Industrial Nitric Acid Market

Industrial Nitric Acid Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_707796 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

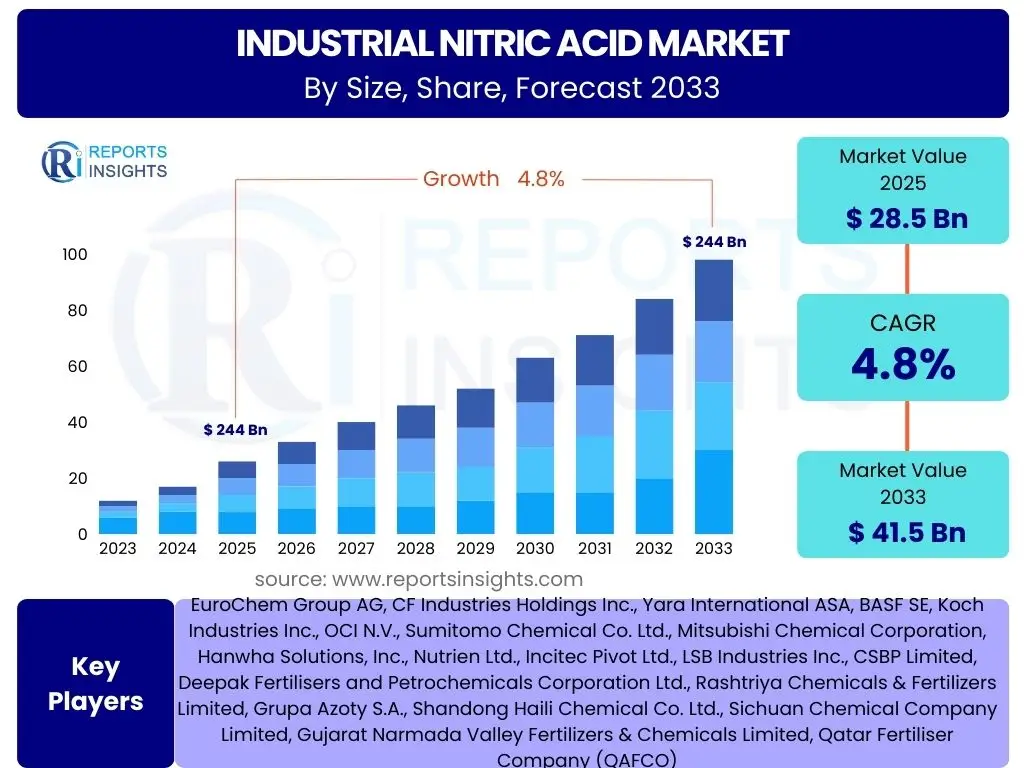

Industrial Nitric Acid Market Size

According to Reports Insights Consulting Pvt Ltd, The Industrial Nitric Acid Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.8% between 2025 and 2033. The market is estimated at USD 28.5 Billion in 2025 and is projected to reach USD 41.5 Billion by the end of the forecast period in 2033.

Key Industrial Nitric Acid Market Trends & Insights

The industrial nitric acid market is undergoing significant transformation, driven by evolving industrial demands and increasing emphasis on sustainability. A key trend involves the surging demand from the agricultural sector, where nitric acid is a critical component in the production of nitrogenous fertilizers such as ammonium nitrate and calcium ammonium nitrate. As global population continues to grow and agricultural practices intensify to meet food demands, the consumption of fertilizers, and consequently nitric acid, is expected to remain robust. This persistent demand underpins much of the market's stability and growth trajectory, particularly in emerging economies with expanding agricultural bases.

Beyond agriculture, the market is also experiencing growth influenced by its diverse applications in other industrial sectors. The chemical industry, for instance, relies heavily on nitric acid for the synthesis of adipic acid, which is a key precursor for nylon production, as well as in the manufacturing of explosives and various specialty chemicals. Technological advancements in production processes, such as improved catalyst technologies and energy-efficient manufacturing methods, are also shaping the market landscape. These innovations aim to reduce operational costs, enhance purity, and minimize environmental impact, thereby driving efficiency and competitiveness among producers.

Furthermore, a growing focus on environmental regulations and sustainability is prompting market players to invest in cleaner production technologies and explore alternative, more eco-friendly methods for nitric acid synthesis. This includes initiatives to reduce greenhouse gas emissions associated with nitric acid production, particularly nitrous oxide. The push towards green chemistry and responsible industrial practices is not just a regulatory imperative but also a growing consumer and stakeholder expectation, influencing investment decisions and market development strategies for the foreseeable future.

- Consistent demand from the fertilizer industry, driven by global food security needs.

- Rising consumption in the chemical sector for adipic acid, explosives, and specialty chemicals.

- Technological advancements in production processes enhancing efficiency and reducing environmental footprint.

- Increasing focus on sustainable manufacturing practices and reduction of nitrous oxide emissions.

- Expansion of industrial bases in emerging economies fueling demand.

AI Impact Analysis on Industrial Nitric Acid

Artificial intelligence (AI) is poised to significantly impact the industrial nitric acid market by revolutionizing various aspects of production, safety, and supply chain management. Common user inquiries often focus on how AI can enhance operational efficiency, optimize complex chemical reactions, and improve predictive capabilities within a highly regulated and energy-intensive industry. AI's ability to analyze vast datasets from sensors, equipment, and historical production logs offers unprecedented opportunities for process optimization. This includes fine-tuning reaction parameters, minimizing raw material waste, and improving energy consumption, all of which directly translate into reduced operational costs and higher yields for nitric acid producers.

Moreover, AI applications are crucial for enhancing safety protocols and predictive maintenance in nitric acid plants, which deal with hazardous materials. Users frequently inquire about AI's role in detecting anomalies in equipment performance, predicting potential failures before they occur, and optimizing maintenance schedules to prevent costly downtime and ensure worker safety. Beyond the plant floor, AI can significantly improve supply chain resilience and demand forecasting. By analyzing market trends, logistical data, and macroeconomic indicators, AI algorithms can provide more accurate predictions of nitric acid demand, helping producers optimize inventory levels, manage raw material procurement, and streamline distribution networks, thereby mitigating supply chain disruptions.

The integration of AI in the industrial nitric acid sector also extends to research and development, where it can accelerate the discovery of new catalysts or more efficient synthesis routes. While the adoption of AI presents challenges such as high initial investment, data security concerns, and the need for specialized expertise, the long-term benefits in terms of efficiency, safety, sustainability, and market responsiveness are compelling. The industry's gradual embrace of digital transformation, with AI at its core, is expected to foster a more resilient, cost-effective, and environmentally responsible production ecosystem for nitric acid.

- Process Optimization: AI-driven algorithms for real-time adjustments to reaction conditions, maximizing yield and purity while minimizing energy consumption.

- Predictive Maintenance: AI models analyze equipment data to forecast failures, enabling proactive maintenance and reducing unscheduled downtime.

- Enhanced Safety: AI systems monitor operational parameters and detect anomalies, providing early warnings for potential hazards and improving plant safety.

- Supply Chain Optimization: AI for demand forecasting, inventory management, and logistics optimization, leading to more efficient distribution and reduced waste.

- Quality Control: AI-powered analytics for continuous monitoring of product quality, ensuring consistency and adherence to specifications.

Key Takeaways Industrial Nitric Acid Market Size & Forecast

The industrial nitric acid market is poised for steady growth through 2033, driven by a confluence of factors that underscore its fundamental role in global industries. A primary takeaway is the sustained demand from the agricultural sector, which continues to be the largest end-user, accounting for a significant portion of the market share due to its indispensability in fertilizer production. This stable demand base provides a strong foundation for market expansion, particularly as global agricultural output is pressured to increase to feed a growing population. Furthermore, the market's trajectory is also significantly influenced by the expanding chemical industry, where nitric acid is vital for the manufacturing of diverse chemical products, including nylon intermediates and explosives, indicating a diversified growth profile.

Another crucial insight is the increasing emphasis on technological advancements and sustainable production practices within the industry. Companies are investing in research and development to improve production efficiency, reduce energy consumption, and minimize environmental impact, particularly concerning nitrous oxide emissions. This focus on sustainability not only addresses stringent regulatory requirements but also enhances the long-term viability and public perception of the industry. The geographic distribution of growth also reveals significant opportunities in emerging economies, particularly in Asia Pacific, where industrialization and agricultural expansion are occurring at a rapid pace, contributing substantially to overall market growth.

In summary, the market's resilience is characterized by its foundational role in essential industries, coupled with a proactive approach to innovation and environmental responsibility. Strategic collaborations, capacity expansions, and continuous process improvements will be key for market players to capitalize on the identified growth opportunities. While challenges related to regulatory compliance and raw material price volatility persist, the overall outlook remains positive, driven by indispensable applications and a concerted effort towards sustainable development.

- The market is projected for consistent growth, primarily fueled by strong demand from the agriculture and chemical industries.

- Emerging economies, particularly in Asia Pacific, are expected to be key growth engines due to industrial and agricultural expansion.

- Technological advancements and a focus on sustainable production are critical for future market development and regulatory compliance.

- Raw material price fluctuations and stringent environmental regulations remain significant influencing factors for market participants.

- Strategic investments in capacity expansion and process optimization are essential for maintaining competitiveness and market share.

Industrial Nitric Acid Market Drivers Analysis

The industrial nitric acid market is primarily driven by the escalating global demand for nitrogenous fertilizers, which constitutes the largest application segment. As the world's population continues to expand, the pressure to increase agricultural yields intensifies, leading to a direct surge in the consumption of fertilizers such as ammonium nitrate and calcium ammonium nitrate, both of which utilize nitric acid as a key raw material. This fundamental demand from the agriculture sector provides a resilient base for market growth, particularly in regions with large agricultural landbases and growing food security concerns.

Beyond agriculture, the robust growth in the chemical industry, particularly in the production of adipic acid (a precursor for nylon 6,6), explosives, and various specialty chemicals, also significantly contributes to market expansion. The increasing industrialization and infrastructure development activities globally necessitate a consistent supply of these derivatives, thereby boosting nitric acid demand. Furthermore, technological advancements in nitric acid manufacturing, focusing on improved efficiency, lower energy consumption, and reduced emissions, encourage capacity expansions and new investments, further propelling market growth by making production more economically viable and environmentally compliant.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing demand for Nitrogenous Fertilizers | +1.2% | Asia Pacific, Latin America, Europe | 2025-2033 |

| Expansion of Adipic Acid & Explosives Manufacturing | +0.8% | North America, Europe, China, India | 2025-2033 |

| Technological Advancements in Production Processes | +0.5% | Global | 2028-2033 |

| Increasing Global Agricultural Output Needs | +0.7% | Developing Economies (APAC, LATAM) | 2025-2033 |

Industrial Nitric Acid Market Restraints Analysis

The industrial nitric acid market faces significant restraints, primarily stemming from stringent environmental regulations concerning the emission of nitrous oxide (N2O), a potent greenhouse gas, during production. Compliance with these regulations necessitates substantial investments in emission control technologies, such as catalytic converters and selective catalytic reduction (SCR) systems. These capital expenditures and ongoing operational costs can deter new market entrants and increase production expenses for existing players, potentially impacting profit margins and slowing capacity expansion, especially in regions with strict environmental policies.

Another major restraint is the volatility in the prices of ammonia, which is the primary raw material for nitric acid production. Ammonia prices are susceptible to fluctuations influenced by natural gas prices, geopolitical tensions, and global supply-demand dynamics. Unpredictable and high raw material costs directly impact the cost of nitric acid production, leading to price instability for end-users and reduced profitability for manufacturers. This volatility can make long-term planning and investment challenging, hindering stable market growth and creating an uncertain operational environment for producers globally.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent Environmental Regulations (N2O emissions) | -0.8% | Europe, North America, China | 2025-2033 |

| Volatility in Raw Material (Ammonia) Prices | -0.7% | Global | 2025-2030 |

| High Energy Consumption in Production | -0.4% | Global | 2025-2033 |

| Safety Concerns in Handling and Storage | -0.3% | Global | 2025-2033 |

Industrial Nitric Acid Market Opportunities Analysis

Significant opportunities exist in the industrial nitric acid market, particularly through capacity expansions and technological upgrades in emerging economies. Countries in the Asia Pacific and Latin America regions are experiencing rapid industrialization and agricultural growth, leading to a substantial increase in demand for nitric acid. Investments in new production facilities or the modernization of existing ones in these regions can yield considerable returns, as they cater to a burgeoning market with increasing consumption of fertilizers, plastics, and explosives. This geographical shift in manufacturing and consumption patterns presents a prime avenue for market players to expand their footprint and capture new market share.

Another prominent opportunity lies in the development and adoption of advanced and sustainable production technologies. Innovations such as enhanced catalytic processes, waste heat recovery systems, and integrated energy-efficient solutions can significantly reduce the environmental footprint and operational costs associated with nitric acid production. The growing global emphasis on green chemistry and sustainable manufacturing practices creates a strong impetus for companies to invest in these technologies. Furthermore, the exploration of novel applications for nitric acid beyond traditional uses, potentially in niche chemical syntheses or environmental remediation, could unlock new revenue streams and diversify the market's growth drivers, offering long-term growth prospects for the industry.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Capacity Expansion in Emerging Economies | +1.0% | Asia Pacific, Latin America, Middle East | 2025-2033 |

| Development of Sustainable Production Technologies | +0.6% | Global | 2028-2033 |

| Increasing Demand from Automotive & Electronics Sectors | +0.4% | North America, Europe, Asia Pacific | 2025-2033 |

| Strategic Collaborations and Partnerships | +0.3% | Global | 2025-2030 |

Industrial Nitric Acid Market Challenges Impact Analysis

The industrial nitric acid market faces significant challenges, particularly related to compliance with increasingly stringent environmental regulations. The production process of nitric acid generates nitrous oxide (N2O), a potent greenhouse gas, which is subject to strict emission limits in many developed and developing nations. Adhering to these regulations requires substantial capital investment in advanced abatement technologies, such as catalytic converters and SCR systems. The ongoing operational costs associated with these technologies, coupled with the potential for heavy fines for non-compliance, can severely impact the profitability and competitiveness of manufacturers, particularly smaller players, potentially stifling market growth.

Another critical challenge is managing the inherent safety risks associated with the storage, handling, and transportation of nitric acid, which is highly corrosive and a strong oxidizing agent. Strict safety protocols, specialized infrastructure, and continuous training are essential to prevent accidents, spills, and environmental contamination. The potential for catastrophic incidents not only poses a threat to human life and the environment but also leads to significant financial liabilities, reputational damage, and increased insurance costs for companies. Ensuring robust safety measures across the entire value chain adds to the operational complexity and cost, representing a constant challenge for market participants in maintaining regulatory adherence and public trust.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Compliance Costs for Environmental Regulations | -0.9% | Europe, North America, Developed Asia | 2025-2033 |

| Safety Risks in Handling and Transportation | -0.6% | Global | 2025-2033 |

| Fluctuations in End-use Industry Demand | -0.4% | Global | 2025-2030 |

| Competition and Price Pressure | -0.3% | Global | 2025-2033 |

Industrial Nitric Acid Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the industrial nitric acid market, offering a detailed assessment of market size, growth trends, competitive landscape, and strategic opportunities. The scope encompasses a thorough examination of key drivers, restraints, opportunities, and challenges influencing market dynamics across various applications, types, and end-use industries, segmented regionally and globally, providing a robust foundation for strategic decision-making.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 28.5 Billion |

| Market Forecast in 2033 | USD 41.5 Billion |

| Growth Rate | 4.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | EuroChem Group AG, CF Industries Holdings Inc., Yara International ASA, BASF SE, Koch Industries Inc., OCI N.V., Sumitomo Chemical Co. Ltd., Mitsubishi Chemical Corporation, Hanwha Solutions, Inc., Nutrien Ltd., Incitec Pivot Ltd., LSB Industries Inc., CSBP Limited, Deepak Fertilisers and Petrochemicals Corporation Ltd., Rashtriya Chemicals & Fertilizers Limited, Grupa Azoty S.A., Shandong Haili Chemical Co. Ltd., Sichuan Chemical Company Limited, Gujarat Narmada Valley Fertilizers & Chemicals Limited, Qatar Fertiliser Company (QAFCO) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The industrial nitric acid market is broadly segmented based on various factors, including its type, application, end-use industry, production method, and grade. This detailed segmentation provides a granular view of market dynamics, allowing for a more precise understanding of demand drivers and competitive landscapes across different product forms and end-user requirements. The distinction between dilute and concentrated nitric acid, for instance, highlights the varying purity and strength needs across industrial applications, with dilute forms typically used in fertilizers and concentrated forms in more specialized chemical syntheses.

Application-wise, the market is heavily dominated by the fertilizer sector, underscoring its foundational role in global agriculture. However, significant growth is also observed in chemical manufacturing, particularly for products like adipic acid for nylon production, toluene diisocyanate (TDI), and nitrobenzene, which cater to a diverse array of downstream industries. The end-use industry segmentation further categorizes demand from agriculture, chemicals, automotive, mining, and defense, revealing the pervasive utility of nitric acid. Additionally, segmenting by production method (e.g., Ostwald process variants) and grade (industrial vs. reagent) offers insights into technological preferences and quality requirements within the market, guiding manufacturers in product development and strategic positioning.

- By Type:

- Dilute Nitric Acid

- Concentrated Nitric Acid

- By Application:

- Fertilizers

- Adipic Acid

- Toluene Diisocyanate (TDI)

- Nitrobenzene

- Nitrochlorobenzene

- Explosives

- Others

- By End-Use Industry:

- Agriculture

- Chemicals

- Automotive

- Mining

- Defense

- Others

- By Production Method:

- Ostwald Process

- High-Pressure Absorption

- Others

- By Grade:

- Industrial Grade

- Reagent Grade

Regional Highlights

- Asia Pacific (APAC): Dominates the industrial nitric acid market, driven by rapid industrialization, expanding agricultural activities, and increasing demand for fertilizers and chemicals in countries like China, India, and Southeast Asian nations. The region is witnessing significant capacity expansions.

- North America: A mature market with stable demand, primarily from the chemical and fertilizer industries. Strict environmental regulations drive investments in advanced emission control technologies and process optimization.

- Europe: Characterized by stringent environmental policies and a focus on sustainable production. Demand is stable from agricultural and chemical sectors, with emphasis on efficiency and reduced emissions.

- Latin America: Exhibiting significant growth due to expanding agricultural land and increasing fertilizer consumption. Brazil and Argentina are key contributors to regional demand.

- Middle East and Africa (MEA): Growing demand from developing agricultural sectors and emerging industrial bases, particularly in the Middle East due to robust petrochemical investments and North Africa for agricultural development.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Industrial Nitric Acid Market.- EuroChem Group AG

- CF Industries Holdings Inc.

- Yara International ASA

- BASF SE

- Koch Industries Inc.

- OCI N.V.

- Sumitomo Chemical Co. Ltd.

- Mitsubishi Chemical Corporation

- Hanwha Solutions, Inc.

- Nutrien Ltd.

- Incitec Pivot Ltd.

- LSB Industries Inc.

- CSBP Limited

- Deepak Fertilisers and Petrochemicals Corporation Ltd.

- Rashtriya Chemicals & Fertilizers Limited

- Grupa Azoty S.A.

- Shandong Haili Chemical Co. Ltd.

- Sichuan Chemical Company Limited

- Gujarat Narmada Valley Fertilizers & Chemicals Limited

- Qatar Fertiliser Company (QAFCO)

Frequently Asked Questions

What are the primary applications of industrial nitric acid?

Industrial nitric acid is primarily used in the production of nitrogenous fertilizers, accounting for the largest share of its consumption. Other significant applications include the manufacturing of adipic acid (for nylon), explosives, toluene diisocyanate (TDI), nitrobenzene, and various other specialty chemicals.

How is the global industrial nitric acid market segmented?

The global industrial nitric acid market is segmented by type (dilute, concentrated), application (fertilizers, adipic acid, explosives, etc.), end-use industry (agriculture, chemicals, automotive, mining, defense), production method, and geographic region.

Which region dominates the industrial nitric acid market?

The Asia Pacific region currently dominates the industrial nitric acid market, driven by extensive agricultural activities, rapid industrialization, and high demand for fertilizers and chemical intermediates in countries like China and India.

What are the major drivers of growth in the industrial nitric acid market?

Key drivers include the increasing global demand for nitrogenous fertilizers due to population growth, expanding applications in the chemical industry (e.g., adipic acid for nylon), and ongoing technological advancements aimed at improving production efficiency and sustainability.

What challenges does the industrial nitric acid market face?

Major challenges include stringent environmental regulations concerning nitrous oxide (N2O) emissions, which necessitate significant compliance costs, and volatility in the prices of raw materials, primarily ammonia. Additionally, managing the inherent safety risks associated with handling and transporting nitric acid poses a continuous challenge.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted