CPV Solar Market

CPV Solar Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_706832 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

CPV Solar Market Size

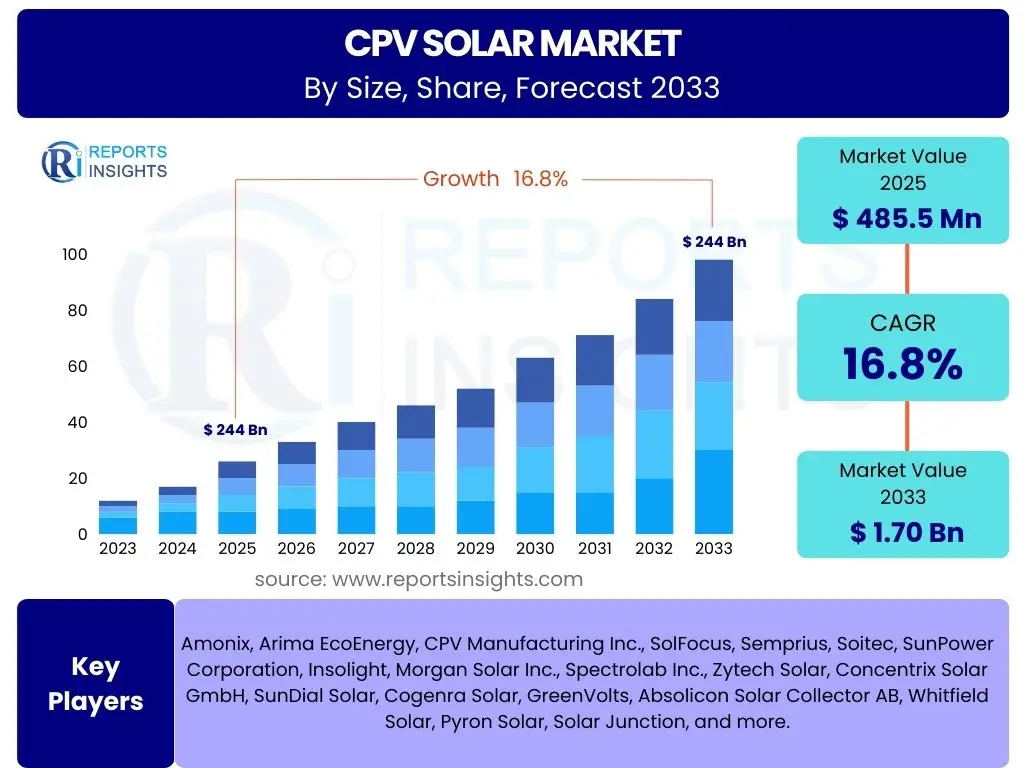

According to Reports Insights Consulting Pvt Ltd, The CPV Solar Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 16.8% between 2025 and 2033. The market is estimated at USD 485.5 Million in 2025 and is projected to reach USD 1.70 Billion by the end of the forecast period in 2033.

The Concentrated Photovoltaic (CPV) Solar Market is experiencing robust growth driven by its inherent advantages in specific solar energy applications. Unlike traditional flat-panel photovoltaic systems, CPV technology utilizes lenses or mirrors to focus a large amount of sunlight onto small, highly efficient multi-junction solar cells. This unique approach allows CPV systems to achieve significantly higher efficiencies, particularly in regions with high direct normal irradiance (DNI), which refers to the amount of solar radiation received per unit area by a surface that is always held perpendicular to the rays of the sun. The market's expansion is predominantly fueled by increasing global demand for renewable energy sources and the continuous advancements in CPV cell efficiency and tracking technologies.

Despite being a niche segment within the broader solar industry, CPV is gaining traction for its suitability in utility-scale projects where land utilization efficiency and high power output per area are critical. Its ability to perform optimally in hot climates, coupled with a smaller physical footprint for equivalent power output compared to conventional PV, positions it as an attractive alternative for specific geographic locations. The projected growth reflects a maturing technology and growing investment, indicating a positive outlook for CPV solutions as energy grids increasingly integrate diverse renewable energy portfolios to meet escalating demands and achieve carbon reduction targets.

Key CPV Solar Market Trends & Insights

Common user questions regarding CPV Solar market trends and insights frequently revolve around the technology's competitive edge, its deployment scalability, and future integration with grid infrastructure. Users are keen to understand if CPV can overcome its historical cost barriers, how it compares to conventional PV in various climates, and what innovations are driving its efficiency and reliability. There is also significant interest in its role within the broader energy transition, particularly concerning its potential in high direct normal irradiance regions and its synergy with emerging energy storage solutions. Insights reveal a market moving towards greater technological refinement and strategic application.

- Increased focus on High Concentration Photovoltaic (HCPV) systems due to their superior efficiency gains in direct sunlight conditions.

- Continuous advancements in multi-junction solar cell technology, pushing conversion efficiencies beyond 40% in laboratory settings and enhancing commercial viability.

- Integration of advanced dual-axis tracking systems to maximize solar energy capture throughout the day and across seasons, optimizing energy yield.

- Development of hybrid CPV-thermal systems that capture both electricity and heat, improving overall system energy utilization.

- Strategic deployment in high direct normal irradiance (DNI) regions such as deserts and arid zones, where CPV offers significant performance advantages over traditional PV.

- Growing investment in research and development to reduce manufacturing costs and improve module durability, addressing historical adoption barriers.

- Increasing interest from utility-scale project developers seeking high-performance, land-efficient solar solutions for specific grid requirements.

AI Impact Analysis on CPV Solar

User inquiries concerning the impact of Artificial Intelligence (AI) on the CPV Solar market primarily center on optimizing system performance, predicting energy output, and enhancing operational efficiency. Stakeholders are keen to understand how AI can mitigate the complexities associated with CPV's tracking mechanisms and sensitive cell technology, improve reliability, and potentially lower overall operational expenditures. Questions also arise regarding AI's role in grid integration, fault detection, and real-time energy management to maximize the economic viability of CPV installations. The consensus is that AI offers transformative potential for CPV, moving it from a niche solution to a more streamlined and competitive renewable energy option.

The integration of AI into CPV solar systems is poised to revolutionize their design, operation, and maintenance. AI algorithms can analyze vast datasets from weather patterns, solar irradiance, and historical performance to optimize the precise movement of dual-axis trackers, ensuring maximum sunlight capture throughout the day. This real-time optimization significantly boosts energy yield and overall system efficiency. Furthermore, AI-powered predictive maintenance can monitor the health of CPV components, such as optics, cells, and tracking motors, identifying potential failures before they occur. This proactive approach minimizes downtime, reduces maintenance costs, and extends the operational lifespan of CPV installations, making them more reliable and economically attractive.

- AI-powered predictive analytics for solar tracking optimization, maximizing direct normal irradiance (DNI) capture and energy yield.

- Implementation of machine learning algorithms for enhanced fault detection and diagnostics in CPV modules and tracking systems, reducing downtime.

- AI-driven forecasting models to predict CPV energy output with higher accuracy, facilitating better grid integration and energy management.

- Optimization of CPV system design and material selection through AI simulations, leading to improved efficiency and reduced manufacturing costs.

- Automated monitoring and control systems for CPV plants, allowing for remote management and real-time performance adjustments.

- AI-enhanced resource allocation and scheduling for CPV deployment projects, improving logistical efficiency and reducing installation times.

- Development of intelligent energy management systems that integrate CPV output with battery storage and grid demand using AI for optimal energy distribution.

Key Takeaways CPV Solar Market Size & Forecast

Common user questions about key takeaways from the CPV Solar market size and forecast often focus on understanding the primary growth drivers, the technology's long-term viability, and its competitive standing against other renewable energy sources. Users seek clarity on where CPV technology is most likely to thrive, what factors could accelerate or hinder its adoption, and whether it represents a significant investment opportunity. Insights indicate a market with specialized applications, poised for steady growth in specific high-DNI regions, underpinned by efficiency gains and declining costs, positioning it as a strategic component of a diversified renewable energy portfolio rather than a mass-market solution.

The CPV Solar market is set for sustained growth, primarily driven by its unparalleled efficiency in high direct normal irradiance (DNI) environments and continuous technological advancements in multi-junction solar cells and tracking systems. While it remains a niche segment compared to conventional PV, its high power density and efficient land use make it particularly attractive for utility-scale projects in sun-rich regions. The market's future expansion hinges on further cost reductions through manufacturing scale-up and ongoing research, as well as overcoming initial capital investment challenges. Its specialized applications and superior performance in specific climatic conditions ensure its distinct role in the global renewable energy landscape, offering significant opportunities for specialized investors and developers.

- The CPV market is projected for significant growth, reaching USD 1.70 Billion by 2033, driven by increasing demand for high-efficiency solar solutions.

- Technological advancements in multi-junction cells and precision tracking are critical enablers for CPV's improved performance and cost-effectiveness.

- CPV systems offer superior efficiency in regions with high direct normal irradiance (DNI), making them a preferred choice for utility-scale projects in such areas.

- Investment in research and development is focused on reducing the balance of system (BoS) costs and enhancing overall system reliability, fostering broader adoption.

- Despite being a niche market, CPV is vital for diversified renewable energy portfolios, especially where land efficiency and high power output are paramount.

CPV Solar Market Drivers Analysis

The CPV Solar market is propelled by a confluence of factors that underscore its unique advantages in the renewable energy sector. A primary driver is its inherent ability to achieve significantly higher energy conversion efficiencies compared to traditional silicon-based photovoltaic panels, especially when exposed to direct sunlight. This superior efficiency translates into more power generated from a smaller land area, making CPV an attractive option for large-scale utility projects where land availability or cost is a constraint. Furthermore, the continuous global push towards decarbonization and the stringent mandates for increased renewable energy adoption worldwide are creating a robust demand environment for all forms of clean energy, including highly efficient CPV technologies. Government incentives and supportive policies, particularly in sun-drenched regions, further stimulate investment and deployment.

Technological advancements also serve as a crucial driver for the CPV market. Breakthroughs in multi-junction solar cell technology, which are central to CPV systems, have consistently pushed efficiency boundaries, making the technology more competitive. Improved optics and precision tracking systems ensure that focused sunlight is optimally directed onto these advanced cells throughout the day, maximizing energy capture. Moreover, the increasing awareness of environmental benefits and the long-term operational savings associated with renewable energy sources are encouraging utility companies and industrial players to integrate CPV into their energy mix. As manufacturing processes become more refined and economies of scale are achieved, the declining cost per watt of CPV systems is expected to accelerate its market penetration in target applications and regions.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Efficiency in Direct Sunlight | +4.5% | MEA, APAC (Australia, India), North America (Southwest US), Latin America | 2025-2033 (Mid-Long Term) |

| Reduced Land Use for Equivalent Power | +3.8% | Europe, APAC ( densely populated areas), North America | 2025-2033 (Mid-Long Term) |

| Supportive Government Policies & Incentives for Renewables | +3.2% | Global (Specific policies vary by country/region) | 2025-2030 (Mid Term) |

| Advancements in Multi-junction Cell Technology | +3.0% | Global (Technology development centers: Europe, North America, APAC) | 2025-2033 (Mid-Long Term) |

CPV Solar Market Restraints Analysis

Despite its advantages, the CPV Solar market faces several significant restraints that impede its broader adoption. A primary challenge remains the relatively high initial capital expenditure (CAPEX) compared to conventional flat-panel PV systems. The sophisticated optics, precision tracking mechanisms, and expensive multi-junction solar cells contribute to higher upfront costs, making CPV less competitive in applications where cost-effectiveness is the paramount decision factor. This high initial investment can be a deterrent for potential investors and project developers, particularly in regions where financial incentives for CPV are less robust or readily available. The payback period for CPV projects can also be longer, further impacting investment decisions.

Another critical restraint is the inherent dependence of CPV systems on high direct normal irradiance (DNI). CPV technology performs optimally only when sunlight is directly focused onto its cells, making it less suitable for regions with diffuse sunlight, cloudy conditions, or high atmospheric aerosols. This limits its geographical applicability to primarily sun-belt regions, thereby restricting its global market potential. Furthermore, the mechanical complexity of dual-axis tracking systems, which are essential for CPV's efficiency, can lead to increased maintenance requirements and potential failure points compared to static PV installations. The competition from rapidly maturing and cost-decreasing conventional silicon PV technologies also poses a significant restraint, as traditional PV continues to capture a dominant share of the solar market due to its versatility, lower cost, and simpler installation processes across diverse environments.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Capital Expenditure (CAPEX) | -3.5% | Global (Impacts emerging and cost-sensitive markets most) | 2025-2030 (Mid Term) |

| Dependence on High Direct Normal Irradiance (DNI) | -3.0% | Regions with high cloud cover or diffuse light (e.g., Northern Europe, parts of Southeast Asia) | 2025-2033 (Mid-Long Term) |

| Complexity of Tracking Systems & Maintenance | -2.8% | Global (Affects operational costs and reliability) | 2025-2033 (Mid-Long Term) |

| Strong Competition from Conventional PV | -2.5% | Global (Especially in regions not optimal for DNI) | 2025-2033 (Mid-Long Term) |

CPV Solar Market Opportunities Analysis

The CPV Solar market, despite its current niche status, is presented with several compelling opportunities for growth and expansion. One significant opportunity lies in the burgeoning demand for highly efficient solar solutions in specific high-direct normal irradiance (DNI) geographies such as the arid regions of the Middle East, North Africa, parts of Latin America, and the southwestern United States. These areas, characterized by abundant direct sunlight, are ideal for CPV deployments, enabling the technology to showcase its superior performance capabilities and achieve optimal energy yields. As these regions continue to invest heavily in renewable energy infrastructure, the demand for specialized, high-performance solar technologies like CPV is expected to surge, creating a fertile ground for market penetration and expansion.

Another crucial opportunity stems from the ongoing advancements in research and development within the solar industry. Continuous innovation in multi-junction solar cell efficiency, material science, and optical design can significantly improve the performance-to-cost ratio of CPV systems. Furthermore, the development of hybrid CPV-thermal systems, which simultaneously generate electricity and useful heat, presents an avenue for enhanced overall energy utilization, particularly in industrial or commercial applications requiring both forms of energy. The integration of CPV with energy storage solutions, such as battery energy storage systems, can also address intermittency issues and enhance grid stability, broadening CPV's applicability. Lastly, the growth of smart grid initiatives and the increasing sophistication of energy management systems worldwide offer opportunities for CPV systems to be seamlessly integrated into complex power networks, optimizing their output and contributing effectively to grid stability and energy security.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into High DNI Emerging Markets | +4.0% | MEA, Latin America, APAC (Australia, India) | 2025-2033 (Mid-Long Term) |

| Technological Breakthroughs in Cell Efficiency & Optics | +3.7% | Global (R&D hubs: North America, Europe, East Asia) | 2025-2033 (Mid-Long Term) |

| Development of Hybrid CPV-Thermal Systems | +3.0% | Global (Industrial, Commercial applications) | 2027-2033 (Long Term) |

| Integration with Energy Storage Solutions | +2.5% | Global (Enhances grid stability) | 2026-2033 (Mid-Long Term) |

CPV Solar Market Challenges Impact Analysis

The CPV Solar market faces several inherent challenges that require innovative solutions to ensure its sustained growth and broader adoption. One significant challenge is the intermittency of solar energy, which applies more acutely to CPV due to its reliance on direct sunlight. Cloud cover or atmospheric aerosols can severely impact performance, leading to fluctuating power output and requiring sophisticated grid integration strategies or robust energy storage solutions. This intermittency makes grid operators hesitant to rely solely on CPV for baseload power, necessitating hybrid solutions or greater grid flexibility, which adds to system complexity and cost. Furthermore, the relatively low public awareness and understanding of CPV technology, compared to conventional PV, contribute to slower market acceptance and perceived risk among potential investors and end-users.

Another major challenge revolves around the complex supply chain and manufacturing processes associated with CPV systems. The production of high-efficiency multi-junction cells, precision optics, and advanced tracking mechanisms requires specialized expertise and infrastructure, which can limit the scalability of production and drive up costs. Unlike the highly standardized and mass-produced components of traditional PV, CPV components often involve more niche suppliers and bespoke manufacturing, which can lead to higher per-unit costs and longer lead times. Additionally, the need for precise installation and commissioning, given the sensitive nature of the optical alignment and tracking systems, adds to the overall project complexity and can deter developers who prefer simpler, plug-and-play solutions. Addressing these challenges will necessitate substantial investment in R&D, manufacturing scale-up, and strategic partnerships across the value chain.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intermittency and Grid Integration Issues | -3.0% | Global (Requires robust grid infrastructure) | 2025-2033 (Mid-Long Term) |

| Complex Supply Chain and Manufacturing | -2.7% | Global (Impacts cost and scalability) | 2025-2030 (Mid Term) |

| Limited Public Awareness and Acceptance | -2.5% | Global (Affects market adoption outside niche areas) | 2025-2033 (Mid-Long Term) |

| High Installation Precision and O&M Costs | -2.0% | Global (Adds to total cost of ownership) | 2025-2033 (Mid-Long Term) |

CPV Solar Market - Updated Report Scope

This comprehensive market research report on the CPV Solar market provides an in-depth analysis of the industry's current landscape, historical performance, and future growth trajectories. The report meticulously covers market size estimations, growth drivers, prevailing restraints, emerging opportunities, and critical challenges impacting the sector. It offers a detailed segmentation analysis, dissecting the market by various types, applications, components, and end-use industries, providing granular insights into specific market dynamics. Furthermore, a thorough regional analysis highlights key geographical contributions and growth prospects across major global regions, offering a holistic view of the CPV solar ecosystem.

The scope extends to a competitive landscape assessment, profiling key market players, their strategic initiatives, product offerings, and market positioning. This includes an evaluation of their strengths, weaknesses, opportunities, and threats (SWOT analysis) to understand the competitive intensity within the market. The report also incorporates an AI impact analysis, assessing how artificial intelligence is shaping the CPV solar industry, from system optimization to predictive maintenance. Ultimately, this document serves as a strategic tool for stakeholders, investors, and industry participants seeking to make informed decisions and capitalize on the evolving opportunities within the CPV solar market over the forecast period.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 485.5 Million |

| Market Forecast in 2033 | USD 1.70 Billion |

| Growth Rate | 16.8% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Amonix, Arima EcoEnergy, CPV Manufacturing Inc., SolFocus, Semprius, Soitec, SunPower Corporation, Insolight, Morgan Solar Inc., Spectrolab Inc., Zytech Solar, Concentrix Solar GmbH, SunDial Solar, Cogenra Solar, GreenVolts, Absolicon Solar Collector AB, Whitfield Solar, Pyron Solar, Solar Junction, and more. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The CPV Solar market is meticulously segmented to provide a granular understanding of its diverse applications and technological nuances. This segmentation highlights the specific characteristics and growth drivers within each sub-market, offering valuable insights for strategic decision-making. By type, the market is bifurcated into High Concentration Photovoltaic (HCPV) and Low Concentration Photovoltaic (LCPV), each catering to different levels of sun concentration and efficiency requirements. HCPV systems, with their superior efficiency, are typically deployed in large-scale utility projects in high Direct Normal Irradiance (DNI) regions, while LCPV systems offer a more robust and cost-effective solution for less stringent DNI conditions or smaller applications. Understanding these distinctions is crucial for identifying optimal deployment scenarios and investment opportunities.

Further segmentation by application categorizes CPV deployment across utility-scale, commercial & industrial, distributed generation, and off-grid scenarios. Utility-scale applications represent the largest segment, driven by the need for high power output and land-efficient solutions for grid-connected power generation. The component-wise breakdown provides insight into the value chain, covering concentrators (primary and secondary optics), solar cells (multi-junction and silicon), tracking systems (single-axis and dual-axis), inverters, and other balance of system components. This detailed analysis allows stakeholders to identify key technological drivers and investment areas within the CPV supply chain. Lastly, the end-use segmentation outlines the diverse sectors benefiting from CPV technology, including conventional power generation, specialized applications in space & satellite, defense & aerospace, and ongoing research & development initiatives, showcasing the versatile potential of CPV beyond just terrestrial power grids.

- By Type:

- High Concentration Photovoltaic (HCPV): Systems utilizing high concentration ratios (typically 300-1000 suns), requiring precise tracking and multi-junction cells for maximum efficiency in high DNI regions.

- Low Concentration Photovoltaic (LCPV): Systems with lower concentration ratios (2-100 suns), offering more forgiving tracking requirements and potentially lower costs, suitable for broader applications.

- By Application:

- Utility-Scale: Large-scale power plants connected to the main electricity grid, leveraging CPV's high efficiency for significant power generation.

- Commercial & Industrial: On-site power generation for businesses and industries seeking to reduce electricity costs and carbon footprint, often in conjunction with energy storage.

- Distributed Generation: Smaller, localized power generation systems, potentially including rooftop or ground-mounted installations for specific community or industrial needs.

- Off-Grid: Remote power solutions for areas without grid access, where CPV's efficiency can provide reliable energy with less land use than conventional PV.

- By Component:

- Concentrators: Primary optics (Fresnel lenses, parabolic mirrors) and secondary optics (homogenizers, non-imaging concentrators) for focusing sunlight.

- Solar Cells: Multi-junction Cells (GaAs-based, III-V compounds for high efficiency) and Silicon Cells (specialized high-efficiency silicon cells for LCPV).

- Tracking Systems: Single-axis (tilts along one axis) and Dual-axis (tilts along two axes for precise sun tracking) for optimal light capture.

- Inverters: Convert DC power generated by CPV modules into AC power suitable for grid or consumption.

- Other Balance of System Components: Wiring, mounting structures, control systems, cooling systems, and electrical hardware.

- By End-Use:

- Power Generation: Primary application for grid-connected electricity production.

- Space & Satellite: Niche but high-value application for power generation in space due to high efficiency and power-to-weight ratio.

- Defense & Aerospace: Specialized power needs for military bases, remote sensing, or aerospace applications.

- Research & Development: Ongoing activities to improve CPV technology, explore new materials, and enhance system integration.

Regional Highlights

The global CPV Solar market exhibits distinct regional dynamics, influenced by varying direct normal irradiance (DNI) levels, regulatory frameworks, technological adoption rates, and economic conditions. North America, particularly the southwestern United States and Mexico, presents a significant market for CPV due to its abundant DNI resources and supportive renewable energy policies. States like California, Arizona, and Nevada have been early adopters of CPV technology for utility-scale projects, driven by mandates for clean energy and the suitability of arid climates for CPV performance. The region continues to see investments in R&D and pilot projects aimed at further improving CPV system efficiency and reducing costs, positioning it as a key innovation hub.

Asia Pacific (APAC) is emerging as a critical growth region, spearheaded by countries like China, India, and Australia. While China has largely focused on conventional PV, its vast land area and ambitious renewable energy targets present opportunities for CPV in high DNI zones. India's growing energy demand and significant solar resources make it a promising market for CPV, particularly for utility-scale deployments and remote electrification projects. Australia, with its high DNI levels and commitment to large-scale solar farms, is also an attractive market for CPV. The Middle East and Africa (MEA) region, with its exceptionally high DNI and substantial investment in large-scale solar projects, stands out as a high-potential market. Countries like Saudi Arabia, UAE, and South Africa are exploring CPV for their ambitious renewable energy roadmaps, leveraging its efficiency in desert environments. Latin America, particularly countries like Chile and Brazil, also offers strong potential due to high DNI, increasing energy demand, and supportive government policies aimed at diversifying their energy mix with renewables.

Europe, while having a strong overall renewable energy market, faces more varied DNI levels, limiting the widespread applicability of CPV to specific Southern European countries such as Spain, Italy, and Greece. These countries, characterized by sunnier climates, have seen some CPV installations and research initiatives. The European Union's strong emphasis on energy efficiency and diversified renewable portfolios could drive niche CPV adoption in suitable locations, especially for applications prioritizing high energy density over pure cost competitiveness. Overall, the market's regional distribution underscores CPV's specialized role, thriving where its unique characteristics align best with climatic conditions and strategic energy objectives.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the CPV Solar Market.- Amonix

- Arima EcoEnergy

- CPV Manufacturing Inc.

- SolFocus

- Semprius

- Soitec

- SunPower Corporation

- Insolight

- Morgan Solar Inc.

- Spectrolab Inc.

- Zytech Solar

- Concentrix Solar GmbH

- SunDial Solar

- Cogenra Solar

- GreenVolts

- Absolicon Solar Collector AB

- Whitfield Solar

- Pyron Solar

- Solar Junction

Frequently Asked Questions

Analyze common user questions about the CPV Solar market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is CPV Solar technology and how does it differ from traditional PV?

CPV, or Concentrated Photovoltaic technology, uses lenses or mirrors to focus sunlight onto small, highly efficient multi-junction solar cells. Unlike traditional PV (photovoltaic) panels that use flat silicon cells to absorb diffuse and direct sunlight, CPV systems require direct sunlight and precise sun tracking to operate effectively. This concentration allows CPV to achieve significantly higher energy conversion efficiencies, often exceeding 40% in lab settings, compared to conventional PV which typically ranges from 15-22%. While traditional PV is more versatile for varied light conditions, CPV excels in regions with high direct normal irradiance (DNI), offering greater power output per unit area and reduced material use for the active solar cell material.

What are the primary advantages of CPV Solar systems?

The primary advantages of CPV Solar systems include their superior energy conversion efficiency, particularly in high direct normal irradiance (DNI) conditions. This high efficiency translates to more electricity generated from a smaller land footprint, making CPV ideal for utility-scale projects where land availability is a concern. CPV cells also perform better in hot climates compared to traditional silicon PV cells, as they are less susceptible to efficiency degradation at higher temperatures, often employing advanced cooling mechanisms. Furthermore, the use of highly efficient multi-junction cells in CPV reduces the amount of expensive semiconductor material needed for a given power output, contributing to long-term cost-effectiveness and resource efficiency.

What are the main challenges hindering the widespread adoption of CPV Solar?

The widespread adoption of CPV Solar technology is primarily hindered by several key challenges. Firstly, CPV systems typically have a higher initial capital expenditure (CAPEX) compared to conventional PV due to the complexity of precision optics, multi-junction cells, and dual-axis tracking systems. Secondly, CPV's performance is highly dependent on high direct normal irradiance (DNI), limiting its optimal deployment to sun-belt regions with clear skies and direct sunlight, making it less suitable for areas with diffuse light or frequent cloud cover. Thirdly, the mechanical complexity of the tracking systems can lead to increased maintenance requirements and potential points of failure. Lastly, strong competition from rapidly declining costs of conventional silicon PV, coupled with lower public awareness of CPV, further complicates its market penetration outside of niche applications.

In which regions is CPV Solar technology most effective and why?

CPV Solar technology is most effective in regions characterized by high direct normal irradiance (DNI) levels and clear skies, where sunlight is abundant and direct. These areas typically include arid and semi-arid regions near the equator, such as the southwestern United States (e.g., California, Arizona), parts of the Middle East and North Africa (e.g., Saudi Arabia, UAE), Latin America (e.g., Chile, Mexico), and Australia. The effectiveness stems from CPV's design, which relies on focusing direct sunlight onto highly efficient cells. In these environments, CPV systems can achieve their maximum conversion efficiencies and yield higher energy outputs per unit area, making them economically viable and technically superior compared to conventional PV that performs optimally under both direct and diffuse light.

How is Artificial Intelligence (AI) impacting the CPV Solar market?

Artificial Intelligence (AI) is significantly impacting the CPV Solar market by enhancing operational efficiency, optimizing performance, and improving predictive capabilities. AI algorithms can be deployed to fine-tune the precise dual-axis tracking systems of CPV modules, ensuring they consistently align with the sun's position for maximum direct light capture, thereby boosting energy yield. AI-driven predictive maintenance analyzes performance data to detect anomalies and anticipate equipment failures in optics, cells, or tracking mechanisms, reducing downtime and maintenance costs. Furthermore, AI is used for more accurate energy output forecasting, crucial for better grid integration and energy management. These applications of AI are making CPV systems more reliable, efficient, and cost-effective, helping to overcome some of their historical operational challenges.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted