Backhoe Loader Market

Backhoe Loader Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703202 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

Backhoe Loader Market Size

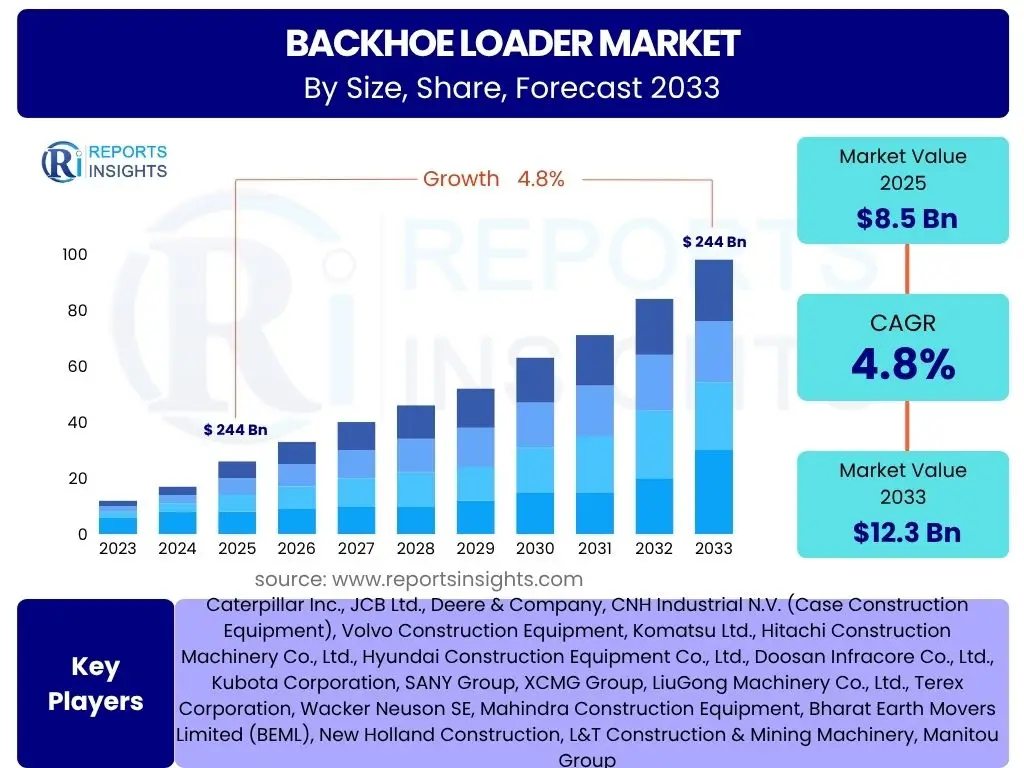

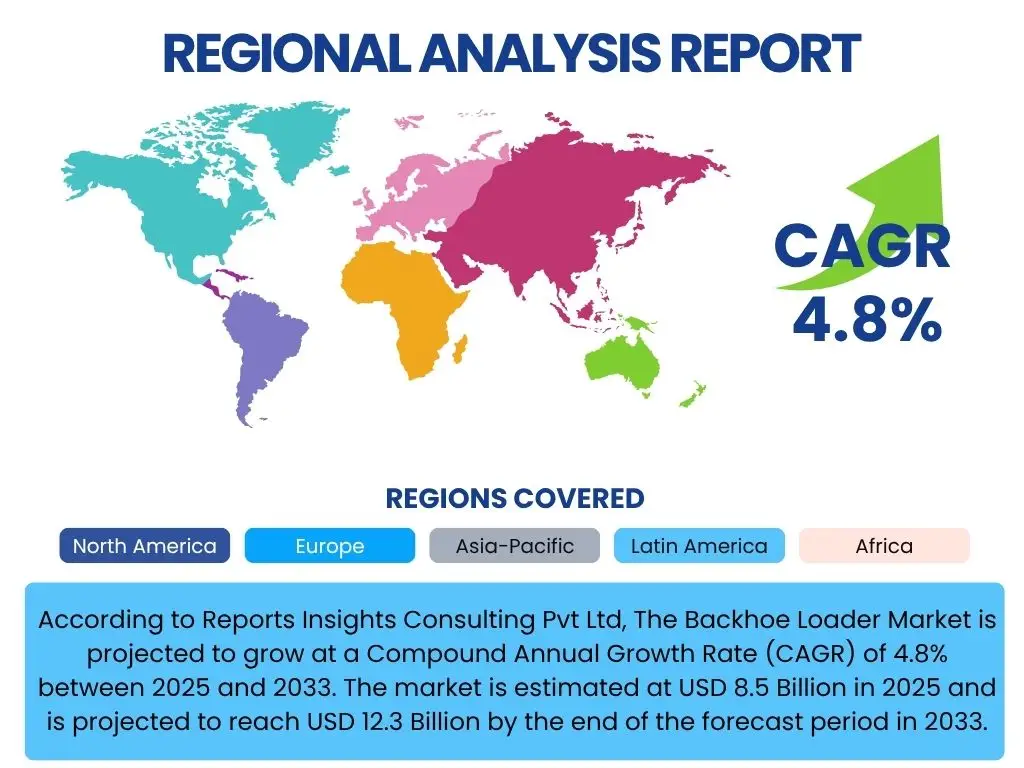

According to Reports Insights Consulting Pvt Ltd, The Backhoe Loader Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.8% between 2025 and 2033. The market is estimated at USD 8.5 Billion in 2025 and is projected to reach USD 12.3 Billion by the end of the forecast period in 2033.

Key Backhoe Loader Market Trends & Insights

The Backhoe Loader market is undergoing significant transformations driven by a confluence of technological advancements, evolving construction practices, and increasing demand from developing economies. A key trend is the growing emphasis on automation and smart technologies, which enhance operational efficiency, reduce labor costs, and improve safety on job sites. This includes features such as telematics for remote monitoring, GPS-enabled guidance systems, and advanced hydraulics for precise control, making machines more versatile and user-friendly. Furthermore, the adoption of sustainable and energy-efficient solutions, including electric and hybrid models, is gaining momentum as environmental regulations become stricter and operational costs for fuel rise.

Another prominent trend is the increasing demand for compact and versatile backhoe loaders, particularly in urban environments where space is limited and maneuverability is critical. These smaller machines offer excellent agility and can perform a wide range of tasks, from excavation and trenching to material handling and loading, making them indispensable for utility work, road maintenance, and residential construction. The rental market for backhoe loaders is also experiencing robust growth, driven by contractors seeking cost-effective solutions and flexibility in managing their equipment fleets without the burden of significant capital investment. This trend supports the wider accessibility of advanced machinery, even for smaller projects or companies.

Moreover, customization and modular design are becoming more prevalent, allowing operators to tailor backhoe loaders with various attachments and configurations to suit specific project requirements. This adaptability enhances the machine's utility across diverse applications, from agricultural tasks to specialized industrial operations. The integration of advanced safety features, such as improved visibility, collision avoidance systems, and ergonomic cabins, also reflects a strong market focus on operator well-being and regulatory compliance. These innovations collectively contribute to a more productive, safer, and environmentally conscious backhoe loader market.

- Growing adoption of advanced telematics and IoT for remote monitoring and predictive maintenance.

- Increased demand for compact and versatile backhoe loaders for urban and utility projects.

- Shift towards electric and hybrid models driven by environmental regulations and fuel efficiency concerns.

- Rise in the popularity of the equipment rental market.

- Enhanced focus on operator comfort and safety through ergonomic designs and advanced safety features.

- Integration of smart attachments and quick-change systems for greater versatility.

- Emphasis on fuel efficiency and reduced emissions across the product range.

AI Impact Analysis on Backhoe Loader

The integration of Artificial Intelligence (AI) into backhoe loaders represents a transformative shift, addressing core user concerns related to operational efficiency, cost management, and precision. Users are particularly keen on how AI can automate repetitive tasks, thereby reducing operator fatigue and increasing overall productivity. Predictive maintenance powered by AI algorithms is a significant area of interest, promising to minimize downtime by forecasting potential equipment failures before they occur. This capability leverages real-time sensor data and historical performance metrics to optimize maintenance schedules, directly impacting operational uptime and reducing unexpected repair costs. Furthermore, AI's role in optimizing fuel consumption and operational routes is seen as a critical benefit, aligning with environmental sustainability goals and direct cost savings for operators.

Beyond maintenance and efficiency, users anticipate AI to enhance safety features and improve the precision of complex operations. AI-driven systems can monitor the working environment, detect potential hazards, and assist operators in challenging conditions, such as working near obstacles or in low visibility. The development of semi-autonomous or fully autonomous backhoe loaders, though still nascent, holds immense potential for large-scale construction projects, mining, and hazardous environments where human presence can be minimized. This advancement addresses concerns about skilled labor shortages and aims to achieve consistent, high-quality output regardless of operator experience. The eventual goal is a more intelligent, responsive, and safer machine that can adapt to varying site conditions and task demands with minimal human intervention, fundamentally reshaping how backhoe loaders are utilized on job sites.

However, user expectations also come with concerns regarding data security, the complexity of AI system integration, and the need for new operator training. There is a strong desire for AI solutions that are intuitive to use, seamlessly integrate with existing fleet management systems, and provide clear, actionable insights without requiring extensive specialized knowledge from operators. The initial investment cost for AI-enabled machinery is another consideration, with users seeking a clear return on investment through enhanced productivity and reduced operational expenditures. The market is thus balancing the significant potential of AI with the practical needs for user-friendliness, reliability, and demonstrable economic benefits, pushing manufacturers to develop robust, secure, and value-driven AI solutions for the backhoe loader segment.

- Predictive Maintenance: AI algorithms analyze machine data to forecast component failures, optimizing maintenance schedules and reducing unplanned downtime.

- Enhanced Operational Efficiency: AI assists in optimizing digging cycles, load management, and fuel consumption for improved productivity and lower operating costs.

- Autonomous and Semi-Autonomous Capabilities: AI enables functions like automated trenching, grading, and material handling, reducing operator workload and improving precision.

- Advanced Safety Features: AI-powered object detection, collision avoidance, and operator fatigue monitoring systems enhance job site safety.

- Site Optimization: AI can analyze terrain and project requirements to suggest optimal paths and techniques, increasing overall project efficiency.

- Training and Simulation: AI-driven simulations can provide realistic training environments for operators, improving skill development and reducing on-site errors.

Key Takeaways Backhoe Loader Market Size & Forecast

The Backhoe Loader Market is poised for consistent expansion, driven significantly by global infrastructure development and urbanization trends, particularly in emerging economies. The projected CAGR of 4.8% from 2025 to 2033, leading to an estimated market value of USD 12.3 Billion, underscores a robust demand outlook. This growth is not merely volume-driven but is increasingly influenced by technological advancements that enhance machine versatility, efficiency, and sustainability. Manufacturers are responding to a market that values not only raw power but also precision, automation, and environmental performance, indicating a shift towards more intelligent and eco-friendly construction equipment.

A crucial insight from the market forecast is the increasing integration of digital technologies and smart features into backhoe loaders. This includes telematics for fleet management, AI for predictive maintenance, and semi-autonomous capabilities that are becoming standard rather than optional. The move towards electrification and hybrid solutions, while still in its nascent stages, is expected to gain significant traction, driven by stricter emission regulations and the long-term cost benefits of reduced fuel consumption. This technological evolution is a key factor in attracting new investments and ensuring the relevance of backhoe loaders in a rapidly modernizing construction landscape.

Furthermore, the market's resilience is bolstered by diverse applications beyond traditional construction, including agriculture, utility work, and rental services, which provide multiple avenues for growth. The rising preference for rental equipment, especially among smaller contractors, allows for wider market penetration and adaptability to fluctuating project demands without substantial capital outlay. Overall, the Backhoe Loader Market's trajectory suggests a future characterized by innovation, sustainability, and adaptability, with a strong emphasis on delivering higher operational efficiency and lower total cost of ownership for end-users globally.

- The Backhoe Loader Market is forecast to grow at a CAGR of 4.8% from USD 8.5 Billion in 2025 to USD 12.3 Billion by 2033.

- Growth is primarily fueled by infrastructure development, urbanization, and increasing demand from developing regions.

- Technological integration, including telematics, AI, and automation, is a significant driver of market expansion and efficiency improvements.

- The shift towards electric and hybrid models is a key long-term trend influencing market development.

- The expanding equipment rental market is a crucial factor in broader market accessibility and demand generation.

- Versatility across diverse applications (construction, agriculture, utility) underpins market stability and growth.

Backhoe Loader Market Drivers Analysis

The global Backhoe Loader Market is significantly propelled by substantial investments in infrastructure development across both developed and emerging economies. Governments worldwide are allocating considerable budgets towards building and upgrading roads, bridges, railways, ports, and public utilities. This sustained push for infrastructure modernization directly translates into heightened demand for versatile construction equipment like backhoe loaders, which are essential for various stages of project execution, from excavation and trenching to material handling and loading. The need for efficient and adaptable machinery in these large-scale projects ensures a continuous revenue stream for manufacturers and rental providers alike, fostering market expansion.

Rapid urbanization and population growth in various regions also serve as powerful drivers for the backhoe loader market. As more people migrate to urban centers, the demand for residential, commercial, and industrial infrastructure surges. Backhoe loaders are indispensable for site preparation, foundation work, utility installations, and landscaping in these urban development projects, which are often characterized by confined spaces requiring highly maneuverable equipment. This demographic shift, particularly prominent in Asia Pacific and parts of Africa, fuels ongoing construction activities and consequently, the demand for compact and efficient machinery capable of operating effectively in densely populated areas.

Furthermore, the increasing adoption of rental equipment across the construction sector is a notable driver. Many small to medium-sized construction companies, and even larger firms, prefer renting equipment over outright purchase to manage capital expenditure, reduce maintenance costs, and gain access to a wider range of specialized machinery without long-term commitment. This trend expands the accessibility of backhoe loaders to a broader base of users and projects, ensuring that demand remains robust even amidst fluctuating economic conditions. The flexibility offered by rental models makes backhoe loaders more readily available for diverse short-term or specialized tasks, contributing significantly to market volume and growth.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Infrastructure Development & Public Works Spending | +1.2% | Global, particularly Asia Pacific, North America, Europe | Mid-term to Long-term (2025-2033) |

| Rapid Urbanization & Residential/Commercial Construction | +1.0% | Asia Pacific, Latin America, Middle East & Africa | Mid-term (2025-2029) |

| Growth in Equipment Rental Market | +0.8% | North America, Europe, Asia Pacific | Mid-term to Long-term (2025-2033) |

| Technological Advancements & Automation Integration | +0.7% | Global | Long-term (2028-2033) |

| Agricultural Sector Mechanization | +0.5% | Asia Pacific, Latin America, Africa | Mid-term to Long-term (2025-2033) |

Backhoe Loader Market Restraints Analysis

The Backhoe Loader Market faces significant restraints, primarily stemming from the high initial capital investment required to purchase these machines. Backhoe loaders are complex pieces of heavy equipment, and their acquisition costs can be substantial, posing a considerable barrier for small and medium-sized enterprises (SMEs) or individual contractors. This high entry cost often forces potential buyers to opt for rental agreements or used equipment, which can limit new unit sales and suppress market growth in certain segments. Additionally, the associated costs of ownership, including financing, insurance, and long-term maintenance, further deter some buyers, especially in economic downturns when capital preservation becomes a priority.

Economic slowdowns and political instability also present significant challenges to the backhoe loader market. Construction projects are highly sensitive to economic cycles; during periods of recession or reduced economic growth, private and public sector investments in infrastructure and real estate tend to decline. This directly impacts the demand for construction machinery. Furthermore, political uncertainties, trade wars, or geopolitical conflicts can disrupt supply chains, increase raw material costs, and deter foreign investment, leading to project delays or cancellations, which subsequently curb the procurement of new backhoe loaders. Such external shocks create an unpredictable market environment, making long-term planning difficult for manufacturers and purchasers.

Moreover, stringent environmental regulations and increasing concerns over emissions contribute to market restraints. Governments worldwide are implementing stricter emission standards for off-road machinery, necessitating significant research and development investments from manufacturers to comply with these rules. The development of more eco-friendly engines, such as those meeting Tier 4 Final or Stage V standards, adds to the production costs, which are often passed on to the consumer, making the equipment more expensive. While beneficial for the environment, these regulations can slow down the adoption of new machinery, particularly in regions where older, less compliant models are still widely in use due to their lower cost and perceived durability. This pressure to innovate while remaining competitive poses a continuous challenge for the industry.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Capital Investment & Maintenance Costs | -0.9% | Global, particularly developing economies | Mid-term to Long-term (2025-2033) |

| Economic Downturns & Fluctuating Construction Activity | -0.8% | Global, varies by regional economic stability | Short-term to Mid-term (2025-2027) |

| Stringent Emission Regulations & Compliance Costs | -0.6% | North America, Europe, increasingly Asia Pacific | Mid-term (2025-2029) |

| Availability of Cheaper Alternatives/Used Equipment | -0.5% | Developing economies | Long-term (2025-2033) |

| Skilled Labor Shortage for Operation & Maintenance | -0.4% | North America, Europe, parts of Asia Pacific | Long-term (2025-2033) |

Backhoe Loader Market Opportunities Analysis

The Backhoe Loader Market presents significant opportunities, particularly in emerging economies that are experiencing rapid industrialization and infrastructure development. Countries in Asia Pacific, Latin America, and the Middle East & Africa are undergoing massive urbanization and development projects, requiring substantial investments in construction equipment. These regions often have burgeoning populations and a growing middle class, leading to increased demand for housing, commercial spaces, and public utilities. This creates a fertile ground for market penetration for backhoe loader manufacturers, especially for models that are cost-effective, robust, and suited to diverse operational environments, offering a strong growth trajectory.

Technological advancements and the development of intelligent backhoe loaders also represent a major opportunity. The integration of telematics, IoT sensors, GPS, and automation features can significantly enhance machine efficiency, precision, and safety. There is a growing demand for 'smart' equipment that offers predictive maintenance capabilities, remote diagnostics, and improved fuel efficiency, leading to lower operating costs and higher uptime for end-users. Manufacturers who can innovate and successfully integrate these cutting-edge technologies into their product lines will gain a competitive edge and tap into a market segment willing to invest in solutions that deliver long-term value and operational superiority.

Furthermore, the increasing focus on sustainable and eco-friendly construction practices worldwide creates a strong opportunity for the development and adoption of electric and hybrid backhoe loaders. With tightening environmental regulations and a global push towards reducing carbon footprints, there is a clear market demand for equipment that operates with lower emissions and reduced noise levels. Companies that invest in research and development for electric drivetrains, battery technologies, and alternative fuels for backhoe loaders can position themselves as leaders in a growing green construction market. This not only addresses regulatory compliance but also appeals to environmentally conscious contractors and projects, opening new revenue streams and fostering a sustainable industry future.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Emerging Economies & Infrastructure Spending | +1.5% | Asia Pacific, Latin America, Middle East & Africa | Long-term (2025-2033) |

| Technological Innovation (Telematics, Automation, AI) | +1.0% | Global | Mid-term to Long-term (2025-2033) |

| Development of Electric & Hybrid Backhoe Loaders | +0.9% | North America, Europe, gradually Asia Pacific | Long-term (2028-2033) |

| Expansion of Equipment Rental Services | +0.7% | Global | Mid-term (2025-2029) |

| Customization for Niche Applications (e.g., Agriculture, Waste Management) | +0.6% | Global | Mid-term (2025-2029) |

Backhoe Loader Market Challenges Impact Analysis

The Backhoe Loader Market faces significant challenges from intense competition and price sensitivity. The market is populated by numerous global and regional manufacturers, leading to fierce competition for market share. This competitive landscape often results in downward pressure on pricing, eroding profit margins for manufacturers and distributors. Furthermore, customers, especially in price-sensitive developing markets, often prioritize initial acquisition cost over advanced features or long-term total cost of ownership. This creates a dilemma for manufacturers trying to balance innovation and compliance with market affordability, potentially limiting investment in new technologies and sustainable solutions. The constant need to differentiate products in a crowded market while maintaining competitive pricing is a pervasive challenge.

Supply chain disruptions and volatility in raw material prices also pose a substantial challenge to the backhoe loader industry. The manufacturing of backhoe loaders relies heavily on a global supply chain for components such as engines, hydraulic systems, steel, and electronic parts. Geopolitical tensions, natural disasters, trade protectionism, and global pandemics can disrupt the flow of these critical components, leading to production delays and increased costs. Simultaneously, fluctuations in the prices of key raw materials like steel and various metals directly impact manufacturing costs. These volatile factors make cost forecasting and production planning difficult, potentially leading to higher end-product prices or reduced profit margins, thereby affecting market stability and growth.

Lastly, the increasing complexity of machinery due to advanced technological integration and the need for skilled labor present a growing challenge. Modern backhoe loaders incorporate sophisticated electronics, telematics, and potentially AI-driven systems, requiring operators and maintenance personnel with specialized training. There is a persistent global shortage of such skilled labor in the construction and equipment maintenance sectors. This shortage can lead to lower operational efficiency, increased downtime due to improper handling or maintenance, and higher labor costs. Manufacturers and training institutions must address this gap to ensure that the industry's technological advancements can be fully leveraged, otherwise, the lack of skilled personnel could hinder the adoption and optimal utilization of advanced backhoe loaders.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Competition & Price Pressure | -0.7% | Global | Long-term (2025-2033) |

| Supply Chain Disruptions & Raw Material Volatility | -0.6% | Global | Short-term to Mid-term (2025-2027) |

| Skilled Labor Shortage for Operation & Maintenance | -0.5% | North America, Europe, parts of Asia Pacific | Long-term (2025-2033) |

| High Research & Development Costs for New Technologies | -0.4% | Global | Mid-term to Long-term (2025-2033) |

| After-sales Service & Parts Availability Challenges in Remote Areas | -0.3% | Developing economies, remote regions | Long-term (2025-2033) |

Backhoe Loader Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the Backhoe Loader Market, covering key market dynamics, trends, and future projections. It delivers critical insights into market sizing, growth drivers, restraints, opportunities, and challenges affecting the industry from 2025 to 2033. The report meticulously segments the market by product type, operating weight, end-use application, and engine power, providing a detailed breakdown of market share and growth potential across various categories. Furthermore, it offers a granular regional analysis, highlighting growth hotspots and key market characteristics in major geographical areas. The competitive landscape section profiles leading companies, examining their strategies, product portfolios, and recent developments to offer a complete understanding of the market's competitive intensity.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 8.5 Billion |

| Market Forecast in 2033 | USD 12.3 Billion |

| Growth Rate | 4.8% |

| Number of Pages | 255 |

| Key Trends | >|

| Segments Covered | >|

| Key Companies Covered | Caterpillar Inc., JCB Ltd., Deere & Company, CNH Industrial N.V. (Case Construction Equipment), Volvo Construction Equipment, Komatsu Ltd., Hitachi Construction Machinery Co., Ltd., Hyundai Construction Equipment Co., Ltd., Doosan Infracore Co., Ltd., Kubota Corporation, SANY Group, XCMG Group, LiuGong Machinery Co., Ltd., Terex Corporation, Wacker Neuson SE, Mahindra Construction Equipment, Bharat Earth Movers Limited (BEML), New Holland Construction, L&T Construction & Mining Machinery, Manitou Group |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Backhoe Loader Market is extensively segmented to provide a granular understanding of its diverse applications and product variations. This segmentation helps in identifying specific growth pockets and understanding user preferences across different operational requirements. The market is primarily divided by type, distinguishing between Center Mount and Side Shift models, each catering to specific geographical preferences and operational demands. Further segmentation by operating weight—Below 5 Tons, 5 to 10 Tons, and Above 10 Tons—addresses the varied needs of projects ranging from compact urban utility work to heavy-duty construction and agricultural tasks, reflecting the machine's adaptability to different scales of operation.

The end-use application segment is crucial, categorizing demand from key industries such as Construction, Agriculture, Mining, Utility, and Rental, alongside other niche applications like landscaping and waste management. This breakdown highlights the multi-functional nature of backhoe loaders and their essential role across various sectors, providing insights into demand drivers from each industry. Lastly, segmentation by engine power—Below 80 HP, 80-100 HP, and Above 100 HP—reflects the performance capabilities and suitability of different backhoe loader models for light, medium, and heavy-duty tasks, enabling a precise analysis of power requirements and technological advancements within the market.

- By Type:

- Center Mount

- Side Shift

- By Operating Weight:

- Below 5 Tons

- 5 to 10 Tons

- Above 10 Tons

- By End-Use Application:

- Construction

- Agriculture

- Mining

- Utility

- Rental

- Others (Landscaping, Waste Management)

- By Engine Power:

- Below 80 HP

- 80-100 HP

- Above 100 HP

Regional Highlights

- North America: This region is characterized by robust infrastructure spending, particularly in the United States and Canada, driving demand for modern and technologically advanced backhoe loaders. The increasing adoption of equipment rental services and a strong emphasis on smart construction technologies are key drivers. The market benefits from a well-established construction industry and a focus on upgrading aging infrastructure.

- Europe: Driven by stringent emission regulations and a strong push towards sustainable construction practices, the European market is witnessing a growing demand for electric and hybrid backhoe loaders. Germany, France, and the UK are key markets, with significant investments in urban development and renovation projects. The rental market is also highly developed, providing easy access to equipment.

- Asia Pacific (APAC): APAC is the fastest-growing region, fueled by rapid urbanization, massive infrastructure projects in countries like China, India, and Southeast Asian nations, and burgeoning residential and commercial construction. This region represents immense potential due to its high population density and developing economies, leading to substantial demand for various types of backhoe loaders, from compact to heavy-duty models.

- Latin America: Countries such as Brazil, Mexico, and Argentina are experiencing growth in construction and mining activities, contributing to the demand for backhoe loaders. Investments in public works and agricultural mechanization are key drivers, though economic volatility can sometimes impact market stability.

- Middle East & Africa (MEA): This region is characterized by large-scale development projects, particularly in the GCC countries (Saudi Arabia, UAE) for smart cities and diversified economies. In Africa, infrastructure development, mining, and agricultural expansion are driving demand. However, political stability and commodity prices can influence market growth.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Backhoe Loader Market.- Caterpillar Inc.

- JCB Ltd.

- Deere & Company

- CNH Industrial N.V. (Case Construction Equipment)

- Volvo Construction Equipment

- Komatsu Ltd.

- Hitachi Construction Machinery Co., Ltd.

- Hyundai Construction Equipment Co., Ltd.

- Doosan Infracore Co., Ltd.

- Kubota Corporation

- SANY Group

- XCMG Group

- LiuGong Machinery Co., Ltd.

- Terex Corporation

- Wacker Neuson SE

- Mahindra Construction Equipment

- Bharat Earth Movers Limited (BEML)

- New Holland Construction

- L&T Construction & Mining Machinery

- Manitou Group

Frequently Asked Questions

Analyze common user questions about the Backhoe Loader market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the current market size and projected growth rate of the Backhoe Loader Market?

The Backhoe Loader Market is estimated at USD 8.5 Billion in 2025 and is projected to reach USD 12.3 Billion by 2033, growing at a Compound Annual Growth Rate (CAGR) of 4.8% during the forecast period.

What are the primary drivers fueling the growth of the Backhoe Loader Market?

Key drivers include global infrastructure development and public works spending, rapid urbanization and increased construction activities, the expansion of the equipment rental market, and ongoing technological advancements in machine capabilities and efficiency.

How is Artificial Intelligence (AI) impacting the Backhoe Loader Market?

AI is increasingly impacting the market through predictive maintenance capabilities, enhanced operational efficiency and automation, advanced safety features, and the development of semi-autonomous functions, leading to reduced downtime and improved productivity.

Which regions are expected to show significant growth in the Backhoe Loader Market?

The Asia Pacific (APAC) region is projected to exhibit the fastest growth due to extensive infrastructure projects and rapid urbanization. North America and Europe also show steady growth driven by technological adoption and robust construction sectors.

What are the main challenges faced by the Backhoe Loader Market?

Major challenges include high initial capital investment costs, intense market competition and price sensitivity, supply chain disruptions, volatility in raw material prices, and the persistent shortage of skilled labor for operation and maintenance.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted