Canned Pet Food Market

Canned Pet Food Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_707221 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

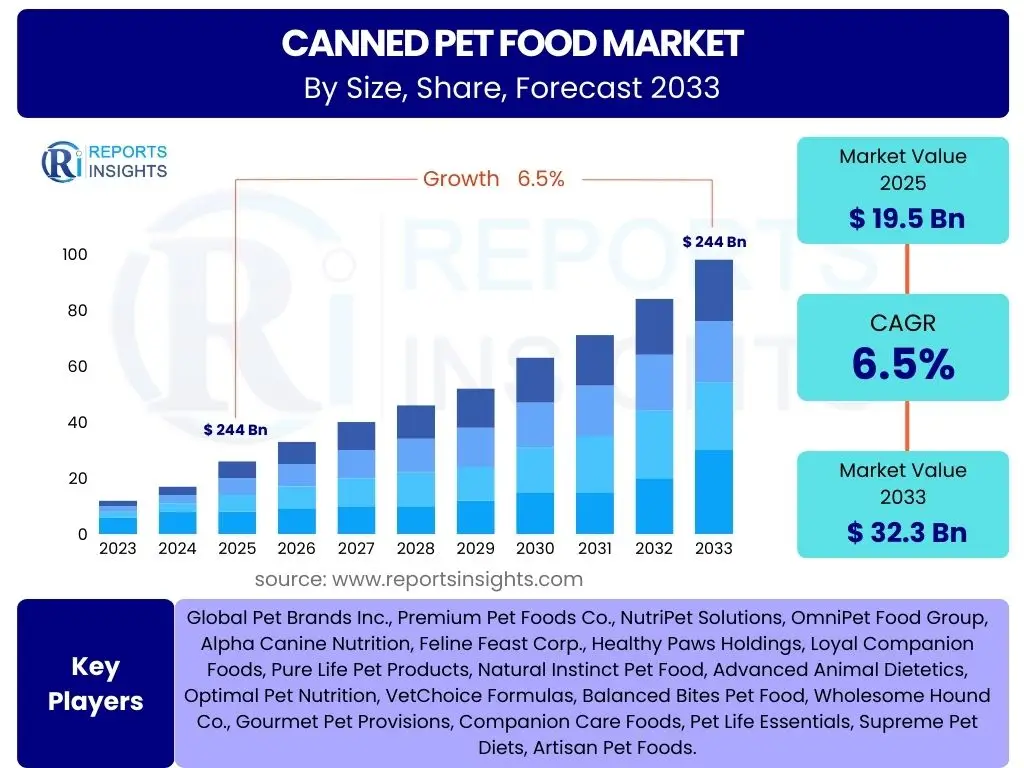

Canned Pet Food Market Size

According to Reports Insights Consulting Pvt Ltd, The Canned Pet Food Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2025 and 2033. The market is estimated at USD 19.5 Billion in 2025 and is projected to reach USD 32.3 Billion by the end of the forecast period in 2033.

Key Canned Pet Food Market Trends & Insights

The canned pet food market is currently shaped by several significant trends reflecting evolving consumer preferences and industry innovations. A primary driver is the increasing humanization of pets, where owners treat their animals as integral family members, leading to a demand for high-quality, nutritious, and ethically sourced food options. This trend fuels premiumization, with consumers willing to pay more for products that offer specific health benefits, natural ingredients, and superior palatability. The focus on pet health and wellness, encompassing digestive health, weight management, and age-specific nutrition, also significantly influences product development and marketing strategies within this sector.

Furthermore, the convenience and extended shelf-life offered by canned pet food continue to appeal to busy pet owners. Innovations in packaging, such as recyclable materials and easier-to-open designs, are gaining traction, addressing environmental concerns and enhancing user experience. The rise of e-commerce platforms has profoundly impacted distribution, making a wider variety of specialized canned pet food brands accessible to a global consumer base. Additionally, the incorporation of novel protein sources and limited ingredient diets addresses dietary sensitivities and provides more diverse options for pets with specific needs, contributing to the market's dynamic growth.

- Humanization of pets driving demand for premium and specialized nutrition.

- Focus on health and wellness, including functional ingredients and tailored formulations.

- Growing popularity of natural, organic, and limited ingredient diets.

- Increased adoption of sustainable and eco-friendly packaging solutions.

- Significant growth in online retail channels for pet food distribution.

- Demand for novel and alternative protein sources (e.g., insect protein, plant-based).

- Emphasis on palatability and flavor variety to entice picky eaters.

AI Impact Analysis on Canned Pet Food

Artificial intelligence is poised to significantly transform various facets of the canned pet food industry, from product development and manufacturing to supply chain management and consumer engagement. AI-powered analytics can process vast amounts of data related to pet health, dietary needs, ingredient efficacy, and market trends, enabling companies to formulate more precise and effective pet food recipes. This includes predicting ingredient interactions, optimizing nutrient profiles for specific breeds or health conditions, and accelerating the research and development cycle for new products. Furthermore, AI can enhance quality control processes on production lines by detecting anomalies and ensuring consistent product quality, minimizing waste and improving efficiency.

In the supply chain, AI algorithms can optimize inventory management, forecast demand with greater accuracy, and streamline logistics, reducing lead times and operational costs. This leads to more efficient sourcing of raw materials and timely delivery of finished products to retailers and consumers. On the consumer front, AI-driven chatbots and recommendation engines can provide personalized dietary advice, assist with product selection, and enhance customer service, thereby improving brand loyalty and satisfaction. Predictive maintenance for manufacturing equipment, enabled by AI, also contributes to reduced downtime and increased production capacity, indicating a holistic impact across the value chain of canned pet food.

- AI-driven personalized nutrition recommendations for pets.

- Enhanced supply chain optimization and demand forecasting using AI analytics.

- Automated quality control and defect detection in manufacturing.

- Accelerated research and development for new ingredient combinations and formulations.

- Improved customer service and engagement through AI-powered chatbots.

- Optimized inventory management and logistics for distribution.

- Predictive maintenance for production equipment, increasing operational efficiency.

Key Takeaways Canned Pet Food Market Size & Forecast

The Canned Pet Food market is on a robust growth trajectory, driven primarily by the global trend of pet humanization and increasing consumer awareness regarding pet nutrition. The substantial projected CAGR indicates a sustained expansion, underpinned by innovations in product formulations, an emphasis on premium ingredients, and the convenience offered by canned formats. This growth is not merely volumetric but also reflects a shift towards higher-value segments as pet owners prioritize the health and well-being of their companions, leading to a willingness to invest in specialized and fortified options. The market's resilience is further supported by diversified distribution channels, with e-commerce playing an increasingly pivotal role in accessibility.

Future growth will be significantly influenced by continuous product innovation, particularly in areas like sustainable sourcing, novel proteins, and functional benefits tailored for specific life stages or health concerns. The market is expected to see a greater penetration in emerging economies as pet ownership rises alongside disposable incomes. Strategic partnerships, mergers, and acquisitions among key players are anticipated to consolidate market share and foster innovation, while addressing challenges such as raw material costs and packaging sustainability will be crucial for long-term success. Overall, the market is poised for significant expansion, offering ample opportunities for both established brands and new entrants focused on quality, convenience, and specialized nutrition.

- The market exhibits strong growth potential, driven by pet humanization and premiumization trends.

- Significant revenue opportunities exist in emerging economies due to increasing pet ownership.

- Innovation in ingredients, formulations, and sustainable packaging is crucial for competitive advantage.

- E-commerce platforms are becoming increasingly vital distribution channels, expanding market reach.

- Focus on health-specific and age-specific formulations will be key growth drivers.

- Challenges related to raw material volatility and environmental impact of packaging require strategic solutions.

Canned Pet Food Market Drivers Analysis

The increasing trend of pet humanization globally is a primary driver for the canned pet food market. As pets are increasingly considered family members, owners are more inclined to provide high-quality, nutritious food that mirrors human dietary standards. This drives demand for premium, natural, and specialized canned pet food products, focusing on ingredients, palatability, and health benefits, thereby positively impacting market growth and product innovation. This cultural shift translates directly into greater expenditure on pet welfare.

Another significant driver is the rising awareness among pet owners regarding the importance of proper nutrition for their pets' health and longevity. Educational campaigns, veterinary recommendations, and readily available information online have highlighted the benefits of nutrient-dense, moisture-rich diets, which canned pet food typically provides. This heightened awareness leads to informed purchasing decisions, where pet owners prioritize balanced diets that can address specific health issues or support overall well-being, consequently boosting the adoption of canned pet food products across various demographic segments.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Pet Humanization and Premiumization | +1.8% | North America, Europe, Asia Pacific (Tier 1 cities) | Short to Medium Term (2025-2029) |

| Rising Awareness of Pet Health and Nutrition | +1.5% | Global | Medium Term (2026-2031) |

| Convenience and Extended Shelf-Life of Canned Food | +1.2% | Global | Short to Medium Term (2025-2030) |

| Growth of E-commerce and Online Pet Food Sales | +1.0% | Global, especially urban areas | Short to Long Term (2025-2033) |

Canned Pet Food Market Restraints Analysis

The relatively higher cost of canned pet food compared to dry kibble acts as a significant restraint, particularly in price-sensitive markets or among consumers with multiple pets. While premiumization is a trend, a large segment of pet owners remains budget-conscious, making the per-serving cost of canned food a deterrent. This economic factor can limit market penetration and growth, especially when consumers seek to optimize expenses without compromising on basic nutritional needs, often leading them towards more economical dry food alternatives or a mix-feeding approach.

Concerns related to packaging waste and the environmental impact of metal cans also pose a restraint. As consumer awareness about sustainability increases, there is a growing demand for eco-friendly packaging solutions. Despite the recyclability of metal cans, the perception of their environmental footprint compared to less resource-intensive packaging options for dry food can influence purchasing decisions. This pressure necessitates ongoing innovation in sustainable packaging materials and recycling infrastructure to mitigate environmental concerns and maintain consumer appeal.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Higher Cost Compared to Dry Pet Food | -0.8% | Emerging Markets, Price-Sensitive Demographics | Short to Medium Term (2025-2030) |

| Perceived Lack of Freshness vs. Raw/Fresh Options | -0.5% | North America, Europe (urban, affluent areas) | Medium Term (2027-2032) |

| Environmental Concerns over Packaging Waste | -0.4% | Europe, North America | Medium to Long Term (2026-2033) |

Canned Pet Food Market Opportunities Analysis

The expanding market for specialized and therapeutic canned pet food presents a significant opportunity. As pets age or develop specific health conditions like kidney disease, allergies, or digestive issues, veterinarians often recommend prescription diets, which are frequently available in canned formulations due to their higher moisture content and palatability. This niche segment allows manufacturers to command premium prices and caters to a growing demand for tailored nutritional solutions, aligning with the humanization trend where pet owners seek advanced care for their companions. Investing in R&D for condition-specific formulas can unlock considerable growth.

Growth in emerging economies, particularly in Asia Pacific and Latin America, represents another substantial opportunity. Rising disposable incomes, increasing urbanization, and a growing middle-class population in these regions are leading to higher rates of pet adoption and a greater willingness to spend on quality pet food. As pet ownership transitions from functional to companionship roles in these areas, the demand for convenient and nutritious canned pet food is expected to surge, providing a fertile ground for market expansion and new market entry strategies for international brands.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion in Emerging Economies (Asia Pacific, Latin America) | +1.5% | Asia Pacific, Latin America | Medium to Long Term (2026-2033) |

| Development of Specialized and Therapeutic Canned Formulations | +1.3% | Global, particularly developed markets | Short to Medium Term (2025-2030) |

| Innovation in Sustainable and Eco-friendly Packaging | +1.1% | North America, Europe | Medium Term (2027-2032) |

| Growth of Direct-to-Consumer (D2C) Sales Models | +0.9% | Global | Short to Medium Term (2025-2030) |

Canned Pet Food Market Challenges Impact Analysis

Volatility in raw material prices poses a significant challenge for canned pet food manufacturers. Ingredients such as meat proteins, grains, and specialty additives are subject to fluctuations driven by agricultural conditions, global supply chain disruptions, and geopolitical factors. These price instabilities directly impact production costs, potentially eroding profit margins or necessitating price increases, which can deter consumers and impact market competitiveness. Managing these fluctuations requires robust supply chain management and strategic hedging by manufacturers to maintain stable pricing and product availability.

Intense competition within the broader pet food industry, not just from other canned brands but also from rapidly growing segments like fresh, frozen, and raw pet food, presents another substantial challenge. As consumer preferences diversify, traditional canned pet food brands face pressure to innovate and differentiate their offerings to retain market share. This competitive landscape demands continuous investment in research and development, marketing, and distribution to stand out amidst a plethora of choices and evolving consumer demands, pushing companies to adapt quickly to new trends and dietary philosophies.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Raw Material Price Volatility and Supply Chain Disruptions | -0.7% | Global | Short Term (2025-2027) |

| Intense Competition from Other Pet Food Formats (Dry, Fresh, Raw) | -0.6% | Developed Markets | Medium to Long Term (2026-2033) |

| Adherence to Stringent Regulatory Standards | -0.3% | North America, Europe | Ongoing |

Canned Pet Food Market - Updated Report Scope

This report provides a comprehensive analysis of the Canned Pet Food Market, offering in-depth insights into market size, growth drivers, restraints, opportunities, and challenges. It covers detailed segmentation analysis across various categories and provides regional breakdowns, offering a holistic view of the market's current state and future trajectory. The report also highlights the competitive landscape by profiling key market players and addressing frequently asked questions to provide actionable intelligence for stakeholders.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 19.5 Billion |

| Market Forecast in 2033 | USD 32.3 Billion |

| Growth Rate | 6.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Pet Brands Inc., Premium Pet Foods Co., NutriPet Solutions, OmniPet Food Group, Alpha Canine Nutrition, Feline Feast Corp., Healthy Paws Holdings, Loyal Companion Foods, Pure Life Pet Products, Natural Instinct Pet Food, Advanced Animal Dietetics, Optimal Pet Nutrition, VetChoice Formulas, Balanced Bites Pet Food, Wholesome Hound Co., Gourmet Pet Provisions, Companion Care Foods, Pet Life Essentials, Supreme Pet Diets, Artisan Pet Foods. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Canned Pet Food Market is segmented across several key dimensions, including pet type, ingredient composition, distribution channels, and packaging types. This granular segmentation provides a detailed understanding of market dynamics and consumer preferences within each category, allowing manufacturers and marketers to tailor their strategies effectively. Each segment contributes uniquely to the market's overall growth, reflecting diverse needs and purchasing behaviors across the global pet owner base. Analyzing these segments helps in identifying niche opportunities and understanding competitive landscapes, fostering informed decision-making for product development and market entry.

Segmentation by pet type, primarily dogs and cats, reveals distinct dietary requirements and market sizes for each. Ingredient-based segmentation highlights consumer demand for specific protein sources, natural components, and functional additives, influencing product formulation trends. The distribution channel breakdown underscores the increasing importance of online retail alongside traditional brick-and-mortar stores. Lastly, segmentation by packaging type indicates preferences for specific can materials, which often relates to factors like shelf-life, recyclability, and perceived convenience, all vital for understanding the comprehensive market structure and anticipating future shifts in demand.

- By Pet Type:

- Dogs

- Cats

- Other (Birds, Small Mammals, etc.)

- By Ingredient:

- Meat (Poultry, Beef, Pork, Fish)

- Vegetables & Fruits

- Grains

- Others (Vitamins, Minerals)

- By Distribution Channel:

- Supermarkets & Hypermarkets

- Pet Specialty Stores

- Online Retail

- Other Channels (Veterinary Clinics, etc.)

- By Packaging Type:

- Steel Cans

- Aluminum Cans

Regional Highlights

North America currently holds a significant share in the Canned Pet Food Market, driven by high rates of pet ownership, strong pet humanization trends, and substantial disposable incomes allowing for premium product purchases. The region benefits from a well-established pet care industry, extensive retail infrastructure including specialized pet stores, and a robust e-commerce penetration. Consumers in North America are highly aware of pet nutrition and seek specialized diets, which drives innovation and premium product offerings in the canned food segment, maintaining the region's leading position.

Europe also represents a mature and substantial market for canned pet food, with countries like Germany, the UK, and France showing strong demand for high-quality, natural, and sustainably sourced products. The region's stringent regulatory standards for pet food quality and safety further contribute to consumer trust and premiumization. Meanwhile, the Asia Pacific region, particularly China, Japan, and India, is emerging as a rapidly growing market. This growth is fueled by increasing pet adoption rates, rising disposable incomes, urbanization, and a growing Western influence on pet care practices, leading to a surge in demand for convenient and nutritious pet food options, including canned varieties. Latin America and the Middle East & Africa regions are also exhibiting nascent but growing potential as pet ownership and awareness of commercial pet food benefits increase.

- North America: Dominant market share due to high pet ownership, pet humanization, and demand for premium products.

- Europe: Strong market driven by focus on natural ingredients, stringent regulations, and high consumer spending on pet welfare.

- Asia Pacific: Fastest growing region, propelled by increasing disposable incomes, urbanization, and rising pet adoption rates in countries like China and India.

- Latin America: Growing market influenced by increasing pet humanization and awareness of commercial pet food benefits.

- Middle East and Africa: Nascent but expanding market, showing potential for growth with increasing modernization and pet ownership.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Canned Pet Food Market.- Global Pet Brands Inc.

- Premium Pet Foods Co.

- NutriPet Solutions

- OmniPet Food Group

- Alpha Canine Nutrition

- Feline Feast Corp.

- Healthy Paws Holdings

- Loyal Companion Foods

- Pure Life Pet Products

- Natural Instinct Pet Food

- Advanced Animal Dietetics

- Optimal Pet Nutrition

- VetChoice Formulas

- Balanced Bites Pet Food

- Wholesome Hound Co.

- Gourmet Pet Provisions

- Companion Care Foods

- Pet Life Essentials

- Supreme Pet Diets

- Artisan Pet Foods

Frequently Asked Questions

What is the projected growth rate for the Canned Pet Food Market?

The Canned Pet Food Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2025 and 2033, indicating a robust and sustained expansion over the forecast period.

What are the primary factors driving the Canned Pet Food Market?

Key drivers include the increasing humanization of pets leading to demand for premium products, rising awareness among pet owners about optimal pet nutrition, and the inherent convenience and long shelf-life offered by canned pet food. The growth of e-commerce also significantly contributes to market expansion.

How does AI impact the Canned Pet Food industry?

AI significantly impacts the industry by enabling personalized nutrition formulation, optimizing supply chain and demand forecasting, enhancing quality control in manufacturing, and improving customer engagement through AI-powered recommendation systems and chatbots.

Which regions are key contributors to the Canned Pet Food Market?

North America and Europe currently represent significant market shares due to high pet ownership and premium product demand. The Asia Pacific region is rapidly emerging as a high-growth market, driven by increasing disposable incomes and pet adoption rates in countries like China and India.

What are the main challenges facing the Canned Pet Food Market?

Major challenges include volatility in raw material prices impacting production costs, intense competition from other pet food formats such as dry, fresh, and raw food, and the need to adhere to stringent regulatory standards globally. Addressing environmental concerns related to packaging waste is also an ongoing challenge.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted