Container Handling Equipment Market

Container Handling Equipment Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709948 | Last Updated : December 24, 2025 |

Format : ![]()

![]()

![]()

![]()

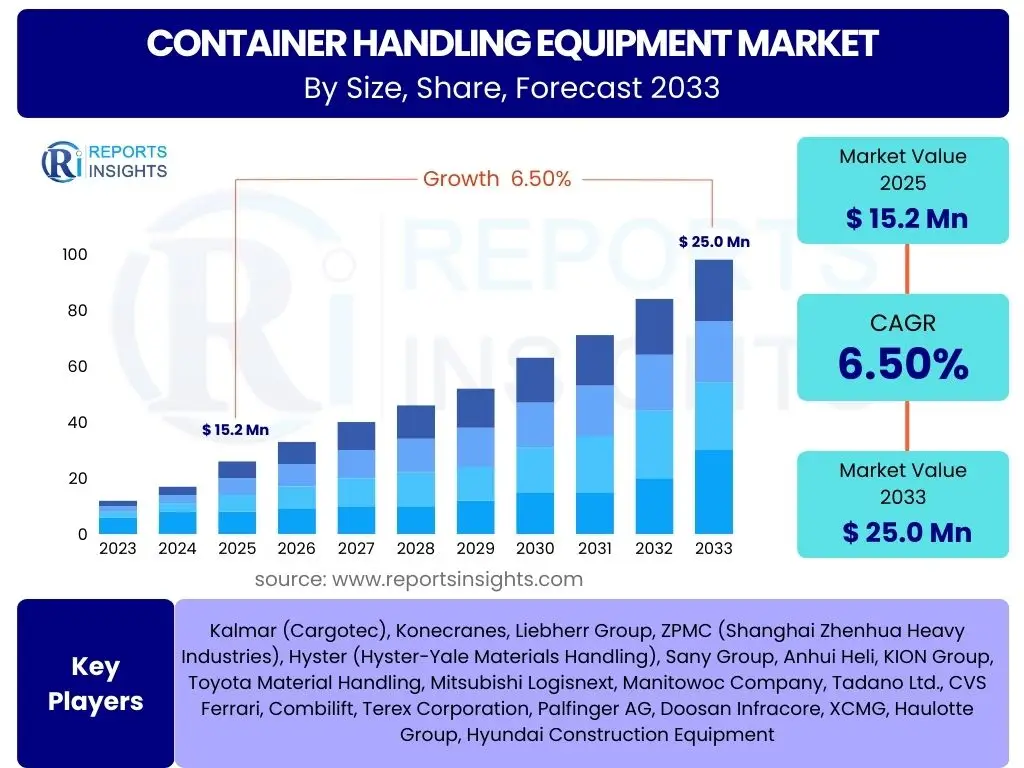

Container Handling Equipment Market Size

According to Reports Insights Consulting Pvt Ltd, The Container Handling Equipment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2025 and 2033. The market is estimated at USD 15.2 billion in 2025 and is projected to reach USD 25.0 billion by the end of the forecast period in 2033.

Key Container Handling Equipment Market Trends & Insights

The container handling equipment market is undergoing significant transformation driven by the escalating demand for global trade, the imperative for operational efficiency, and the adoption of advanced technologies. Users frequently inquire about the trajectory of automation, the impact of sustainability initiatives, and how digitalization is reshaping port operations. The market is witnessing a strong shift towards intelligent and interconnected systems that optimize cargo flow and reduce human intervention, addressing labor shortages and enhancing safety standards.

Furthermore, the focus on environmental sustainability is a predominant theme, with increasing investments in electric, hybrid, and hydrogen-powered equipment to meet stringent emission regulations and corporate sustainability goals. The integration of data analytics and IoT (Internet of Things) devices is providing real-time operational insights, predictive maintenance capabilities, and improved asset utilization. These advancements collectively aim to create more resilient, efficient, and eco-friendly supply chains capable of handling the increasing volume and complexity of global logistics.

- Automation and Digitization: Increased adoption of automated guided vehicles (AGVs), automated stacking cranes (ASCs), and remote-controlled equipment to enhance efficiency and reduce labor costs.

- Electrification and Decarbonization: Growing demand for electric, hybrid, and fuel cell-powered container handling equipment to reduce emissions and comply with environmental regulations.

- IoT and Data Analytics: Integration of IoT sensors and data analytics platforms for real-time monitoring, predictive maintenance, and optimized operational workflows.

- Modular and Flexible Equipment Design: Development of adaptable equipment that can be easily configured for various terminal layouts and operational requirements, improving versatility.

- Safety Enhancements: Implementation of advanced safety features, including collision avoidance systems, remote operation, and enhanced visibility solutions to minimize accidents.

AI Impact Analysis on Container Handling Equipment

Artificial intelligence is poised to revolutionize the container handling equipment sector by significantly enhancing operational intelligence, predictive capabilities, and autonomous functionalities. User inquiries often center on how AI can optimize crane movements, manage container flow in real-time, and contribute to fully autonomous ports. AI-powered algorithms are being developed to analyze vast amounts of operational data, predicting equipment failures, optimizing energy consumption, and dynamically scheduling tasks to maximize throughput and minimize idle times.

The application of AI extends beyond mere automation, enabling intelligent decision-making that can adapt to unforeseen circumstances, such as adverse weather conditions or sudden cargo volume spikes. This cognitive layer allows for more resilient and responsive port operations, contributing to improved efficiency and reduced operational costs. Concerns about job displacement are balanced by the potential for AI to create new roles in system management, data analysis, and robotics maintenance, while upskilling existing workforces for higher-value tasks.

- Predictive Maintenance: AI algorithms analyze sensor data to predict equipment failures, enabling proactive maintenance and reducing downtime.

- Optimized Container Flow: AI-driven systems manage the movement of containers within terminals, optimizing routes, stacking, and retrieval sequences for maximum efficiency.

- Autonomous Navigation and Operation: Enhanced autonomy for AGVs, straddle carriers, and cranes through AI-powered perception, planning, and control systems.

- Real-time Decision Making: AI facilitates instantaneous adjustments to operational plans based on live data, improving responsiveness to dynamic port conditions.

- Energy Efficiency Optimization: AI analyzes energy consumption patterns and adjusts equipment operation to minimize power usage, particularly in electric and hybrid fleets.

Key Takeaways Container Handling Equipment Market Size & Forecast

The container handling equipment market is on a robust growth trajectory, underscoring its pivotal role in facilitating global trade and logistics. Users frequently seek concise summaries of the market's growth potential, the primary factors driving expansion, and the long-term outlook for investment. The projected increase in market value from USD 15.2 billion in 2025 to USD 25.0 billion by 2033, at a CAGR of 6.5%, highlights a sustained demand fueled by increasing port modernization, expanding intermodal transportation networks, and the relentless pressure for greater operational efficiency.

The market's resilience is further supported by technological advancements, particularly in automation, electrification, and digital integration, which are becoming non-negotiable for competitive port and terminal operations. Stakeholders are keen to understand the implications of these trends on equipment procurement, infrastructure development, and workforce evolution. The consistent growth forecast suggests a stable yet dynamic market environment, where innovation and strategic investment in advanced equipment will be key determinants of success for market participants and end-users alike.

- Significant Market Expansion: The market is projected to grow from USD 15.2 billion in 2025 to USD 25.0 billion by 2033, indicating strong demand.

- Steady Growth Rate: A CAGR of 6.5% reflects consistent underlying growth drivers, including global trade expansion and port modernization.

- Technology as a Core Driver: Automation, electrification, and digitalization are crucial for future market growth and competitive advantage.

- Operational Efficiency Imperative: End-users are prioritizing equipment that enhances throughput, reduces operational costs, and improves safety.

- Long-term Investment Outlook: The positive forecast suggests favorable conditions for investment in advanced container handling solutions and related infrastructure.

Container Handling Equipment Market Drivers Analysis

The container handling equipment market is primarily propelled by the exponential growth in global containerized trade, which necessitates continuous upgrades and expansions of port and terminal infrastructure. As international commerce continues to expand, the demand for efficient and high-capacity equipment capable of managing larger vessels and increasing container volumes becomes critical. This global trade impetus is further amplified by the ongoing development of emerging economies, which are investing heavily in modernizing their logistics capabilities to support industrialization and exports.

Another significant driver is the persistent pressure for operational efficiency and cost reduction across the logistics value chain. Ports and terminals are increasingly adopting automation and digital technologies to accelerate turnaround times, minimize labor costs, and optimize space utilization. The drive for sustainability also plays a crucial role, with regulations and corporate environmental mandates pushing for the adoption of electric, hybrid, and low-emission equipment, thus stimulating demand for advanced and greener solutions.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Global Containerized Trade | +1.8% | Global, particularly Asia Pacific, Europe | Long-term (2025-2033) |

| Increasing Automation & Digitalization in Ports | +1.5% | North America, Europe, China | Mid to Long-term (2025-2030) |

| Demand for Operational Efficiency & Cost Reduction | +1.2% | Global | Long-term (2025-2033) |

| Focus on Sustainable & Green Logistics Solutions | +1.0% | Europe, North America, Japan | Mid to Long-term (2026-2033) |

| Infrastructure Development in Emerging Economies | +1.0% | Asia Pacific, Latin America, Africa | Long-term (2025-2033) |

Container Handling Equipment Market Restraints Analysis

The container handling equipment market faces several significant restraints that could impede its growth trajectory. One primary challenge is the substantial capital expenditure required for acquiring advanced and automated equipment. The high upfront investment for large-scale cranes, AGVs, and integrated terminal systems can be a deterrent for smaller ports or those with limited financial resources, particularly in developing regions. This financial barrier often leads to extended procurement cycles and delays in modernization efforts, affecting market penetration for cutting-edge solutions.

Another restraint is the complexity associated with integrating new, sophisticated equipment into existing port infrastructure and IT systems. Legacy systems often pose compatibility issues, requiring extensive customization and substantial training for personnel. Furthermore, the shortage of skilled labor capable of operating and maintaining advanced automated equipment presents a significant bottleneck. This labor challenge, coupled with potential resistance from traditional labor unions regarding automation, adds layers of complexity and cost to equipment adoption and deployment, affecting the pace of market expansion.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Expenditure for Equipment Procurement | -0.9% | Global, particularly smaller ports | Long-term (2025-2033) |

| Complexity of Integrating New Technologies with Legacy Systems | -0.7% | Global, older ports | Mid-term (2025-2029) |

| Shortage of Skilled Labor for Advanced Equipment | -0.6% | North America, Europe | Long-term (2025-2033) |

| Economic Volatility and Trade Protectionism | -0.5% | Global, specific trade blocs | Short to Mid-term (2025-2027) |

| Infrastructure Limitations at Smaller Ports | -0.4% | Developing regions | Long-term (2025-2033) |

Container Handling Equipment Market Opportunities Analysis

The container handling equipment market presents several compelling opportunities for growth, driven by the continuous evolution of logistics and supply chain demands. The expansion of port capacities and the development of new deep-sea terminals, particularly in rapidly urbanizing coastal regions and key trade routes, create a sustained demand for a wide range of specialized equipment. Investments in infrastructure upgrades, often backed by government initiatives and international trade agreements, pave the way for modern, high-capacity handling solutions capable of servicing ultra-large container vessels.

Furthermore, the increasing adoption of Industry 4.0 principles, including the integration of IoT, AI, and big data analytics, offers significant avenues for innovation. Manufacturers and service providers can capitalize on developing smarter, interconnected equipment that offers enhanced predictive maintenance, real-time diagnostics, and optimized operational workflows. The growing emphasis on environmental sustainability also opens opportunities for developing and deploying electric, hydrogen-powered, and other low-emission equipment, aligning with global green initiatives and regulatory mandates, providing a competitive edge for environmentally conscious solutions.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion of Port Capacities & New Terminal Development | +1.3% | Asia Pacific, Middle East, Africa | Long-term (2025-2033) |

| Integration of Advanced IoT & AI Technologies | +1.1% | Global | Mid to Long-term (2025-2032) |

| Growing Demand for Electric & Hydrogen-Powered Equipment | +1.0% | Europe, North America, Japan | Mid to Long-term (2026-2033) |

| Development of Intermodal Transportation Networks | +0.9% | North America, Europe, China | Long-term (2025-2033) |

| Aftermarket Services and Maintenance Contracts Growth | +0.8% | Global | Long-term (2025-2033) |

Container Handling Equipment Market Challenges Impact Analysis

The container handling equipment market is confronted by several formidable challenges that require strategic responses from manufacturers and operators. One significant challenge stems from geopolitical instabilities and trade wars, which can disrupt global supply chains, alter trade routes, and lead to unpredictable fluctuations in container volumes. Such uncertainties make long-term investment planning difficult for ports and equipment manufacturers, potentially leading to subdued demand in certain periods or regions.

Moreover, the intense competition within the equipment manufacturing sector, particularly from Asian players offering cost-effective solutions, pressures established companies to innovate continually while maintaining competitive pricing. This drives down profit margins and necessitates robust R&D investment. Additionally, regulatory complexities, including varying safety standards and environmental mandates across different regions, create hurdles for global market entry and product standardization, requiring localized adaptations and increasing compliance costs for market participants.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Geopolitical Instabilities & Trade Protectionism | -0.8% | Global | Short to Mid-term (2025-2027) |

| Intense Competition & Price Pressure from Manufacturers | -0.7% | Global | Long-term (2025-2033) |

| High R&D Costs for Innovation & Technology Upgrades | -0.6% | Global | Long-term (2025-2033) |

| Cybersecurity Risks in Automated & Connected Systems | -0.5% | Global, technologically advanced regions | Long-term (2025-2033) |

| Adherence to Diverse Environmental Regulations | -0.4% | Europe, North America, China | Mid to Long-term (2026-2033) |

Container Handling Equipment Market - Updated Report Scope

This comprehensive market report provides an in-depth analysis of the Container Handling Equipment market, offering detailed insights into market dynamics, segmentation, regional outlook, and competitive landscape. It covers a historical period to identify foundational trends and projects future growth across various segments, considering technological advancements and regulatory impacts. The scope is designed to equip stakeholders with actionable intelligence for strategic decision-making in a rapidly evolving global logistics environment.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 15.2 Billion |

| Market Forecast in 2033 | USD 25.0 Billion |

| Growth Rate | 6.5% CAGR |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Kalmar (Cargotec), Konecranes, Liebherr Group, ZPMC (Shanghai Zhenhua Heavy Industries), Hyster (Hyster-Yale Materials Handling), Sany Group, Anhui Heli, KION Group, Toyota Material Handling, Mitsubishi Logisnext, Manitowoc Company, Tadano Ltd., CVS Ferrari, Combilift, Terex Corporation, Palfinger AG, Doosan Infracore, XCMG, Haulotte Group, Hyundai Construction Equipment |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Container Handling Equipment market is meticulously segmented to provide a granular understanding of its diverse components and their respective contributions to overall market growth. This segmentation allows for a detailed analysis of demand patterns, technological preferences, and operational requirements across different end-user industries and geographic regions. Understanding these distinct segments is crucial for manufacturers to tailor their product offerings and for end-users to make informed procurement decisions that align with their specific operational contexts and sustainability goals.

The market is primarily divided by equipment type, which includes a wide range of machinery from traditional forklifts to advanced automated gantry cranes, reflecting varying capacities and functionalities. Further segmentation by application highlights the key sectors utilizing this equipment, such as busy international ports, inland depots, and manufacturing facilities, each with unique operational demands. Additionally, segmentation by power source and automation level underscores the industry's shift towards greener and more efficient technologies, catering to evolving environmental regulations and the ongoing pursuit of operational excellence.

- By Equipment Type: This segment encompasses a broad spectrum of machinery, from agile reach stackers and versatile forklift trucks to massive ship-to-shore cranes and advanced automated guided vehicles (AGVs), each designed for specific container handling tasks.

- By Application: This segmentation details the primary end-use sectors, including bustling Ports & Terminals, efficient Inland Container Depots (ICDs) & Container Freight Stations (CFSs), diverse Manufacturing & Logistics hubs, and critical Rail Yards, each requiring specialized equipment solutions.

- By Power Source: This segment delineates equipment based on their energy supply, including conventional Diesel, environmentally friendly Electric, fuel-efficient Hybrid, and emerging Fuel Cell technologies, reflecting the industry's drive towards sustainability.

- By Automation Level: This classification categorizes equipment by their degree of autonomy, ranging from traditional Manual operations to Semi-Automated systems with operator assistance, and cutting-edge Fully Automated solutions that operate with minimal human intervention.

Regional Highlights

Regional analysis of the Container Handling Equipment market reveals diverse growth dynamics influenced by local economic conditions, trade volumes, infrastructural development, and regulatory landscapes. Asia Pacific emerges as a dominant and rapidly growing region, driven by its expansive manufacturing base, surging international trade, and significant investments in port expansion and modernization, particularly in countries like China, India, and Southeast Asian nations. The region's increasing adoption of automation and sustainable technologies further propels market expansion.

Europe and North America represent mature markets characterized by high levels of automation, stringent environmental regulations, and a strong emphasis on operational efficiency and safety. These regions are witnessing a continuous demand for advanced, electric, and hybrid equipment, along with sophisticated software solutions for terminal management. Latin America, the Middle East, and Africa are also showing promising growth, albeit from a smaller base, fueled by infrastructure projects, increasing regional trade, and strategic investments in logistics capabilities to enhance global connectivity. Each region presents unique opportunities and challenges that shape market development.

- Asia Pacific (APAC): Dominant market share due to robust manufacturing, high trade volumes, and extensive port development in China, India, and Southeast Asian countries. Significant investment in automation and eco-friendly equipment.

- Europe: Mature market with strong focus on automation, digitalization, and electrification to meet stringent environmental standards and optimize port operations across key maritime hubs.

- North America: Stable demand driven by port modernization projects, expansion of intermodal facilities, and a growing emphasis on autonomous and semi-automated solutions to enhance efficiency and address labor shortages.

- Middle East & Africa (MEA): Emerging growth region with substantial investments in new port infrastructure and logistics hubs, particularly in the UAE, Saudi Arabia, and developing African nations, supporting increasing trade flows.

- Latin America: Moderate growth fueled by commodity exports, regional trade agreements, and ongoing infrastructure upgrades in countries like Brazil and Mexico, leading to demand for efficient handling equipment.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Container Handling Equipment Market.- Kalmar (Cargotec)

- Konecranes

- Liebherr Group

- ZPMC (Shanghai Zhenhua Heavy Industries)

- Hyster (Hyster-Yale Materials Handling)

- Sany Group

- Anhui Heli

- KION Group

- Toyota Material Handling

- Mitsubishi Logisnext

- Manitowoc Company

- Tadano Ltd.

- CVS Ferrari

- Combilift

- Terex Corporation

- Palfinger AG

- Doosan Infracore

- XCMG

- Haulotte Group

- Hyundai Construction Equipment

Frequently Asked Questions

Analyze common user questions about the Container Handling Equipment market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the projected growth rate for the Container Handling Equipment Market?

The Container Handling Equipment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2025 and 2033, reaching USD 25.0 billion by the end of the forecast period.

What are the primary drivers of growth in the Container Handling Equipment Market?

Key drivers include the growth in global containerized trade, increasing demand for automation and digitalization in ports, the imperative for operational efficiency, and the rising focus on sustainable and green logistics solutions.

How is AI impacting the Container Handling Equipment sector?

AI is significantly impacting the sector by enabling predictive maintenance, optimizing container flow, enhancing autonomous navigation, facilitating real-time decision-making, and improving energy efficiency for container handling operations.

What are the major challenges faced by the Container Handling Equipment Market?

Major challenges include high capital expenditure for equipment, the complexity of integrating new technologies with legacy systems, geopolitical instabilities, intense market competition, and the shortage of skilled labor.

Which regions are expected to show significant growth in container handling equipment adoption?

Asia Pacific is expected to exhibit significant growth due to extensive trade volumes and infrastructure development, while Europe and North America will continue to lead in adopting advanced, automated, and eco-friendly solutions.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted