Conductive Die Attach Adhesive Market

Conductive Die Attach Adhesive Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708364 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

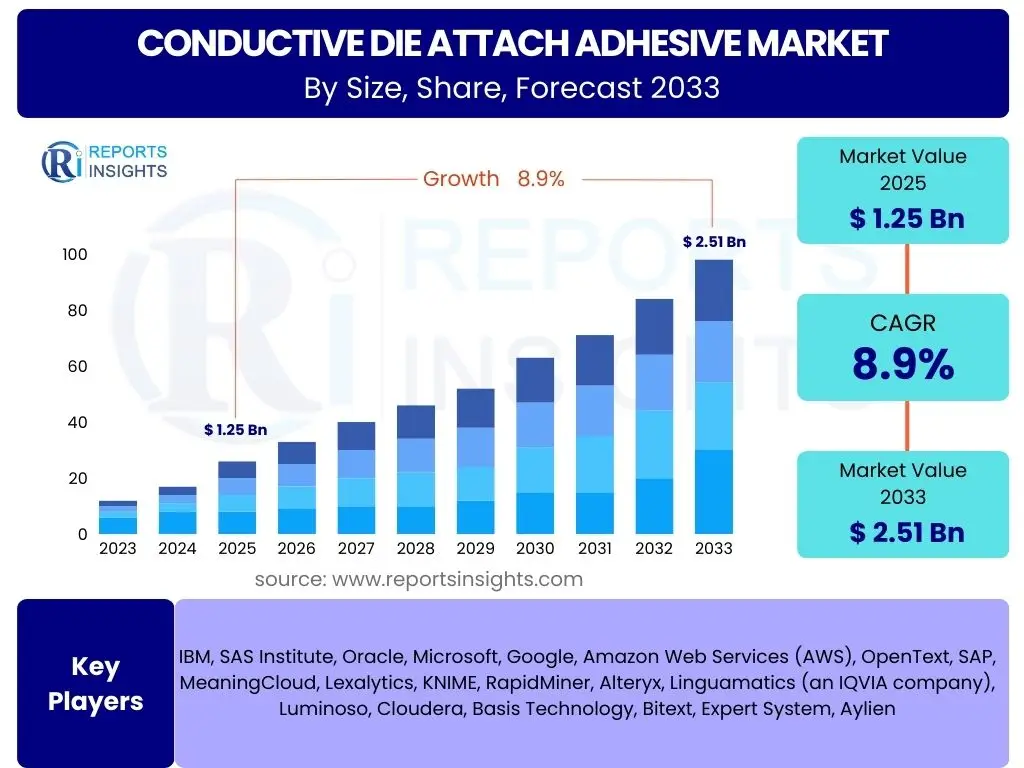

Conductive Die Attach Adhesive Market Size

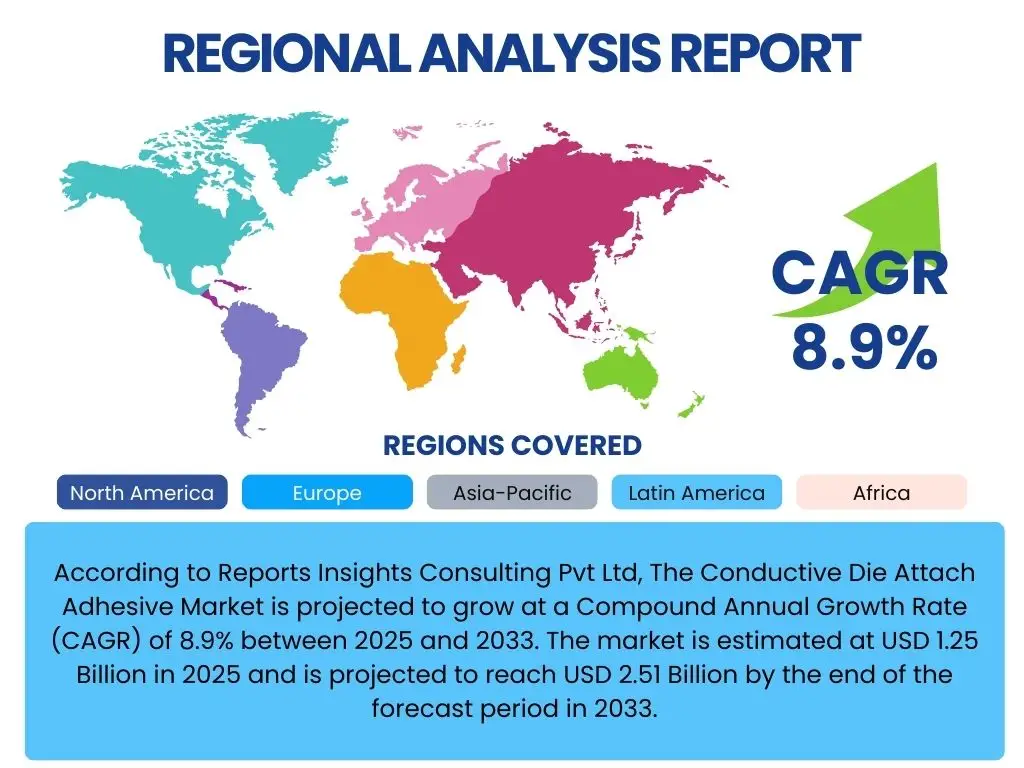

According to Reports Insights Consulting Pvt Ltd, The Conductive Die Attach Adhesive Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.9% between 2025 and 2033. The market is estimated at USD 1.25 Billion in 2025 and is projected to reach USD 2.51 Billion by the end of the forecast period in 2033.

Key Conductive Die Attach Adhesive Market Trends & Insights

User queries frequently highlight the evolving demands for advanced material solutions in semiconductor packaging. A significant trend involves the development of adhesives capable of meeting stringent thermal and electrical performance requirements, driven by miniaturization and increasing power densities in electronic devices. Furthermore, there is growing interest in eco-friendly and robust conductive adhesives that can withstand harsh operating conditions, reflecting a broader industry shift towards sustainability and enhanced product reliability. The convergence of high-performance computing, artificial intelligence, and sophisticated automotive electronics also underscores a need for materials offering superior long-term stability and precise conductivity.

Another prominent area of inquiry relates to the adoption of novel material compositions, such as silver-sintering technology and alternative conductive fillers, to achieve ultra-high thermal conductivity and improved electrical interconnects. The market is also witnessing a trend towards lower curing temperatures and faster processing times, which are crucial for high-volume manufacturing and cost efficiency. These innovations are vital for supporting the next generation of advanced packaging solutions, including System-in-Package (SiP), Chip-on-Board (CoB), and multi-chip modules, which require exceptional adhesive performance for reliable operation.

- Miniaturization of electronic components driving demand for fine-pitch, high-resolution adhesives.

- Increasing integration of advanced packaging technologies such as 3D ICs and SiP.

- Growth in automotive electronics, particularly for ADAS and electric vehicle power modules, requiring high reliability.

- Development of lead-free and halogen-free formulations to comply with environmental regulations.

- Rising adoption of 5G infrastructure and IoT devices necessitating high-frequency performance.

- Advancements in thermal management solutions for high-power semiconductor devices.

- Shift towards lower temperature curing and faster processing times for enhanced manufacturing efficiency.

AI Impact Analysis on Conductive Die Attach Adhesive

Common user questions regarding AI's impact on the Conductive Die Attach Adhesive market often center on its role in material discovery, process optimization, and quality control. Users are keen to understand how AI can accelerate the development of new adhesive formulations with tailored properties, moving beyond traditional trial-and-error methods. There is also significant interest in AI's ability to enhance manufacturing efficiency by optimizing parameters like curing profiles, dispensing accuracy, and yield rates, thereby reducing production costs and time-to-market. Predictive analytics powered by AI for defect detection and reliability assessment during the production of semiconductor packages is another key area of user inquiry, addressing concerns about consistency and performance.

Beyond material and process improvements, users are exploring AI's potential in supply chain management for conductive die attach adhesives. This includes forecasting demand more accurately, optimizing inventory levels, and identifying potential supply disruptions proactively. The application of AI in simulating the long-term performance and degradation mechanisms of adhesives under various environmental conditions also features prominently in discussions. This capability allows for more robust product design and validation, ultimately contributing to higher reliability and extended lifespan of electronic devices. The overall expectation is that AI will introduce unprecedented levels of precision, efficiency, and innovation into the entire lifecycle of conductive die attach adhesives.

- Accelerated material discovery and formulation design through AI-driven simulations and predictive modeling.

- Optimization of manufacturing processes, including dispensing, curing, and bonding parameters, leading to higher yields and reduced waste.

- Enhanced quality control and defect detection via machine vision and deep learning algorithms.

- Predictive maintenance for manufacturing equipment, minimizing downtime and increasing operational efficiency.

- Supply chain optimization for raw materials and finished products, improving logistics and reducing lead times.

- Advanced performance prediction and reliability testing of adhesives under diverse operating conditions.

Key Takeaways Conductive Die Attach Adhesive Market Size & Forecast

User inquiries concerning key takeaways from the Conductive Die Attach Adhesive market size and forecast consistently point towards a strong growth trajectory driven by the insatiable demand for advanced electronics. A significant insight is the critical role these adhesives play in enabling next-generation semiconductor technologies, making their market expansion intrinsically linked to the broader electronics industry's innovation pace. The market's resilience is further highlighted by its ability to adapt to evolving performance demands, such as higher thermal conductivity and mechanical robustness, which are essential for the increasingly complex and power-dense integrated circuits.

Another crucial takeaway is the geographical shift in market dynamics, with the Asia Pacific region continuing to dominate due to its robust semiconductor manufacturing ecosystem and burgeoning consumer electronics market. The forecast also underscores the increasing emphasis on sustainable and compliant material solutions, pushing manufacturers towards eco-friendly formulations. Overall, the market is characterized by continuous technological advancements and strategic investments aimed at addressing the diverse and stringent requirements across various end-use industries, ensuring its sustained growth and pivotal role in electronic packaging.

- The market is poised for robust expansion, driven by continuous innovation in semiconductor and advanced electronics packaging.

- Asia Pacific remains the leading region, propelled by its manufacturing prowess and high electronics consumption.

- Technological advancements, particularly in thermal management and mechanical reliability, are critical growth enablers.

- Increasing demand from automotive, 5G, and IoT sectors is a significant contributor to market acceleration.

- Environmental regulations are shaping product development towards sustainable and high-performance lead-free solutions.

- Strategic collaborations and R&D investments are key for competitive advantage and addressing complex application requirements.

Conductive Die Attach Adhesive Market Drivers Analysis

The conductive die attach adhesive market is propelled by several fundamental drivers stemming from the rapidly evolving electronics and semiconductor industries. The relentless pursuit of miniaturization and increased functionality in electronic devices necessitates advanced materials that can perform reliably in confined spaces. This, coupled with the escalating demand for high-power and high-frequency components, drives innovation in adhesive formulations capable of superior thermal dissipation and electrical conductivity. The proliferation of diverse electronic applications, from consumer gadgets to sophisticated industrial and automotive systems, further fuels the market's expansion.

The increasing complexity of semiconductor packaging, including the adoption of advanced techniques such as 3D stacking, System-in-Package (SiP), and multi-chip modules, relies heavily on high-performance die attach adhesives. These packaging technologies require materials that offer excellent adhesion to various substrates, high bond line uniformity, and consistent electrical and thermal properties. Moreover, the global shift towards electric vehicles, 5G communication infrastructure, and the Internet of Things (IoT) generates significant demand for robust and reliable electronic components, making conductive die attach adhesives indispensable for the next generation of electronic devices.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Miniaturization and High-Density Packaging | +2.1% | Global, particularly APAC (Taiwan, South Korea, China) | Short to Medium Term (2025-2029) |

| Growth in Automotive Electronics and EVs | +1.8% | North America, Europe, Asia Pacific (China, Japan, Germany, USA) | Medium to Long Term (2026-2033) |

| Expansion of 5G and IoT Infrastructure | +1.5% | Global, especially North America, Asia Pacific (China) | Short to Medium Term (2025-2030) |

| Increasing Demand for High-Power Devices | +1.3% | Global, particularly industrial and data center hubs | Medium Term (2026-2031) |

Conductive Die Attach Adhesive Market Restraints Analysis

Despite robust growth, the conductive die attach adhesive market faces several significant restraints that could impede its trajectory. The high cost associated with advanced conductive fillers, particularly silver, which is a primary component in many high-performance formulations, poses a substantial challenge. This cost factor directly impacts the overall production expenses of electronic devices, especially for mass-produced consumer electronics where cost-efficiency is paramount. Furthermore, the inherent complexity in developing adhesives that simultaneously offer high electrical conductivity, excellent thermal management, and robust mechanical properties, all while maintaining low stress and long-term reliability, presents a considerable technical hurdle.

Another key restraint involves the stringent performance requirements and reliability standards demanded by various end-use industries, such as automotive and aerospace. Meeting these rigorous specifications often necessitates extensive research and development, prolonged qualification cycles, and specialized manufacturing processes, adding to product development costs and time-to-market. Moreover, environmental regulations, such as RoHS and REACH, increasingly restrict the use of certain materials, compelling manufacturers to invest in developing compliant yet equally effective alternatives, which can be a complex and resource-intensive endeavor, potentially slowing down innovation and product adoption in some segments.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Cost of Raw Materials (e.g., Silver Fillers) | -1.5% | Global, especially price-sensitive consumer electronics markets | Short to Medium Term (2025-2030) |

| Complexity in Achieving Multifunctional Properties | -1.2% | Global, impacting high-performance application segments | Medium Term (2026-2031) |

| Stringent Reliability and Performance Standards | -1.0% | North America, Europe (Automotive, Aerospace) | Long Term (2027-2033) |

| Environmental and Regulatory Compliance | -0.8% | Europe, North America, parts of Asia (China, Japan) | Short to Medium Term (2025-2029) |

Conductive Die Attach Adhesive Market Opportunities Analysis

The conductive die attach adhesive market is rich with opportunities, primarily driven by the continuous evolution of electronic device architecture and emerging application areas. A significant opportunity lies in the development of advanced packaging technologies like fan-out wafer-level packaging (FOWLP) and hybrid bonding, which demand ultra-fine pitch interconnects and superior thermal performance. These next-generation packaging methods require innovative adhesive solutions that can meet more exacting specifications for miniaturization, speed, and power efficiency, opening avenues for specialized product development and market penetration for manufacturers capable of meeting these demanding criteria.

Another key area of opportunity is the growing adoption of high-power semiconductor devices in sectors such as electric vehicles, renewable energy systems, and industrial power electronics. These applications require adhesives with exceptional thermal conductivity and long-term reliability under extreme operating conditions. Furthermore, the burgeoning biomedical and wearable electronics markets present unique demands for biocompatible, flexible, and reliable conductive adhesives, offering a niche yet high-growth segment. The ongoing transition towards greener electronics also creates an opportunity for developing and commercializing sustainable, solvent-free, and low-VOC (Volatile Organic Compound) adhesive formulations that comply with global environmental standards while maintaining performance integrity.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Advancements in Advanced Packaging Technologies | +2.0% | Global, particularly APAC (Taiwan, South Korea) | Short to Medium Term (2025-2030) |

| Emergence of High-Power and Wide-Bandgap Devices | +1.7% | Global (Industrial, Automotive, Energy sectors) | Medium to Long Term (2026-2033) |

| Expansion into Biomedical and Wearable Electronics | +1.4% | North America, Europe, Asia Pacific (China, USA) | Medium Term (2026-2031) |

| Development of Eco-friendly and Sustainable Adhesives | +1.1% | Europe, North America, Japan | Short to Medium Term (2025-2029) |

Conductive Die Attach Adhesive Market Challenges Impact Analysis

The conductive die attach adhesive market confronts significant challenges, predominantly driven by the ever-increasing performance demands of modern electronics. One primary challenge is achieving superior thermal management alongside high electrical conductivity within a single adhesive formulation, especially as semiconductor devices generate more heat in smaller packages. Balancing these conflicting requirements, while also ensuring robust mechanical properties such as low stress and excellent adhesion, poses a complex material science problem. The need for adhesives that can maintain integrity and performance under extreme thermal cycling and high humidity conditions further exacerbates this challenge, directly impacting device reliability and lifespan.

Another critical challenge stems from the miniaturization trend, which necessitates adhesives capable of ultra-fine pitch bonding and consistent bond line thickness at micron levels. This requires high precision in dispensing and curing, along with formulations that prevent voids and delamination, especially in advanced packaging architectures. Furthermore, the volatility of raw material prices, particularly for precious metals like silver, introduces cost unpredictability and supply chain risks for manufacturers. Addressing these multifaceted challenges requires continuous innovation in material science, sophisticated manufacturing processes, and strategic partnerships across the value chain to ensure product competitiveness and market viability.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Balancing Thermal Conductivity and Mechanical Stress | -1.6% | Global, particularly high-performance computing and power electronics | Short to Medium Term (2025-2030) |

| Achieving Ultra-Fine Pitch and Void-Free Bonding | -1.3% | Global, affecting advanced packaging manufacturers | Medium Term (2026-2031) |

| Raw Material Price Volatility and Supply Chain Risks | -1.1% | Global, especially for manufacturers relying on precious metals | Short Term (2025-2028) |

| Ensuring Long-Term Reliability in Harsh Environments | -0.9% | Automotive, Aerospace, Industrial sectors globally | Long Term (2027-2033) |

Conductive Die Attach Adhesive Market - Updated Report Scope

This updated report provides an in-depth analysis of the global Conductive Die Attach Adhesive Market, offering comprehensive insights into its current size, historical performance, and future growth projections from 2025 to 2033. It meticulously covers key market trends, growth drivers, formidable restraints, emerging opportunities, and significant challenges impacting the industry landscape. The report segments the market by product type, application, and end-use industry, providing detailed regional breakdowns to highlight specific market dynamics and competitive landscapes across major geographies. Furthermore, it incorporates an AI impact analysis, illustrating how artificial intelligence is reshaping material development, manufacturing processes, and quality control within this critical sector, ultimately offering stakeholders a strategic roadmap for navigating market complexities and capitalizing on future growth avenues.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.25 Billion |

| Market Forecast in 2033 | USD 2.51 Billion |

| Growth Rate | 8.9% |

| Number of Pages | 267 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Henkel AG & Co. KGaA, Dow Inc., Lord Corporation (Parker Hannifin), Shin-Etsu Chemical Co., Ltd., Sumitomo Bakelite Co., Ltd., Showa Denko Materials Co., Ltd., 3M Company, DuPont de Nemours, Inc., Hitachi Chemical Company, Ltd. (Showa Denko Materials), Momentive Performance Materials Inc., Master Bond Inc., Kyocera Corporation, Indium Corporation, Ablestik Laboratories (Henkel), BASF SE |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Conductive Die Attach Adhesive Market is rigorously segmented to provide a granular understanding of its diverse components and drivers. This segmentation allows for precise analysis of market dynamics across various product types, filler materials, specific applications, and broad end-use industries, reflecting the multifaceted demands placed upon these critical materials. By categorizing the market in this manner, stakeholders can identify high-growth areas, emerging technological preferences, and the specific needs of different vertical markets, enabling more targeted strategic planning and product development initiatives.

Each segment is influenced by unique technological advancements and market forces. For instance, the choice of product type (e.g., epoxy, silicone) depends heavily on the required performance characteristics like thermal stability, flexibility, and curing profile. Similarly, the filler type (e.g., silver, copper) is crucial for achieving specific electrical and thermal conductivities, often balanced against cost considerations. Application-specific demands (e.g., LED packaging vs. automotive power devices) drive the need for tailored adhesive properties, while end-use industry requirements dictate adherence to specific industry standards and long-term reliability expectations. This detailed segmentation highlights the market's complexity and the necessity for specialized adhesive solutions across the electronics manufacturing landscape.

- By Product Type:

- Epoxy Based: Dominant due to excellent adhesion, mechanical strength, and thermal stability.

- Silicone Based: Preferred for flexibility, high-temperature performance, and low stress applications.

- Acrylic Based: Valued for quick curing and strong adhesion.

- Polyimide Based: Used in demanding high-temperature and harsh environment applications.

- Others: Includes polyurethane and cyanate ester formulations for niche requirements.

- By Filler Type:

- Silver: Offers highest electrical and thermal conductivity, but higher cost.

- Copper: Cost-effective alternative to silver, with good conductivity.

- Carbon: Used for specific applications where cost-effectiveness is crucial and moderate conductivity suffices.

- Hybrid: Combines different fillers to optimize performance and cost.

- Others: Including nickel, gold, and other metallic or carbon-based materials.

- By Application:

- LED Packaging: Critical for thermal dissipation and electrical connection in high-brightness LEDs.

- RF Devices: Essential for high-frequency performance and signal integrity.

- Power Devices: Requires excellent thermal management for high-power semiconductor components.

- MEMS: Used for precise bonding in miniature electromechanical systems.

- Image Sensors: Demands high purity and low outgassing to prevent contamination.

- Logic & Memory Devices: Supports advanced packaging for CPUs, GPUs, and memory chips.

- Others: Encompasses optoelectronics, medical devices, and custom industrial applications.

- By End-Use Industry:

- Consumer Electronics: Driven by demand for smartphones, tablets, laptops, and wearables.

- Automotive: Critical for ADAS, infotainment, powertrain, and EV components, demanding high reliability.

- Telecommunications: Supports 5G infrastructure, base stations, and network equipment.

- Industrial: Used in power management, automation, and control systems.

- Aerospace & Defense: Requires extreme reliability and performance in harsh conditions.

- Healthcare: Utilized in medical implants, diagnostic equipment, and portable devices.

- Others: Includes smart home devices, IoT sensors, and renewable energy systems.

Regional Highlights

- Asia Pacific (APAC): Dominates the global market share, primarily due to the presence of major semiconductor manufacturing hubs in countries like Taiwan, South Korea, China, and Japan. The region benefits from a robust electronics industry, high consumer electronics consumption, and significant government investments in semiconductor R&D and production. China, in particular, is a key growth engine due to its massive electronics manufacturing base and burgeoning domestic market.

- North America: A significant market characterized by strong innovation in high-tech industries, including advanced computing, aerospace, and medical electronics. The United States leads in R&D for next-generation semiconductor technologies and packaging, driving demand for high-performance conductive die attach adhesives. Growth is also fueled by the expanding automotive electronics sector and investments in 5G infrastructure.

- Europe: Exhibits steady growth, driven by its robust automotive industry, strong focus on industrial automation, and increasing adoption of sustainable electronic solutions. Countries like Germany, France, and the UK are key contributors, emphasizing high-reliability and environmentally compliant adhesive solutions for specialized applications. The region's stringent regulations also push for innovations in lead-free and halogen-free products.

- Latin America: An emerging market with growing electronics manufacturing capabilities, particularly in countries like Mexico and Brazil. While smaller than other regions, it offers potential for growth fueled by increasing consumer electronics penetration and investment in telecommunications infrastructure.

- Middle East and Africa (MEA): Represents a nascent market for conductive die attach adhesives. Growth is expected to be moderate, driven by urbanization, increasing disposable incomes, and developing telecommunications and automotive sectors in select countries. Local manufacturing initiatives and foreign investments could accelerate market expansion in the long term.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Conductive Die Attach Adhesive Market.- Henkel AG & Co. KGaA

- Dow Inc.

- Lord Corporation (Parker Hannifin)

- Shin-Etsu Chemical Co., Ltd.

- Sumitomo Bakelite Co., Ltd.

- Showa Denko Materials Co., Ltd.

- 3M Company

- DuPont de Nemours, Inc.

- Hitachi Chemical Company, Ltd. (Showa Denko Materials)

- Momentive Performance Materials Inc.

- Master Bond Inc.

- Kyocera Corporation

- Indium Corporation

- Ablestik Laboratories (Henkel)

- BASF SE

- Dymax Corporation

- DELO Industrial Adhesives

- Heraeus Group

- Fujifilm Corporation

- Electronic Materials Inc.

Frequently Asked Questions

What is a Conductive Die Attach Adhesive?

A Conductive Die Attach Adhesive is a specialized material used in semiconductor packaging to mechanically bond a silicon die (chip) to a substrate or lead frame, while also providing an electrical connection and often aiding in thermal dissipation. These adhesives typically contain conductive fillers, such as silver or copper, embedded in a polymer matrix like epoxy or silicone.

What are the primary applications of Conductive Die Attach Adhesives?

Primary applications include LED packaging, power devices (e.g., IGBTs, MOSFETs), RFdevices, MEMS, image sensors, and logic and memory devices. They are crucial in consumer electronics, automotive electronics, telecommunications (5G), industrial equipment, and aerospace & defense for their ability to ensure reliable electrical and thermal performance.

How do Conductive Die Attach Adhesives differ from non-conductive adhesives?

The key difference lies in their electrical properties. Conductive die attach adhesives are engineered to provide an electrical pathway between the die and its substrate, typically using metallic fillers. Non-conductive adhesives, in contrast, are electrically insulating and are used where electrical isolation between components is required.

What factors influence the performance and selection of these adhesives?

Key factors include electrical conductivity, thermal conductivity, adhesion strength, coefficient of thermal expansion (CTE) match, curing temperature and time, mechanical properties (e.g., modulus, flexibility), reliability under thermal cycling and humidity, and environmental compliance (e.g., lead-free, halogen-free).

What are the current trends in the Conductive Die Attach Adhesive market?

Current trends include the development of adhesives for miniaturized components, advanced packaging technologies (SiP, 3D ICs), enhanced thermal management for high-power devices, growth in automotive electronics and 5G infrastructure, and a strong push towards eco-friendly and sustainable formulations compliant with global environmental regulations.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted