eFuel Market

eFuel Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_707254 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

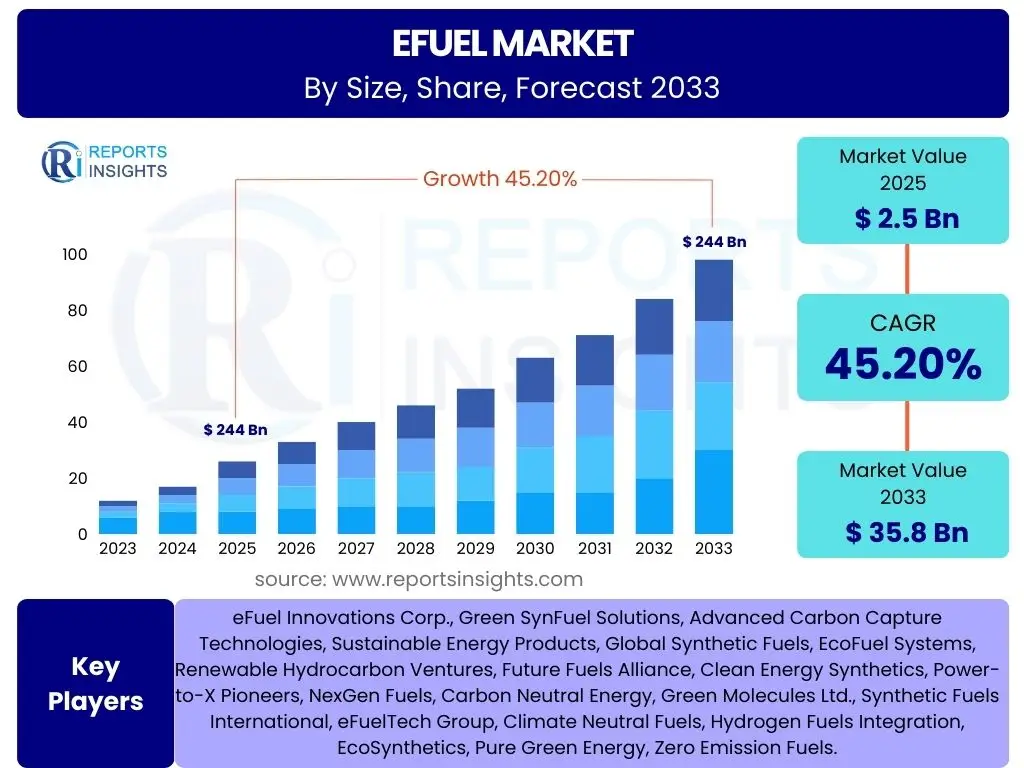

eFuel Market Size

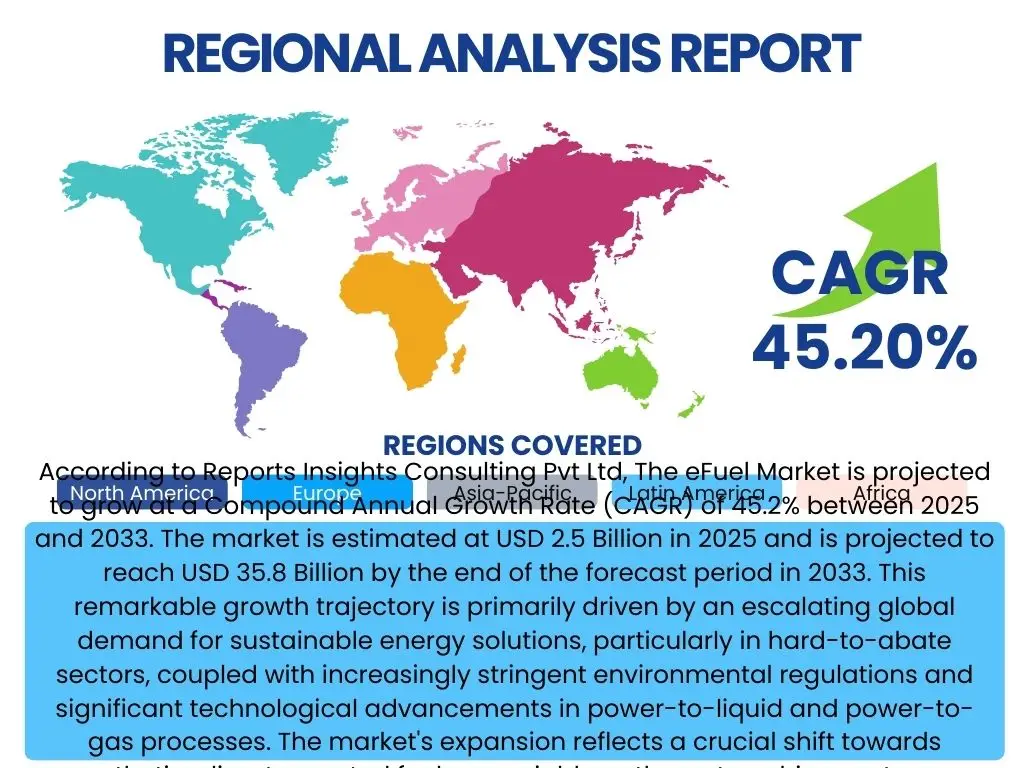

According to Reports Insights Consulting Pvt Ltd, The eFuel Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 45.2% between 2025 and 2033. The market is estimated at USD 2.5 Billion in 2025 and is projected to reach USD 35.8 Billion by the end of the forecast period in 2033. This remarkable growth trajectory is primarily driven by an escalating global demand for sustainable energy solutions, particularly in hard-to-abate sectors, coupled with increasingly stringent environmental regulations and significant technological advancements in power-to-liquid and power-to-gas processes. The market's expansion reflects a crucial shift towards synthetic, climate-neutral fuels as a viable pathway to achieve net-zero emission targets.

Key eFuel Market Trends & Insights

The eFuel market is currently experiencing dynamic evolution, driven by a confluence of global decarbonization imperatives and technological innovation. Common user inquiries frequently revolve around the viability of eFuels in various sectors, the integration of green hydrogen, and the role of government policies in accelerating adoption. Analysis reveals a prominent trend of increasing cross-sectoral interest, particularly from the aviation and maritime industries, which face immense challenges in reducing their carbon footprint through conventional electrification alone. This sustained demand from difficult-to-decarbonize sectors is a significant market driver, fostering research and development into scalable and cost-efficient eFuel production methods. Furthermore, the market is characterized by a strong emphasis on leveraging abundant renewable energy sources to produce green hydrogen, which serves as a critical feedstock for eFuel synthesis, thereby ensuring the fuels' carbon-neutral credentials. Policy support, including carbon pricing mechanisms and mandates for sustainable alternative fuels, continues to play a pivotal role in shaping market dynamics and investment flows.

Another notable trend is the escalating private and public investment in large-scale eFuel production facilities, signaling growing confidence in the commercial viability and long-term potential of these synthetic fuels. Companies are forming strategic partnerships across the value chain, from renewable energy generation to CO2 capture and eFuel distribution, to de-risk investments and accelerate market penetration. Technological advancements in catalyst development, electrolyzer efficiency, and carbon capture utilization (CCU) are continuously improving the overall energy conversion efficiency and economic feasibility of eFuel production. This focus on efficiency is crucial for addressing the energy intensity associated with eFuel synthesis, making the product more competitive with traditional fossil fuels. The industry is also witnessing an increasing emphasis on achieving standardized certification and regulatory frameworks, which are essential for market acceptance, international trade, and ensuring the environmental integrity of eFuels.

- Accelerated Decarbonization Push: Global commitments to net-zero emissions drive demand for carbon-neutral fuels.

- Rising Investment & Strategic Partnerships: Significant capital inflow and collaborative ventures across the eFuel value chain.

- Cross-Sectoral Adoption: Increasing interest and mandates from aviation, maritime, and heavy industry sectors.

- Technological Advancements: Improvements in Power-to-X processes, electrolyzer efficiency, and CO2 capture technologies.

- Integration with Green Hydrogen Economy: eFuels serve as a crucial derivative for green hydrogen, expanding its utility.

- Policy & Regulatory Support: Government incentives, carbon pricing, and blending mandates are fostering market growth.

- Focus on Scalability: Emphasis on developing large-scale production facilities to reduce costs and meet demand.

AI Impact Analysis on eFuel

User inquiries frequently explore how artificial intelligence can optimize the complex processes involved in eFuel production, from renewable energy management to chemical synthesis. The consensus points towards AI being a transformative force, capable of significantly enhancing efficiency, reducing operational costs, and accelerating the research and development lifecycle within the eFuel industry. AI algorithms can optimize the dispatch and utilization of intermittent renewable energy sources, ensuring a stable and cost-effective power supply for electrolyzers. Furthermore, predictive analytics and machine learning can be employed to monitor and control the complex chemical reactions involved in CO2 hydrogenation and Fischer-Tropsch synthesis, identifying optimal operating conditions and predicting equipment failures, thereby minimizing downtime and maximizing output. The data-intensive nature of eFuel production, encompassing diverse parameters from feedstock composition to reaction kinetics, creates an ideal environment for AI to derive actionable insights that human analysis might miss.

Beyond process optimization, AI's influence extends to supply chain management and market forecasting, addressing common user concerns about the logistical complexities of scaling eFuel production and distribution. AI-driven models can analyze vast datasets to forecast eFuel demand across different sectors and regions, enabling producers to optimize production schedules and inventory management, thereby reducing waste and ensuring timely supply. AI also plays a critical role in accelerating the discovery and development of new catalysts and materials for more efficient eFuel synthesis, significantly shortening the traditional R&D timeline. While the integration of AI presents challenges related to data privacy, cybersecurity, and the need for specialized expertise, its potential benefits in driving down costs, improving efficiency, and speeding up innovation are widely recognized as vital for the long-term competitiveness and scalability of the eFuel market.

- Optimized Renewable Energy Integration: AI manages intermittent solar and wind power for stable eFuel production.

- Enhanced Process Control & Efficiency: Machine learning optimizes chemical reactions and synthesis processes.

- Predictive Maintenance: AI algorithms predict equipment failures, reducing downtime and operational costs.

- Supply Chain Optimization: AI analyzes logistics for efficient feedstock procurement and eFuel distribution.

- Accelerated R&D and Material Discovery: AI speeds up the identification of new catalysts and production pathways.

- Improved Demand Forecasting: AI models predict market needs, enabling efficient production planning.

- Quality Control & Anomaly Detection: AI monitors production quality and identifies deviations in real-time.

Key Takeaways eFuel Market Size & Forecast

The eFuel market's projected growth trajectory, characterized by a substantial CAGR, reflects a critical global shift towards decarbonization across various industrial sectors. User inquiries frequently focus on understanding the primary drivers behind this rapid expansion and the segments expected to lead demand. The market is propelled by a confluence of factors, including increasingly ambitious national and international climate targets, the urgent need for sustainable solutions in hard-to-abate sectors like aviation and maritime transport, and significant governmental policy support through incentives and mandates. This robust growth indicates a strong market confidence in eFuels as a viable, long-term solution for achieving net-zero emissions where direct electrification is not feasible or practical.

A key takeaway from the market forecast is the pivotal role of technological advancements and scaling up production capacities. While eFuels currently face cost competitiveness challenges compared to traditional fossil fuels, continuous innovation in Power-to-X technologies, coupled with the decreasing cost of renewable electricity, is expected to narrow this gap over the forecast period. Furthermore, the market's future will be significantly shaped by the successful establishment of robust, geographically diverse supply chains and the development of clear international standards for eFuel production and trade. The significant investment flowing into this sector underscores the belief that eFuels will become an indispensable component of the future energy mix, driving the transition to a more sustainable global economy.

- Rapid Market Expansion: The eFuel market is poised for exceptional growth, driven by global decarbonization efforts.

- Strategic Importance for Hard-to-Abate Sectors: Critical for aviation, maritime, and heavy industry to meet emission targets.

- Strong Policy Tailwinds: Government mandates, incentives, and carbon pricing are accelerating adoption.

- Investment Momentum: Significant capital infusion into R&D and large-scale production facilities.

- Cost Reduction Potential: Technological advancements and scaling up production are expected to improve cost-competitiveness.

- Green Hydrogen Synergy: Growth is intrinsically linked to the expansion of green hydrogen infrastructure.

eFuel Market Drivers Analysis

The eFuel market is experiencing substantial growth propelled by several influential drivers, primarily stemming from the global imperative to mitigate climate change and achieve ambitious decarbonization targets. International agreements and national policies, such as the European Union's Fit for 55 package and various net-zero commitments, are creating a strong regulatory push for the adoption of sustainable fuels. This regulatory landscape is forcing industries, particularly those with high carbon footprints and limited electrification options, to seek alternative energy sources that can significantly reduce their greenhouse gas emissions. Coupled with this, a rising corporate focus on Environmental, Social, and Governance (ESG) criteria is leading companies across sectors to voluntarily invest in and adopt eFuels to meet their own sustainability objectives and enhance brand reputation.

Technological advancements in the Power-to-X processes, which convert renewable electricity into liquid or gaseous fuels using captured CO2, are making eFuel production more efficient and economically viable. Innovations in electrolyzer technology, CO2 capture solutions, and catalytic converters are continuously improving energy conversion rates and reducing overall production costs. Additionally, the increasing volatility and rising prices of fossil fuels, alongside the implementation of carbon pricing mechanisms, are creating a financial incentive for industries to transition towards more stable and environmentally friendly eFuel alternatives. The strategic importance of energy security, particularly in light of geopolitical uncertainties, also drives interest in domestic eFuel production, leveraging local renewable energy resources to reduce reliance on imported fossil fuels.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Decarbonization Mandates | +15% | Europe, North America, APAC | Short to Mid-Term (2025-2030) |

| Stringent Environmental Regulations | +12% | Europe, North America | Mid to Long-Term (2028-2033) |

| Technological Advancements in PtX | +10% | Global | Mid-Term (2027-2032) |

| Rising Corporate Sustainability Goals | +8% | Global | Short to Mid-Term (2025-2030) |

| Increasing Carbon Pricing Mechanisms | +7% | Europe, North America, Select APAC | Mid to Long-Term (2028-2033) |

eFuel Market Restraints Analysis

Despite the promising growth trajectory, the eFuel market faces several significant restraints that could impede its widespread adoption and scalability. Foremost among these is the high production cost of eFuels compared to conventional fossil fuels. The energy-intensive nature of the Power-to-X process, coupled with the current cost of green hydrogen production and carbon capture technologies, makes eFuels economically less competitive without substantial subsidies or carbon pricing mechanisms. This cost disparity presents a significant barrier to entry for many potential end-users and necessitates considerable financial incentives or regulatory pressure to drive adoption. Addressing this cost challenge is crucial for eFuels to move beyond niche applications and become a mainstream energy solution.

Another key restraint is the current limited availability of dedicated renewable energy infrastructure required for large-scale eFuel production. eFuel synthesis demands vast quantities of cheap, clean electricity, and the build-out of sufficient solar, wind, and other renewable energy capacities, along with the necessary grid infrastructure, is a time-consuming and capital-intensive endeavor. Furthermore, the nascent stage of the eFuel supply chain and distribution networks poses logistical challenges. Unlike well-established fossil fuel infrastructure, the specialized infrastructure for transporting and delivering eFuels is still under development, which can limit market reach and increase distribution costs. Finally, the energy efficiency losses inherent in the multi-step conversion process from renewable electricity to eFuels can be significant, raising questions about the overall energy footprint and resource optimization, especially when compared to direct electrification solutions where applicable.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Production Costs | -18% | Global | Short to Mid-Term (2025-2030) |

| Limited Renewable Energy Infrastructure | -15% | Global | Short to Mid-Term (2025-2030) |

| Scalability Challenges | -10% | Global | Short Term (2025-2027) |

| Nascent Supply Chain & Distribution | -8% | Global | Short to Mid-Term (2025-2030) |

eFuel Market Opportunities Analysis

The eFuel market presents significant opportunities for growth and innovation, particularly in addressing the decarbonization needs of sectors that are challenging to electrify directly. The aviation and maritime industries represent prime opportunities, as they currently lack viable zero-emission alternatives for long-haul transport and heavy-duty operations. eFuels, specifically eKerosene and eDiesel, offer a 'drop-in' solution, meaning they can utilize existing infrastructure, making them an attractive and relatively quick pathway to reduce emissions in these hard-to-abate segments. This inherent compatibility with current engine technologies and fuel distribution networks significantly lowers the barriers to adoption compared to entirely new propulsion systems. The increasing pressure from international bodies and national governments for these sectors to reduce their carbon footprint creates a captive and growing demand for eFuel solutions, driving investment and development.

Beyond transportation, the integration of eFuels into broader power-to-X ecosystems represents a substantial opportunity. This involves leveraging surplus renewable electricity to produce eFuels, which can then serve as energy storage, a chemical feedstock for industrial processes, or a source for grid balancing. The concept of carbon capture and utilization (CCU) further enhances the appeal of eFuels by transforming industrial CO2 emissions from a waste product into a valuable resource, closing the carbon loop and creating a truly circular economy. Additionally, emerging economies with abundant untapped renewable energy resources, such as those in Latin America, Africa, and parts of Asia, present greenfield opportunities for large-scale eFuel production tailored for both domestic consumption and export. These regions can leapfrog traditional fossil fuel development by directly investing in eFuel infrastructure, positioning themselves as future leaders in the global sustainable energy landscape.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Decarbonization of Aviation & Marine | +18% | Global | Short to Long-Term (2025-2033) |

| Integration with Power-to-X Ecosystem | +14% | Europe, North America | Mid to Long-Term (2028-2033) |

| Carbon Capture & Utilization (CCU) Synergy | +10% | Global | Mid-Term (2027-2032) |

| Untapped Renewable Energy Resources | +8% | Latin America, Africa, Australia | Long-Term (2030-2033) |

eFuel Market Challenges Impact Analysis

While the eFuel market holds immense promise, it is confronted by several significant challenges that could affect its growth trajectory and adoption rates. A primary concern is the inherent energy efficiency loss during the conversion process from renewable electricity to eFuels. Multiple energy conversion steps, including electrolysis, CO2 capture, and synthesis, result in substantial energy losses, making the overall process less efficient than direct electrification where feasible. This efficiency challenge impacts the economic viability of eFuels and necessitates a much larger input of renewable energy to produce a given amount of fuel, potentially increasing the demand on renewable energy infrastructure. Overcoming these energy losses through technological breakthroughs and process optimization is critical for the long-term sustainability and competitiveness of eFuels.

Another notable challenge is the intense competition from alternative decarbonization pathways, such as advanced biofuels, direct electrification, and hydrogen fuel cells. Each of these alternatives presents its own set of advantages and disadvantages depending on the specific application and sector, creating a complex competitive landscape for eFuels. Market players must clearly articulate the unique value proposition of eFuels, particularly for sectors where other options are less viable. Furthermore, the lack of universally accepted standardization and certification mechanisms for eFuels poses a significant hurdle to market development. Without clear and consistent global standards for production processes, quality, and sustainability criteria, consumer confidence and international trade could be inhibited. Finally, public perception and awareness of eFuels, their benefits, and their role in the energy transition remain relatively low. Educating stakeholders and the broader public about the distinct advantages and the carbon-neutral credentials of eFuels is essential for fostering wider acceptance and demand.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Energy Efficiency Losses | -12% | Global | Short to Mid-Term (2025-2030) |

| Competition from Alternative Fuels | -9% | Global | Short to Mid-Term (2025-2030) |

| Lack of Standardization & Certification | -7% | Global | Mid-Term (2027-2032) |

| Public Perception & Awareness | -5% | Global | Long-Term (2030-2033) |

eFuel Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global eFuel market, covering historical trends from 2019 to 2023, base year 2024, and offering a robust forecast spanning 2025 to 2033. The scope includes a detailed examination of market size, growth drivers, restraints, opportunities, and challenges influencing the industry landscape. Emphasis is placed on understanding key market trends, the impact of artificial intelligence, and a thorough segmentation analysis across various types, applications, and end-use sectors. The report also highlights regional market dynamics, identifying key countries and their contributions to the overall market trajectory. A dedicated section profiles leading market players, offering insights into their strategic initiatives and competitive positioning. The objective is to provide stakeholders with actionable intelligence for informed decision-making and strategic planning within the evolving eFuel ecosystem.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 2.5 Billion |

| Market Forecast in 2033 | USD 35.8 Billion |

| Growth Rate | 45.2% CAGR |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | eFuel Innovations Corp., Green SynFuel Solutions, Advanced Carbon Capture Technologies, Sustainable Energy Products, Global Synthetic Fuels, EcoFuel Systems, Renewable Hydrocarbon Ventures, Future Fuels Alliance, Clean Energy Synthetics, Power-to-X Pioneers, NexGen Fuels, Carbon Neutral Energy, Green Molecules Ltd., Synthetic Fuels International, eFuelTech Group, Climate Neutral Fuels, Hydrogen Fuels Integration, EcoSynthetics, Pure Green Energy, Zero Emission Fuels. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The eFuel market is meticulously segmented to provide a granular understanding of its diverse applications, production methods, and end-use sectors, enabling stakeholders to identify precise growth opportunities. This comprehensive segmentation reflects the versatility of eFuels in addressing various energy demands across the global economy. By dissecting the market into distinct categories based on fuel type, application, and end-use, the report offers detailed insights into the specific drivers and challenges pertinent to each segment. This analytical approach allows for a clearer picture of market dynamics, investment priorities, and the potential for eFuels to integrate into existing energy infrastructures, facilitating strategic planning for market participants.

The segmentation by type, specifically Power-to-Liquid and Power-to-Gas, highlights the different chemical pathways and resulting fuel forms, each with unique characteristics and suitability for various applications. The application segmentation, encompassing transportation, chemical feedstock, and heating & power generation, underscores the broad utility of eFuels beyond just mobility, showcasing their potential in industrial processes and energy storage. Furthermore, the end-use segmentation provides a deep dive into the specific industries that are poised to adopt eFuels, such as automotive, aviation, marine, and industrial sectors, revealing where demand is most concentrated and where eFuels offer the most compelling decarbonization solutions. This multi-dimensional segmentation ensures a comprehensive market overview, allowing for targeted strategies and resource allocation.

- By Type:

- Power-to-Liquid (eKerosene, eDiesel, eGasoline)

- Power-to-Gas (eMethane, eHydrogen)

- Other eFuels (e.g., eMethanol)

- By Application:

- Transportation (Aviation, Marine, Road, Rail)

- Chemical Feedstock

- Heating & Power Generation

- By End-Use:

- Automotive

- Aviation

- Marine

- Industrial

- Residential & Commercial

Regional Highlights

- Europe: Leading the global eFuel market due to ambitious decarbonization targets, stringent environmental regulations (e.g., Fit for 55 package, REPowerEU), and significant public and private investments in green hydrogen and Power-to-X projects. Countries like Germany, Norway, and the Netherlands are at the forefront of establishing large-scale eFuel production facilities and integrating eFuels into their energy strategies, particularly for aviation and maritime sectors.

- North America: Exhibiting robust growth driven by increasing corporate sustainability commitments, emerging policy support (e.g., Inflation Reduction Act in the U.S.), and a strong focus on technological innovation in carbon capture and utilization. The region is seeing significant R&D efforts and pilot projects aimed at scaling up eFuel production, with particular relevance for heavy-duty transportation and industrial applications.

- Asia Pacific (APAC): Poised for substantial market expansion due to rapid industrialization, increasing energy demand, and growing awareness of environmental concerns. Countries such as Australia, China, Japan, and India are investing in renewable energy infrastructure and exploring eFuels as a pathway to reduce reliance on fossil fuel imports and meet their climate goals, leveraging their vast renewable energy potential.

- Latin America: Emerging as a strategic region for eFuel production, capitalizing on its abundant and cost-effective renewable energy resources, particularly solar and wind. Countries like Chile and Brazil are positioning themselves as future exporters of green hydrogen and its derivatives, including eFuels, attracting international investments for large-scale production facilities.

- Middle East & Africa (MEA): Demonstrating growing interest in eFuel development, particularly in nations with significant renewable energy potential and strategic geographical locations. Countries like Saudi Arabia and the UAE are investing heavily in green hydrogen and ammonia projects, which serve as foundational elements for eFuel production, aiming to diversify their economies and become global leaders in sustainable energy exports.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the eFuel Market.- eFuel Innovations Corp.

- Green SynFuel Solutions

- Advanced Carbon Capture Technologies

- Sustainable Energy Products

- Global Synthetic Fuels

- EcoFuel Systems

- Renewable Hydrocarbon Ventures

- Future Fuels Alliance

- Clean Energy Synthetics

- Power-to-X Pioneers

- NexGen Fuels

- Carbon Neutral Energy

- Green Molecules Ltd.

- Synthetic Fuels International

- eFuelTech Group

- Climate Neutral Fuels

- Hydrogen Fuels Integration

- EcoSynthetics

- Pure Green Energy

- Zero Emission Fuels

Frequently Asked Questions

What are eFuels and how are they produced?

eFuels, or electrofuels, are synthetic fuels produced by combining green hydrogen (made from renewable electricity and water through electrolysis) with captured carbon dioxide. This Power-to-X process typically involves electrolysis to produce hydrogen, followed by a synthesis step (like Fischer-Tropsch) where hydrogen reacts with CO2 to create liquid or gaseous hydrocarbons. The carbon dioxide used is either captured directly from the air or from industrial emissions, making the fuels carbon-neutral when combusted.

What are the primary benefits of eFuels?

eFuels offer several key benefits, including their carbon-neutrality, as they only release the CO2 that was previously captured. They are 'drop-in' fuels, meaning they can utilize existing internal combustion engine technology and fuel infrastructure without modifications, which simplifies adoption. eFuels are particularly beneficial for hard-to-abate sectors like aviation, shipping, and heavy industry where direct electrification is challenging, providing a crucial pathway to decarbonization.

What are the main challenges facing the eFuel market?

The primary challenges include high production costs compared to fossil fuels, largely due to the energy-intensive conversion processes and the current cost of green hydrogen and carbon capture. Additionally, significant energy efficiency losses occur during production, and the industry faces limitations in the availability of large-scale renewable energy infrastructure. The lack of standardized certification and nascent supply chains also present hurdles for widespread adoption.

Which sectors are expected to drive the demand for eFuels?

The aviation and maritime sectors are anticipated to be the primary drivers of eFuel demand. These industries face immense pressure to decarbonize but have limited alternative solutions for long-haul transport. eFuels offer a viable and immediate path to reduce emissions while leveraging existing fleets and infrastructure. Heavy-duty road transport and certain industrial applications also represent significant demand opportunities for eFuels.

What is the future outlook for the eFuel market?

The eFuel market is projected for significant growth, driven by escalating global decarbonization efforts, increasing regulatory support, and continuous technological advancements. While current costs and infrastructure limitations pose challenges, ongoing investments in R&D and scaling up production capacities are expected to improve economic viability. eFuels are seen as an indispensable component of the future energy mix, particularly for sectors difficult to electrify, contributing significantly to achieving net-zero emission targets.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted