Die Casting Market

Die Casting Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700037 | Last Updated : July 22, 2025 |

Format : ![]()

![]()

![]()

![]()

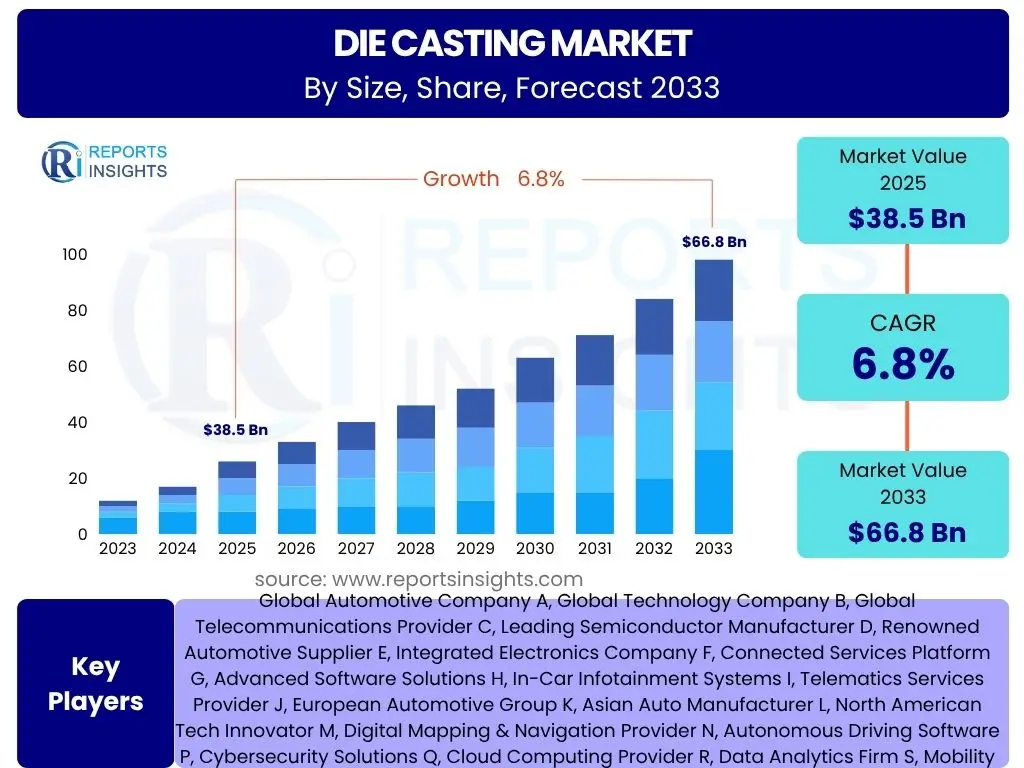

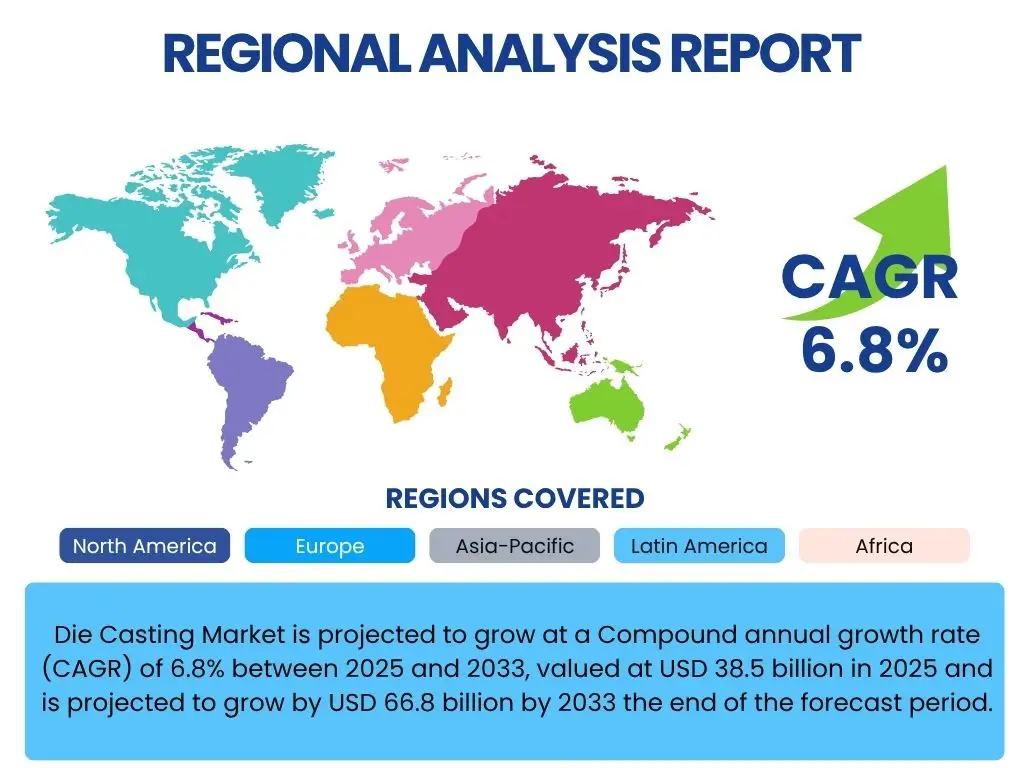

Die Casting Market is projected to grow at a Compound annual growth rate (CAGR) of 6.8% between 2025 and 2033, valued at USD 38.5 billion in 2025 and is projected to grow by USD 66.8 billion by 2033 the end of the forecast period.

Key Die Casting Market Trends & Insights

The global die casting market is experiencing dynamic shifts driven by advancements in material science, evolving industrial demands, and technological innovations. Key trends reflect a move towards sustainable manufacturing practices, the integration of smart technologies, and an increasing focus on lightweighting components across various end-use industries. These developments are reshaping traditional production methodologies and fostering new opportunities for market expansion and efficiency.

- Growing adoption of high-pressure die casting (HPDC) for complex geometries.

- Increased demand for lightweight components in automotive and aerospace sectors.

- Rising integration of automation and robotics in die casting processes.

- Development of advanced alloys for improved performance and durability.

- Focus on sustainable practices and energy-efficient casting solutions.

- Expansion of applications in consumer electronics and medical devices.

- Shift towards localized manufacturing and resilient supply chains.

AI Impact Analysis on Die Casting

Artificial Intelligence (AI) is poised to revolutionize the die casting industry by enhancing precision, optimizing operational efficiency, and enabling predictive maintenance. AI algorithms can analyze vast datasets from production lines, identifying patterns that lead to defects, predicting equipment failures, and fine-tuning parameters for optimal yield. This transformative capability extends from the design phase through manufacturing, promising significant improvements in quality, cost-effectiveness, and overall throughput.

- AI-driven optimization of die design and tooling for reduced material waste.

- Predictive analytics for maintenance of die casting machinery, minimizing downtime.

- Real-time quality control and defect detection using machine vision and AI algorithms.

- Enhanced process control through AI-powered parameter adjustments.

- Improved supply chain management and demand forecasting with AI models.

- Automated robot programming and path optimization for greater efficiency.

Key Takeaways Die Casting Market Size & Forecast

- Market size projected to reach USD 66.8 billion by 2033.

- Anticipated Compound Annual Growth Rate (CAGR) of 6.8% from 2025 to 2033.

- Automotive industry remains a dominant end-use segment.

- Significant growth expected from electronics and telecommunications applications.

- Asia Pacific continues to be the leading region in terms of market share.

- Technological advancements in casting alloys are driving market expansion.

- Focus on energy efficiency and sustainable manufacturing practices is increasing.

Die Casting Market Drivers Analysis

The die casting market is propelled by a confluence of robust drivers, primarily stemming from the escalating demand for lightweight, high-performance components across various industries. The automotive sector's relentless pursuit of fuel efficiency and electric vehicle (EV) integration significantly boosts the need for precision die-cast parts. Concurrently, the growth of consumer electronics, telecommunications, and industrial machinery sectors, which heavily rely on intricate metal components, further fuels market expansion. Technological advancements in casting processes and material science also play a pivotal role, enabling the production of more complex and durable parts.

Moreover, the increasing global emphasis on sustainable manufacturing and the adoption of automation within production facilities contribute to the market's upward trajectory. Manufacturers are investing in advanced die casting techniques that offer reduced material waste, energy efficiency, and higher production rates. The diverse application spectrum of die-cast components, ranging from structural parts to heat sinks and housings, ensures a consistent demand, underscoring the market's inherent resilience and growth potential in the coming years.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rising Demand from Automotive Industry for Lightweight Components | +1.5% | Global, particularly North America, Europe, Asia Pacific (China, India, Japan) | Short to Long Term (2025-2033) |

| Growth in Consumer Electronics and Telecommunications | +1.2% | Asia Pacific (China, South Korea), North America, Europe | Short to Mid Term (2025-2029) |

| Advancements in Die Casting Technologies and Alloys | +1.0% | Global, with R&D hubs in Germany, Japan, USA | Mid to Long Term (2027-2033) |

| Increasing Demand for Industrial Machinery and Equipment | +0.8% | Europe, Asia Pacific, North America | Short to Mid Term (2025-2030) |

| Expansion of Renewable Energy Sector | +0.7% | Europe, North America, Asia Pacific (China) | Mid to Long Term (2028-2033) |

| Urbanization and Infrastructure Development | +0.6% | Asia Pacific (India, Southeast Asia), Middle East & Africa | Long Term (2029-2033) |

Die Casting Market Restraints Analysis

Despite its significant growth potential, the die casting market faces several notable restraints that could temper its expansion. One primary challenge involves the volatility of raw material prices, particularly for metals like aluminum, zinc, and magnesium. Fluctuations in these commodity prices directly impact production costs, squeezing profit margins for manufacturers and potentially leading to delays in investment or project execution. This instability introduces a degree of uncertainty for market participants, complicating long-term planning and pricing strategies.

Furthermore, the high initial capital investment required for advanced die casting machinery and the associated tooling presents a significant barrier to entry for new players and limits the ability of smaller enterprises to scale operations. Stringent environmental regulations concerning emissions, waste disposal, and energy consumption also pose a challenge, necessitating costly compliance measures and the adoption of more sustainable but often more expensive manufacturing processes. The emergence of alternative manufacturing techniques, such as additive manufacturing (3D printing) for certain applications, also presents a competitive threat, potentially diverting demand from traditional die casting processes in niche markets.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility in Raw Material Prices (Aluminum, Zinc, Magnesium) | -0.8% | Global | Short to Mid Term (2025-2030) |

| High Initial Capital Investment for Machinery and Tooling | -0.6% | Global, more pronounced in developing regions | Long Term (2025-2033) |

| Stringent Environmental Regulations and Energy Consumption Concerns | -0.5% | Europe, North America, parts of Asia Pacific (China) | Mid to Long Term (2027-2033) |

| Competition from Alternative Manufacturing Technologies (e.g., Additive Manufacturing) | -0.4% | Global, particularly in high-value, low-volume applications | Long Term (2029-2033) |

Die Casting Market Opportunities Analysis

The die casting market is ripe with opportunities, particularly stemming from the accelerating transition to electric vehicles (EVs). The demand for lightweight battery housings, motor casings, and structural components crucial for EVs presents a substantial growth avenue for die casters capable of producing large, complex, and high-integrity parts. This shift necessitates innovation in alloy development and casting processes, opening doors for companies investing in advanced technologies. Furthermore, the global drive towards sustainable practices and energy efficiency encourages the adoption of more advanced, environmentally friendly die casting techniques, offering a competitive edge to innovators.

Beyond the automotive sector, the burgeoning medical devices industry and the telecommunications infrastructure expansion (especially 5G rollout) create new niches for precision die-cast components. These sectors require parts with high dimensional accuracy, excellent surface finish, and often superior electromagnetic shielding properties. Moreover, the increasing trend of reshoring manufacturing activities and strengthening regional supply chains, particularly in North America and Europe, provides an opportunity for local die casters to capture a larger market share by offering proximity, reduced lead times, and enhanced quality control. Leveraging automation and AI to optimize production further enhances efficiency and opens up new revenue streams.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Electric Vehicle (EV) Production and Lightweighting | +1.8% | Global, significant in Asia Pacific (China), Europe, North America | Short to Long Term (2025-2033) |

| Expansion into New Applications (Medical Devices, 5G Infrastructure) | +1.3% | North America, Europe, Asia Pacific | Mid to Long Term (2027-2033) |

| Adoption of Industry 4.0 and Smart Manufacturing Principles | +1.0% | Developed economies (Germany, Japan, USA) spreading globally | Mid to Long Term (2028-2033) |

| Focus on Circular Economy and Recyclable Materials | +0.9% | Europe, North America | Long Term (2029-2033) |

| Reshoring of Manufacturing and Regional Supply Chain Strengthening | +0.7% | North America, Europe | Short to Mid Term (2025-2030) |

Die Casting Market Challenges Impact Analysis

The die casting market, while growing, confronts several significant challenges that demand strategic responses from industry players. One major hurdle is the increasing complexity of part geometries and the stringent quality requirements from end-use industries, particularly automotive and aerospace. Meeting these demands requires sophisticated tooling, advanced simulation software, and highly skilled labor, leading to higher production costs and a greater risk of defects if processes are not meticulously controlled. The ongoing shortage of skilled labor, especially for specialized roles in operating and maintaining advanced die casting machinery, further exacerbates this challenge, impacting productivity and increasing operational expenses.

Moreover, intense global competition, especially from low-cost manufacturing regions, puts pressure on pricing and profitability for established players in developed markets. This necessitates continuous innovation and efficiency improvements to maintain competitiveness. The high energy consumption associated with the die casting process and the need to reduce carbon footprints also present a dual challenge of operational cost and environmental compliance. Addressing these challenges requires sustained investment in R&D, workforce development, and the adoption of cutting-edge technologies to enhance efficiency and maintain a competitive edge in a dynamic global market.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Energy Consumption and Environmental Regulations | -0.7% | Global, particularly Europe and North America | Short to Long Term (2025-2033) |

| Shortage of Skilled Labor and Workforce Training Costs | -0.6% | Global, more acute in developed economies | Short to Mid Term (2025-2030) |

| Intense Global Competition and Pricing Pressure | -0.5% | Global, significant for manufacturers in high-cost regions | Short to Mid Term (2025-2030) |

| Technological Obsolescence and Need for Continuous R&D Investment | -0.4% | Global | Mid to Long Term (2027-2033) |

| Quality Control and Defect Minimization for Complex Parts | -0.3% | Global | Short to Mid Term (2025-2029) |

Die Casting Market - Updated Report Scope

This comprehensive report offers an in-depth analysis of the global die casting market, providing crucial insights into market dynamics, segmentation, and regional landscapes. It details historical data, current trends, and future projections, enabling stakeholders to make informed strategic decisions. The scope covers key growth drivers, significant restraints, emerging opportunities, and prevailing challenges, alongside an evaluation of the competitive landscape and technological advancements shaping the industry. This document serves as an essential resource for businesses aiming to understand market potential and navigate strategic growth pathways.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 38.5 Billion |

| Market Forecast in 2033 | USD 66.8 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Casting Solutions, Precision Alloys Group, Advanced Die-Cast Technologies, Universal Metal Forming, Elite Component Manufacturing, Integrated Die Casting, Future Forge Industries, Prime Casting Innovations, Dynamic Engineered Metals, Cornerstone Castings, Zenith Die Products, Pioneer Metal Solutions, Legacy Die-Cast, Optima Manufacturing, Stellar Castings, Apex Precision Parts, Synergy Die Casting, Vertex Metalworks, Quantum Components, Horizon Casting Enterprises |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The die casting market is comprehensively segmented to provide granular insights into its diverse components and driving factors. This segmentation allows for a detailed understanding of how different material types, casting processes, end-use applications, and industry verticals contribute to the overall market landscape. By analyzing these distinct segments, stakeholders can identify key growth areas, evaluate competitive advantages, and tailor their strategies to specific market demands. This structured approach ensures a thorough examination of the market's complexities, from the fundamental material choices to the specialized end-products.

Understanding the interplay between these segments is crucial for accurate market forecasting and strategic planning. For instance, the dominance of aluminum in certain applications due to its lightweight properties, or the growing adoption of high-pressure die casting for intricate parts, highlights specific trends within the market. Similarly, the varying demands across industries like automotive versus electronics underscore the need for diversified production capabilities. This detailed segmentation not only clarifies the current market structure but also illuminates future opportunities and challenges across its various dimensions.

- By Material Type: This segment categorizes the market based on the primary metal alloys used in the die casting process, each possessing distinct properties and applications.

- Aluminum Die Casting: Dominant due to its lightweight, high strength-to-weight ratio, excellent thermal and electrical conductivity, and corrosion resistance. Widely used in automotive, consumer electronics, and telecommunications.

- Zinc Die Casting: Known for its excellent castability, high ductility, impact strength, and ease of plating. Commonly used for intricate, precision parts in electronics, hardware, and small appliances.

- Magnesium Die Casting: Valued for its extremely low density, making it ideal for ultralight components, especially in automotive and portable electronics where weight reduction is critical.

- Others: Includes alloys such as copper and lead, used for specialized applications requiring specific properties like high conductivity or radiation shielding.

- By Process: This segmentation focuses on the different methodologies employed in the die casting process, each suited for varying production volumes, part complexities, and material types.

- High-Pressure Die Casting (HPDC): The most common method, involving injecting molten metal at high speed and pressure into a die cavity. Ideal for high-volume production of complex, thin-walled parts with excellent surface finish and dimensional accuracy.

- Low-Pressure Die Casting (LPDC): Molten metal is forced into the die cavity under low pressure from below, reducing turbulence and gas porosity. Suitable for larger, denser castings and structural components.

- Gravity Die Casting: Relies on gravity to fill the die cavity, offering slower fill rates and better control over solidification. Often used for components requiring high integrity and mechanical properties, suitable for smaller to medium batches.

- Vacuum Die Casting: A variant of HPDC where air is evacuated from the die cavity before metal injection, minimizing porosity and improving mechanical properties. Used for critical, high-strength applications.

- Squeeze Die Casting: Combines casting with forging, applying pressure during solidification to eliminate porosity and enhance mechanical properties. Suitable for high-strength, structural components.

- By Application: This segment categorizes the market based on the specific functional use of the die-cast components within various end products.

- Engine Parts: Includes engine blocks, cylinder heads, manifolds, and other intricate components vital for internal combustion and electric vehicle powertrains.

- Transmission Parts: Gears, casings, valve bodies, and other components essential for power transmission systems in vehicles and machinery.

- Body Parts: Structural components, chassis elements, door frames, and other exterior and interior parts contributing to vehicle integrity and aesthetics.

- Others: Covers a wide range of diverse applications such as HVAC components, steering components, braking system parts, and various smaller functional elements across industries.

- By End-use Industry: This segmentation classifies the market based on the major industrial sectors that consume die-cast products, reflecting the diverse demand landscape.

- Automotive: The largest end-use sector, driven by the demand for lightweight, high-strength components for traditional internal combustion engine vehicles and rapidly expanding electric vehicles.

- Industrial: Includes machinery and equipment for manufacturing, construction, agriculture, and various other industrial applications requiring durable and precision-engineered metal parts.

- Consumer Electronics: Encompasses parts for smartphones, laptops, cameras, home appliances, and other electronic gadgets, often requiring intricate designs and excellent heat dissipation.

- Telecommunications: Components for networking equipment, base stations, optical transceivers, and other infrastructure, demanding high precision and often EMI shielding capabilities.

- Medical & Healthcare: Specialized parts for medical devices, diagnostic equipment, surgical instruments, and prosthetic components, requiring high purity and precise dimensions.

- Building & Construction: Includes architectural hardware, plumbing fixtures, structural connectors, and other components used in residential, commercial, and industrial construction.

- Others: Broad category covering aerospace, defense, marine, and other niche sectors with specialized requirements for die-cast components.

Regional Highlights

The global die casting market exhibits significant regional disparities, with certain geographies leading in production, consumption, and technological innovation. These regional dynamics are influenced by factors such as industrialization levels, automotive production hubs, regulatory environments, and the presence of key manufacturing clusters. Understanding these regional highlights is crucial for market participants to tailor their investment strategies and supply chain operations effectively.

- Asia Pacific (APAC) is the undisputed leader in the global die casting market, driven primarily by China, India, Japan, and South Korea. China stands out due to its vast manufacturing base, particularly in automotive, consumer electronics, and industrial machinery sectors, coupled with lower labor costs and supportive government policies. India's rapidly growing automotive industry and infrastructure development projects are also significant contributors. Japan and South Korea excel in advanced manufacturing techniques and cater to high-precision automotive and electronics applications. The region's robust economic growth and increasing disposable incomes fuel demand across various end-use industries, making it a critical hub for die casting production and consumption.

- Europe represents a mature yet innovative market, with Germany, Italy, and France being key players. Germany, known for its strong automotive industry and advanced engineering capabilities, heavily invests in high-tech die casting solutions, especially for premium vehicles and industrial applications. Italy is renowned for its expertise in aluminum die casting, serving various sectors including automotive, machinery, and electrical equipment. Strict environmental regulations and a focus on energy efficiency in Europe drive the adoption of advanced and sustainable die casting processes, pushing technological boundaries.

- North America, primarily the United States and Mexico, is a substantial market for die casting, particularly influenced by the automotive and aerospace industries. The United States has a robust demand for high-strength, lightweight die-cast components for vehicles, defense applications, and heavy machinery. Mexico's strategic location and growing automotive manufacturing sector, driven by nearshoring trends, make it an attractive production base for die casting companies serving the North American market. The region also sees significant investments in automation and smart manufacturing.

- Latin America, particularly Brazil and Mexico, is experiencing steady growth in the die casting market, largely propelled by the automotive and construction sectors. As industrialization progresses and regional manufacturing capabilities expand, the demand for locally produced die-cast components is expected to rise.

- Middle East and Africa (MEA) represent an emerging market for die casting. Growth in this region is linked to increasing investments in infrastructure development, industrial diversification initiatives, and a nascent automotive manufacturing sector. Countries like UAE and Saudi Arabia are focusing on developing their industrial bases, which will gradually increase the demand for die-cast components.

Top Key Players:

The market research report covers the analysis of key stake holders of the Die Casting Market. Some of the leading players profiled in the report include -

- Global Casting Solutions

- Precision Alloys Group

- Advanced Die-Cast Technologies

- Universal Metal Forming

- Elite Component Manufacturing

- Integrated Die Casting

- Future Forge Industries

- Prime Casting Innovations

- Dynamic Engineered Metals

- Cornerstone Castings

- Zenith Die Products

- Pioneer Metal Solutions

- Legacy Die-Cast

- Optima Manufacturing

- Stellar Castings

- Apex Precision Parts

- Synergy Die Casting

- Vertex Metalworks

- Quantum Components

- Horizon Casting Enterprises

Frequently Asked Questions:

What is die casting?

Die casting is a metal casting process that involves forcing molten metal under high pressure into a mold cavity, known as a die. This method is primarily used for producing geometrically complex metal parts with high precision, excellent surface finish, and consistent dimensions. It is suitable for non-ferrous metals like aluminum, zinc, and magnesium.What are the primary applications of die casting?

Die casting finds extensive applications across various industries due to its ability to produce complex, high-strength, and lightweight components. Key applications include automotive parts (engine blocks, transmission housings, structural components), consumer electronics (laptop frames, smartphone casings), industrial machinery (pump housings, valve bodies), telecommunications equipment, and medical devices.What materials are commonly used in die casting?

The most common materials used in die casting are non-ferrous metals and their alloys. Aluminum alloys are dominant due to their lightweight properties, strength-to-weight ratio, and thermal conductivity. Zinc alloys are favored for their excellent castability, ductility, and ability to produce intricate parts. Magnesium alloys are increasingly used for ultralight components where weight reduction is critical.What are the key market trends influencing the die casting industry?

Key trends shaping the die casting market include the growing demand for lightweight components, especially from the electric vehicle sector, increased adoption of automation and robotics in manufacturing, advancements in die casting technologies and alloy development, and a rising focus on sustainable and energy-efficient production processes. The expansion of applications in consumer electronics and medical devices also represents a significant trend.What is the future outlook for the global die casting market?

The global die casting market is projected for robust growth, driven by continued demand from the automotive industry, particularly electric vehicles, and expanding applications in electronics, telecommunications, and industrial sectors. While challenges like raw material price volatility and high capital investment exist, opportunities in sustainable manufacturing and technological advancements are expected to propel market expansion, particularly in the Asia Pacific region.| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted