 2033. This robust growth is primarily driven by the escalating global demand for high-performance batteries in electric vehicles, consumer electronics, and grid-scale energy storage systems. The market is expected to expand significantly as these sectors continue their rapid development and adoption.

Which factors are primarily driving the Electrolyte Additive Market?

The market is primarily driven by the accelerating global adoption of electric vehicles (EVs), the increasing deployment of grid-scale energy storage systems (ESS) for renewable energy integration, and continuous technological advancements in battery chemistry. Furthermore, the pervasive growth of consumer electronics and stringent safety regulations for batteries also significantly contribute to market expansion.

How is AI impacting the Electrolyte Additive sector?

AI is profoundly impacting the electrolyte additive sector by accelerating research and development, optimizing material discovery, and streamlining manufacturing processes. It enables the prediction of additive properties, identification of optimal formulations, and simulation of battery performance, significantly reducing time and cost. AI also enhances quality control and allows for more sophisticated data analysis from battery testing.

What are the key opportunities in the Electrolyte Additive Market?

Key opportunities include the development of specialized additives for next-generation battery chemistries (e.g., solid-state, lithium-sulfur, sodium-ion), the growing demand for sustainable and eco-friendly additive solutions, and expansion into high-value, niche applications. The integration of AI for accelerated discovery and an increased focus on circular economy principles also present significant growth avenues.

Which regions are leading in the Electrolyte Additive Market?

The Asia Pacific (APAC) region currently dominates the electrolyte additive market due to the strong presence of major battery manufacturers and significant electric vehicle production hubs in countries like China, South Korea, and Japan. North America and Europe are also substantial markets, driven by investments in EV infrastructure and energy storage systems, along with supportive regulatory environments.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted