Die Bonding Machine Market

Die Bonding Machine Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703230 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

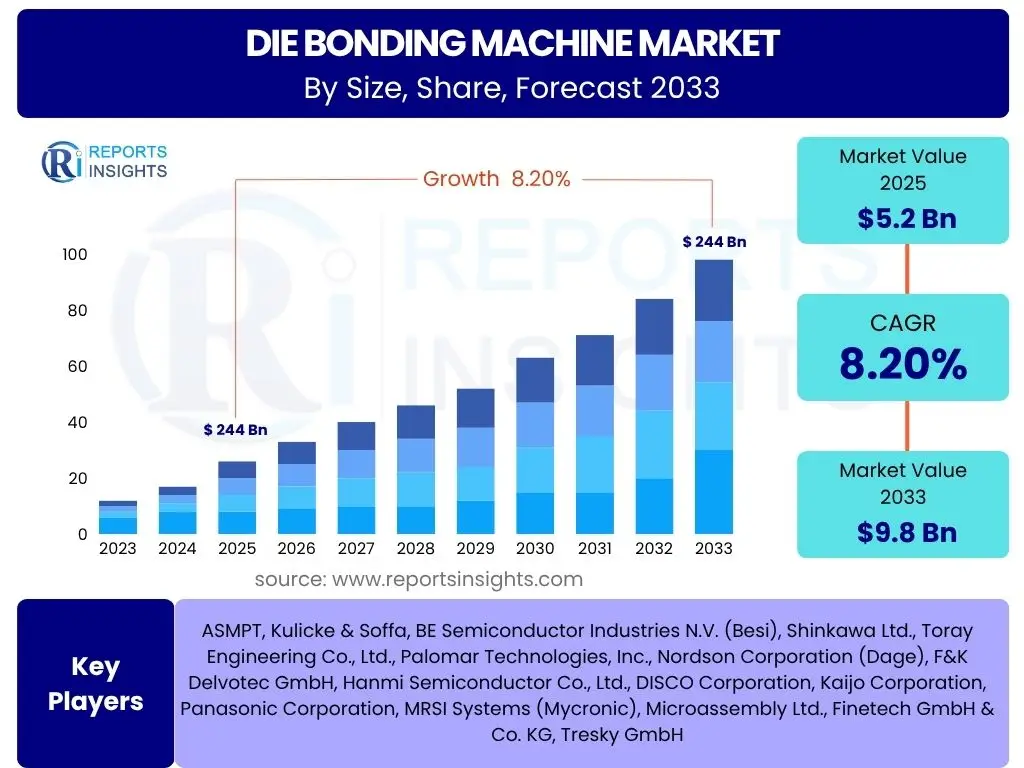

Die Bonding Machine Market Size

According to Reports Insights Consulting Pvt Ltd, The Die Bonding Machine Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.2% between 2025 and 2033. The market is estimated at USD 5.2 Billion in 2025 and is projected to reach USD 9.8 Billion by the end of the forecast period in 2033.

Key Die Bonding Machine Market Trends & Insights

User inquiries regarding the Die Bonding Machine market frequently highlight the shift towards enhanced precision, automation, and integration within semiconductor manufacturing. A significant trend observed is the increasing demand for advanced packaging solutions, such as 3D ICs and System-in-Package (SiP), which necessitates more sophisticated and accurate die bonding capabilities. Manufacturers are also keen on understanding the impact of miniaturization across various electronic devices, driving the need for higher density and finer pitch bonding.

Furthermore, discussions reveal a growing emphasis on smart manufacturing practices, including the adoption of Industry 4.0 principles, where connectivity and data analytics play a crucial role in optimizing bonding processes. The market is also witnessing a trend towards multi-die and hybrid bonding technologies, enabling diverse materials and components to be integrated onto a single substrate. These technological advancements are pivotal in addressing the complex requirements of next-generation electronic components and applications.

- Miniaturization and compact device design requiring finer pitch and higher accuracy.

- Rising adoption of advanced packaging technologies (e.g., SiP, PoP, 3D ICs).

- Increased demand for automated and intelligent die bonding solutions with integrated vision systems.

- Development of multi-die bonding and hybrid bonding for heterogeneous integration.

- Emphasis on high-speed and high-throughput machines to meet mass production demands.

- Integration of real-time monitoring and data analytics for process optimization.

- Growing application in automotive electronics, 5G infrastructure, and IoT devices.

AI Impact Analysis on Die Bonding Machine

Common user questions regarding AI's influence on Die Bonding Machines revolve around improvements in operational efficiency, predictive capabilities, and enhanced quality control. Users are interested in how Artificial intelligence (AI) and Machine Learning (ML) algorithms can optimize bonding parameters, reduce defects, and increase yield rates. The integration of AI promises to elevate die bonding from a purely mechanical process to an intelligent, self-optimizing system capable of adapting to varying material properties and environmental conditions.

AI's role extends to predictive maintenance, where algorithms analyze operational data to anticipate equipment failures, thereby minimizing downtime and extending machine lifespan. Furthermore, AI-powered vision systems can enhance inspection accuracy, identifying microscopic defects that human operators or traditional systems might miss. The potential for AI to automate complex decision-making processes, such as identifying optimal bonding force or temperature profiles for new materials, is a key area of interest, promising significant advancements in manufacturing flexibility and precision.

- Enhanced precision and alignment through AI-powered vision systems.

- Predictive maintenance capabilities reducing downtime and optimizing machine lifespan.

- Real-time process optimization via machine learning algorithms for improved yield.

- Automated defect detection and classification, leading to higher quality output.

- Adaptive bonding parameter adjustments based on material variations and environmental factors.

- Reduced reliance on manual calibration and increased overall equipment effectiveness (OEE).

Key Takeaways Die Bonding Machine Market Size & Forecast

Analysis of common user inquiries regarding the Die Bonding Machine market size and forecast highlights a robust growth trajectory driven by the escalating demand for semiconductor devices across various industries. Users are keenly interested in understanding the primary growth catalysts, such as the proliferation of 5G technology, the expansion of electric vehicles, and the continuous innovation in consumer electronics. The forecast indicates significant opportunities for market participants, particularly those offering advanced, high-precision, and automated bonding solutions.

The market's expansion is intrinsically linked to the global semiconductor industry's resilience and its ongoing need for sophisticated packaging techniques. Key takeaways underscore the importance of technological innovation, strategic partnerships, and regional market dynamics in shaping future growth. Furthermore, the forecast suggests that investments in R&D for novel bonding materials and processes will be crucial for companies aiming to maintain a competitive edge and capture a larger market share in the evolving landscape of microelectronics manufacturing.

- Significant market expansion anticipated due to increasing semiconductor demand.

- Technological advancements in advanced packaging are key growth drivers.

- Rising adoption of automation and AI in manufacturing processes enhances efficiency.

- Asia Pacific to remain a dominant region, driven by large-scale electronics manufacturing.

- Focus on high-precision and high-speed solutions to meet stringent industry requirements.

- Market growth influenced by investments in IoT, 5G, automotive, and consumer electronics sectors.

Die Bonding Machine Market Drivers Analysis

The Die Bonding Machine market is primarily driven by the relentless expansion of the global semiconductor industry, which underpins the vast majority of modern electronic devices. The continuous demand for smaller, more powerful, and energy-efficient electronic components necessitates advanced packaging techniques, directly fueling the need for highly precise and automated die bonding solutions. The proliferation of emerging technologies such as 5G, Artificial Intelligence, Internet of Things (IoT), and autonomous vehicles significantly boosts the production of integrated circuits, thereby increasing the deployment of die bonding machines.

Furthermore, the automotive sector's rapid transition towards electric vehicles (EVs) and advanced driver-assistance systems (ADAS) creates a substantial demand for robust and reliable power modules and sensor components, which rely heavily on sophisticated die bonding processes. The consumer electronics market, with its constant innovation cycle in smartphones, wearables, and smart home devices, also acts as a consistent demand generator for high-volume, high-accuracy die bonding equipment. These factors collectively create a strong positive momentum for market growth.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Surging Demand for Semiconductors | +2.5% | Global, particularly Asia Pacific (China, Taiwan, South Korea) | 2025-2033 |

| Advancements in Advanced Packaging Technologies | +1.8% | North America, Asia Pacific (Japan, Taiwan) | 2025-2033 |

| Growth of IoT, 5G, and AI Applications | +1.5% | Global | 2026-2033 |

| Increasing Adoption in Automotive Electronics | +1.2% | Europe, North America, Asia Pacific (China, Japan) | 2025-2033 |

Die Bonding Machine Market Restraints Analysis

Despite the positive growth outlook, the Die Bonding Machine market faces several significant restraints. One primary challenge is the high capital investment required for acquiring and maintaining advanced die bonding equipment. These machines often incorporate cutting-edge robotics, precision optics, and complex software, making them prohibitively expensive for smaller manufacturers or startups. This high entry barrier can limit market expansion, particularly in emerging economies where access to substantial capital is more restricted.

Another crucial restraint is the inherent complexity and precision required in the die bonding process. Even minor misalignments or variations in bonding parameters can lead to significant yield losses and product defects. This necessitates highly skilled labor for operation and maintenance, which can be scarce and expensive, adding to operational costs. Furthermore, the semiconductor industry's cyclical nature, characterized by periods of oversupply or demand fluctuations, can lead to unpredictable investment patterns and slower adoption rates for new equipment, posing a challenge to consistent market growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Investment and Equipment Cost | -1.0% | Global, impacting smaller players | 2025-2033 |

| Complexity and Need for Skilled Workforce | -0.8% | Global, particularly developed regions | 2025-2033 |

| Supply Chain Disruptions and Geopolitical Risks | -0.7% | Global, impacting key manufacturing hubs | 2025-2028 |

Die Bonding Machine Market Opportunities Analysis

The Die Bonding Machine market presents substantial opportunities driven by evolving technological landscapes and expanding application areas. The continuous innovation in advanced packaging, including fan-out wafer-level packaging (FOWLP) and system-in-package (SiP) solutions, opens new avenues for specialized die bonding machines capable of handling complex geometries and higher integration densities. The development of next-generation power electronics for electric vehicles and renewable energy systems also creates a niche for high-power die bonders that can handle larger dies and higher thermal requirements.

Moreover, the increasing demand for miniaturized medical devices, wearables, and other highly compact electronic products necessitates ultra-precision die bonding, offering opportunities for manufacturers to develop highly specialized equipment. The growing focus on smart factories and Industry 4.0 principles also encourages the integration of AI, machine learning, and automation into die bonding processes, providing a competitive edge for companies that can offer intelligent, self-optimizing solutions. Furthermore, expansion into emerging markets, particularly in Southeast Asia and Latin America, where semiconductor manufacturing is growing, presents new geographical opportunities.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of New Advanced Packaging Technologies | +1.5% | Global, focusing on R&D hubs | 2026-2033 |

| Growing Demand for Heterogeneous Integration | +1.3% | North America, Asia Pacific | 2025-2033 |

| Increasing Automation and AI Integration in Manufacturing | +1.0% | Global, early adopters in developed economies | 2025-2033 |

| Expansion into Emerging Markets and Niche Applications | +0.8% | Southeast Asia, Latin America | 2027-2033 |

Die Bonding Machine Market Challenges Impact Analysis

The Die Bonding Machine market faces several challenges that could impede its growth. Technological complexity is a significant hurdle; as semiconductor devices become smaller and more intricate, the demand for extreme precision and accuracy in die bonding increases. This necessitates continuous investment in research and development to keep pace with evolving chip designs and materials, posing a financial burden on manufacturers. Ensuring high yield rates while handling ultra-thin and fragile dies is a constant challenge, requiring sophisticated process control and advanced automation.

Furthermore, intense competition among existing players and the entry of new market participants lead to pricing pressures and reduced profit margins. Maintaining a competitive edge requires not only technological superiority but also efficient manufacturing processes and robust customer support. Geopolitical tensions and trade disputes, particularly affecting the global semiconductor supply chain, can disrupt manufacturing schedules, increase material costs, and create uncertainty, impacting market stability and investment decisions. Addressing these challenges requires strategic foresight and agile operational capabilities.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Technological Complexity and Miniaturization | -0.9% | Global | 2025-2033 |

| Intense Competition and Pricing Pressures | -0.6% | Global | 2025-2033 |

| Volatility in Semiconductor Industry Demand Cycles | -0.5% | Global | 2025-2033 |

| Environmental Regulations and Sustainability Demands | -0.4% | Europe, North America | 2026-2033 |

Die Bonding Machine Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global Die Bonding Machine market, covering historical data, current market trends, and future growth projections from 2025 to 2033. It examines market size, growth drivers, restraints, opportunities, and challenges, offering a detailed understanding of market dynamics across various segments and regions. The report leverages extensive market research methodologies to deliver actionable insights for stakeholders within the semiconductor manufacturing industry and related sectors.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 5.2 Billion |

| Market Forecast in 2033 | USD 9.8 Billion |

| Growth Rate | 8.2% CAGR |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | ASMPT, Kulicke & Soffa, BE Semiconductor Industries N.V. (Besi), Shinkawa Ltd., Toray Engineering Co., Ltd., Palomar Technologies, Inc., Nordson Corporation (Dage), F&K Delvotec GmbH, Hanmi Semiconductor Co., Ltd., DISCO Corporation, Kaijo Corporation, Panasonic Corporation, MRSI Systems (Mycronic), Microassembly Ltd., Finetech GmbH & Co. KG, Tresky GmbH |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Die Bonding Machine market is comprehensively segmented to provide a granular view of its various facets, enabling a deeper understanding of market dynamics and opportunities. This segmentation considers machine type, bonding technology, specific application areas, and the diverse end-use industries that leverage these critical devices. Each segment exhibits unique growth patterns and demand drivers, reflecting the varied requirements across the microelectronics manufacturing ecosystem.

Understanding these segments is crucial for market participants to tailor their product offerings, develop targeted marketing strategies, and identify emerging growth pockets. The segmentation highlights the market's response to technological shifts, such as the increasing sophistication of packaging, and the evolving demands of sectors like automotive and telecommunications for higher performance and reliability. This detailed breakdown ensures a thorough market assessment.

- By Type:

- Automatic Die Bonders

- Semi-automatic Die Bonders

- Manual Die Bonders

- By Bonding Type:

- Flip-chip Die Bonders

- Die-to-die Bonders

- Die-to-wafer Bonders

- Wafer-to-wafer Bonders

- Other Bonding Types (e.g., thermosonic, eutectic)

- By Application:

- RF Devices

- LED

- MEMS (Micro-Electro-Mechanical Systems)

- Optoelectronics

- Power Devices

- Others (e.g., sensors, medical devices)

- By End-Use Industry:

- Consumer Electronics

- Automotive

- Industrial

- Telecommunications

- Healthcare

- Defense & Aerospace

- By Region:

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Regional Highlights

- Asia Pacific (APAC): Dominates the Die Bonding Machine market, primarily driven by the presence of major semiconductor foundries, packaging houses, and electronics manufacturing hubs in countries like China, Taiwan, South Korea, and Japan. High investments in advanced packaging technologies, robust consumer electronics production, and increasing government support for domestic semiconductor industries contribute significantly to its market share. The region is a hotbed for both demand and supply of advanced die bonding solutions.

- North America: Exhibits steady growth fueled by significant R&D activities, the presence of leading technology companies, and increasing adoption of advanced packaging for high-performance computing, AI, and defense applications. The region focuses on high-precision and specialized bonding solutions, especially in aerospace and medical device manufacturing.

- Europe: Shows growth, particularly in automotive electronics, industrial automation, and optoelectronics sectors. Countries like Germany, France, and the Netherlands are key contributors, driven by stringent quality standards and a focus on advanced manufacturing processes. Investments in smart factory initiatives also bolster market expansion.

- Latin America: An emerging market with growing potential, driven by expanding manufacturing capabilities and increasing foreign investments in the electronics sector, particularly in countries like Mexico and Brazil. While smaller in market size compared to APAC, it presents opportunities for cost-effective and semi-automated solutions.

- Middle East and Africa (MEA): Currently a nascent market but with anticipated growth due to diversifying economies, increasing technological adoption, and nascent electronics manufacturing initiatives. Investments in data centers and telecom infrastructure are expected to contribute to future demand for die bonding equipment in this region.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Die Bonding Machine Market.- ASMPT

- Kulicke & Soffa

- BE Semiconductor Industries N.V. (Besi)

- Shinkawa Ltd.

- Toray Engineering Co., Ltd.

- Palomar Technologies, Inc.

- Nordson Corporation (Dage)

- F&K Delvotec GmbH

- Hanmi Semiconductor Co., Ltd.

- DISCO Corporation

- Kaijo Corporation

- Panasonic Corporation

- MRSI Systems (Mycronic)

- Microassembly Ltd.

- Finetech GmbH & Co. KG

- Tresky GmbH

- Yamaha Motor Co., Ltd.

- Datacon (Besi Group)

Frequently Asked Questions

Analyze common user questions about the Die Bonding Machine market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is a die bonding machine and its primary function?

A die bonding machine, also known as a die attach machine, is a specialized equipment used in semiconductor manufacturing to precisely attach a silicon die (chip) onto a substrate, lead frame, or another die. Its primary function is to create a secure electrical and mechanical connection, forming the foundation of an integrated circuit or electronic component.

What are the key drivers for the Die Bonding Machine market growth?

The key drivers for market growth include the surging global demand for semiconductors, rapid advancements in advanced packaging technologies (e.g., 3D ICs, SiP), the proliferation of IoT, 5G, and AI applications, and the increasing adoption of electronics in the automotive sector, particularly for electric vehicles and ADAS.

How does AI impact the performance of die bonding machines?

AI significantly enhances die bonding machine performance through improved precision via AI-powered vision systems, predictive maintenance capabilities to minimize downtime, real-time process optimization for higher yields, and automated defect detection. AI enables machines to adapt parameters intelligently, leading to superior quality and efficiency.

Which region dominates the Die Bonding Machine market?

The Asia Pacific (APAC) region currently dominates the Die Bonding Machine market due to the concentration of major semiconductor manufacturing facilities, extensive electronics production, and substantial investments in advanced packaging technologies in countries like China, Taiwan, South Korea, and Japan.

What are the main types of die bonding machines available?

Die bonding machines are primarily categorized by their level of automation: Automatic Die Bonders (high-volume, high-precision), Semi-automatic Die Bonders (flexible, for moderate volumes), and Manual Die Bonders (for R&D or low-volume specialized applications).

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted