Construction Adhesive and Sealant Market

Construction Adhesive and Sealant Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703985 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

Construction Adhesive and Sealant Market Size

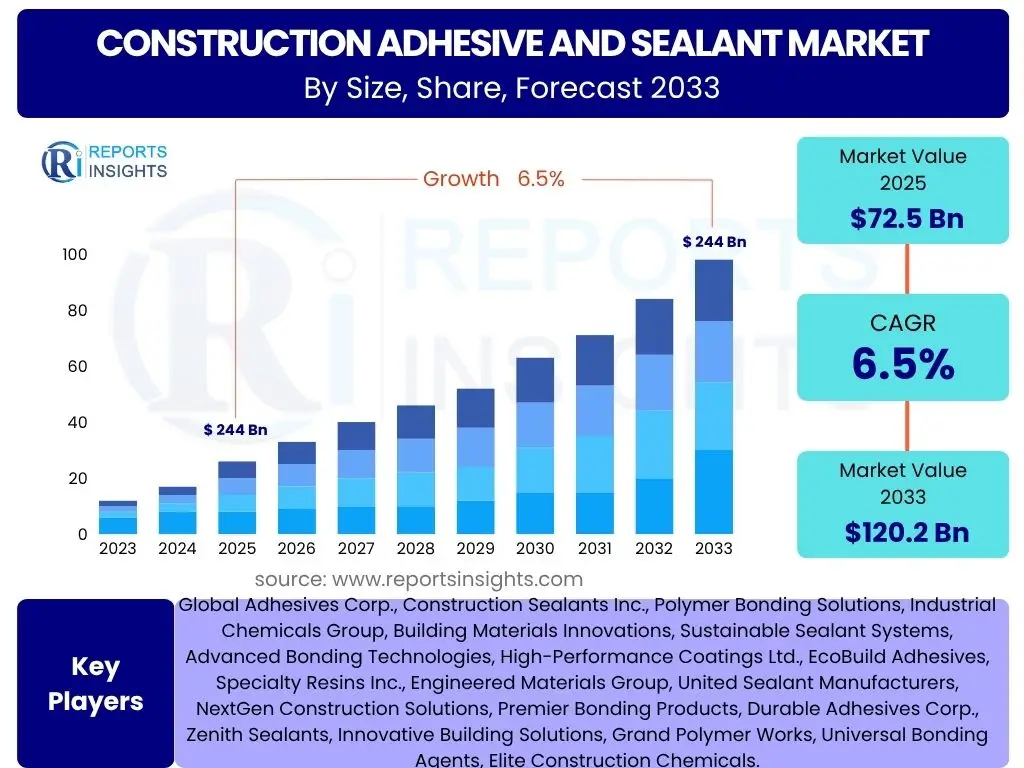

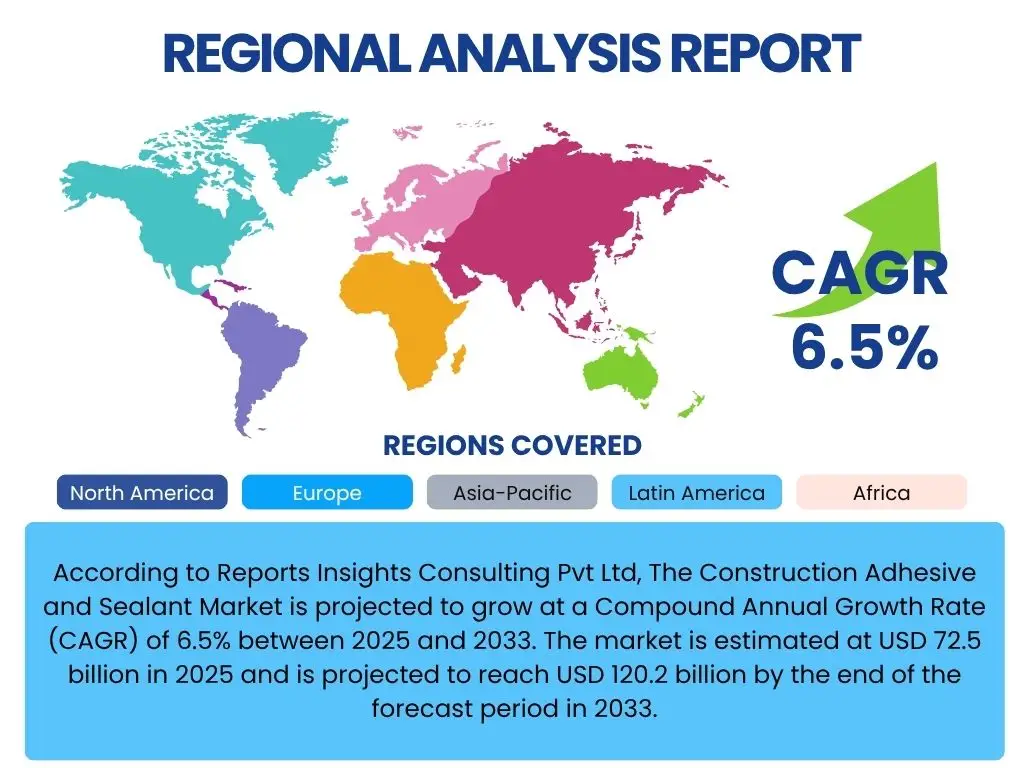

According to Reports Insights Consulting Pvt Ltd, The Construction Adhesive and Sealant Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2025 and 2033. The market is estimated at USD 72.5 billion in 2025 and is projected to reach USD 120.2 billion by the end of the forecast period in 2033.

Key Construction Adhesive and Sealant Market Trends & Insights

User inquiries frequently center on the evolving landscape of construction materials and methodologies, seeking to understand the pivotal shifts impacting adhesive and sealant demand. A predominant theme is the increasing emphasis on sustainable and eco-friendly building practices, which drives innovation towards bio-based, low-VOC (Volatile Organic Compound), and energy-efficient adhesive and sealant solutions. This trend is not merely a regulatory compliance measure but a fundamental shift in consumer and developer preference, aiming to reduce environmental footprints throughout a building's lifecycle. Another significant area of interest revolves around the adoption of advanced material science, specifically concerning high-performance polymers and smart materials that offer enhanced durability, flexibility, and application efficiency, crucial for modern construction techniques like modular and prefabrication.

Furthermore, discussions highlight the impact of urbanization and the concomitant surge in infrastructure development projects across emerging economies. This creates a robust demand for high-strength, weather-resistant, and rapidly curing adhesives and sealants that can withstand diverse climatic conditions and structural stresses. The construction industry is also witnessing a gradual shift towards automation and industrialized building processes, necessitating adhesives and sealants that are compatible with robotic application systems and offer consistent performance in controlled environments. These trends collectively underscore a market moving towards greater specialization, sustainability, and technological integration to meet the complex demands of contemporary construction.

The market also shows a growing demand for multi-functional products that can serve various purposes, such as sealing, bonding, and insulating simultaneously, thereby streamlining construction processes and reducing labor costs. This integration of functionalities is particularly appealing in fast-paced construction projects where efficiency and speed are paramount. The confluence of these trends indicates a dynamic market driven by innovation, environmental consciousness, and the relentless pursuit of operational excellence within the construction sector.

- Growing adoption of sustainable and low-VOC adhesive and sealant formulations.

- Increasing demand for high-performance and specialty adhesives in modular construction.

- Rapid urbanization and infrastructure development driving market expansion in APAC.

- Technological advancements in product efficacy, durability, and application methods.

- Shift towards multi-functional products for streamlined construction processes.

- Integration of smart features for enhanced performance monitoring and longevity.

AI Impact Analysis on Construction Adhesive and Sealant

User queries regarding the impact of Artificial Intelligence (AI) on the construction adhesive and sealant market primarily revolve around predictive capabilities, process optimization, and material innovation. Stakeholders are keen to understand how AI can enhance the quality control of adhesive and sealant manufacturing, predict material performance under various environmental conditions, and optimize supply chain logistics to ensure timely delivery and reduce waste. The potential for AI-driven analytics to identify optimal formulations based on specific project requirements, considering factors like substrate type, climate, and structural load, is a key area of interest, promising to minimize material failure and improve overall structural integrity. This suggests a future where material selection is data-driven, precise, and highly customized.

Concerns and expectations also extend to the automation of adhesive and sealant application processes on construction sites. Users anticipate AI-powered robotics or drones equipped with vision systems could significantly improve the precision, speed, and safety of applying these materials, especially in hard-to-reach or hazardous areas. This automation would not only mitigate labor shortages but also ensure consistent application quality, reducing human error and material consumption. Furthermore, there is an expectation that AI could facilitate the development of novel adhesive and sealant materials by rapidly analyzing vast datasets of chemical compositions and their potential properties, accelerating the research and development cycle for next-generation products with superior characteristics.

The overarching theme in user inquiries is the desire for AI to bring greater efficiency, predictability, and innovation to a traditionally labor-intensive and experience-driven sector. From improving the material life cycle through predictive maintenance algorithms to streamlining on-site operations and fostering groundbreaking material science, AI's potential is seen as a transformative force. Users envision a future where AI not only optimizes existing processes but also unlocks entirely new possibilities for how construction adhesives and sealants are designed, manufactured, and utilized, leading to more resilient, sustainable, and cost-effective construction outcomes.

- AI-driven optimization of adhesive and sealant formulation for enhanced performance.

- Predictive analytics for material degradation and maintenance scheduling.

- Automation and robotic application of adhesives and sealants on construction sites.

- Supply chain optimization and inventory management through AI algorithms.

- Accelerated R&D for novel materials using AI-powered data analysis.

- Enhanced quality control and defect detection in manufacturing processes.

Key Takeaways Construction Adhesive and Sealant Market Size & Forecast

User questions about key takeaways from the Construction Adhesive and Sealant market size and forecast frequently highlight the primary growth drivers and potential impediments to market expansion. A significant insight derived is that the robust growth projection is largely underpinned by the global surge in both residential and non-residential construction, particularly in developing economies experiencing rapid urbanization and industrialization. The increasing adoption of advanced construction techniques, such as prefabrication and modular building, further contributes to this growth by demanding specialized, high-performance bonding solutions that offer speed and efficiency. This suggests a direct correlation between construction activity levels and the demand for these essential building materials, emphasizing the market's sensitivity to global economic and demographic shifts.

Another crucial takeaway relates to the persistent influence of sustainability trends and stringent environmental regulations. The market forecast consistently points towards a future where demand for low-VOC, eco-friendly, and energy-efficient adhesives and sealants will intensify, compelling manufacturers to invest heavily in green product innovation. This trend is not merely a niche segment but a fundamental shift driving the entire industry towards more environmentally conscious practices, indicating that companies failing to adapt might face competitive disadvantages. Additionally, the forecast reveals a market characterized by continuous product development, with ongoing research into materials offering improved durability, versatility, and ease of application, catering to the evolving needs of modern construction.

In essence, the market's trajectory is defined by a dynamic interplay of macroeconomic factors, technological advancements, and a strong push towards environmental responsibility. While urbanization and infrastructure spending provide the foundational demand, the imperative for sustainable solutions and innovative product performance acts as a powerful catalyst for growth and market evolution. Companies that strategically align with these prevailing trends—investing in green technologies, R&D for advanced materials, and expanding into high-growth regional markets—are best positioned to capitalize on the opportunities presented by this expanding market. Conversely, challenges such as raw material price volatility and supply chain disruptions remain critical factors requiring vigilant management to ensure sustained growth.

- Significant market growth driven by global construction boom, especially in emerging economies.

- Increasing regulatory pressure and consumer demand for sustainable and low-VOC products.

- Technological advancements leading to high-performance, specialized adhesive and sealant solutions.

- Raw material price fluctuations and supply chain vulnerabilities pose ongoing challenges.

- Opportunity for market players through product innovation and strategic regional expansion.

- Residential and non-residential construction remain primary application segments.

Construction Adhesive and Sealant Market Drivers Analysis

The construction adhesive and sealant market is propelled by a confluence of macroeconomic and industry-specific factors. Rapid urbanization, particularly in Asia Pacific and parts of Africa, fuels an unprecedented demand for new residential and commercial infrastructure. This demographic shift necessitates extensive building projects, from housing complexes and office towers to retail centers and transportation networks, all of which heavily rely on adhesives and sealants for structural integrity, finishing, and insulation. Alongside this, government investments in infrastructure development, including roads, bridges, and public utilities, create a substantial and consistent demand for high-performance bonding and sealing solutions that can withstand harsh environmental conditions and significant structural loads.

Technological advancements in construction methodologies, such as the increasing adoption of prefabrication, modular construction, and off-site manufacturing, are also significant drivers. These modern techniques require specialized adhesives and sealants that offer rapid curing times, strong bonds, and compatibility with a diverse range of substrates, enabling faster project completion and reduced on-site labor. Furthermore, the growing global emphasis on green building initiatives and energy efficiency mandates the use of advanced sealants and adhesives that contribute to improved building insulation and reduced energy consumption. This regulatory push, combined with a rising awareness among consumers and developers regarding environmental impact, encourages the shift towards sustainable, low-VOC, and bio-based product formulations, thereby driving innovation and market growth.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Urbanization & Infrastructure Development | +2.1% | Asia Pacific, Latin America, Middle East & Africa | Long-term (2025-2033) |

| Growth in Residential & Commercial Construction | +1.8% | North America, Europe, Asia Pacific | Mid-to-Long term (2025-2033) |

| Increasing Adoption of Green Building Practices | +1.5% | Global, particularly Europe & North America | Mid-to-Long term (2025-2033) |

| Technological Advancements in Construction (e.g., Prefabrication) | +1.1% | North America, Europe, Developed Asia Pacific | Mid-term (2025-2029) |

Construction Adhesive and Sealant Market Restraints Analysis

Despite robust growth drivers, the construction adhesive and sealant market faces several significant restraints that could impede its trajectory. One primary concern is the volatility in raw material prices. Key ingredients such as crude oil derivatives (for polymers), silicone, and various specialty chemicals are subject to global supply chain disruptions, geopolitical tensions, and fluctuations in commodity markets. This instability directly impacts manufacturing costs, leading to unpredictable pricing for end-products, which can deter large-scale construction projects and squeeze profit margins for manufacturers. The reliance on these finite resources also exposes the market to supply shortages and bottlenecks, further complicating production schedules and market stability.

Another substantial restraint is the increasing stringency of environmental regulations concerning VOC emissions and hazardous chemicals. While promoting sustainability, these regulations often necessitate costly research and development efforts to reformulate existing products, increase production expenses, and lengthen time-to-market for new innovations. Compliance with diverse regional and national regulations can be particularly challenging for international manufacturers, requiring different product versions for different markets. Furthermore, the cyclical nature of the construction industry itself poses an inherent restraint; economic downturns, rising interest rates, or credit crises can lead to a slowdown in new construction projects, directly translating to reduced demand for adhesives and sealants. This inherent sensitivity to economic cycles makes long-term planning challenging and can result in periods of reduced investment and slower growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatile Raw Material Prices | -1.2% | Global | Mid-to-Long term (2025-2033) |

| Stringent Environmental Regulations | -0.8% | Europe, North America, Developed Asia Pacific | Long-term (2025-2033) |

| Cyclical Nature of the Construction Industry | -0.7% | Global | Short-to-Mid term (2025-2029) |

| Competition from Traditional Fasteners | -0.5% | Global | Long-term (2025-2033) |

Construction Adhesive and Sealant Market Opportunities Analysis

Significant opportunities are emerging within the construction adhesive and sealant market, driven by evolving industry needs and technological advancements. One key area of growth lies in the increasing demand for specialized and high-performance products tailored for specific applications. As construction projects become more complex, requiring materials that offer enhanced durability, flexibility, and resistance to extreme conditions (e.g., high temperatures, seismic activity, moisture), manufacturers have an opportunity to innovate and develop premium solutions. This includes sealants designed for challenging climates, adhesives for unconventional building materials like composites or advanced alloys, and products with integrated functionalities such as fire resistance or acoustic dampening. The market is increasingly segmenting into niches that value precise performance over generic applicability, creating avenues for product differentiation and higher profit margins.

The burgeoning trend of green building and sustainable construction also presents a substantial opportunity. With growing environmental consciousness and stricter regulations worldwide, there is an escalating demand for eco-friendly adhesives and sealants, including bio-based, water-based, and low-VOC formulations. Companies investing in sustainable R&D and manufacturing processes can gain a significant competitive advantage and capture a larger share of this ethically driven market segment. Furthermore, the vast potential for market expansion in emerging economies, particularly in Asia Pacific, Latin America, and the Middle East, offers immense opportunities. These regions are undergoing rapid urbanization and infrastructure development, leading to a surge in construction activity that outpaces mature markets. Companies that strategically establish local manufacturing facilities, adapt products to regional climate conditions, and build strong distribution networks can tap into these high-growth areas, capitalizing on the immense scale of ongoing and planned projects.

Moreover, the integration of smart technologies and automation in construction offers a pathway for new product development. Opportunities exist for adhesives and sealants compatible with robotic application systems, or those incorporating sensors for real-time performance monitoring. The lifecycle extension of existing structures through renovation, repair, and maintenance activities also provides a consistent demand for adhesives and sealants, independent of new construction cycles. Manufacturers focusing on these aftermarket segments with specialized repair solutions can secure stable revenue streams. The continuous drive towards construction efficiency and reduced labor costs further underscores the potential for pre-applied or easy-to-use adhesive and sealant solutions that minimize on-site complexity and accelerate project timelines.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand for Green & Sustainable Products | +1.5% | Global, Europe, North America, Asia Pacific | Long-term (2025-2033) |

| Expansion in Emerging Economies (Infrastructure & Housing) | +1.8% | Asia Pacific, Latin America, Middle East & Africa | Long-term (2025-2033) |

| Development of High-Performance & Specialty Adhesives | +1.2% | Global | Mid-to-Long term (2025-2033) |

| Increasing Renovation & Repair Activities | +0.9% | North America, Europe | Long-term (2025-2033) |

Construction Adhesive and Sealant Market Challenges Impact Analysis

The construction adhesive and sealant market faces several significant challenges that require strategic navigation by industry participants. One primary challenge is the intense competition from traditional mechanical fastening methods. While adhesives and sealants offer numerous advantages like improved aesthetics, reduced material stress, and enhanced design flexibility, established construction practices often favor nails, screws, and bolts due to familiarity, perceived ease of use, and immediate bond strength. Overcoming this ingrained preference requires continuous education of contractors and specifiers, along with robust demonstration of long-term benefits and cost-effectiveness of adhesive and sealant solutions. This necessitates significant marketing and technical support from manufacturers to drive adoption.

Another critical challenge is the inherent variability and unpredictability of construction site conditions. Environmental factors such as temperature extremes, humidity, dust, and moisture can significantly affect the application and curing performance of adhesives and sealants. Ensuring consistent product performance across diverse and often uncontrolled jobsite environments poses a considerable technical hurdle. Manufacturers must develop products with broad operational windows and provide comprehensive application guidelines, which can add to development costs and complexity. Furthermore, the demand for highly skilled labor for proper application of advanced adhesive and sealant systems can be a bottleneck. A shortage of trained professionals can lead to improper application, material wastage, and compromised performance, ultimately impacting the reputation of the product and the industry as a whole. This challenge is compounded by global labor shortages in the construction sector, putting pressure on training initiatives and the development of easier-to-apply formulations.

Moreover, the continuous pressure to reduce project timelines and costs often leads to a preference for rapid-curing or instantly bonding solutions, which can limit the types of adhesives and sealants that are suitable for certain applications. Balancing fast performance with durability, sustainability, and cost-effectiveness remains an ongoing balancing act for manufacturers. The fragmented nature of the construction industry, with numerous small and medium-sized enterprises, can also make market penetration and distribution challenging, requiring extensive sales networks and localized support. Navigating these multifaceted challenges is crucial for sustained growth and market leadership in a dynamic construction landscape.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Competition from Mechanical Fasteners | -0.9% | Global | Long-term (2025-2033) |

| Variability in Construction Site Conditions | -0.7% | Global | Long-term (2025-2033) |

| Shortage of Skilled Labor for Application | -0.6% | North America, Europe | Mid-to-Long term (2025-2033) |

| Adherence to Diverse Regional Building Codes | -0.4% | Global | Long-term (2025-2033) |

Construction Adhesive and Sealant Market - Updated Report Scope

This report provides an in-depth analysis of the Construction Adhesive and Sealant Market, offering a comprehensive overview of its current size, historical performance, and future growth projections. It delves into the key market dynamics, including drivers, restraints, opportunities, and challenges, providing a holistic understanding of the factors influencing market expansion. The scope encompasses detailed segmentation analysis across various product types, technologies, applications, and end-use sectors, alongside a thorough regional assessment to highlight geographical market trends and growth pockets. Furthermore, the report identifies and profiles key industry players, offering insights into their strategic initiatives and competitive positioning, enabling stakeholders to make informed business decisions. The objective is to equip market participants with actionable intelligence to navigate the complexities of this evolving market and capitalize on emerging opportunities.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 72.5 billion |

| Market Forecast in 2033 | USD 120.2 billion |

| Growth Rate | 6.5% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Adhesives Corp., Construction Sealants Inc., Polymer Bonding Solutions, Industrial Chemicals Group, Building Materials Innovations, Sustainable Sealant Systems, Advanced Bonding Technologies, High-Performance Coatings Ltd., EcoBuild Adhesives, Specialty Resins Inc., Engineered Materials Group, United Sealant Manufacturers, NextGen Construction Solutions, Premier Bonding Products, Durable Adhesives Corp., Zenith Sealants, Innovative Building Solutions, Grand Polymer Works, Universal Bonding Agents, Elite Construction Chemicals. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Construction Adhesive and Sealant market is meticulously segmented to provide a granular view of its diverse components and their respective contributions to overall market dynamics. This comprehensive segmentation allows for a precise analysis of demand patterns, technological shifts, and application-specific requirements across various product types, technological formulations, and end-use applications. Understanding these segments is crucial for identifying niche growth areas, assessing competitive landscapes, and tailoring product development strategies to meet specific industry needs. Each segment exhibits distinct characteristics in terms of material properties, performance attributes, and market adoption rates, driven by specific building codes, environmental regulations, and construction practices prevalent in different regions.

The segmentation by product type reflects the chemical composition and primary performance characteristics of the adhesives and sealants, influencing their suitability for different bonding and sealing applications. Technology segmentation, on the other hand, highlights the formulation methods and curing mechanisms, impacting factors such as application versatility, cure time, and environmental impact. The application and end-use segments delineate where these materials are primarily utilized within the broader construction sector, from foundational elements and structural components to interior finishes and specialized installations. This detailed breakdown offers critical insights into the evolving preferences of contractors, architects, and builders, as they seek materials that not only meet performance criteria but also align with sustainability goals and project efficiency demands.

- By Product Type:

- Acrylic

- Polyurethane

- Epoxy

- Silicone

- Polysulfide

- Silyl Modified Polymer (SMP)

- Others (e.g., Butyl, Latex, Hybrid)

- By Technology:

- Water-based

- Solvent-based

- Hot-melt

- Reactive (e.g., moisture-curing, UV-curing)

- Others

- By Application:

- Residential Construction

- Single-family

- Multi-family

- Commercial Construction

- Office Buildings

- Retail & Shopping Centers

- Healthcare Facilities

- Educational Institutions

- Hospitality

- Infrastructure

- Roads & Bridges

- Dams & Ports

- Airports

- Utilities (Water, Wastewater, Power)

- Industrial Construction

- Residential Construction

- By End-Use:

- Building & Construction

- Residential

- Non-Residential (Commercial, Industrial, Institutional)

- Flooring

- Wall Covering

- Glazing

- Roofing

- Sanitary & Plumbing

- HVAC (Heating, Ventilation, and Air Conditioning)

- Other Construction Elements (e.g., Tile & Stone, Waterproofing)

- Building & Construction

Regional Highlights

- Asia Pacific (APAC): Expected to be the fastest-growing region, driven by rapid urbanization, significant government investments in infrastructure development (e.g., China's Belt and Road Initiative, India's Smart Cities Mission), and booming residential construction due to population growth. Countries like China, India, and Southeast Asian nations are at the forefront of this expansion, demanding large volumes of adhesives and sealants for new builds and renovation projects.

- North America: A mature market characterized by increasing demand for sustainable and high-performance products. Growth is primarily propelled by renovation and repair activities, smart building initiatives, and the adoption of advanced construction techniques such as modular and prefabricated building, particularly in the United States and Canada. Stringent building codes also drive the adoption of specialized, high-quality solutions.

- Europe: Shows steady growth, largely influenced by stringent environmental regulations, a strong emphasis on energy efficiency in buildings, and the renovation of aging infrastructure. Western European countries lead in the adoption of eco-friendly, low-VOC adhesives and sealants, driven by directives promoting green construction and circular economy principles. Eastern Europe also contributes to growth through new construction projects and infrastructure upgrades.

- Latin America: Demonstrates significant growth potential, fueled by increasing foreign investments in infrastructure, rising residential construction to address housing deficits, and expanding commercial development in key economies like Brazil, Mexico, and Argentina. The market here is characterized by a growing awareness of modern construction materials and techniques.

- Middle East and Africa (MEA): Projects in the Gulf Cooperation Council (GCC) countries, such as Saudi Arabia's Vision 2030 and UAE's diversification efforts, are driving substantial demand for adhesives and sealants in mega-projects, commercial hubs, and residential complexes. African nations are experiencing growth due to urbanization and infrastructure development, albeit from a lower base, making it a region of emerging opportunity.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Construction Adhesive and Sealant Market.- Global Adhesives Corp.

- Construction Sealants Inc.

- Polymer Bonding Solutions

- Industrial Chemicals Group

- Building Materials Innovations

- Sustainable Sealant Systems

- Advanced Bonding Technologies

- High-Performance Coatings Ltd.

- EcoBuild Adhesives

- Specialty Resins Inc.

- Engineered Materials Group

- United Sealant Manufacturers

- NextGen Construction Solutions

- Premier Bonding Products

- Durable Adhesives Corp.

- Zenith Sealants

- Innovative Building Solutions

- Grand Polymer Works

- Universal Bonding Agents

- Elite Construction Chemicals

Frequently Asked Questions

What are the primary drivers of growth in the Construction Adhesive and Sealant Market?

The market is primarily driven by rapid urbanization and extensive infrastructure development globally, particularly in emerging economies. Additionally, the increasing adoption of sustainable building practices, technological advancements in material science, and the growing preference for modular and prefabricated construction techniques significantly contribute to market expansion.

How do environmental regulations impact the Construction Adhesive and Sealant industry?

Environmental regulations, especially those concerning Volatile Organic Compound (VOC) emissions and hazardous chemicals, significantly influence the market by compelling manufacturers to develop and adopt eco-friendly, low-VOC, and bio-based formulations. This drives innovation towards greener products but can also increase R&D costs and production complexities.

What are the key product types dominating the Construction Adhesive and Sealant Market?

Key product types include acrylics, polyurethanes, epoxies, and silicones. Each type offers distinct performance characteristics, making them suitable for specific applications based on factors such as bond strength, flexibility, weather resistance, and curing properties, catering to diverse construction needs.

Which regions are expected to exhibit the highest growth in this market?

Asia Pacific is projected to be the fastest-growing region due to its booming construction sector, driven by rapid urbanization, significant government investments in infrastructure, and increasing residential and commercial development. Other high-growth regions include Latin America and the Middle East & Africa.

What are the major challenges faced by manufacturers in the Construction Adhesive and Sealant Market?

Manufacturers face challenges such as volatile raw material prices, intense competition from traditional mechanical fastening methods, the inherent variability of construction site conditions, and the need for highly skilled labor for proper application of advanced adhesive and sealant systems. Adherence to diverse regional building codes also presents a constant challenge.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted