Silicon Electrical Steel Market

Silicon Electrical Steel Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700285 | Last Updated : July 23, 2025 |

Format : ![]()

![]()

![]()

![]()

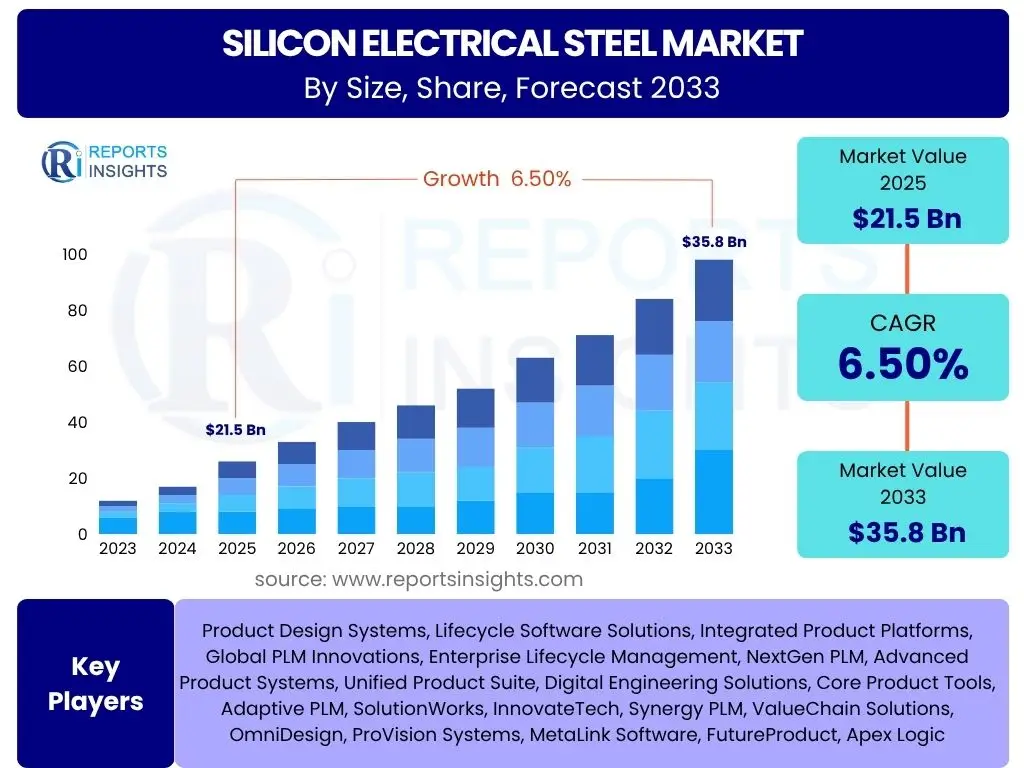

Silicon Electrical Steel Market is projected to grow at a Compound annual growth rate (CAGR) of 6.5% between 2025 and 2033, reaching USD 21.5 Billion in 2025 and is projected to grow to USD 35.8 Billion by 2033 the end of the forecast period.

Key Silicon Electrical Steel Market Trends & Insights

The global silicon electrical steel market is currently experiencing dynamic shifts driven by several pervasive trends that are reshaping its landscape. A significant emphasis on energy efficiency across various industrial and consumer applications is prompting increased demand for high-performance electrical steel grades, specifically those with enhanced magnetic properties and reduced core losses. This focus is directly aligned with global initiatives aimed at decarbonization and sustainable energy consumption, making advanced material science in electrical steel production a critical area of innovation. Furthermore, the rapid expansion of renewable energy infrastructure, including wind turbines and solar power installations, necessitates robust and efficient transformer and generator components, thereby fueling the need for specialized silicon electrical steel products. The automotive industry's accelerating transition towards electric vehicles (EVs) is also creating a substantial new segment for electrical steel, as it is an indispensable material for efficient EV motors and charging infrastructure.

- Growing adoption of high-efficiency transformers and electric motors to meet stringent energy consumption regulations and reduce operational costs.

- Escalating investments in renewable energy infrastructure, particularly wind and solar farms, which require large volumes of specialized electrical steel for power generation and transmission.

- The rapid expansion of the electric vehicle (EV) market, driving demand for advanced electrical steel grades used in efficient EV motors and charging stations.

- Advancements in material science and manufacturing processes leading to the development of thinner, higher-grade electrical steel with superior magnetic properties.

- Increasing focus on smart grid technologies and grid modernization projects globally, integrating electrical steel components for enhanced reliability and efficiency.

- Rising industrialization and urbanization in emerging economies, leading to increased electricity demand and subsequent infrastructure development, including power transformers and distribution networks.

AI Impact Analysis on Silicon Electrical Steel

Artificial intelligence is poised to significantly transform the silicon electrical steel market by enhancing various stages of its value chain, from material design and manufacturing to supply chain optimization and market analysis. In the realm of material science, AI algorithms can accelerate the discovery and optimization of new alloy compositions and microstructures, leading to the development of electrical steel with superior magnetic properties, reduced core losses, and improved ductility. This data-driven approach allows for predictive modeling of material performance, significantly cutting down research and development cycles and costs. Furthermore, AI-powered predictive maintenance in manufacturing facilities can optimize production processes, minimize defects, and ensure consistent quality, thereby improving yield rates and operational efficiency. By analyzing vast datasets, AI can also provide more accurate demand forecasts, supply chain risk assessments, and market trend predictions, enabling manufacturers and suppliers to make more informed strategic decisions and respond dynamically to market shifts.

- AI-driven material discovery and optimization for novel electrical steel alloys with enhanced performance characteristics and reduced material waste.

- Predictive analytics and machine learning applied to manufacturing processes for real-time quality control, defect detection, and optimization of rolling and annealing parameters.

- AI-enhanced supply chain management to improve logistics, inventory optimization, and demand forecasting, leading to more resilient and efficient material flow.

- Automated inspection systems utilizing computer vision and AI for non-destructive testing of electrical steel sheets, ensuring higher product quality and compliance.

- Development of smart electrical steel products with embedded sensors or AI capabilities for real-time performance monitoring and predictive maintenance in end-use applications.

- Leveraging AI for market intelligence, competitive analysis, and strategic planning, identifying emerging trends, customer needs, and potential disruptions.

Key Takeaways Silicon Electrical Steel Market Size & Forecast

- The global silicon electrical steel market is projected to reach USD 35.8 Billion by 2033, demonstrating robust growth potential.

- A Compound Annual Growth Rate (CAGR) of 6.5% is anticipated for the period between 2025 and 2033, indicating steady expansion.

- The market's initial valuation in 2025 is estimated at USD 21.5 Billion, serving as the base for future growth.

- Growth is primarily driven by increasing demand for energy-efficient electrical components and rapid expansion in electric vehicle manufacturing.

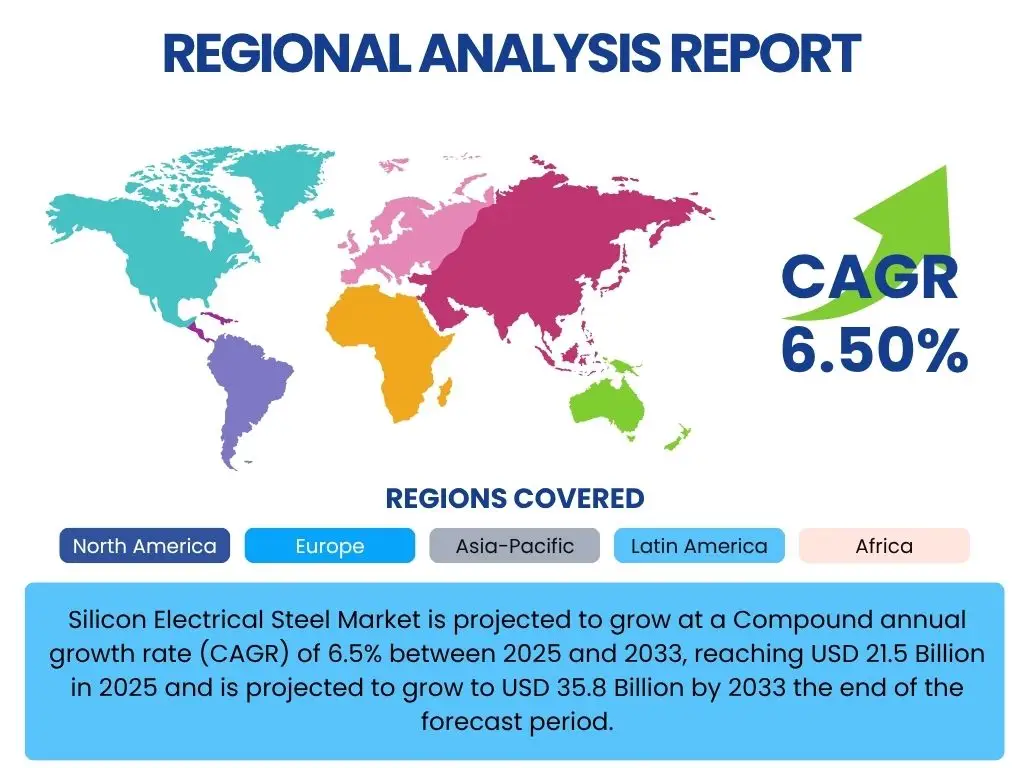

- Asia Pacific is expected to remain the dominant region, driven by extensive infrastructure development and industrialization.

- Technological advancements in material composition and manufacturing processes are contributing significantly to market expansion and product innovation.

- Investments in renewable energy projects globally are a key catalyst for sustained demand for silicon electrical steel in transformers and generators.

Silicon Electrical Steel Market Drivers Analysis

The silicon electrical steel market is fundamentally propelled by a confluence of global mega-trends, chief among them being the escalating emphasis on energy efficiency and the profound shift towards electrification across various sectors. Governments and industries worldwide are implementing stricter energy consumption regulations and performance standards for electrical equipment, directly stimulating demand for high-grade electrical steel that minimizes energy losses in transformers, motors, and generators. This regulatory push, combined with an economic incentive to reduce operational costs through greater efficiency, makes the adoption of advanced silicon electrical steel an imperative for manufacturers. The rapid expansion of renewable energy sources, such as wind and solar power, further necessitates robust and highly efficient electrical infrastructure for power generation, transmission, and distribution, creating a consistent demand for specialized electrical steel products essential for these systems.

Beyond energy efficiency, the transformative growth of the electric vehicle (EV) industry stands as a monumental driver for the silicon electrical steel market. EVs rely heavily on high-performance electrical steel for their traction motors, where efficiency, power density, and durability are paramount. As global EV production scales rapidly, so too does the demand for the specialized grades of silicon electrical steel required for these advanced electric powertrains. Furthermore, widespread industrialization and urbanization, particularly in developing economies, are continuously expanding electricity grids and industrial infrastructure, leading to increased installation of power and distribution transformers, industrial motors, and other electrical apparatus. This sustained infrastructural development worldwide ensures a steady underlying demand for silicon electrical steel, solidifying its position as a critical material in the modern electrical landscape.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Push for Energy Efficiency and Decarbonization | +1.8% | Global, particularly Europe, North America, China | Long-term (2025-2033) |

| Rapid Growth of Electric Vehicle (EV) Industry | +1.5% | China, Europe, North America, Japan, South Korea | Medium to Long-term (2025-2033) |

| Expansion of Renewable Energy Infrastructure (Wind, Solar) | +1.2% | Global, especially China, India, US, EU countries | Long-term (2025-2033) |

| Modernization and Expansion of Power Grids | +1.0% | Emerging economies (APAC, Latin America, MEA), US, Europe | Medium to Long-term (2025-2033) |

| Industrialization and Urbanization in Developing Regions | +0.8% | Asia Pacific (India, Southeast Asia), Latin America, Africa | Long-term (2025-2033) |

Silicon Electrical Steel Market Restraints Analysis

Despite robust growth drivers, the silicon electrical steel market faces significant restraints that could temper its expansion. One of the primary concerns is the volatility in raw material prices, particularly for steel, silicon, and other alloying elements. Fluctuations in the global commodity markets can lead to unpredictable production costs, impacting manufacturers' profitability and pricing strategies. This instability makes long-term planning challenging and can deter new investments in production capacity. Additionally, the capital-intensive nature of silicon electrical steel manufacturing, involving specialized equipment and high energy consumption for processes like annealing and rolling, presents a substantial barrier to entry for new players and limits the agility of existing ones to quickly scale up production in response to demand surges.

Furthermore, stringent environmental regulations related to steel production, including emissions control and waste management, impose additional operational costs and necessitate significant investments in compliance technologies. While these regulations promote sustainability, they can also increase the overall cost of production and potentially slow down capacity expansions in some regions. The market also grapples with the potential for technological substitution from alternative materials or designs that aim to achieve similar magnetic properties or energy efficiency with different compositions. Although silicon electrical steel remains superior for many applications, ongoing research into new materials could pose a long-term threat. Lastly, geopolitical tensions and trade disputes can disrupt global supply chains, affecting the availability of raw materials and the smooth flow of finished products, thereby creating market uncertainty and hindering international trade in electrical steel.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility in Raw Material Prices (Steel, Silicon) | -0.9% | Global, particularly major steel-producing/consuming regions | Short to Medium-term (2025-2028) |

| High Capital Investment and Production Costs | -0.7% | Global, impacts new entrants and capacity expansion | Long-term (2025-2033) |

| Stringent Environmental Regulations and Compliance Costs | -0.6% | Europe, North America, China | Medium to Long-term (2025-2033) |

| Potential for Material Substitution or Design Innovations | -0.5% | Global, R&D focused regions | Long-term (2028-2033) |

| Geopolitical Instability and Trade Barriers | -0.4% | Global, impacting supply chains | Short to Medium-term (2025-2028) |

Silicon Electrical Steel Market Opportunities Analysis

The silicon electrical steel market is brimming with promising opportunities, primarily stemming from the accelerating global transition towards sustainable energy systems and advanced electric mobility. The significant expansion of offshore wind power projects, large-scale solar farms, and grid-scale battery storage solutions presents a substantial demand for high-grade electrical steel used in power transformers, generators, and specialized inductors crucial for efficient power conversion and transmission. As countries worldwide commit to ambitious renewable energy targets, the underlying need for robust and efficient electrical infrastructure components, where silicon electrical steel is indispensable, will continue to grow exponentially. Furthermore, the imperative for grid modernization, including smart grid initiatives and the integration of decentralized energy resources, opens up new avenues for advanced electrical steel applications in more complex and intelligent electrical networks.

Beyond the energy sector, the burgeoning adoption of electric vehicles (EVs) offers a transformative growth opportunity. The continuous innovation in EV powertrain technology drives the demand for lighter, more efficient, and high-performance electrical steel grades with improved magnetic properties capable of handling higher frequencies and temperatures. This specialization represents a high-value segment for manufacturers willing to invest in research and development for tailored solutions. Additionally, the increasing demand for high-efficiency motors across various industrial and household applications, coupled with stringent energy efficiency regulations, creates a persistent need for improved Non-Grain Oriented Electrical Steel (NGOES). Lastly, the digitalization of manufacturing processes and the adoption of Industry 4.0 principles, including artificial intelligence and predictive analytics, present opportunities for silicon electrical steel manufacturers to optimize production, enhance product quality, and develop customized solutions, thereby improving competitiveness and market reach.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Advanced Electrical Steel for EV Motors | +1.7% | Global, particularly leading automotive manufacturing hubs | Long-term (2025-2033) |

| Growth in Offshore Wind and Large-Scale Solar Projects | +1.5% | Europe, Asia Pacific (China, India), North America | Long-term (2025-2033) |

| Expansion into Smart Grid and Modernization Projects | +1.3% | Global, developed and emerging economies alike | Medium to Long-term (2025-2033) |

| Increasing Demand for High-Efficiency Industrial Motors | +1.1% | Global, particularly industrial and manufacturing sectors | Medium-term (2025-2030) |

| Technological Advancements in Production and Material Science | +0.9% | Global, R&D intensive regions | Long-term (2025-2033) |

Silicon Electrical Steel Market Challenges Impact Analysis

The silicon electrical steel market faces several significant challenges that could impede its growth trajectory and operational efficiency. One prominent challenge is the increasing cost of energy, a critical input for the highly energy-intensive production processes of electrical steel, including smelting, rolling, and annealing. Rising electricity and fuel prices directly translate to higher operational expenditures for manufacturers, squeezing profit margins and potentially leading to increased product prices, which can affect market competitiveness. Furthermore, the escalating cost of compliance with increasingly stringent environmental regulations, particularly concerning carbon emissions and waste disposal, requires substantial investments in pollution control technologies and sustainable practices. While necessary, these investments add to the financial burden on manufacturers and can make it harder to expand or modernize facilities.

Another key challenge is managing the complex and often volatile global supply chain for raw materials, especially for specialized alloying elements and high-purity silicon. Geopolitical tensions, trade protectionism, and logistical disruptions can lead to supply shortages or price spikes, making it difficult for manufacturers to secure consistent and cost-effective inputs. This supply chain fragility can impact production schedules and overall market stability. Additionally, the market faces the challenge of developing and scaling advanced grades of electrical steel, particularly those required for high-frequency applications in EVs and renewable energy systems, which demand sophisticated manufacturing capabilities and rigorous quality control. Achieving the necessary precision and efficiency for these next-generation materials while maintaining cost-effectiveness remains a significant hurdle. Lastly, intense competition from established players and the risk of overcapacity in certain segments can exert downward pressure on prices, affecting profitability and market share, especially in regions with fragmented manufacturing landscapes.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Escalating Energy Costs for Production | -0.8% | Global, particularly Europe and energy-intensive manufacturing regions | Short to Medium-term (2025-2028) |

| Stringent Quality Requirements for Advanced Applications | -0.7% | Global, impacting high-tech manufacturing regions | Long-term (2025-2033) |

| Supply Chain Disruptions and Raw Material Availability | -0.6% | Global, affecting trade flows and raw material sourcing | Short to Medium-term (2025-2028) |

| Intense Competition and Potential Overcapacity | -0.5% | Asia Pacific (especially China), Europe | Medium-term (2025-2030) |

| Technological Obsolescence and Need for Continuous Innovation | -0.4% | Global, R&D leaders | Long-term (2028-2033) |

Silicon Electrical Steel Market - Updated Report Scope

The updated report on the Silicon Electrical Steel Market offers an exhaustive analysis, providing critical insights into market dynamics, segmentation, and future growth trajectories. This comprehensive study covers historical trends, current market performance, and detailed projections, enabling stakeholders to make informed strategic decisions. It meticulously examines the forces shaping the market, including key drivers, restraints, opportunities, and challenges, along with their quantified impact on the market's Compound Annual Growth Rate (CAGR). The report also delves into the competitive landscape, profiling key industry players and their strategies, while providing a thorough regional breakdown to highlight significant growth areas and market concentrations. With a focus on granular data and actionable intelligence, this report serves as an invaluable resource for manufacturers, suppliers, investors, and end-use industries navigating the complexities of the global silicon electrical steel sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 21.5 Billion |

| Market Forecast in 2033 | USD 35.8 Billion |

| Growth Rate | 6.5% CAGR from 2025 to 2033 |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | ArcelorMittal, POSCO, Nippon Steel Corporation, JFE Steel Corporation, thyssenkrupp AG, Allegheny Technologies Incorporated, United States Steel Corporation, Ansteel Group Corporation, Baowu Steel Group, Shougang Group, Benxi Iron and Steel Group, HBIS Group, CSC (China Steel Corporation), Hyundai Steel Company, Acerinox S.A., Aperam S.A., AK Steel Corporation, Voestalpine AG, Nucor Corporation, Tata Steel Limited |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The silicon electrical steel market is meticulously segmented to provide a granular understanding of its diverse components and their respective contributions to overall market dynamics. This comprehensive segmentation allows for a detailed analysis of key product types, their myriad applications across various industries, and the distinct requirements of different end-use sectors, enabling stakeholders to identify specific growth avenues and tailor strategies accordingly. The market's structural breakdown helps in understanding demand patterns, technological preferences, and regional consumption trends, providing a holistic view of the market landscape.

- By Type: This segment differentiates the market based on the crystalline structure and processing methods of electrical steel, profoundly impacting its magnetic properties and suitability for specific applications.

- Grain-Oriented Electrical Steel (GOES): Characterized by its highly anisotropic magnetic properties, GOES is primarily used in the cores of large power and distribution transformers where minimizing core losses in the direction of rolling is crucial for efficiency. Its superior magnetic performance makes it indispensable for high-voltage transmission systems.

- Non-Grain Oriented Electrical Steel (NGOES): Exhibiting isotropic magnetic properties, NGOES is preferred for applications where magnetic flux flows in multiple directions.

- Fully Processed NGOES: Supplied in a final annealed condition, ready for use, and typically employed in motors, generators, and smaller transformers requiring uniform magnetic properties.

- Semi-Processed NGOES: Requires further annealing by the end-user to achieve its final magnetic properties, offering flexibility for specific fabrication needs, often used in less stringent applications or where in-house processing is preferred.

- By Application: This segmentation highlights the diverse end-uses where silicon electrical steel's magnetic properties are leveraged for efficient electrical energy conversion and transmission.

- Transformers: The largest application segment, encompassing devices that transfer electrical energy between circuits.

- Power Transformers: Large, high-voltage transformers used in power generation and transmission networks, heavily relying on GOES for efficiency.

- Distribution Transformers: Used in local grids to step down voltage for commercial and residential use, utilizing both GOES and high-grade NGOES.

- Specialty Transformers: Includes instrument transformers, auto transformers, and other custom designs for specific industrial or electronic applications.

- Motors: Devices converting electrical energy into mechanical energy, where NGOES is critical for core efficiency.

- Industrial Motors: Used in a wide range of manufacturing, processing, and machinery applications, demanding robust and efficient electrical steel.

- Automotive Motors (EV/HEV): A rapidly growing segment, requiring advanced, high-performance NGOES for traction motors in electric and hybrid vehicles due to high frequency and temperature demands.

- Consumer Motors: Found in household appliances, tools, and smaller electronic devices.

- Generators: Equipment that converts mechanical energy into electrical energy, often employing NGOES for efficient power generation.

- Inductors: Passive electronic components used for storing energy in a magnetic field, utilizing smaller quantities of electrical steel.

- Other Electrical Equipment: Includes various other devices like ballasts, relays, and magnetic shielding.

- Transformers: The largest application segment, encompassing devices that transfer electrical energy between circuits.

- By End-Use Industry: This segment categorizes demand based on the primary industry consuming silicon electrical steel, reflecting sector-specific trends and growth drivers.

- Energy & Power: Encompasses power generation, transmission, and distribution sectors, including utilities, renewable energy producers, and grid infrastructure developers, which are major consumers of electrical steel for transformers and generators.

- Automotive: Driven by the increasing production of electric vehicles (EVs) and hybrid electric vehicles (HEVs), which critically depend on high-performance electrical steel for their motors and charging components.

- Manufacturing & Industrial: Includes various industrial machinery, automation, and manufacturing processes that utilize motors, industrial transformers, and other electrical equipment.

- Consumer Electronics: Incorporates applications in household appliances, consumer gadgets, and small electronic devices that require efficient miniature motors and power components.

- Others: Covers niche applications in sectors such as aerospace and defense (e.g., specialized aircraft motors, radar systems), medical equipment (e.g., MRI machines), and telecommunications infrastructure.

- By Region: This segmentation provides a geographical breakdown of market size, growth rates, and key market trends across different continents and major countries, offering insights into regional market dynamics and investment opportunities.

Regional Highlights

The global silicon electrical steel market exhibits distinct regional dynamics, with certain geographies emerging as pivotal growth centers due to a combination of industrial development, policy support, and technological advancement. These regional highlights underscore the varying drivers and investment opportunities present across the world.

- Asia Pacific (APAC): This region consistently dominates the silicon electrical steel market, primarily driven by rapid industrialization, extensive urbanization, and massive investments in infrastructure development, particularly in China and India. China, as the world's largest producer and consumer of electrical steel, benefits from its vast manufacturing base in power equipment, automotive, and electronics. India's burgeoning energy demand, coupled with ambitious renewable energy targets and smart grid initiatives, fuels significant consumption. Southeast Asian countries are also contributing to growth through expanding industrial sectors and electrification projects. The region's robust growth in electric vehicle production further solidifies its leading position, demanding high volumes of advanced electrical steel grades.

- Europe: Europe represents a mature but technologically advanced market for silicon electrical steel, characterized by stringent energy efficiency regulations and a strong focus on renewable energy integration. Countries like Germany, France, and the UK are major consumers due to their advanced manufacturing industries, extensive power transmission networks, and a significant push towards electric mobility. The region's emphasis on circular economy principles and sustainable production practices also drives demand for high-quality, efficient electrical steel solutions. Investments in offshore wind power and grid modernization projects are key drivers in this region.

- North America: The North American market, led by the United States, demonstrates steady demand for silicon electrical steel, largely propelled by ongoing investments in grid infrastructure upgrades, renewable energy expansion, and the accelerating transition to electric vehicles. The emphasis on energy independence and resilience, coupled with federal incentives for clean energy technologies and EV adoption, boosts the consumption of high-efficiency electrical steel in transformers, motors, and charging infrastructure. Canada and Mexico also contribute to regional demand through industrial growth and cross-border energy projects.

- Latin America: This region is experiencing gradual growth in the silicon electrical steel market, supported by expanding industrial sectors, increasing electrification rates, and investments in renewable energy, particularly hydropower and solar. Brazil and Mexico are key markets, driven by their manufacturing bases and efforts to modernize aging power grids. The growth in automotive production and consumer electronics further contributes to the demand for electrical steel, albeit at a slower pace compared to leading Asian economies.

- Middle East & Africa (MEA): The MEA region is an emerging market for silicon electrical steel, primarily influenced by large-scale infrastructure projects, rapid urbanization, and significant investments in power generation and transmission capacity, including both conventional and renewable sources. Countries in the Gulf Cooperation Council (GCC) are focusing on diversifying their economies away from oil, leading to industrial development and smart city initiatives that require substantial electrical infrastructure. Sub-Saharan Africa's ongoing electrification efforts and industrial expansion also present long-term growth opportunities for the electrical steel market.

Top Key Players:

The market research report covers the analysis of key stake holders of the Silicon Electrical Steel Market. Some of the leading players profiled in the report include -

- ArcelorMittal

- POSCO

- Nippon Steel Corporation

- JFE Steel Corporation

- thyssenkrupp AG

- Allegheny Technologies Incorporated

- United States Steel Corporation

- Ansteel Group Corporation

- Baowu Steel Group

- Shougang Group

- Benxi Iron and Steel Group

- HBIS Group

- CSC (China Steel Corporation)

- Hyundai Steel Company

- Acerinox S.A.

- Aperam S.A.

- AK Steel Corporation

- Voestalpine AG

- Nucor Corporation

- Tata Steel Limited

Frequently Asked Questions:

What is silicon electrical steel used for?

Silicon electrical steel, also known as electrical steel or silicon steel, is primarily used as core material in electrical equipment due to its excellent magnetic properties, especially low core loss and high permeability. Its main applications include transformers (for power transmission and distribution), electric motors (in industrial machinery, home appliances, and electric vehicles), generators, and various electromagnetic devices like inductors and relays. It is crucial for efficient energy conversion and minimizing energy waste in electrical systems.

What is the difference between GOES and NGOES?

GOES stands for Grain-Oriented Electrical Steel, while NGOES stands for Non-Grain Oriented Electrical Steel. The key difference lies in their crystalline structure and magnetic properties. GOES has a highly organized crystal structure oriented in a specific direction (rolling direction), making it ideal for applications like power transformers where magnetic flux primarily travels in one direction, offering very low core losses in that specific direction. NGOES has a more random crystal orientation, resulting in uniform or isotropic magnetic properties in all directions, making it suitable for applications like motors and generators where magnetic flux rotates or travels in multiple directions.

What factors are driving the growth of the silicon electrical steel market?

The silicon electrical steel market is primarily driven by the increasing global focus on energy efficiency and decarbonization, leading to demand for high-performance electrical equipment. The rapid expansion of the electric vehicle (EV) industry, requiring advanced electrical steel for efficient motors, is a significant growth catalyst. Furthermore, massive investments in renewable energy infrastructure (wind, solar) and ongoing modernization of power grids globally are continually fueling the demand for electrical steel in transformers and generators.

What are the key challenges facing the silicon electrical steel market?

The silicon electrical steel market faces several challenges, including the volatility of raw material prices (steel, silicon), which impacts production costs and profitability. High capital investments required for manufacturing and compliance with increasingly stringent environmental regulations also pose significant hurdles. Additionally, potential supply chain disruptions due to geopolitical tensions and the need for continuous technological innovation to meet evolving performance demands for advanced applications are persistent challenges for market players.

Which region holds the largest share in the silicon electrical steel market?

Asia Pacific (APAC) holds the largest share in the global silicon electrical steel market. This dominance is attributed to rapid industrialization, extensive infrastructure development, and substantial investments in power generation and distribution networks, particularly in economies like China and India. The region's robust manufacturing sector, including a booming electric vehicle industry and significant expansion of renewable energy projects, further solidifies its leading position in both production and consumption of silicon electrical steel.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted