Consumer Credit Market

Consumer Credit Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702052 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

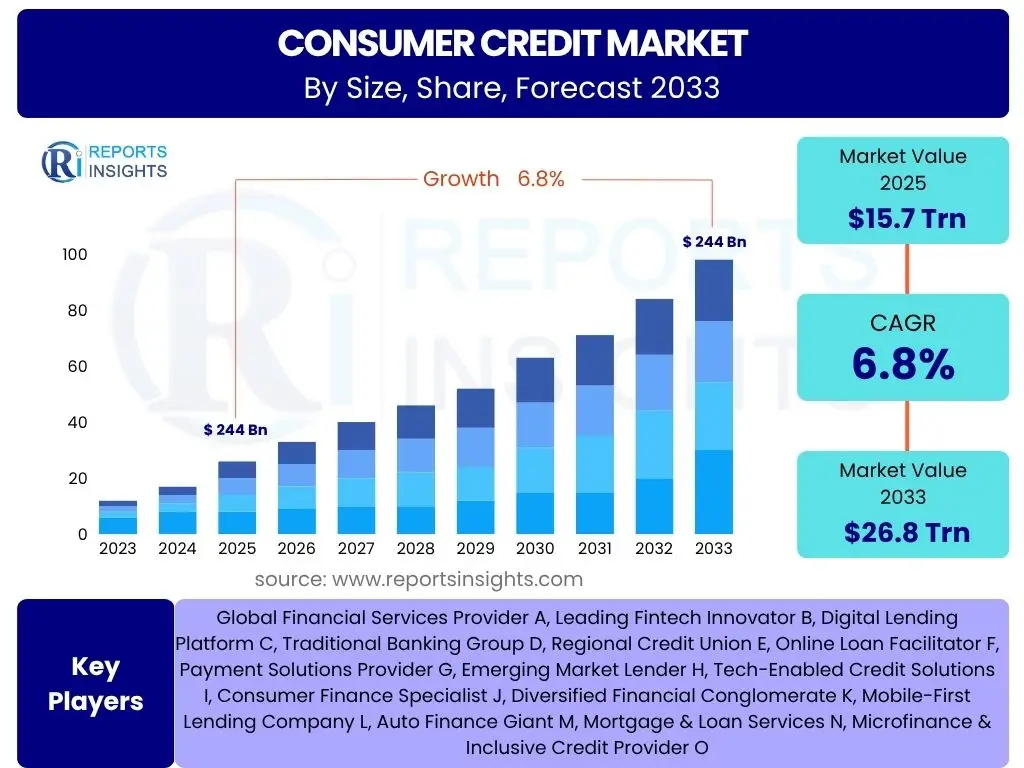

Consumer Credit Market Size

According to Reports Insights Consulting Pvt Ltd, The Consumer Credit Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 15.7 trillion in 2025 and is projected to reach USD 26.8 trillion by the end of the forecast period in 2033.

Key Consumer Credit Market Trends & Insights

The consumer credit landscape is undergoing significant transformation, driven by technological advancements, evolving consumer expectations, and a dynamic regulatory environment. Users frequently inquire about the shift towards digital lending platforms, the increasing demand for personalized credit products, and the influence of alternative data in credit assessment. These inquiries highlight a collective interest in how innovation is making credit more accessible, efficient, and tailored to individual needs, while also raising questions about the associated risks and regulatory responses.

Another major area of user curiosity revolves around the rise of embedded finance and Buy Now, Pay Later (BNPL) schemes. These models are redefining traditional credit access points, integrating financial services directly into consumer purchasing journeys. The widespread adoption of mobile banking and digital wallets further accelerates these trends, enabling seamless transactions and immediate credit decisions. Consequently, the market is witnessing a surge in competition from fintech companies, pushing established banks to innovate and adapt their service offerings to remain relevant.

- Digitalization of credit application and approval processes.

- Increased demand for personalized and flexible credit products.

- Proliferation of Buy Now, Pay Later (BNPL) solutions.

- Greater adoption of alternative data sources for credit scoring.

- Integration of embedded finance solutions across various consumer touchpoints.

- Focus on financial wellness and responsible lending practices.

AI Impact Analysis on Consumer Credit

Common user questions regarding AI's impact on consumer credit predominantly center on its role in enhancing efficiency, improving risk assessment, and personalizing offerings. Users are keen to understand how artificial intelligence and machine learning algorithms are revolutionizing traditional underwriting processes by analyzing vast datasets, enabling faster and more accurate credit decisions. This technological advancement allows lenders to identify creditworthy individuals beyond conventional credit scores, potentially expanding access to credit for underserved populations while simultaneously mitigating fraud risks.

Furthermore, there is significant interest in AI's capacity to deliver hyper-personalized financial products and services. Through predictive analytics, AI can anticipate consumer needs and preferences, leading to tailored loan products, dynamic interest rates, and proactive financial advice. While these capabilities promise a more customer-centric credit experience, users also express concerns about data privacy, algorithmic bias, and the ethical implications of AI-driven decision-making. The industry is actively addressing these concerns through the development of explainable AI (XAI) and robust ethical guidelines to ensure fairness and transparency.

- Enhanced credit risk assessment through advanced analytics and machine learning.

- Automation of loan application processing and approval, reducing turnaround times.

- Improved fraud detection and prevention mechanisms.

- Development of highly personalized credit products and pricing models.

- Greater efficiency in customer service through AI-powered chatbots and virtual assistants.

- Potential for expanded credit access for thin-file or unbanked populations.

Key Takeaways Consumer Credit Market Size & Forecast

Analyzing common user questions about the consumer credit market size and forecast reveals a strong interest in understanding the underlying drivers of growth and the long-term sustainability of current market trends. Users frequently inquire about the factors contributing to the projected expansion, such as rising disposable incomes, urbanization, and the expanding digital economy. The insights suggest that the market's growth is not merely cyclical but indicative of deeper structural shifts in consumer behavior and financial technology adoption.

Another prevalent theme in user queries relates to the resilience of the consumer credit market amidst economic fluctuations and potential regulatory changes. There is a clear desire to grasp how evolving macroeconomic conditions, interest rate policies, and government interventions might influence market trajectory. The forecast indicates a robust growth trajectory, underpinned by continuous innovation in product offerings and delivery channels, alongside a growing global middle class seeking access to diverse credit solutions for significant life purchases and daily financial management.

- The consumer credit market is poised for substantial growth, driven by digital transformation and evolving consumer financial needs.

- Technological advancements, particularly in AI and data analytics, are key enablers of this growth, improving efficiency and accessibility.

- Emerging markets present significant untapped potential for credit expansion.

- Regulatory frameworks are adapting to ensure consumer protection and market stability amid rapid innovation.

- Personalization and embedded finance are critical for competitive differentiation and consumer engagement.

Consumer Credit Market Drivers Analysis

The consumer credit market is propelled by a confluence of macroeconomic, technological, and behavioral factors that collectively enhance demand and expand the reach of credit products. A primary driver is the increasing disposable income across various global regions, empowering consumers to seek financing for larger purchases such as homes, vehicles, and education, as well as for daily expenses. This economic uplift, particularly in emerging economies, fosters a growing consumer base with aspirations for improved living standards, directly translating into higher demand for credit.

Furthermore, rapid digitalization and the widespread adoption of smartphones have revolutionized how consumers interact with financial services. The ease of applying for loans online, coupled with faster approval processes facilitated by fintech innovations, significantly reduces friction in accessing credit. The expansion of e-commerce and the emergence of innovative payment solutions like Buy Now, Pay Later (BNPL) schemes also contribute significantly, integrating credit seamlessly into the consumer purchasing journey and driving transactional volume.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Disposable Income | +1.2% | Asia Pacific, Latin America, Middle East | Medium to Long-term (2025-2033) |

| Digital Transformation & Fintech Innovation | +1.5% | Global, particularly North America, Europe, APAC | Short to Long-term (2025-2033) |

| Expansion of E-commerce and Online Retail | +0.9% | Global | Short to Medium-term (2025-2029) |

| Growing Demand for Personalized Credit Products | +0.8% | North America, Europe, Developed APAC | Medium-term (2027-2033) |

| Government Initiatives for Financial Inclusion | +0.7% | Emerging Markets (India, Indonesia, Brazil) | Long-term (2028-2033) |

Consumer Credit Market Restraints Analysis

Despite robust growth prospects, the consumer credit market faces several significant restraints that could temper its expansion. Regulatory scrutiny and evolving compliance requirements pose a considerable challenge, as governments worldwide implement stricter lending guidelines to protect consumers and prevent financial instability. These regulations, often varying by region and product type, increase operational costs for lenders and can limit the scope of their offerings, potentially slowing down market innovation and expansion.

Economic volatility, characterized by fluctuating interest rates, inflation, and unemployment levels, also serves as a major restraint. During periods of economic downturn, consumer confidence wanes, leading to reduced demand for new credit and an increase in loan defaults. High household debt levels in certain developed economies can further restrict growth, as consumers become less willing or able to take on additional financial obligations. Furthermore, cybersecurity risks and data breaches continue to be a concern, eroding consumer trust in digital lending platforms and potentially leading to stricter data protection laws.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stricter Regulatory Compliance & Scrutiny | -0.7% | Global, particularly Europe, North America | Short to Medium-term (2025-2029) |

| Economic Downturns & Interest Rate Volatility | -1.0% | Global, varies by economic cycle | Short-term (2025-2027) |

| High Household Debt Levels in Developed Nations | -0.5% | North America, Western Europe | Medium to Long-term (2027-2033) |

| Data Privacy Concerns & Cybersecurity Risks | -0.6% | Global | Short to Medium-term (2025-2030) |

| Increased Competition from Non-traditional Lenders | -0.4% | Global | Medium-term (2026-2031) |

Consumer Credit Market Opportunities Analysis

Significant opportunities abound in the consumer credit market, primarily stemming from the vast untapped potential in emerging economies and the continuous innovation in product development. Regions like Asia Pacific, Latin America, and Africa possess large populations with nascent or underserved credit markets, presenting immense scope for growth as financial literacy improves and digital infrastructure expands. Tailoring credit products to the specific needs and income patterns of these diverse populations represents a substantial opportunity for market players seeking expansion beyond saturated mature markets.

Technological advancements, particularly in artificial intelligence, blockchain, and big data analytics, create avenues for developing more inclusive and efficient credit models. The application of alternative data sources for credit scoring, for instance, allows lenders to assess the creditworthiness of individuals without traditional credit histories, unlocking new customer segments. Furthermore, the burgeoning demand for embedded finance solutions, where credit services are seamlessly integrated into retail, e-commerce, and lifestyle platforms, offers a strategic pathway for lenders to reach consumers at their point of need, enhancing convenience and driving adoption. The growing focus on ESG (Environmental, Social, and Governance) factors also presents opportunities for developing sustainable and socially responsible credit products, appealing to a new generation of conscious consumers.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Untapped Markets in Emerging Economies | +1.3% | Asia Pacific, Latin America, Africa | Medium to Long-term (2026-2033) |

| Development of Niche & Personalized Credit Products | +1.1% | Global | Short to Long-term (2025-2033) |

| Expansion of Embedded Finance & BNPL Models | +1.0% | Global | Short to Medium-term (2025-2030) |

| Leveraging Alternative Data for Credit Scoring | +0.9% | Global, particularly in emerging markets | Medium-term (2027-2032) |

| Partnerships between Traditional Banks & Fintechs | +0.8% | Global | Short to Medium-term (2025-2029) |

Consumer Credit Market Challenges Impact Analysis

The consumer credit market faces a spectrum of challenges that necessitate strategic responses from market participants. One significant hurdle is the escalating competition from a diverse array of financial technology firms, challenger banks, and even non-financial entities entering the lending space. This intensified competition often leads to pricing pressures, shrinking profit margins, and the need for continuous innovation to differentiate offerings, placing a burden on traditional lenders to modernize their infrastructure and customer experience rapidly.

Navigating the complex and fragmented regulatory landscape across different jurisdictions is another substantial challenge. Compliance with varying data privacy laws, consumer protection acts, and anti-money laundering (AML) regulations requires significant investment in legal expertise and technological solutions. Moreover, the risk of credit defaults and non-performing loans (NPLs) remains a perpetual concern, particularly during economic downturns or periods of high inflation. Lenders must implement sophisticated risk management frameworks and robust collections strategies to mitigate these financial exposures, which can otherwise severely impact profitability and capital adequacy. Addressing consumer financial literacy and ensuring responsible lending practices are also ongoing challenges that require industry-wide collaboration and educational initiatives.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intensifying Competition from Fintechs | -0.8% | Global | Short to Medium-term (2025-2030) |

| Managing Credit Risk & Potential Defaults | -1.1% | Global, particularly volatile economies | Short-term (2025-2027) |

| Complex & Evolving Regulatory Environment | -0.9% | Global | Short to Long-term (2025-2033) |

| Maintaining Data Security & Preventing Fraud | -0.7% | Global | Short to Medium-term (2025-2029) |

| Ensuring Financial Inclusion & Responsible Lending | -0.6% | Global | Long-term (2028-2033) |

Consumer Credit Market - Updated Report Scope

This report provides a comprehensive analysis of the consumer credit market, encompassing its historical performance, current dynamics, and future projections. The scope includes detailed segmentation by product type, lender type, end-use, and application, alongside a thorough regional and country-level assessment. It highlights key trends, identifies growth drivers, restraints, opportunities, and challenges, and evaluates the competitive landscape with profiles of leading market participants. The report also incorporates an in-depth analysis of the impact of artificial intelligence on the market, offering strategic insights for stakeholders.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 15.7 Trillion |

| Market Forecast in 2033 | USD 26.8 Trillion |

| Growth Rate | 6.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Financial Services Provider A, Leading Fintech Innovator B, Digital Lending Platform C, Traditional Banking Group D, Regional Credit Union E, Online Loan Facilitator F, Payment Solutions Provider G, Emerging Market Lender H, Tech-Enabled Credit Solutions I, Consumer Finance Specialist J, Diversified Financial Conglomerate K, Mobile-First Lending Company L, Auto Finance Giant M, Mortgage & Loan Services N, Microfinance & Inclusive Credit Provider O |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The consumer credit market is meticulously segmented to provide a granular understanding of its diverse components and drivers. This segmentation allows for targeted analysis of consumer behavior, lender strategies, and regional nuances across various credit products and delivery channels. Understanding these segments is crucial for identifying specific growth opportunities and tailoring business strategies to meet the evolving demands of different consumer groups and market ecosystems.

- By Product Type: This segment includes Credit Cards, Personal Loans, Mortgages, Auto Loans, Student Loans, Point-of-Sale Loans (BNPL), and Other specialized credit instruments.

- By Lender Type: Categories here cover traditional financial institutions such as Banks and Credit Unions, alongside emerging players like Non-Banking Financial Companies (NBFCs), Fintech Companies, and Online Lenders.

- By End-Use: This segmentation analyzes credit extended for specific purposes, including Housing, Vehicles, Education, Consumer Durables, Travel, Healthcare, and various Other personal expenditures.

- By Application: Differentiates between credit accessed through Online platforms (digital applications, mobile apps) and Offline channels (branch visits, direct sales agents).

Regional Highlights

- North America: This region represents a mature and highly developed consumer credit market, characterized by significant technological adoption and a robust regulatory framework. The U.S. and Canada lead in digital lending innovation, personalized credit products, and the widespread use of credit cards and mortgages. Growth here is driven by fintech partnerships, advanced data analytics, and a consumer base accustomed to diverse credit options, although high household debt levels remain a concern.

- Europe: The European consumer credit market is diverse, with strong variations across countries in terms of regulatory environments and consumer behavior. Western European countries are technologically advanced with high penetration of credit products, while Central and Eastern Europe offer growth opportunities as economies mature. The region is focusing on open banking initiatives, sustainable finance, and regulatory harmonization, striving for greater transparency and consumer protection.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing region in the consumer credit market, fueled by large populations, increasing disposable incomes, rapid urbanization, and significant digital adoption. Countries like China, India, Indonesia, and Vietnam are experiencing exponential growth in mobile-first lending, BNPL solutions, and innovative digital payment ecosystems. Untapped rural markets and a growing middle class present immense opportunities for credit expansion, alongside challenges related to financial literacy and regulatory oversight.

- Latin America: This region presents a dynamic consumer credit landscape with substantial growth potential, driven by efforts towards financial inclusion and increasing smartphone penetration. Brazil, Mexico, and Argentina are key markets witnessing the rise of digital lenders and alternative credit scoring models to serve previously unbanked or underbanked populations. The market is characterized by a blend of traditional banking services and burgeoning fintech innovation, though economic volatility can pose challenges.

- Middle East and Africa (MEA): The MEA region is an emerging market for consumer credit, with varying degrees of development across countries. The GCC states (e.g., UAE, Saudi Arabia) have relatively sophisticated markets, while Sub-Saharan Africa is characterized by rapid digital transformation, mobile money adoption, and a strong drive for financial inclusion. Opportunities lie in microfinance, mobile lending platforms, and providing credit access to a young, tech-savvy population, though regulatory frameworks and political stability are critical considerations.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Consumer Credit Market.- Global Financial Services Provider A

- Leading Fintech Innovator B

- Digital Lending Platform C

- Traditional Banking Group D

- Regional Credit Union E

- Online Loan Facilitator F

- Payment Solutions Provider G

- Emerging Market Lender H

- Tech-Enabled Credit Solutions I

- Consumer Finance Specialist J

- Diversified Financial Conglomerate K

- Mobile-First Lending Company L

- Auto Finance Giant M

- Mortgage & Loan Services N

- Microfinance & Inclusive Credit Provider O

Frequently Asked Questions

What is consumer credit?

Consumer credit refers to personal debt incurred by individuals for household, family, or personal purposes. It typically includes loans, credit cards, and other forms of financing used for purchasing goods and services, excluding mortgage loans.

How is the consumer credit market projected to grow?

The consumer credit market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033, reaching an estimated USD 26.8 trillion by 2033, driven by digitalization and increased consumer spending.

What are the key trends shaping the consumer credit market?

Key trends include the rapid digitalization of lending, the rise of Buy Now, Pay Later (BNPL) services, increasing demand for personalized credit products, the use of alternative data for credit scoring, and the growth of embedded finance solutions.

What is the impact of AI on consumer credit?

AI significantly impacts consumer credit by enhancing risk assessment, automating loan processing, improving fraud detection, and enabling highly personalized product offerings, leading to more efficient and accessible credit solutions.

Which regions offer the most significant growth opportunities?

Asia Pacific (APAC) and Latin America present the most significant growth opportunities due to their large unbanked populations, increasing disposable incomes, and rapid digital transformation, leading to expanded access to various credit products.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted