Additive Manufacturing for General Aviation Market

Additive Manufacturing for General Aviation Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702431 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

Additive Manufacturing for General Aviation Market Size

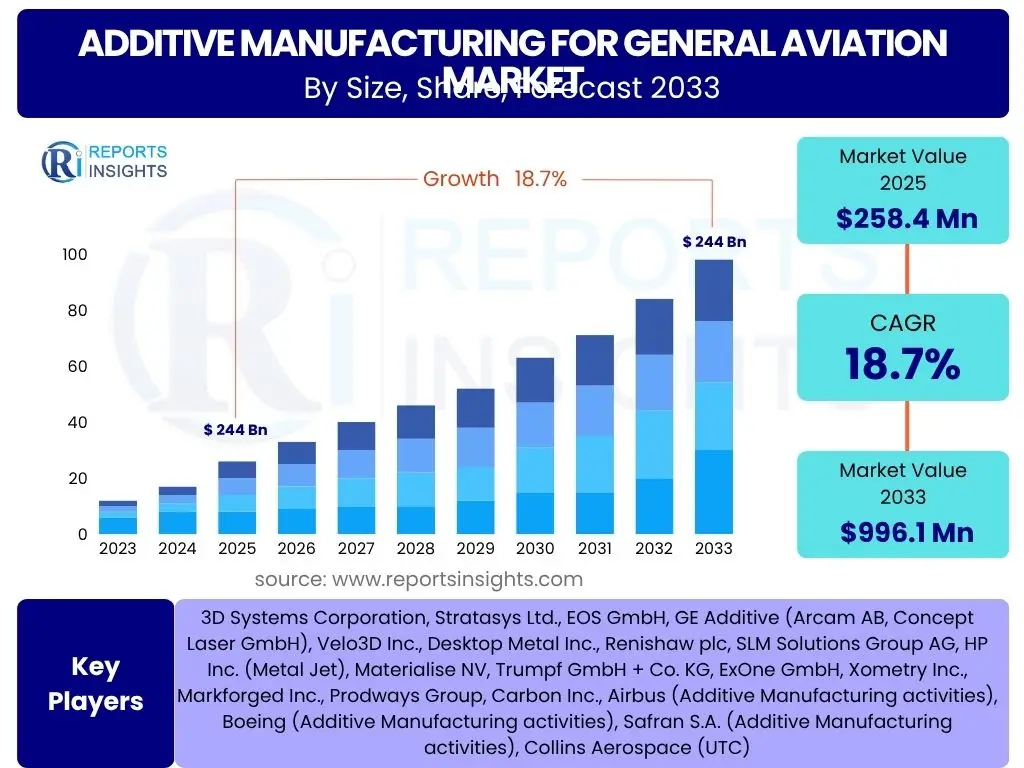

According to Reports Insights Consulting Pvt Ltd, The Additive Manufacturing for General Aviation Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 18.7% between 2025 and 2033. The market is estimated at USD 258.4 Million in 2025 and is projected to reach USD 996.1 Million by the end of the forecast period in 2033.

Key Additive Manufacturing for General Aviation Market Trends & Insights

The Additive Manufacturing for General Aviation market is currently undergoing significant transformation, driven by a confluence of technological advancements and increasing operational demands. Key inquiries from industry stakeholders often revolve around the adoption rates of new materials, the integration of advanced digital manufacturing workflows, and the expanding scope of applications beyond prototyping into production-grade components and MRO. There is a growing emphasis on leveraging additive manufacturing for its unique capabilities in part consolidation, weight reduction, and the creation of highly complex geometries previously unattainable with traditional manufacturing methods. This paradigm shift is not only enhancing aircraft performance and fuel efficiency but also fundamentally reshaping supply chain dynamics for general aviation.

Another prominent trend is the increasing collaboration between additive manufacturing technology providers, material scientists, and aerospace original equipment manufacturers (OEMs) and MRO providers. This collaborative ecosystem is accelerating material qualification and certification processes, which are critical for aerospace applications due to stringent safety and performance requirements. Furthermore, the push towards sustainable aviation is fueling interest in additive manufacturing's ability to reduce material waste and enable on-demand production, thereby minimizing inventory costs and environmental impact. The ongoing refinement of post-processing techniques and surface finish capabilities is also contributing to the broader acceptance and deployment of additive manufactured parts in critical general aviation systems.

- Increased adoption of advanced metallic and polymer materials for flight-critical components.

- Growing integration of design for additive manufacturing (DfAM) principles to optimize part performance and reduce weight.

- Expansion of additive manufacturing applications from prototyping and tooling to end-use parts and MRO.

- Development of digital twins and advanced simulation tools to streamline the AM design and validation process.

- Emphasis on supply chain localization and resilience through on-demand additive manufacturing capabilities.

- Standardization and certification efforts gaining momentum to facilitate wider industry acceptance.

AI Impact Analysis on Additive Manufacturing for General Aviation

User inquiries concerning AI's influence on Additive Manufacturing for General Aviation frequently center on its potential to revolutionize design, optimize production parameters, enhance quality control, and streamline maintenance operations. There is a strong interest in how artificial intelligence algorithms can unlock new possibilities in generative design, allowing for the creation of lightweight and high-performance components with optimized lattice structures. Users also question AI's role in predictive analytics for machine maintenance, ensuring higher uptime and operational efficiency for costly additive manufacturing equipment. Furthermore, the application of machine learning for process monitoring and anomaly detection during the build process is a significant area of focus, promising improved part consistency and reduced defect rates, which are crucial for aerospace safety standards.

Beyond design and manufacturing, AI is also anticipated to play a pivotal role in post-processing and quality assurance by automating inspection processes and identifying potential flaws with greater accuracy than manual methods. This leads to a more robust validation framework for additively manufactured parts. The integration of AI-powered data analytics is enabling manufacturers to gain deeper insights from vast datasets generated during the AM process, leading to continuous improvement in material properties, process reliability, and overall component performance. This holistic approach, from design to end-of-life, positions AI as a transformative force, enabling the aerospace industry to fully leverage the potential of additive manufacturing for general aviation applications.

- Generative design and topology optimization using AI for lightweight, high-performance parts.

- AI-driven process parameter optimization for enhanced print quality and reduced material waste.

- Real-time quality monitoring and defect detection through AI-powered vision systems and sensors.

- Predictive maintenance of additive manufacturing equipment to minimize downtime and optimize production schedules.

- Enhanced supply chain management and inventory optimization via AI-driven demand forecasting for spare parts.

- Automated post-processing and inspection using robotic systems guided by AI algorithms.

Key Takeaways Additive Manufacturing for General Aviation Market Size & Forecast

The primary insights derived from the Additive Manufacturing for General Aviation market size and forecast data highlight a robust growth trajectory, driven by the inherent advantages additive manufacturing offers to the aerospace sector. Common user questions indicate a keen interest in understanding the core reasons behind this expansion, with a focus on how AM addresses critical industry pain points such as reducing lead times for complex parts, optimizing inventory management, and enhancing aircraft performance through lightweighting. The market's upward trend is fundamentally tied to the increasing maturity of AM technologies, the broader availability of aerospace-grade materials, and a growing acceptance by regulatory bodies of additively manufactured components in certificated aircraft. This indicates a strategic shift from traditional manufacturing toward more agile and efficient production methodologies.

Furthermore, the forecast underscores the long-term investment potential within this market, emphasizing opportunities across various segments including prototyping, tooling, and an expanding share in direct part manufacturing and Maintenance, Repair, and Overhaul (MRO) operations. The significant projected increase in market valuation by 2033 suggests that general aviation stakeholders are increasingly recognizing the cost efficiencies, design flexibility, and performance improvements that additive manufacturing provides. This trend is further solidified by ongoing research and development into new materials and processes, promising even greater integration and impact on the future of general aviation manufacturing and maintenance practices.

- Significant market growth driven by demand for lightweighting and customized components.

- Increasing adoption of AM for both prototyping and end-use parts in general aviation.

- Strong potential for cost reduction through optimized material usage and reduced assembly.

- Growing confidence in AM technologies due to advancements in material science and process control.

- Regulatory advancements expected to further accelerate market penetration and application scope.

- MRO applications represent a substantial and expanding segment for additive manufacturing.

Additive Manufacturing for General Aviation Market Drivers Analysis

The market for additive manufacturing in general aviation is propelled by several critical factors that address the industry's evolving needs for efficiency, performance, and flexibility. A primary driver is the continuous demand for lightweight aircraft components to improve fuel efficiency and extend operational range, a capability uniquely facilitated by additive manufacturing's ability to create complex, optimized geometries. Furthermore, the inherent design freedom offered by AM allows for part consolidation, reducing the number of individual components in an assembly, which in turn simplifies supply chains, lowers manufacturing costs, and enhances overall system reliability for general aviation aircraft.

Another significant driver is the growing need for rapid prototyping and on-demand spare parts, particularly crucial for the diverse and often older fleet of general aviation aircraft where traditional parts may be scarce or lead times prohibitively long. Additive manufacturing provides an agile solution for producing low-volume, highly customized parts, reducing inventory holding costs and minimizing aircraft downtime. This capability, combined with advancements in material science offering aerospace-grade polymers and metals, positions additive manufacturing as a cornerstone technology for modernizing general aviation manufacturing and maintenance operations.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Demand for Lightweight Components & Fuel Efficiency | +4.2% | Global, particularly North America, Europe | Short- to Mid-term (2025-2030) |

| Increased Design Freedom & Part Consolidation | +3.8% | Global | Short- to Mid-term (2025-2030) |

| Need for Rapid Prototyping & On-Demand Parts | +3.5% | Global, especially developing regions for MRO | Short- to Mid-term (2025-2030) |

| Advancements in Materials Science & AM Technologies | +3.0% | Global, concentrated in R&D hubs | Mid- to Long-term (2027-2033) |

| Reduction in Production Lead Times & Supply Chain Simplification | +2.5% | Global | Short-term (2025-2027) |

Additive Manufacturing for General Aviation Market Restraints Analysis

Despite its significant advantages, the additive manufacturing for general aviation market faces several restraints that could impede its growth. A primary challenge is the high initial capital investment required for industrial-grade additive manufacturing machines and associated infrastructure. This substantial upfront cost can be prohibitive for smaller general aviation companies or maintenance facilities, limiting widespread adoption, particularly for those operating on tighter margins or with less access to large-scale funding.

Another significant restraint involves the stringent certification and qualification processes unique to the aerospace industry. While progress is being made, obtaining approval for additively manufactured parts to be used in flight-critical applications can be a time-consuming and expensive endeavor, often requiring extensive testing and validation. Furthermore, the limited availability of certified aerospace-grade materials specifically optimized for additive processes, coupled with concerns regarding consistency and repeatability of material properties in printed parts, continues to pose challenges for broader application and acceptance within the general aviation sector.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Capital Investment | -3.5% | Global, particularly SMEs | Short- to Mid-term (2025-2030) |

| Stringent Regulatory & Certification Processes | -3.0% | Global, highly impactful in North America, Europe | Mid- to Long-term (2027-2033) |

| Limited Availability of Certified Materials | -2.8% | Global | Short- to Mid-term (2025-2030) |

| Post-Processing Requirements & Surface Finish Challenges | -2.0% | Global | Short-term (2025-2027) |

Additive Manufacturing for General Aviation Market Opportunities Analysis

The additive manufacturing for general aviation market presents significant opportunities for growth and innovation. One major area of opportunity lies in the expanding use of AM for Maintenance, Repair, and Overhaul (MRO) applications. As general aviation aircraft often have long service lives, the ability to rapidly produce obsolete or hard-to-find spare parts on demand can drastically reduce downtime, improve fleet readiness, and lower overall operational costs. This shift from traditional spare parts logistics to localized, digital inventory management offers substantial efficiency gains.

Furthermore, the continuous development of novel additive manufacturing materials, including high-performance polymers, advanced metal alloys, and composites, opens up new avenues for component design and functional integration. These material innovations will enable the creation of lighter, stronger, and more resilient parts specifically tailored for general aviation environments. The increasing demand for customization in aircraft interiors, avionics housing, and specialized tooling also provides fertile ground for additive manufacturing, allowing for bespoke solutions that enhance passenger comfort, crew efficiency, and aircraft functionality, thereby driving market expansion and adoption across diverse segments of the general aviation industry.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into MRO Applications & Spare Parts Production | +4.5% | Global, high impact in North America, Europe, Asia Pacific | Short- to Mid-term (2025-2030) |

| Development of New & Advanced AM Materials | +3.9% | Global, focused on R&D regions | Mid- to Long-term (2027-2033) |

| Growth in Mass Customization & Personalization | +3.2% | Global, high impact in affluent markets | Short- to Mid-term (2025-2030) |

| Increased Integration with Digital Manufacturing & Industry 4.0 | +2.8% | Global | Mid- to Long-term (2027-2033) |

Additive Manufacturing for General Aviation Market Challenges Impact Analysis

The additive manufacturing for general aviation market faces a distinct set of challenges that require careful navigation for sustainable growth. One significant challenge is the ongoing need for robust standardization and regulatory harmonization across different jurisdictions. The lack of universally accepted standards for materials, processes, and post-processing limits the widespread adoption and interchangeability of additively manufactured parts, particularly for safety-critical components, posing a hurdle for general aviation manufacturers operating globally.

Another key challenge is the scalability of current additive manufacturing processes for high-volume production. While AM excels in low-volume, complex part manufacturing, scaling up to meet the demands of serial production for certain general aviation components can be cost-prohibitive and time-consuming compared to traditional methods. Furthermore, there is a persistent challenge in developing and retaining a skilled workforce proficient in both additive manufacturing technologies and the specific requirements of aerospace engineering, impacting the pace of innovation and effective deployment of AM solutions within the general aviation sector.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Lack of Standardization & Regulatory Harmonization | -3.0% | Global | Mid- to Long-term (2027-2033) |

| Scalability for High-Volume Production | -2.5% | Global | Short- to Mid-term (2025-2030) |

| Workforce Skill Gap & Training Requirements | -2.2% | Global | Short- to Mid-term (2025-2030) |

| Intellectual Property & Data Security Concerns | -1.8% | Global | Short- to Mid-term (2025-2030) |

Additive Manufacturing for General Aviation Market - Updated Report Scope

This report provides a comprehensive analysis of the Additive Manufacturing for General Aviation market, offering in-depth insights into market size, growth drivers, restraints, opportunities, and challenges across various segments and key regions. It encompasses a detailed examination of technological advancements, material trends, and their applications within the general aviation sector, providing a strategic outlook for stakeholders.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 258.4 Million |

| Market Forecast in 2033 | USD 996.1 Million |

| Growth Rate | 18.7% |

| Number of Pages | 255 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | 3D Systems Corporation, Stratasys Ltd., EOS GmbH, GE Additive (Arcam AB, Concept Laser GmbH), Velo3D Inc., Desktop Metal Inc., Renishaw plc, SLM Solutions Group AG, HP Inc. (Metal Jet), Materialise NV, Trumpf GmbH + Co. KG, ExOne GmbH, Xometry Inc., Markforged Inc., Prodways Group, Carbon Inc., Airbus (Additive Manufacturing activities), Boeing (Additive Manufacturing activities), Safran S.A. (Additive Manufacturing activities), Collins Aerospace (UTC) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Additive Manufacturing for General Aviation market is meticulously segmented to provide a granular understanding of its diverse components and dynamics. This comprehensive segmentation allows for a detailed analysis of market performance across different materials, technologies, applications, and aircraft types, reflecting the varied needs and advancements within the general aviation sector. Understanding these segments is crucial for identifying specific growth pockets, competitive landscapes, and strategic opportunities for stakeholders.

The segmentation by material includes various metals like titanium, aluminum, and nickel alloys, alongside high-performance polymers and composites, each chosen for their unique properties essential for aerospace applications. Technology segmentation encompasses prominent AM processes such as FDM, SLS, DMLS, and EBM, highlighting the adoption trends of different printing methods. Applications are categorized into prototyping, tooling, end-use component manufacturing, and the rapidly growing MRO segment, indicating the expanding utility of AM. Lastly, segmentation by aircraft type, including business jets, light aircraft, and helicopters, reveals the specific demands and adoption rates across different general aviation platforms, providing a holistic view of the market structure.

- By Material:

- Metals (Titanium Alloys, Aluminum Alloys, Nickel Alloys, Stainless Steel, Cobalt-Chrome)

- Polymers (PEEK, ULTEM, Nylon, ABS, PLA)

- Composites (Carbon Fiber Reinforced Polymers, Ceramic Matrix Composites)

- By Technology:

- Fused Deposition Modeling (FDM) / Fused Filament Fabrication (FFF)

- Selective Laser Sintering (SLS)

- Stereolithography (SLA)

- Direct Metal Laser Sintering (DMLS) / Selective Laser Melting (SLM)

- Electron Beam Melting (EBM)

- Binder Jetting

- Material Jetting (PolyJet/MultiJet Modeling)

- Powder Bed Fusion (PBF)

- By Application:

- Prototyping & Tooling

- Manufacturing of Components (Engine Components, Airframe Components, Interior Components, Hydraulic & Electrical Systems)

- Maintenance, Repair, and Overhaul (MRO)

- By Aircraft Type:

- Business Jets

- Light Aircraft & Trainer Aircraft

- Helicopters (Civilian)

- Sport Aircraft & Ultralights

Regional Highlights

- North America: Expected to dominate the market due to the presence of key aerospace manufacturers, a robust general aviation industry, significant R&D investments in additive manufacturing, and favorable regulatory support from agencies like the FAA. The region's strong focus on advanced materials and digital manufacturing also contributes to its leading position.

- Europe: A significant market player, driven by strong government initiatives supporting additive manufacturing research, a well-established aerospace industry, and a growing emphasis on sustainable aviation practices. Countries like Germany, France, and the UK are at the forefront of AM adoption in general aviation.

- Asia Pacific (APAC): Projected to exhibit the fastest growth, fueled by increasing general aviation aircraft fleets, rising demand for MRO services, and growing investments in advanced manufacturing technologies by countries such as China, India, and Japan. The region's expanding aviation infrastructure and cost-effective manufacturing capabilities also play a crucial role.

- Latin America: Emerging as a market with nascent but growing adoption, primarily driven by increasing private aircraft ownership and regional efforts to modernize aviation maintenance facilities. Opportunities exist for AM to address challenges in parts availability and lead times.

- Middle East and Africa (MEA): Showing gradual adoption, with growth spurred by strategic investments in aerospace infrastructure and diversification efforts away from oil economies. The demand for localized MRO capabilities and regional airline expansion supports the slow but steady integration of additive manufacturing.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Additive Manufacturing for General Aviation Market.- 3D Systems Corporation

- Stratasys Ltd.

- EOS GmbH

- GE Additive (Arcam AB, Concept Laser GmbH)

- Velo3D Inc.

- Desktop Metal Inc.

- Renishaw plc

- SLM Solutions Group AG

- HP Inc. (Metal Jet)

- Materialise NV

- Trumpf GmbH + Co. KG

- ExOne GmbH

- Xometry Inc.

- Markforged Inc.

- Prodways Group

- Carbon Inc.

- Airbus (Additive Manufacturing activities)

- Boeing (Additive Manufacturing activities)

- Safran S.A. (Additive Manufacturing activities)

- Collins Aerospace (UTC)

Frequently Asked Questions

Analyze common user questions about the Additive Manufacturing for General Aviation market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is Additive Manufacturing for General Aviation?

Additive Manufacturing (AM), or 3D printing, for General Aviation involves using layered deposition processes to create aircraft components from digital designs. This includes parts for business jets, light aircraft, and helicopters, covering applications from prototyping and tooling to end-use flight-critical components and MRO.

What are the primary benefits of using Additive Manufacturing in General Aviation?

Key benefits include significant weight reduction for improved fuel efficiency, design freedom to create complex and optimized geometries, part consolidation to reduce assembly complexity, rapid prototyping for faster development cycles, and on-demand production of spare parts to minimize downtime and inventory costs.

Which materials are commonly used in Additive Manufacturing for General Aviation?

Commonly used materials include high-performance metals like titanium alloys, aluminum alloys, and nickel alloys, as well as engineering polymers such as PEEK and ULTEM, and advanced composite materials. Material selection depends on the specific application's structural, thermal, and environmental requirements.

What are the main challenges facing the adoption of Additive Manufacturing in General Aviation?

Major challenges include high initial capital investment for AM equipment, stringent and evolving regulatory certification processes for flight-critical parts, the need for standardized material properties and processes, and a shortage of skilled labor proficient in both AM technologies and aerospace engineering.

How is AI impacting Additive Manufacturing for General Aviation?

AI is significantly impacting AM by enabling generative design for optimal part structures, optimizing print parameters for improved quality, facilitating real-time quality control and defect detection during manufacturing, and supporting predictive maintenance for AM equipment, thereby enhancing overall efficiency and reliability.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted