Consumer Electronic Store Market

Consumer Electronic Store Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705261 | Last Updated : August 11, 2025 |

Format : ![]()

![]()

![]()

![]()

Consumer Electronic Store Market Size

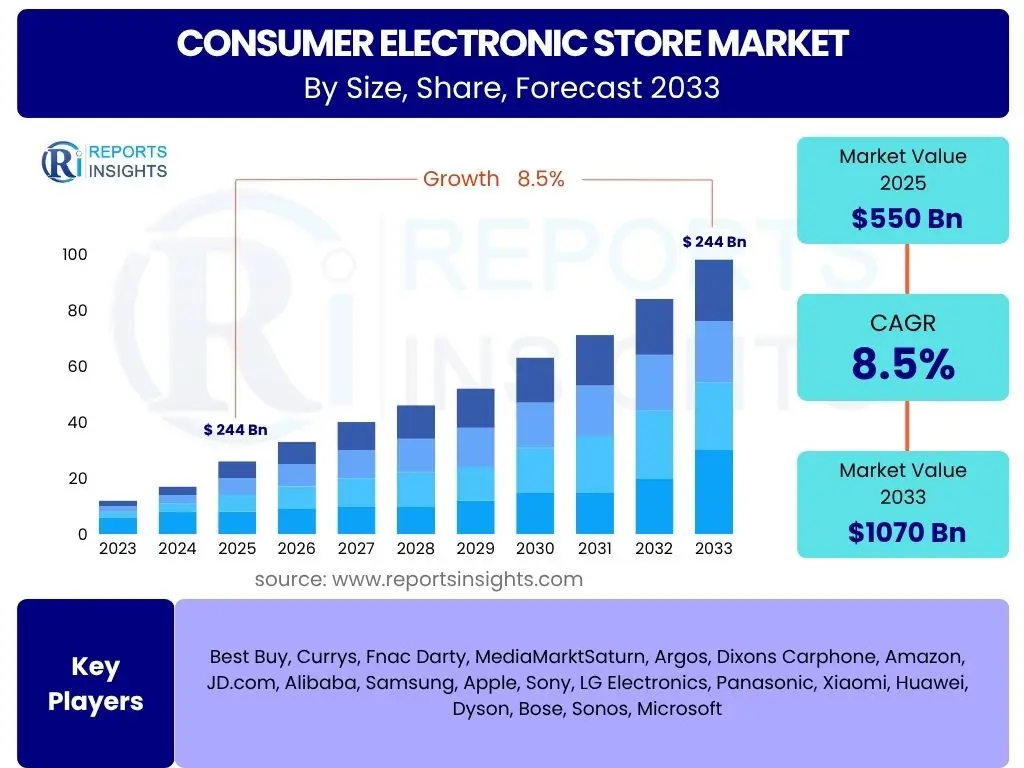

According to Reports Insights Consulting Pvt Ltd, The Consumer Electronic Store Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2025 and 2033. The market is estimated at USD 550 Billion in 2025 and is projected to reach USD 1070 Billion by the end of the forecast period in 2033.

Key Consumer Electronic Store Market Trends & Insights

The consumer electronic store market is undergoing a significant transformation, driven by evolving consumer behaviors, rapid technological advancements, and the increasing integration of digital technologies into daily life. Common user inquiries often center on how physical retail adapts to the dominance of e-commerce, the impact of smart home ecosystems, and the growing demand for personalized shopping experiences. The market is witnessing a shift towards experiential retail, where stores are designed to offer immersive product demonstrations and hands-on interactions, moving beyond mere transactional spaces. This strategy aims to differentiate brick-and-mortar stores from online competitors by leveraging the unique advantages of physical presence.

Furthermore, sustainability and ethical sourcing are becoming increasingly important for consumers, prompting electronic retailers to focus on eco-friendly products, recycling programs, and transparent supply chains. There is also a notable trend towards subscription-based models for certain electronics or services, offering convenience and affordability. Omnichannel retail, seamlessly blending online and offline shopping experiences, remains a critical focus, allowing customers to research online, purchase in-store, or vice versa. The integration of artificial intelligence and data analytics is also paramount, enabling stores to offer highly customized recommendations and optimize inventory management, directly addressing user interest in how technology enhances the shopping journey and operational efficiency.

- Shift towards Experiential Retail: Focus on in-store demonstrations and immersive experiences.

- Growth of Omnichannel Strategies: Seamless integration of online and offline shopping channels.

- Increased Demand for Smart Home Devices: Expansion of connected ecosystems and IoT products.

- Sustainability and Circular Economy Focus: Emphasis on eco-friendly products and recycling.

- Personalization through Data Analytics: Tailored recommendations and promotions based on customer data.

- Rise of Subscription Models: Offering electronics or services on a recurring payment basis.

- Integration of In-store Technology: Use of AR/VR, interactive displays, and self-checkout.

AI Impact Analysis on Consumer Electronic Store

User questions frequently revolve around the transformative potential of Artificial Intelligence (AI) within the consumer electronic store sector, particularly concerning its ability to personalize the customer journey and streamline operational efficiencies. Consumers are increasingly curious about how AI-powered recommendations can enhance their product discovery, while retailers are exploring AI's role in optimizing inventory management and supply chain logistics. The application of AI in customer service, through advanced chatbots and virtual assistants, is also a key area of interest, promising quicker and more accurate responses to inquiries, thereby improving the overall customer experience. This allows human staff to focus on more complex, high-value interactions, addressing a common concern about balancing technological integration with human touchpoints.

Moreover, AI is anticipated to revolutionize in-store analytics, providing retailers with real-time insights into customer traffic patterns, product engagement, and purchasing behaviors. This data-driven approach enables dynamic store layouts, targeted promotions, and optimized staffing levels, contributing to enhanced profitability. The long-term impact extends to predictive maintenance for store equipment and advanced fraud detection systems, safeguarding assets and ensuring operational continuity. While there are expectations for increased efficiency and improved customer satisfaction, users also express concerns about data privacy and the potential for job displacement, highlighting the need for ethical AI deployment and workforce upskilling within the retail environment.

- Personalized Customer Recommendations: AI algorithms analyze browsing and purchase history to suggest relevant products.

- Optimized Inventory Management: Predictive AI models forecast demand, reducing overstocking and stockouts.

- Enhanced Customer Service: AI-powered chatbots and virtual assistants provide instant support and FAQs.

- In-Store Analytics and Insights: AI vision systems track customer movement and product interaction for layout optimization.

- Supply Chain Optimization: AI predicts disruptions and optimizes logistics for timely product availability.

- Automated Pricing and Promotions: Dynamic pricing strategies based on competitor data and demand fluctuations.

- Virtual Try-On and Augmented Reality (AR) Experiences: AI-driven AR tools enhance product visualization before purchase.

Key Takeaways Consumer Electronic Store Market Size & Forecast

Common user questions regarding the consumer electronic store market size and forecast consistently point towards an eagerness to understand the trajectory of retail in the digital age, particularly the resilience of physical stores amidst e-commerce expansion. The primary takeaway is the market's robust growth, largely fueled by persistent innovation in consumer electronics, rising disposable incomes in emerging economies, and the increasing adoption of smart and connected devices. Despite the pervasive influence of online retail, physical stores are projected to maintain a significant presence by evolving into experiential hubs, focusing on personalized service and immediate product gratification, which online channels cannot fully replicate. This dual-channel approach, or omnichannel strategy, is critical for sustained market performance.

The forecast period from 2025 to 2033 indicates a substantial expansion, with market values nearly doubling. This growth is not uniform across all segments or regions, underscoring the importance of targeted strategies for retailers. Key drivers such as technological advancements (e.g., 5G, IoT, AI), expanding product portfolios, and a consumer shift towards premium and sustainable electronics will underpin this growth. Retailers that strategically invest in technology, integrate diverse sales channels, and prioritize customer experience are best positioned to capture market share. The data suggests a dynamic and evolving landscape where adaptability and innovation are paramount for success, addressing user inquiries about future market viability and competitive positioning.

- Significant Market Expansion: Projected doubling of market value from 2025 to 2033.

- Resilience of Physical Stores: Evolution into experiential and service-oriented hubs.

- Omnichannel Imperative: Seamless integration of online and offline customer journeys.

- Innovation as a Growth Engine: Continuous introduction of new technologies and products.

- Regional Growth Disparities: APAC and emerging markets contributing significantly to expansion.

- Consumer Demand for Smart Devices: Driving sales of connected home, health, and personal electronics.

- Focus on Customer Experience: Key differentiator for market leaders amidst increasing competition.

Consumer Electronic Store Market Drivers Analysis

The consumer electronic store market is primarily driven by a confluence of factors that stimulate consumer demand and expand retail accessibility. Rapid technological advancements, such as the proliferation of 5G, IoT, and AI-enabled devices, consistently introduce new product categories and upgrade cycles, compelling consumers to purchase the latest innovations. Alongside this, rising disposable incomes, particularly in developing economies, enable greater discretionary spending on electronic gadgets and home appliances. The increasing urbanization and adoption of digital lifestyles globally further fuel the demand for smart, connected devices that enhance convenience and entertainment, pushing the boundaries of traditional retail offerings.

Furthermore, the expanding e-commerce infrastructure has not only created new sales channels but also spurred brick-and-mortar stores to innovate, improving their in-store experience and omnichannel capabilities. This competitive environment encourages constant improvement and investment in retail technology. The growing consumer preference for interconnected ecosystems, from smart homes to wearable tech, also plays a crucial role, as consumers seek integrated solutions, often best explored and purchased in specialized electronic stores that can offer comprehensive advice and demonstrations. These combined drivers create a fertile ground for sustained market growth and evolution.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Technological Advancements (5G, IoT, AI) | +2.5% | Global, particularly North America, APAC, Europe | Short to Mid-Term (2025-2030) |

| Rising Disposable Incomes | +1.8% | APAC, Latin America, Middle East & Africa | Mid to Long-Term (2026-2033) |

| Increasing Adoption of Smart Devices | +2.0% | Global | Short to Mid-Term (2025-2029) |

| Urbanization and Digital Lifestyles | +1.2% | APAC, Latin America, Africa | Mid to Long-Term (2027-2033) |

| Growth of E-commerce and Omnichannel Retail | +1.0% | Global | Short to Long-Term (2025-2033) |

Consumer Electronic Store Market Restraints Analysis

The consumer electronic store market faces several significant restraints that can impede its growth trajectory. Economic downturns and inflationary pressures directly impact consumer discretionary spending, leading to reduced purchases of non-essential electronic goods. Supply chain disruptions, often exacerbated by geopolitical tensions or unforeseen global events, can result in product shortages and increased operational costs, severely affecting inventory availability and pricing. Intense competition from online retailers and direct-to-consumer brands also puts immense pressure on profit margins for traditional brick-and-mortar stores, forcing them to constantly innovate and differentiate their offerings.

Furthermore, the inherent price sensitivity of consumers, especially for mature product categories, makes it challenging for retailers to maintain healthy margins without resorting to frequent discounts. Regulatory challenges, including import tariffs, environmental regulations, and data privacy laws, add layers of complexity and cost to operations. The rapid pace of technological obsolescence means that electronic products have shorter lifecycles, requiring constant inventory refresh and posing risks of dead stock for retailers. These combined factors necessitate agile strategies and robust risk management for market participants.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Economic Volatility and Inflation | -1.5% | Global, particularly developed economies | Short-Term (2025-2027) |

| Supply Chain Disruptions | -1.0% | Global, affects specific product categories | Short to Mid-Term (2025-2028) |

| Intense Price Competition from Online Retailers | -1.2% | Global | Long-Term (2025-2033) |

| Short Product Lifecycles/Technological Obsolescence | -0.8% | Global | Long-Term (2025-2033) |

| Data Privacy and Security Concerns | -0.5% | Europe, North America | Mid to Long-Term (2026-2033) |

Consumer Electronic Store Market Opportunities Analysis

Significant opportunities abound for growth and innovation within the consumer electronic store market, particularly through strategic adaptation to evolving consumer demands and technological advancements. The expansion into emerging markets, where digital penetration and disposable incomes are rapidly increasing, presents a substantial untapped customer base for electronic goods. Furthermore, the increasing consumer demand for personalized shopping experiences, enabled by AI and data analytics, offers retailers a chance to differentiate themselves by providing highly tailored product recommendations and customized services, moving beyond generic sales interactions to create unique customer journeys.

The continued growth of the smart home ecosystem, alongside other connected devices like wearables and health tech, represents a burgeoning product category with high growth potential, allowing stores to position themselves as holistic solution providers. Embracing circular economy principles through the sale of refurbished electronics, offering trade-in programs, and providing repair services also taps into growing consumer consciousness about sustainability and offers new revenue streams. Moreover, the integration of augmented reality (AR) and virtual reality (VR) technologies in-store can provide immersive product demonstrations, enhancing the experiential aspect of shopping and attracting tech-savvy consumers, thereby creating a distinct competitive advantage for forward-thinking retailers.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into Emerging Markets | +2.2% | APAC, Latin America, Middle East & Africa | Long-Term (2027-2033) |

| Personalized Shopping Experiences | +1.7% | Global | Mid to Long-Term (2026-2033) |

| Growth of Smart Home & IoT Ecosystems | +1.9% | Global | Short to Mid-Term (2025-2030) |

| Sustainable & Refurbished Electronics Sales | +1.5% | North America, Europe | Mid to Long-Term (2026-2033) |

| Integration of AR/VR for Experiential Retail | +1.0% | North America, Europe, parts of APAC | Mid-Term (2027-2031) |

Consumer Electronic Store Market Challenges Impact Analysis

The consumer electronic store market grapples with several formidable challenges that necessitate strategic agility and continuous innovation for sustained success. Managing the complexity of inventory across a vast array of constantly evolving electronic products, each with its own sales cycle and component requirements, is a significant operational hurdle. This is compounded by the rapid pace of technological obsolescence, which can lead to rapid depreciation of stock value if not managed efficiently. Furthermore, evolving consumer expectations, particularly the demand for instant gratification, seamless omnichannel experiences, and competitive pricing, put immense pressure on traditional retail models to adapt quickly and effectively, often requiring substantial investment in technology and infrastructure.

Cybersecurity threats, ranging from data breaches to point-of-sale system vulnerabilities, pose a constant risk, potentially eroding consumer trust and incurring significant financial penalties. The intense competition, not just from direct rivals but also from online giants and niche players, compresses profit margins and requires retailers to constantly differentiate their value proposition. Attracting and retaining skilled talent capable of understanding complex electronics and providing expert customer service is another critical challenge, particularly as product sophistication increases. Navigating these multifaceted challenges requires a proactive approach to technology adoption, robust operational management, and a deep understanding of dynamic consumer preferences.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Managing Inventory Complexity & Obsolescence | -1.3% | Global | Long-Term (2025-2033) |

| Evolving Consumer Expectations (Omnichannel, Speed) | -1.0% | Global | Long-Term (2025-2033) |

| Cybersecurity Threats & Data Privacy Compliance | -0.7% | Global, particularly regulated regions | Long-Term (2025-2033) |

| Intense Competition and Profitability Pressures | -1.1% | Global | Long-Term (2025-2033) |

| Talent Acquisition and Retention for Specialized Roles | -0.6% | Developed Economies | Mid to Long-Term (2026-2033) |

Consumer Electronic Store Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the Consumer Electronic Store Market, offering a detailed understanding of its current landscape, historical performance, and future growth projections. It covers market size estimations, growth drivers, restraints, opportunities, and challenges, providing a holistic view for strategic decision-making. The report segments the market extensively by product type, distribution channel, and application, alongside a thorough regional analysis. Key market trends, the impact of AI, and competitive insights into leading players are also included to offer actionable intelligence for stakeholders. This updated scope aims to address the dynamic nature of the consumer electronics retail sector, providing timely and relevant data for businesses looking to navigate its complexities and capitalize on emerging trends.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 550 Billion |

| Market Forecast in 2033 | USD 1070 Billion |

| Growth Rate | 8.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Best Buy, Currys, Fnac Darty, MediaMarktSaturn, Argos, Dixons Carphone, Amazon, JD.com, Alibaba, Samsung, Apple, Sony, LG Electronics, Panasonic, Xiaomi, Huawei, Dyson, Bose, Sonos, Microsoft |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Consumer Electronic Store Market is comprehensively segmented to provide granular insights into its diverse components, reflecting the varied product categories, purchasing behaviors, and end-use applications. This segmentation allows for a detailed analysis of market dynamics within each specific sub-segment, aiding stakeholders in identifying high-growth areas and tailoring their strategies accordingly. The market is primarily broken down by product type, which includes a wide array of devices from personal electronics like smartphones and laptops to major home appliances and specialized gadgets. This categorization helps understand which product categories are driving growth and where consumer demand is concentrated.

Further segmentation by distribution channel distinguishes between traditional brick-and-mortar stores, rapidly expanding online retail platforms (including brand-specific websites and major e-commerce marketplaces), and other retail formats such as hypermarkets and specialty stores. This provides insights into consumer preferences regarding purchasing avenues and the competitive landscape across different retail environments. Finally, segmentation by application categorizes sales based on whether products are intended for residential, commercial, or institutional use, highlighting the different market drivers and purchasing cycles inherent in each segment. This multi-faceted segmentation ensures a robust and nuanced understanding of the market structure and its underlying growth engines.

- By Product:

- Smartphones

- Laptops & Desktops

- Televisions

- Home Appliances

- Refrigerators

- Washing Machines

- Microwaves

- Air Conditioners

- Dishwashers

- Vacuum Cleaners

- Audio Devices

- Headphones

- Speakers

- Soundbars

- Wearable Devices

- Smartwatches

- Fitness Trackers

- Gaming Consoles

- Cameras & Photography Equipment

- Drones

- Others (Printers, Routers, Storage Devices, etc.)

- By Distribution Channel:

- Brick-and-Mortar Stores

- Online Retail Stores

- Company-owned Websites

- E-commerce Marketplaces

- Hypermarkets & Supermarkets

- Specialty Electronic Stores

- Department Stores

- By Application:

- Residential

- Commercial

- Institutional

Regional Highlights

- North America: This region represents a mature yet highly innovative market, characterized by high disposable incomes, early adoption of advanced technologies (such as 5G and smart home devices), and a strong presence of established electronic retailers and e-commerce giants. Consumer preferences lean towards premium products and integrated smart ecosystems, driving growth in categories like smart appliances, wearables, and high-definition entertainment systems.

- Europe: The European market is diverse, with varying consumer preferences and regulatory landscapes across countries. Western Europe demonstrates high adoption rates of smart devices and a growing emphasis on sustainability and energy efficiency in electronic products. Eastern Europe and emerging economies within the region are witnessing increasing penetration rates as disposable incomes rise, leading to a surge in demand for affordable yet feature-rich electronics.

- Asia Pacific (APAC): APAC is the fastest-growing region in the consumer electronic store market, fueled by large populations, rapid urbanization, increasing disposable incomes, and a booming middle class. Countries like China, India, Japan, South Korea, and Southeast Asian nations are key growth engines. The region exhibits high adoption of smartphones and smart consumer electronics, driven by digital transformation initiatives and a strong appetite for technological innovation.

- Latin America: This region is experiencing steady growth, driven by increasing internet penetration, rising disposable incomes, and a growing consumer interest in connected devices. Key markets such as Brazil, Mexico, and Argentina are seeing expansion in both online and offline retail channels, with a particular demand for affordable smartphones, personal computing devices, and entertainment electronics.

- Middle East and Africa (MEA): The MEA market is an emerging region with significant growth potential, particularly in urban centers. Increasing government investments in digital infrastructure, a young population, and rising disposable incomes are contributing to the demand for consumer electronics. Countries in the GCC region (e.g., UAE, Saudi Arabia) lead in adoption of premium and smart devices, while African countries are seeing a rise in demand for basic and mid-range electronics.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Consumer Electronic Store Market.- Best Buy

- Currys

- Fnac Darty

- MediaMarktSaturn

- Argos

- Dixons Carphone

- Amazon

- JD.com

- Alibaba

- Samsung

- Apple

- Sony

- LG Electronics

- Panasonic

- Xiaomi

- Huawei

- Dyson

- Bose

- Sonos

- Microsoft

Frequently Asked Questions

Analyze common user questions about the Consumer Electronic Store market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the projected growth of the Consumer Electronic Store Market?

The Consumer Electronic Store Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2025 and 2033, reaching an estimated USD 1070 Billion by 2033 from USD 550 Billion in 2025.

How is AI impacting the Consumer Electronic Store Market?

AI is significantly impacting the market by enabling personalized customer recommendations, optimizing inventory and supply chain management, enhancing customer service through chatbots, and providing advanced in-store analytics for improved operational efficiency.

What are the primary drivers of growth in the Consumer Electronic Store Market?

Key drivers include rapid technological advancements (5G, IoT, AI), rising disposable incomes, increasing adoption of smart devices, ongoing urbanization, and the continuous evolution of omnichannel retail strategies.

What are the main challenges faced by Consumer Electronic Stores?

Major challenges include managing complex inventory with rapid obsolescence, adapting to evolving consumer expectations for seamless experiences, mitigating cybersecurity threats, navigating intense competition, and attracting skilled talent.

Which regions are key contributors to the Consumer Electronic Store Market?

North America and Europe are mature markets leading in premium tech adoption, while Asia Pacific (APAC) is the fastest-growing region due to rising disposable incomes and high technology adoption. Latin America, Middle East, and Africa (MEA) are emerging markets with substantial growth potential.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted