Precision Reduction Gear Market

Precision Reduction Gear Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700814 | Last Updated : July 28, 2025 |

Format : ![]()

![]()

![]()

![]()

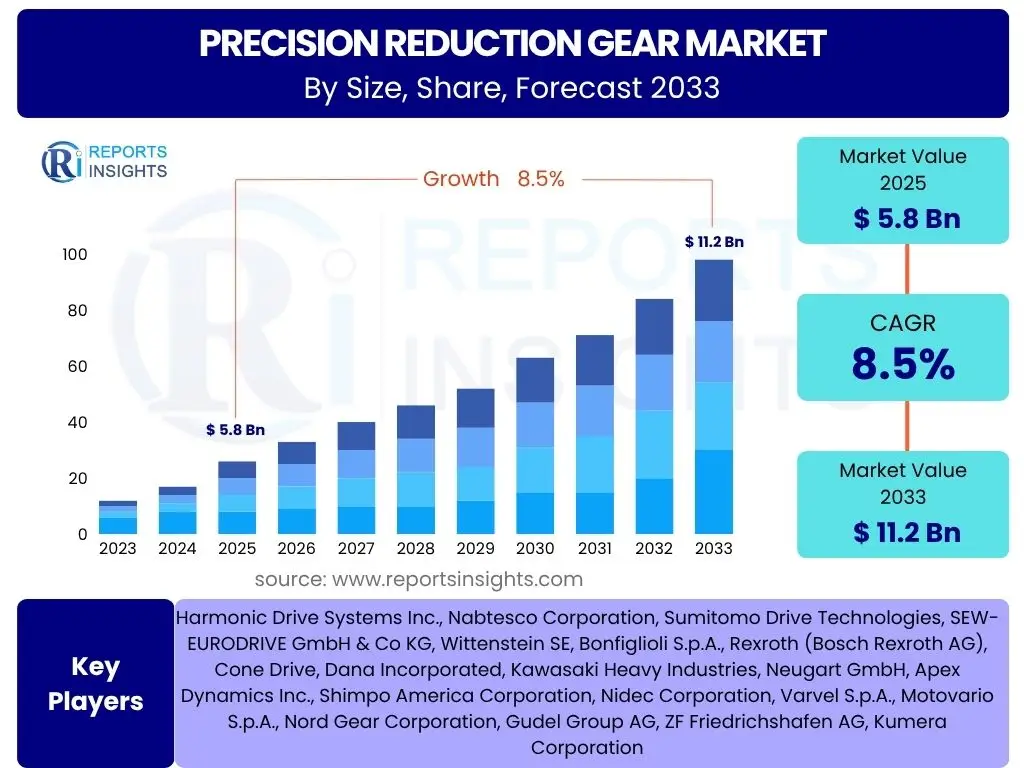

Precision Reduction Gear Market Size

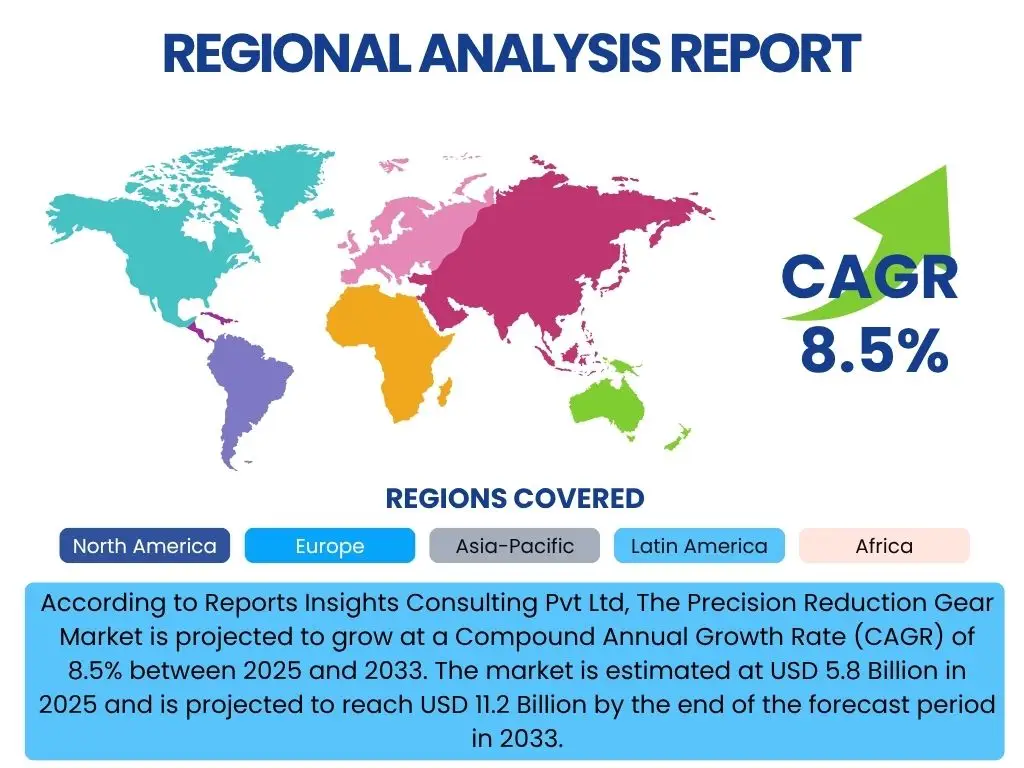

According to Reports Insights Consulting Pvt Ltd, The Precision Reduction Gear Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2025 and 2033. The market is estimated at USD 5.8 Billion in 2025 and is projected to reach USD 11.2 Billion by the end of the forecast period in 2033.

Key Precision Reduction Gear Market Trends & Insights

The precision reduction gear market is undergoing significant transformation, driven by a confluence of technological advancements and evolving industrial demands. A primary trend involves the increasing integration of these gears into advanced robotic systems and automation solutions across various sectors. This surge is fueled by the global push for higher manufacturing efficiency, improved precision in delicate operations, and the widespread adoption of Industry 4.0 principles, which necessitate robust and accurate motion control components.

Another prominent insight reveals a growing demand for miniaturized and lightweight precision gears. As industries move towards more compact machinery, portable automation, and high-density production lines, the ability to deliver high torque and precise motion in a smaller footprint becomes critical. This trend is particularly evident in medical robotics, consumer electronics manufacturing, and compact industrial automation, driving innovation in material science and design methodologies to achieve higher power density and reduced weight without compromising performance.

Furthermore, the market is observing a rising emphasis on smart gears equipped with sensors for real-time monitoring and predictive maintenance. This integration allows for continuous assessment of gear performance, temperature, vibration, and wear, enabling proactive maintenance schedules and significantly reducing downtime. Such capabilities align with the broader digitalization initiatives within industrial settings, offering enhanced reliability, extended operational lifespan, and optimized overall equipment effectiveness (OEE) for end-users.

- Increased adoption of industrial and collaborative robots.

- Growing demand for miniaturized and lightweight gear solutions.

- Integration of smart sensing capabilities for predictive maintenance.

- Emphasis on high-efficiency and low-backlash designs.

- Expansion into new application areas such as medical and aerospace.

- Development of advanced materials for enhanced durability and performance.

AI Impact Analysis on Precision Reduction Gear

Artificial Intelligence (AI) is poised to significantly impact the precision reduction gear market, primarily by revolutionizing design, manufacturing, and operational aspects. In the design phase, AI-powered generative design tools can explore countless configurations and material combinations, optimizing gear geometry for specific performance parameters like torque density, backlash, and noise reduction, far beyond what traditional human-led design can achieve. This enables the creation of more efficient, durable, and customized gear solutions that meet increasingly stringent application requirements.

In manufacturing, AI and machine learning algorithms are enhancing process control, quality assurance, and predictive maintenance. AI-driven vision systems can inspect gears for microscopic defects with unparalleled accuracy, ensuring consistent quality. Machine learning models analyze real-time data from production lines to optimize machining parameters, reduce waste, and identify potential equipment failures before they occur, thereby improving manufacturing efficiency and reducing operational costs for gear producers. This leads to higher yield rates and better overall product reliability.

Operationally, AI contributes to the longevity and performance of precision reduction gears through advanced analytics and intelligent control systems within the machinery they power. AI algorithms can optimize motion profiles to reduce stress on gears, predict remaining useful life based on operational data, and even adapt control strategies to compensate for wear, extending maintenance intervals and minimizing unexpected breakdowns. This proactive approach significantly enhances the value proposition of precision reduction gears in high-stakes applications such, robotics, and aerospace, by ensuring peak performance and reliability throughout their lifecycle.

- AI-driven generative design for optimized gear geometry and performance.

- Enhanced manufacturing precision and quality control through AI vision systems.

- Predictive maintenance analytics for extended gear lifespan and reduced downtime.

- Optimization of machining processes and parameters using machine learning.

- Development of intelligent control systems that adapt to gear wear and optimize operational loads.

Key Takeaways Precision Reduction Gear Market Size & Forecast

The precision reduction gear market is on a robust growth trajectory, driven by an accelerating global demand for automation, robotics, and high-precision machinery across diverse industries. The significant projected Compound Annual Growth Rate (CAGR) indicates a dynamic expansion, reflecting fundamental shifts in manufacturing paradigms towards higher efficiency, greater accuracy, and enhanced system reliability. This growth is not merely incremental but represents a fundamental adoption of advanced motion control solutions in increasingly sophisticated applications.

A crucial takeaway is the pervasive influence of Industry 4.0 initiatives and the widespread integration of advanced robotics. These technologies are not only expanding the traditional scope of precision gears but are also creating new, highly specialized application niches. The market's upward forecast is a direct consequence of industries investing heavily in automated production lines, medical devices, aerospace systems, and renewable energy infrastructure, all of which rely critically on the superior performance and durability of precision reduction gears for optimal operation.

Furthermore, the market's anticipated financial milestones, reaching substantial valuations by the end of the forecast period, underscore the strategic importance of these components. The consistent growth highlights resilient demand, driven by technological evolution within end-user industries and the continuous innovation by gear manufacturers. This indicates a healthy market environment characterized by ongoing research and development aimed at improving power density, reducing backlash, enhancing efficiency, and exploring new material applications to meet the evolving and stringent demands of high-tech industries globally.

- Strong market growth fueled by automation and robotics adoption.

- Significant expansion across industrial, medical, and aerospace sectors.

- Continuous innovation in gear design and materials for enhanced performance.

- Increasing integration of smart features for improved reliability and maintenance.

- Market size projected to nearly double by 2033, indicating robust demand.

Precision Reduction Gear Market Drivers Analysis

The precision reduction gear market is primarily propelled by the burgeoning growth in the global robotics and automation industries. As manufacturers worldwide increasingly adopt industrial and collaborative robots to enhance productivity, reduce labor costs, and improve operational safety, the demand for high-precision, low-backlash gearing systems becomes indispensable. These gears are critical components enabling the accurate and repetitive movements essential for advanced robotic arms, automated guided vehicles (AGVs), and sophisticated pick-and-place machines, directly correlating their market expansion with robotic deployments.

Another significant driver is the rapid advancement and widespread adoption of Industry 4.0 principles, including smart manufacturing, the Internet of Things (IoT), and digital factories. These initiatives demand highly precise and reliable motion control components that can seamlessly integrate into networked systems, provide real-time data, and operate efficiently in complex, interconnected environments. Precision reduction gears, with their ability to deliver accurate and repeatable motion, are foundational to achieving the synchronized and optimized processes central to Industry 4.0 architectures.

Furthermore, the expanding applications in critical sectors such as medical devices, aerospace and defense, and semiconductor manufacturing significantly contribute to market growth. In these industries, the need for extreme accuracy, reliability, and compact designs is paramount. Precision gears are essential for surgical robots, advanced imaging systems, satellite positioning mechanisms, and wafer handling equipment, where even marginal errors can have severe consequences. This pushes innovation in gear technology, driving demand for specialized and high-performance solutions.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Surging Robotics and Automation Adoption | +2.5% | Global, particularly Asia Pacific, Europe, North America | Short to Mid-term (2025-2030) |

| Industry 4.0 and Smart Manufacturing Initiatives | +2.0% | Global, strong in developed economies | Mid-term (2026-2033) |

| Growing Demand in Medical and Aerospace Sectors | +1.8% | North America, Europe, select APAC countries | Mid to Long-term (2027-2033) |

| Miniaturization and Compact Design Trends | +1.5% | Global, especially electronics manufacturing hubs | Short to Mid-term (2025-2030) |

Precision Reduction Gear Market Restraints Analysis

Despite the robust growth drivers, the precision reduction gear market faces several significant restraints, notably the high initial cost associated with these specialized components. Manufacturing precision gears requires advanced materials, intricate machining processes, and rigorous quality control, all of which contribute to a substantially higher price point compared to standard gears. This elevated cost can be a deterrent for small and medium-sized enterprises (SMEs) or for applications where budget constraints override the need for extreme precision, thereby limiting market penetration in certain segments.

Another key restraint is the complexity of design and manufacturing, which demands highly specialized expertise and sophisticated production facilities. The stringent requirements for low backlash, high torque density, and compact form factors necessitate highly skilled engineers and technicians, as well as significant investments in R&D and advanced manufacturing equipment. This creates a high barrier to entry for new players and can slow down innovation cycles, as the development of new gear technologies is resource-intensive and time-consuming.

Furthermore, the susceptibility to wear and tear, coupled with the need for precise installation and maintenance, poses a challenge. While precision gears are designed for durability, their intricate nature makes them vulnerable to damage from improper installation, lack of lubrication, or operation outside specified parameters. Repair or replacement of these components can be costly and time-consuming, leading to potential downtime for end-user systems. Educating users on proper handling and maintenance is crucial, yet this ongoing operational cost and potential for failure can act as a restraint on broader adoption.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Cost and Investment | -1.2% | Global, particularly cost-sensitive emerging markets | Short to Mid-term (2025-2030) |

| Complexity of Design and Manufacturing | -1.0% | Global | Mid to Long-term (2027-2033) |

| Vulnerability to Wear and Tear; Maintenance Needs | -0.8% | Global | Short to Mid-term (2025-2030) |

| Availability of Alternative Motion Control Solutions | -0.7% | Global, in less demanding applications | Short to Mid-term (2025-2030) |

Precision Reduction Gear Market Opportunities Analysis

The precision reduction gear market is presented with significant opportunities arising from the burgeoning demand for collaborative robots, or "cobots." Unlike traditional industrial robots, cobots are designed to work alongside human operators, necessitating extremely safe, precise, and quiet motion. This creates a specialized demand for compact, lightweight, and low-backlash precision gears that can ensure smooth and controlled movements, opening up new design and application avenues for manufacturers to innovate in this rapidly expanding segment of the robotics market.

Another substantial opportunity lies in the continued growth of the medical and healthcare sector, particularly in surgical robotics, rehabilitation devices, and advanced diagnostic equipment. The aging global population and increasing investment in healthcare infrastructure are driving the need for highly accurate and reliable automated solutions. Precision reduction gears are critical for the delicate and precise movements required in these applications, offering a fertile ground for market expansion, especially with the trend towards minimally invasive procedures and personalized medicine.

Furthermore, the proliferation of electric vehicles (EVs) and the broader transition towards electric propulsion systems across various transportation modes, including aerospace and marine, present a long-term growth opportunity. Precision gears are essential in EV powertrains for optimal power transfer and efficiency, as well as in auxiliary systems requiring precise motion control. As the automotive industry shifts from internal combustion engines, the demand for specialized, high-performance gears that can withstand high torques and operate quietly in electric systems is set to accelerate, opening up a new high-volume market segment.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Collaborative Robotics (Cobots) Market | +1.8% | Global, especially North America, Europe, Asia Pacific | Short to Mid-term (2025-2030) |

| Expansion in Medical and Healthcare Sector | +1.5% | North America, Europe, developed Asia Pacific countries | Mid to Long-term (2027-2033) |

| Emergence of Electric Vehicles and E-Mobility | +1.3% | Global, strong in China, Europe, North America | Mid to Long-term (2028-2033) |

| Additive Manufacturing for Custom Gear Production | +1.0% | Global, for specialized and niche applications | Long-term (2029-2033) |

Precision Reduction Gear Market Challenges Impact Analysis

The precision reduction gear market faces the significant challenge of managing manufacturing complexity and maintaining stringent quality control. The production of these gears demands exceptionally tight tolerances, specialized heat treatments, and complex machining processes to achieve the required levels of accuracy, low backlash, and high efficiency. Ensuring consistent quality across large production volumes, especially for customized or highly specialized applications, poses a considerable hurdle, requiring continuous investment in advanced machinery, quality assurance systems, and highly skilled personnel.

Another key challenge is the intense competition and pricing pressure from established players, particularly in mature markets. The precision reduction gear market is dominated by a few large, well-established manufacturers with extensive R&D capabilities, strong distribution networks, and economies of scale. New entrants or smaller players often struggle to compete on price while maintaining the necessary quality standards. This pressure can erode profit margins and limit investment in innovation for some market participants, particularly in regions where cost-effectiveness is a primary purchasing criterion.

Furthermore, the global supply chain vulnerabilities, exacerbated by geopolitical tensions and unforeseen events such as pandemics, present a persistent challenge. The sourcing of high-grade raw materials, specialized components, and maintaining efficient logistics channels across continents can be disrupted, leading to increased lead times, higher costs, and production delays. Relying on a limited number of specialized suppliers for critical materials or processes can further amplify these risks, compelling manufacturers to diversify their supply chains and build greater resilience, which adds to operational complexity and costs.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Manufacturing Complexity and Quality Control | -0.9% | Global | Ongoing (2025-2033) |

| Intense Competition and Pricing Pressure | -0.8% | Global, particularly in competitive markets like Asia Pacific | Short to Mid-term (2025-2030) |

| Supply Chain Disruptions and Material Sourcing | -0.7% | Global | Short to Mid-term (2025-2028) |

| Attracting and Retaining Skilled Workforce | -0.6% | Global, particularly developed economies | Mid to Long-term (2027-2033) |

Precision Reduction Gear Market - Updated Report Scope

This comprehensive market research report delves into the intricate dynamics of the global precision reduction gear market, providing a detailed analysis of its size, growth trajectory, key trends, and influencing factors. It offers an in-depth exploration of market segmentation by type, application, and end-use industry, alongside a robust regional analysis to highlight geographical disparities and opportunities. The report also profiles leading market players, assessing their competitive strategies and product offerings to provide a holistic view of the market landscape and future outlook.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 5.8 Billion |

| Market Forecast in 2033 | USD 11.2 Billion |

| Growth Rate | 8.5% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Harmonic Drive Systems Inc., Nabtesco Corporation, Sumitomo Drive Technologies, SEW-EURODRIVE GmbH & Co KG, Wittenstein SE, Bonfiglioli S.p.A., Rexroth (Bosch Rexroth AG), Cone Drive, Dana Incorporated, Kawasaki Heavy Industries, Neugart GmbH, Apex Dynamics Inc., Shimpo America Corporation, Nidec Corporation, Varvel S.p.A., Motovario S.p.A., Nord Gear Corporation, Gudel Group AG, ZF Friedrichshafen AG, Kumera Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The precision reduction gear market is meticulously segmented to provide granular insights into its diverse components and application areas. This segmentation allows for a detailed analysis of market dynamics, identifying specific high-growth areas and emerging trends within each category. The primary segmentation includes analysis by gear type, reflecting the different design philosophies and performance characteristics; by application, showcasing the specific industrial and technological uses; and by end-use industry, illustrating the broad spectrum of sectors leveraging these advanced components.

- By Type: Harmonic Drive, Cycloidal Drive, Planetary Gear, Worm Gear, Spur Gear, Bevel Gear, and Others.

- By Application: Robotics (Industrial Robots, Collaborative Robots, Service Robots), Machine Tools, Semiconductor Manufacturing Equipment, Medical Devices, Aerospace & Defense, Automotive, Packaging & Printing Machinery, Textile Machinery, Material Handling Equipment, and Others.

- By End-use Industry: Manufacturing & Automation, Automotive, Healthcare, Aerospace & Defense, Electronics & Semiconductor, Energy & Power, Logistics & Warehousing, Food & Beverage, and Others.

Regional Highlights

- North America: This region is a significant market for precision reduction gears, driven by substantial investments in industrial automation, advanced manufacturing, and the robust growth of the aerospace and defense sectors. The United States, in particular, leads in adopting robotics and advanced medical technologies, fueling demand for high-precision motion control. Canadian and Mexican markets also contribute, albeit to a lesser extent, with increasing automation in their manufacturing sectors. The presence of leading research institutions and technological innovation hubs further accelerates market expansion through continuous R&D and application development.

- Europe: Europe represents a mature yet highly innovative market, characterized by strong industrial bases in Germany, Italy, and France. The region's emphasis on Industry 4.0, advanced automotive manufacturing (including electric vehicles), and sophisticated machine tool production drives consistent demand for precision gears. Countries like Switzerland and the Netherlands also contribute significantly due to their strong presence in specialized machinery and robotics. European manufacturers are at the forefront of developing energy-efficient and highly precise gear solutions, catering to stringent quality and performance standards.

- Asia Pacific (APAC): APAC is the fastest-growing region in the precision reduction gear market, primarily propelled by rapid industrialization, burgeoning manufacturing sectors, and aggressive adoption of automation in countries like China, Japan, South Korea, and India. China's massive manufacturing output and its "Made in China 2025" initiative heavily emphasize robotics and smart factories, creating immense demand. Japan and South Korea, established leaders in industrial robotics and electronics, continue to drive innovation and adoption. India's growing manufacturing base and increasing foreign investments are also contributing to accelerated market growth. This region's large and expanding industrial base makes it a critical area for market players.

- Latin America: The Latin American market for precision reduction gears is experiencing gradual growth, primarily influenced by expanding manufacturing and automotive industries in Brazil and Mexico. While smaller in scale compared to other regions, increasing foreign direct investment in automation and the modernization of industrial infrastructure are fostering demand. The focus is often on cost-effective yet reliable solutions, with opportunities arising from efforts to enhance productivity and competitiveness in various manufacturing sectors.

- Middle East and Africa (MEA): The MEA region is an emerging market for precision reduction gears, with growth primarily driven by diversification efforts away from oil and gas, particularly in the UAE and Saudi Arabia. Investments in new industrial cities, infrastructure projects, and the adoption of automation in sectors like logistics, food processing, and defense are creating nascent demand. While the overall market size is currently smaller, the potential for long-term growth is significant as these economies continue to industrialize and embrace technological advancements in their pursuit of economic transformation.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Precision Reduction Gear Market.- Harmonic Drive Systems Inc.

- Nabtesco Corporation

- Sumitomo Drive Technologies

- SEW-EURODRIVE GmbH & Co KG

- Wittenstein SE

- Bonfiglioli S.p.A.

- Rexroth (Bosch Rexroth AG)

- Cone Drive

- Dana Incorporated

- Kawasaki Heavy Industries

- Neugart GmbH

- Apex Dynamics Inc.

- Shimpo America Corporation

- Nidec Corporation

- Varvel S.p.A.

- Motovario S.p.A.

- Nord Gear Corporation

- Gudel Group AG

- ZF Friedrichshafen AG

- Kumera Corporation

Frequently Asked Questions

What are precision reduction gears?

Precision reduction gears are highly engineered mechanical components designed to accurately transmit rotational motion and multiply torque while minimizing backlash (lost motion) and ensuring high positional accuracy. They are crucial for applications requiring precise control, smooth operation, and high reliability, such as robotics, machine tools, and aerospace systems.

What industries primarily utilize precision reduction gears?

Key industries that extensively use precision reduction gears include robotics and automation, machine tools, semiconductor manufacturing, medical devices (e.g., surgical robots), aerospace and defense, automotive (especially electric vehicles), and packaging and printing machinery. Their precise motion control capabilities are vital across these high-tech sectors.

What are the main types of precision reduction gears?

The primary types include Harmonic Drive gears (for high precision and zero backlash), Cycloidal Drive gears (for high torque density and shock resistance), Planetary gears (for compact size and high efficiency), and specialized Worm, Spur, and Bevel gears adapted for precision applications. Each type offers distinct advantages depending on specific application requirements.

How does AI influence the precision reduction gear market?

AI impacts the market by enabling generative design for optimized gear geometry, enhancing manufacturing precision through AI-powered quality control and process optimization, and facilitating predictive maintenance by analyzing operational data. This leads to more efficient, durable, and reliable gear solutions, streamlining production and extending product lifespans.

What is the growth outlook for the precision reduction gear market?

The precision reduction gear market is projected for robust growth, with a Compound Annual Growth Rate (CAGR) of 8.5% from 2025 to 2033, reaching an estimated USD 11.2 Billion by 2033. This growth is primarily driven by the accelerating adoption of robotics and automation across global industries, coupled with continuous technological advancements in gear design and manufacturing.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted