The Food Industry Metal Detector Market

The Food Industry Metal Detector Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_707333 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

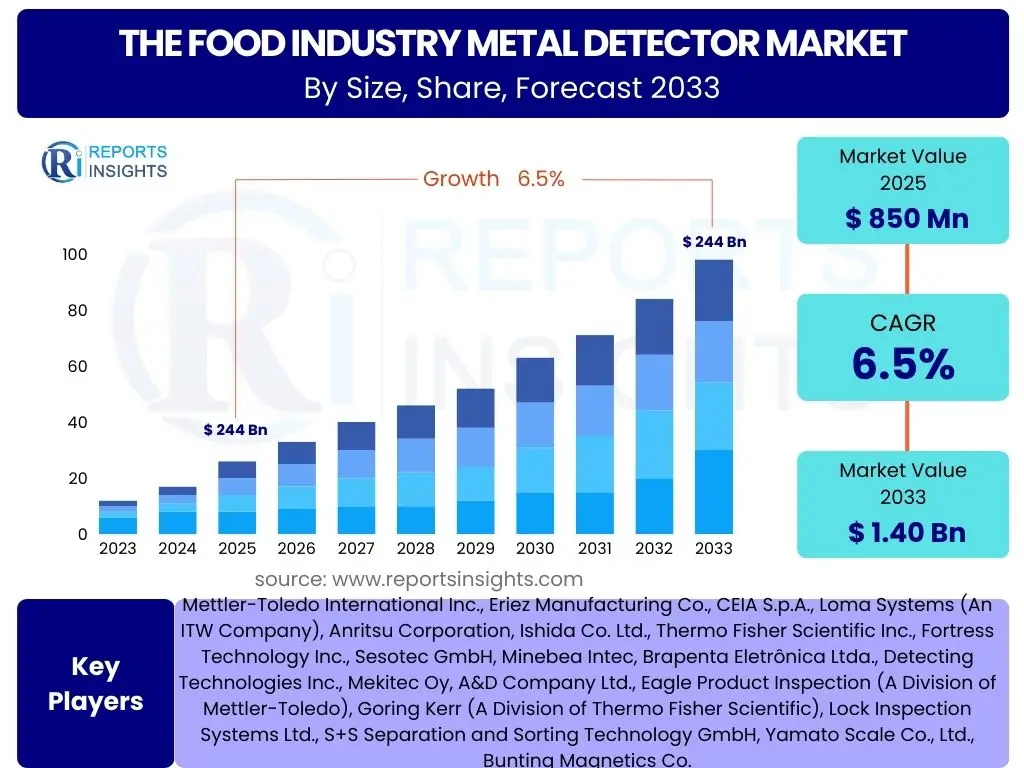

The Food Industry Metal Detector Market Size

According to Reports Insights Consulting Pvt Ltd, The Food Industry Metal Detector Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2025 and 2033. The market is estimated at USD 850 million in 2025 and is projected to reach USD 1.40 billion by the end of the forecast period in 2033. This steady growth is primarily attributed to stringent global food safety regulations, increasing consumer awareness regarding food quality, and the continuous expansion of the processed food industry worldwide. The imperative to prevent contamination and ensure product integrity across the food supply chain is a fundamental driver shaping market expansion.

Key The Food Industry Metal Detector Market Trends & Insights

Common user questions regarding trends in the Food Industry Metal Detector market often revolve around technological advancements, the adoption of Industry 4.0 concepts, and evolving regulatory landscapes. Users are keen to understand how manufacturers are addressing challenges such as product effect, enhancing detection sensitivity for smaller contaminants, and integrating inspection systems seamlessly into high-speed production lines. There is also significant interest in solutions that reduce false rejects and improve overall operational efficiency, signaling a shift towards more intelligent and automated inspection processes.

The market is currently witnessing a pronounced trend towards the development of highly sensitive and intelligent metal detection systems capable of identifying minute contaminants even within complex product matrices. Manufacturers are focusing on incorporating advanced digital signal processing (DSP) technologies and multi-frequency operations to mitigate product effect and enhance detection accuracy. Furthermore, the integration of these systems with broader factory automation frameworks, including SCADA and MES, is becoming a standard expectation, enabling real-time data analysis and centralized control. This push for connectivity supports predictive maintenance and overall equipment effectiveness (OEE) initiatives within food processing plants.

- Increased demand for higher sensitivity and accuracy in detection, even for non-magnetic stainless steel.

- Rising adoption of multi-frequency metal detectors to minimize product effect and false rejections.

- Integration of metal detection systems with Industry 4.0 technologies, including IoT, cloud connectivity, and data analytics platforms.

- Emphasis on hygienic design and washdown capabilities to meet stringent sanitation requirements in food processing environments.

- Growing preference for user-friendly interfaces and automated setup processes to reduce operator intervention and training needs.

- Development of combination systems that integrate metal detection with checkweighing or X-ray inspection for comprehensive quality control.

AI Impact Analysis on The Food Industry Metal Detector

User inquiries concerning the impact of Artificial Intelligence (AI) on Food Industry Metal Detectors frequently explore its potential to enhance detection precision, reduce operational errors, and automate decision-making processes. Key themes include how AI can differentiate between actual metallic contaminants and benign product variations, thereby minimizing costly false positives. There is considerable expectation that AI will streamline maintenance, improve system calibration, and provide deeper insights into contamination patterns, moving beyond simple detection to predictive analysis.

AI's influence on metal detection systems is transformative, enabling a paradigm shift from reactive error identification to proactive quality assurance. By leveraging machine learning algorithms, AI-powered detectors can analyze vast datasets of product characteristics and environmental factors, learning to distinguish between genuine contaminants and benign anomalies with unprecedented accuracy. This capability significantly reduces false rejects, optimizes throughput, and minimizes product waste, leading to substantial cost savings for food manufacturers. Moreover, AI facilitates predictive maintenance by monitoring system performance in real-time, anticipating potential failures, and scheduling maintenance proactively, thereby maximizing uptime and operational efficiency.

Beyond detection accuracy, AI is poised to revolutionize data interpretation and process optimization. It can identify subtle trends in contamination occurrences, trace potential sources, and recommend adjustments to upstream processes to prevent future incidents. The integration of AI also promises more intuitive user interfaces, self-optimizing calibration routines, and enhanced diagnostic capabilities, making metal detection technology more accessible and effective for a wider range of users. This continuous learning and adaptation capability ensures that inspection systems remain highly effective even as product formulations or environmental conditions change.

- Enhanced detection accuracy and reduction of false positives through machine learning algorithms that differentiate between product effect and actual contaminants.

- Predictive maintenance capabilities, allowing systems to anticipate component failures and schedule servicing proactively.

- Automated calibration and sensitivity adjustments, optimizing performance without constant manual intervention.

- Data analysis and reporting improvements, providing deeper insights into contamination trends and operational efficiencies.

- Integration with advanced robotics and automation for seamless product handling and contaminant removal.

- Improved anomaly detection, learning from historical data to identify novel or complex contamination scenarios.

Key Takeaways The Food Industry Metal Detector Market Size & Forecast

Common user questions regarding key takeaways from the Food Industry Metal Detector market size and forecast often focus on identifying the primary growth drivers, understanding regional market dominance, and pinpointing emerging opportunities. Users are particularly interested in which sectors within the food industry will experience the most significant adoption, and how evolving regulatory landscapes will continue to shape market dynamics. Insights into the long-term sustainability and technological trajectory of the market are also frequently sought.

The Food Industry Metal Detector Market is poised for consistent growth, driven fundamentally by the escalating global emphasis on food safety and quality. Stringent regulations, such as those imposed by HACCP, GFSI, and national food agencies, mandate effective contamination prevention, making metal detection an indispensable component of food processing lines. This regulatory pressure, combined with increasing consumer demand for safe and high-quality food products, forms the bedrock of market expansion. Furthermore, the rapid growth of the processed and packaged food sector, particularly in developing economies, necessitates robust inspection systems to ensure product integrity at scale.

Technological innovation plays a pivotal role in the market's trajectory, with advancements in detection sensitivity, multi-frequency capabilities, and digital signal processing continuously enhancing system performance. The ongoing integration of smart technologies like IoT and AI is transforming metal detectors into intelligent data-gathering and decision-making tools, moving beyond simple contaminant detection to offer predictive insights and operational efficiencies. Regional dynamics show North America and Europe as mature markets driven by regulatory compliance and technological upgrades, while Asia Pacific emerges as a high-growth region propelled by industrialization, rising food production, and increasing awareness of food safety standards.

- The market's growth is predominantly fueled by stringent global food safety regulations and increasing consumer demand for product integrity.

- Technological advancements, including multi-frequency detection and digital signal processing, are enhancing system accuracy and reliability.

- Integration of Industry 4.0 principles, such as IoT and AI, is creating intelligent, networked inspection solutions.

- North America and Europe remain key markets due to robust regulatory frameworks, while Asia Pacific offers significant growth opportunities driven by expanding food processing sectors.

- The adoption of metal detectors is becoming critical across diverse food segments, from packaged goods to bulk and liquid applications.

The Food Industry Metal Detector Market Drivers Analysis

The Food Industry Metal Detector Market is significantly propelled by a confluence of critical factors that underscore the indispensable role of these systems in modern food production. Paramount among these drivers are the escalating global food safety regulations and the relentless pursuit of product quality, which compel manufacturers to implement advanced inspection technologies. Furthermore, the expansion of the processed and packaged food industry, particularly in emerging economies, coupled with increased automation in manufacturing, creates a fertile ground for market growth. These factors collectively emphasize the necessity for robust contaminant detection solutions to protect consumers and uphold brand reputation.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Strict Food Safety Regulations and Standards | +1.8% | Global (EU, US, China, India) | Short- to Long-Term |

| Rising Consumer Awareness Regarding Food Quality | +1.5% | Global (Developed and Emerging Markets) | Mid- to Long-Term |

| Growth of the Processed and Packaged Food Industry | +1.2% | Asia Pacific, Latin America, Africa | Short- to Mid-Term |

| Increasing Automation in Food Manufacturing Facilities | +1.0% | North America, Europe, Developed Asia Pacific | Mid-Term |

| Risk of Product Recalls and Brand Reputation Damage | +0.8% | Global | Short- to Mid-Term |

| Technological Advancements in Detection Capabilities | +0.7% | Global | Ongoing, Long-Term |

The Food Industry Metal Detector Market Restraints Analysis

Despite robust growth drivers, the Food Industry Metal Detector Market faces several significant restraints that could potentially impede its expansion. A primary limiting factor is the substantial initial capital investment required for purchasing and integrating advanced metal detection systems, which can be a barrier for small and medium-sized enterprises (SMEs). Furthermore, the complexity of maintaining and operating these sophisticated machines, coupled with the shortage of skilled personnel, presents operational challenges. The existence of alternative inspection technologies, such as X-ray systems, which offer broader contaminant detection capabilities, also introduces competitive pressure. Addressing these restraints through cost-effective solutions and enhanced user training will be crucial for sustained market growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Investment Cost for Advanced Systems | -0.9% | Global (particularly SMEs) | Short- to Mid-Term |

| Product Effect and False Reject Rates in Certain Applications | -0.7% | Global (specific product types) | Ongoing |

| Availability of Alternative Inspection Technologies (e.g., X-ray) | -0.6% | Global (highly sensitive applications) | Mid-Term |

| Lack of Skilled Operators and Maintenance Personnel | -0.5% | Emerging Markets | Short- to Mid-Term |

| Complexity of System Integration and Calibration | -0.4% | Global | Short-Term |

The Food Industry Metal Detector Market Opportunities Analysis

The Food Industry Metal Detector Market presents substantial opportunities for innovation and expansion, driven by evolving industry needs and technological advancements. A significant avenue for growth lies in the burgeoning demand from emerging markets, where food processing industries are rapidly industrializing and adopting international food safety standards. The increasing integration of metal detection systems with Industry 4.0 technologies, such as the Internet of Things (IoT) and artificial intelligence (AI), offers pathways for developing smarter, more efficient, and connected inspection solutions. Furthermore, the development of highly specialized detectors for challenging applications, such as liquid or frozen products, and the rising interest in rental or service-based models, represent lucrative prospects for market players to diversify their offerings and cater to a broader client base.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion in Emerging Markets (Asia Pacific, Latin America) | +1.5% | Asia Pacific, Latin America, Africa | Long-Term |

| Integration with Industry 4.0 and Smart Factory Initiatives | +1.3% | Global (Developed Markets Leading) | Mid- to Long-Term |

| Demand for Specialized Detectors for Challenging Products | +1.0% | Global (Specific Food Segments) | Mid-Term |

| Aftermarket Services and Maintenance Contracts Growth | +0.8% | Global | Short- to Long-Term |

| Focus on Sustainable and Energy-Efficient Detection Systems | +0.6% | Europe, North America | Long-Term |

The Food Industry Metal Detector Market Challenges Impact Analysis

While the Food Industry Metal Detector Market exhibits robust potential, it faces several intrinsic challenges that demand strategic responses from manufacturers and users alike. A significant hurdle is the persistent issue of product effect, where the inherent conductivity or moisture content of food products can mimic metallic signals, leading to false rejects and reduced throughput. Furthermore, the rapid pace of technological advancements, while an opportunity, also presents a challenge by demanding continuous innovation and significant R&D investment to stay competitive. Ensuring the seamless integration of new detection systems into existing complex production lines and mitigating the impact of global supply chain disruptions on component availability are also critical challenges that the industry must navigate for sustained growth and operational efficiency.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Managing Product Effect in Diverse Food Applications | -0.8% | Global | Ongoing |

| Technological Obsolescence and Need for Continuous R&D | -0.7% | Global | Long-Term |

| Supply Chain Volatility and Component Availability | -0.6% | Global | Short- to Mid-Term |

| Ensuring Compatibility and Integration with Existing Production Lines | -0.5% | Global (Retrofit Projects) | Short- to Mid-Term |

| Intense Competition and Pricing Pressures | -0.4% | Global | Ongoing |

The Food Industry Metal Detector Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of The Food Industry Metal Detector Market, offering a detailed understanding of its current size, historical performance, and future growth projections. It meticulously examines market dynamics, including key drivers, restraints, opportunities, and challenges that shape the industry landscape. The report also provides extensive segmentation analysis by type, application, end-user, and technology, alongside a thorough regional assessment to identify prominent market trends and investment opportunities. Additionally, it profiles leading market players, offering insights into their strategic initiatives and competitive positioning within the global market.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 850 million |

| Market Forecast in 2033 | USD 1.40 billion |

| Growth Rate | 6.5% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Mettler-Toledo International Inc., Eriez Manufacturing Co., CEIA S.p.A., Loma Systems (An ITW Company), Anritsu Corporation, Ishida Co. Ltd., Thermo Fisher Scientific Inc., Fortress Technology Inc., Sesotec GmbH, Minebea Intec, Brapenta Eletrônica Ltda., Detecting Technologies Inc., Mekitec Oy, A&D Company Ltd., Eagle Product Inspection (A Division of Mettler-Toledo), Goring Kerr (A Division of Thermo Fisher Scientific), Lock Inspection Systems Ltd., S+S Separation and Sorting Technology GmbH, Yamato Scale Co., Ltd., Bunting Magnetics Co. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Food Industry Metal Detector Market is meticulously segmented to provide a granular understanding of its diverse components and sub-markets. This segmentation allows for precise analysis of market dynamics, identifying specific growth areas, and understanding the varying requirements of different food processing applications and end-users. Key segments include classifications by the type of detector, the application area within food processing, the size and nature of the end-user facility, and the underlying detection technology employed. This multi-faceted approach ensures a comprehensive market overview, enabling stakeholders to pinpoint niche opportunities and tailor their strategies effectively.

Each segment exhibits unique characteristics and growth trajectories. For instance, conveyor-based metal detectors remain dominant due to their versatility across various packaged and bulk food products, while pipeline detectors are crucial for liquid and paste applications. The application segment highlights the diverse needs of sectors like meat and poultry, bakery, and dairy, each requiring specialized sensitivities and hygienic designs. Furthermore, the end-user segmentation differentiates between the scale of operations, revealing distinct market demands from large-scale industrial processors versus smaller, artisanal producers. Technological segmentation emphasizes the evolution from traditional balanced coil systems to advanced multi-frequency and digital signal processing units, which offer superior performance and adaptability to challenging product effects. Understanding these intricate segmentations is vital for effective market penetration and product development.

- By Type: This segment categorizes metal detectors based on their operational mechanism and installation type. It includes Conveyor-based Metal Detectors, widely used for packaged and bulk products; Gravity-fed Metal Detectors, essential for free-falling dry products; Pipeline Metal Detectors, designed for liquid, paste, and slurry applications; Pharmaceutical Metal Detectors, optimized for high sensitivity in pill and capsule inspection; Hand-held Metal Detectors, used for spot checks and quality control; and Tunnel Metal Detectors, offering robust detection for specific product shapes.

- By Application: This segmentation outlines the diverse food and beverage sectors where metal detectors are applied. Key applications include Packaged Food Products, Bulk Food Products, Liquid and Paste Food Products, Dairy and Cheese Products, Meat, Poultry, and Seafood, Bakery and Confectionery, Snacks and Cereals, Beverages, and specific Pharmaceutical applications such as food supplements and over-the-counter (OTC) products.

- By End-User: This segment categorizes consumers of metal detection equipment based on their operational scale and type. It primarily differentiates between Large Food Processing Facilities, which require high-throughput and integrated systems; Small and Medium-sized Food Processing Facilities, often seeking more cost-effective and compact solutions; and Catering and Food Service Providers, who may utilize simpler or hand-held devices for quality assurance.

- By Technology: This segment focuses on the underlying technological principles governing metal detection. It encompasses Balanced Coil Technology, a traditional and widely used method; Ferrous in Foil Technology, designed for products packaged in aluminum foil; Digital Signal Processing (DSP), which enhances sensitivity and reduces false rejects through advanced signal analysis; and Multi-frequency Technology, allowing detectors to operate at multiple frequencies simultaneously to mitigate product effect and improve detection across diverse products.

Regional Highlights

The global Food Industry Metal Detector Market exhibits distinct regional dynamics, influenced by varying regulatory environments, levels of industrialization, consumer preferences, and technological adoption rates. North America and Europe are established markets characterized by stringent food safety regulations, a mature processed food industry, and a high emphasis on automation and advanced inspection technologies. These regions typically lead in adopting multi-frequency and AI-integrated systems, driven by a continuous need for efficiency and compliance. The market here is also heavily influenced by continuous technological upgrades and replacement cycles.

Asia Pacific is emerging as the fastest-growing market, propelled by rapid urbanization, expanding middle-class populations, and the substantial growth of the processed and packaged food sector. Countries like China and India are witnessing significant investments in food processing infrastructure, leading to increased demand for robust and cost-effective metal detection solutions. While regulatory frameworks are evolving, the drive for export compliance and improving domestic food safety standards are key accelerators. Latin America and the Middle East and Africa (MEA) regions are also showing considerable growth potential, primarily driven by increasing food production capabilities, rising awareness of international food safety norms, and a growing demand for quality imported and domestically produced food items. These regions often seek foundational and mid-range solutions, with a growing interest in advanced systems as their food industries mature and integrate into global supply chains.

- North America: A mature market with high adoption rates due to strict FDA and USDA regulations. Emphasis on advanced, integrated systems and solutions that minimize false positives. United States and Canada are key contributors.

- Europe: Driven by comprehensive EU food safety directives and high consumer expectations. Focus on hygienic design, multi-frequency technology, and energy efficiency. Germany, UK, France, and Italy are significant markets.

- Asia Pacific (APAC): Fastest-growing region, fueled by expanding food processing industries, increasing population, and rising food safety awareness. China, India, Japan, and Australia are key markets, with demand for both basic and advanced systems.

- Latin America: Experiencing steady growth due to rising food production and processing capabilities. Brazil and Mexico are leading markets, driven by domestic consumption and export requirements.

- Middle East and Africa (MEA): Emerging market with increasing investments in food processing and a growing awareness of food safety standards. Saudi Arabia, UAE, and South Africa are key developing markets.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in The Food Industry Metal Detector Market.- Mettler-Toledo International Inc.

- Eriez Manufacturing Co.

- CEIA S.p.A.

- Loma Systems (An ITW Company)

- Anritsu Corporation

- Ishida Co. Ltd.

- Thermo Fisher Scientific Inc.

- Fortress Technology Inc.

- Sesotec GmbH

- Minebea Intec

- Brapenta Eletrônica Ltda.

- Detecting Technologies Inc.

- Mekitec Oy

- A&D Company Ltd.

- Eagle Product Inspection (A Division of Mettler-Toledo)

- Goring Kerr (A Division of Thermo Fisher Scientific)

- Lock Inspection Systems Ltd.

- S+S Separation and Sorting Technology GmbH

- Yamato Scale Co., Ltd.

- Bunting Magnetics Co.

Frequently Asked Questions

Analyze common user questions about the The Food Industry Metal Detector market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is a metal detector in the food industry?

A metal detector in the food industry is an electronic inspection system designed to detect and reject metallic contaminants (ferrous, non-ferrous, and stainless steel) from food products during processing. Its primary function is to ensure product safety, protect consumers from potential harm, and safeguard brand reputation by preventing the distribution of contaminated goods. These systems are crucial at various points in the production line, from raw material inspection to final product packaging, to comply with global food safety standards and regulations.

Why are metal detectors important in food processing?

Metal detectors are critically important in food processing because they serve as a final line of defense against physical contamination, which can occur from machinery wear and tear, foreign objects, or human error. They help food manufacturers comply with stringent international food safety regulations (like HACCP, FSMA, BRC, IFS), prevent costly product recalls, avoid potential legal liabilities, and protect consumer health. By ensuring products are free from metallic impurities, these systems safeguard brand integrity and maintain consumer trust in the quality and safety of food products.

What types of metal contaminants can food industry metal detectors detect?

Food industry metal detectors are engineered to detect all types of metals that could potentially contaminate food products. This includes ferrous metals (such as iron and steel), which are magnetic; non-ferrous metals (like aluminum, copper, and brass), which are non-magnetic but conductive; and challenging non-magnetic stainless steel, which requires higher sensitivity due to its low magnetic and conductive properties. Modern multi-frequency and digital signal processing technologies enhance the ability to detect even minute particles of these diverse metallic contaminants within various food matrices.

How do modern food industry metal detectors minimize false rejections?

Modern food industry metal detectors minimize false rejections primarily through advanced technologies such as multi-frequency operation and sophisticated Digital Signal Processing (DSP). Multi-frequency systems allow the detector to operate at several frequencies simultaneously or optimize for specific products, effectively differentiating between metallic contaminants and the "product effect" (signals caused by the food product's natural conductivity or moisture content). DSP capabilities enable the system to analyze signals intelligently, filter out interference, and precisely identify only genuine metallic foreign objects, significantly reducing costly false rejects and maximizing production uptime.

What are the benefits of integrating metal detectors with Industry 4.0 technologies?

Integrating metal detectors with Industry 4.0 technologies, such as the Internet of Things (IoT), artificial intelligence (AI), and cloud connectivity, offers numerous benefits for food manufacturers. These benefits include real-time performance monitoring and remote diagnostics, enabling proactive maintenance and minimizing downtime. AI-powered analytics improve detection accuracy by learning from data, reducing false positives, and providing insights into contamination trends. Connectivity allows for seamless data exchange with other factory systems (e.g., MES, SCADA), facilitating centralized control, enhanced traceability, and optimized production processes, ultimately leading to higher operational efficiency and improved product quality assurance.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted