Pet Dry Food Market

Pet Dry Food Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_707291 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

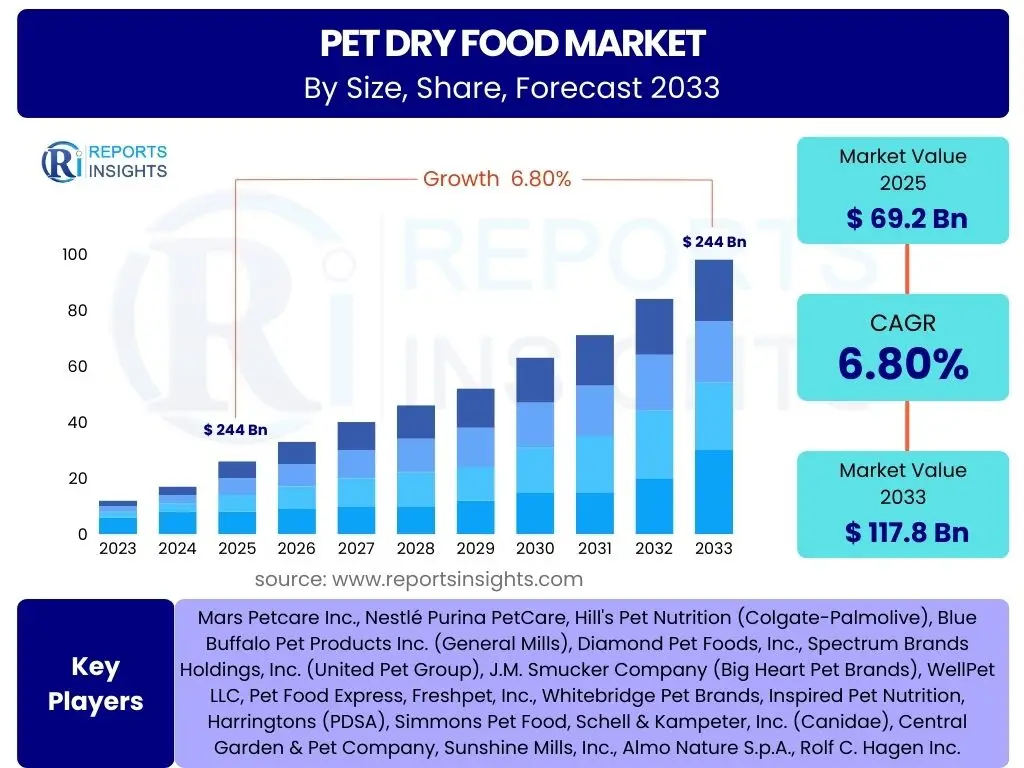

Pet Dry Food Market Size

According to Reports Insights Consulting Pvt Ltd, The Pet Dry Food Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 69.2 billion in 2025 and is projected to reach USD 117.8 billion by the end of the forecast period in 2033.

Key Pet Dry Food Market Trends & Insights

The pet dry food market is undergoing a significant transformation driven by evolving consumer preferences and increasing awareness of pet health. A key trend is the humanization of pets, where owners treat their animals as family members, leading to a demand for higher quality, healthier, and more specialized dry food options. This trend fuels the growth of premium and super-premium segments, characterized by natural ingredients, limited additives, and specific dietary formulations. Consumers are increasingly scrutinizing ingredient lists, seeking transparency and ethically sourced components, moving away from generic formulations towards products that offer tangible health benefits for their pets.

Sustainability is another major influencing factor shaping the market. Pet owners are becoming more environmentally conscious, demanding eco-friendly packaging, sustainably sourced ingredients, and products with a reduced carbon footprint. This extends to the exploration of novel protein sources, such as insect-based proteins or plant-based alternatives, to address environmental concerns associated with traditional meat production. Furthermore, the convenience offered by e-commerce platforms and subscription services is profoundly impacting distribution channels, making it easier for consumers to access a wide variety of dry pet food products, including niche and specialized brands, directly to their homes.

- Humanization of Pets: Increased demand for premium, natural, and specialized dry food.

- Premiumization and Health Focus: Shift towards natural, organic, grain-free, and functional ingredients.

- Sustainability & Ethical Sourcing: Growing preference for eco-friendly packaging and responsibly sourced components.

- Alternative Protein Sources: Rise of insect-based, plant-based, and cultured meat proteins to reduce environmental impact.

- E-commerce Dominance: Accelerated adoption of online retail and subscription models for convenience.

- Personalized Nutrition: Demand for tailored dry food formulations based on breed, age, activity level, and specific health needs.

- Transparency in Labeling: Consumer desire for clear, understandable ingredient lists and sourcing information.

AI Impact Analysis on Pet Dry Food

Artificial intelligence is poised to revolutionize the pet dry food market by enhancing efficiency, enabling personalization, and improving product development. User queries often focus on how AI can contribute to more precise nutritional formulations, optimize supply chains, and create tailored dietary solutions for individual pets. AI algorithms can analyze vast datasets concerning pet health, dietary needs, ingredient effectiveness, and consumer purchasing patterns, leading to the creation of highly specialized and efficacious dry food products. This analytical capability allows manufacturers to respond rapidly to emerging nutritional science and consumer demands, reducing time-to-market for innovative products.

Furthermore, AI plays a crucial role in optimizing manufacturing processes and quality control within the dry pet food industry. From predicting equipment maintenance needs to monitoring ingredient quality and final product consistency, AI-powered systems can minimize waste, reduce operational costs, and ensure product safety and compliance. Consumers also express interest in AI-driven tools that can help them select the best dry food for their pets, such as AI-powered apps that provide dietary recommendations based on a pet's profile, health history, and even genetic information. This integration of AI creates a more responsive, efficient, and consumer-centric ecosystem within the pet dry food sector, addressing concerns about product efficacy and safety through data-driven insights.

- Enhanced Ingredient Sourcing and Quality Control: AI algorithms optimize raw material selection and detect contaminants.

- Personalized Nutrition Formulation: AI analyzes pet data (breed, age, health) to create customized dry food recipes.

- Optimized Manufacturing Processes: Predictive maintenance, efficiency improvements, and waste reduction in production.

- Supply Chain Optimization: AI-driven logistics improve inventory management, distribution, and demand forecasting.

- Consumer Engagement & Recommendations: AI-powered platforms guide pet owners in selecting appropriate dry food products.

- Predictive Market Analytics: AI helps identify emerging trends and consumer preferences for new product development.

- Sustainability Tracking: AI can monitor and optimize resource usage, contributing to greener production.

Key Takeaways Pet Dry Food Market Size & Forecast

The Pet Dry Food Market is poised for substantial growth over the next decade, driven by an increasing global pet population, the humanization of pets, and a heightened focus on pet health and wellness. The projected Compound Annual Growth Rate (CAGR) of 6.8% signifies a robust expansion, reflecting sustained consumer investment in high-quality pet nutrition. This growth is particularly bolstered by emerging economies where pet ownership is on the rise, coupled with developed markets where premiumization and specialized dietary needs are driving higher per-pet spending. Understanding these dynamics is crucial for stakeholders to capitalize on the evolving landscape.

The forecast reaching USD 117.8 billion by 2033 underscores a significant market opportunity across various segments, including premium, therapeutic, and sustainable dry food options. Key market players are expected to focus on innovation in ingredients, formulation, and packaging to meet diverse consumer demands. The shift towards e-commerce and direct-to-consumer models will continue to reshape distribution strategies, offering new avenues for market penetration and customer engagement. Strategic investments in research and development, alongside robust supply chain management, will be vital for maintaining competitiveness and capturing market share in this expanding industry.

- Significant Market Expansion: Expected to grow from USD 69.2 billion in 2025 to USD 117.8 billion by 2033.

- Robust Growth Rate: Projected CAGR of 6.8% indicates strong sustained demand.

- Premiumization Trend: Consumers prioritize quality, natural ingredients, and functional benefits.

- E-commerce Dominance: Online sales channels are crucial for reaching modern consumers.

- Focus on Health & Wellness: Therapeutic and specialized dry food options will see continued demand.

- Innovation Imperative: Product diversification and sustainable practices are key for future growth.

Pet Dry Food Market Drivers Analysis

The increasing humanization of pets represents a primary driver for the pet dry food market, as pet owners are increasingly treating their companion animals as integral family members. This cultural shift translates into a willingness to spend more on premium and high-quality pet food products, seeking formulations that mirror human food trends, such as natural, organic, grain-free, and limited ingredient diets. Pet owners are becoming more educated about pet nutrition, driving demand for dry foods that offer specific health benefits, cater to particular life stages, or address sensitivities, thereby fostering innovation and market expansion within the specialized segments.

The burgeoning global pet population, coupled with rising disposable incomes in developing regions, further fuels market growth. As economic conditions improve, more households are adopting pets, and existing pet owners are able to allocate larger portions of their budgets towards pet care, including superior quality dry food. The convenience and longer shelf life of dry food, compared to wet or raw alternatives, also contribute to its widespread adoption among busy pet owners. Additionally, the proliferation of e-commerce platforms has significantly enhanced product accessibility, allowing consumers to easily discover and purchase a wider variety of dry pet food brands, including niche and international offerings, directly to their homes, thereby expanding market reach and consumer choice.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Pet Humanization | +1.8% | Global, particularly North America, Europe | 2025-2033 (Long-term) |

| Rise in Global Pet Ownership | +1.5% | Asia Pacific, Latin America, Eastern Europe | 2025-2033 (Long-term) |

| Growing Awareness of Pet Health & Nutrition | +1.3% | North America, Western Europe, Australia | 2025-2033 (Long-term) |

| Increasing Disposable Income | +1.0% | Emerging Economies (China, India, Brazil) | 2025-2033 (Long-term) |

| Expansion of E-commerce & Online Retail | +0.8% | Global, particularly urban areas | 2025-2030 (Mid-term) |

Pet Dry Food Market Restraints Analysis

The pet dry food market faces significant restraints, including the rising cost and volatility of raw material prices, particularly for high-quality proteins and specialized ingredients. Fluctuations in agricultural commodity markets, geopolitical events, and supply chain disruptions can lead to increased production costs, which manufacturers may pass on to consumers. This can dampen demand, especially in price-sensitive segments, and lead to reduced profit margins for producers, potentially limiting investment in innovation and market expansion. The reliance on specific protein sources also exposes the industry to supply chain vulnerabilities and sustainability concerns, driving up costs associated with sourcing and processing.

Another restraint is the increasing competition from alternative pet food formats, such as wet food, raw food, and fresh pet food. These alternatives are gaining traction among pet owners who perceive them as more natural, palatable, or beneficial for their pets' health, challenging the traditional dominance of dry food. Perceptions of dry food being overly processed or containing fillers also deter some consumers. Furthermore, stringent regulatory landscapes concerning pet food safety, labeling, and ingredient sourcing in various regions can impose additional compliance costs and complexities on manufacturers. Ensuring adherence to diverse national and international standards requires significant investment in quality control and documentation, acting as a barrier to market entry for new players and increasing operational overheads for existing ones.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatile Raw Material Prices | -0.9% | Global | 2025-2030 (Mid-term) |

| Competition from Alternative Pet Food Formats | -0.7% | North America, Western Europe | 2025-2033 (Long-term) |

| Stringent Pet Food Regulations & Standards | -0.5% | Europe, North America | 2025-2033 (Long-term) |

| Consumer Perceptions of Dry Food Processing | -0.4% | Developed Markets | 2025-2030 (Mid-term) |

Pet Dry Food Market Opportunities Analysis

The rising demand for personalized and functional pet dry food presents a significant opportunity for market players. As pet owners increasingly seek tailored nutritional solutions for their pets based on specific breed, age, activity level, or health conditions (e.g., allergies, joint health, digestive issues), there is a growing niche for highly specialized dry food formulations. This includes products fortified with probiotics, prebiotics, omega fatty acids, or joint supplements, offering targeted health benefits. Manufacturers can leverage advancements in nutritional science and data analytics to develop and market these customized solutions, commanding premium prices and fostering strong brand loyalty among discerning consumers.

Expansion into emerging markets offers another substantial growth opportunity. Countries in Asia Pacific, Latin America, and parts of Eastern Europe are experiencing rapid urbanization, increasing disposable incomes, and a cultural shift towards pet ownership. These regions represent largely untapped markets with significant potential for growth in pet dry food consumption. Establishing robust distribution networks, adapting product offerings to local preferences, and investing in consumer education campaigns in these regions can yield substantial returns. Furthermore, the development and adoption of sustainable and novel protein sources, such as insect proteins, plant-based proteins, or cell-cultured meats, provide a dual opportunity. They address growing environmental concerns among consumers and offer innovative, potentially cost-effective, and hypoallergenic ingredients for future dry pet food formulations, aligning with global sustainability trends and opening new product categories.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Personalized & Functional Pet Food | +1.5% | Global, particularly Developed Markets | 2025-2033 (Long-term) |

| Expansion in Emerging Markets | +1.2% | Asia Pacific, Latin America, Eastern Europe | 2025-2033 (Long-term) |

| Development of Sustainable & Novel Protein Sources | +1.0% | Global | 2027-2033 (Mid to Long-term) |

| Leveraging E-commerce & D2C Models | +0.8% | Global | 2025-2030 (Mid-term) |

| Product Innovation in Specialized Diets (e.g., senior, weight management) | +0.7% | North America, Europe | 2025-2033 (Long-term) |

Pet Dry Food Market Challenges Impact Analysis

The pet dry food market faces significant challenges, notably the intense competition from a burgeoning number of new entrants and established brands, leading to market saturation in certain segments. This heightened competition often results in price wars, increased marketing expenditures, and reduced profit margins for manufacturers. Differentiating products in a crowded market requires substantial investment in branding, innovation, and consumer education, posing a significant hurdle for companies aiming to gain or maintain market share. The need to continuously innovate and offer unique selling propositions while maintaining competitive pricing puts considerable pressure on R&D and operational budgets.

Another critical challenge is managing complex and vulnerable global supply chains, particularly concerning ingredient sourcing and distribution. Disruptions caused by geopolitical events, trade disputes, climate change impacts on agriculture, or widespread pandemics can severely affect the availability and cost of raw materials, from specialized proteins to essential vitamins and minerals. These disruptions can lead to production delays, stockouts, and increased logistical costs, ultimately impacting product availability and consumer prices. Furthermore, maintaining stringent quality control and ensuring product safety across diverse supply chains is a constant challenge, with product recalls potentially causing severe brand damage and financial losses. Navigating the evolving regulatory landscape across different regions also adds complexity, requiring continuous adaptation and compliance efforts to avoid penalties and maintain market access.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Market Competition & Saturation | -0.8% | Developed Markets (North America, Europe) | 2025-2033 (Long-term) |

| Supply Chain Disruptions & Raw Material Volatility | -0.6% | Global | 2025-2028 (Short to Mid-term) |

| Evolving Consumer Preferences & Dietary Trends | -0.5% | Global, particularly Developed Markets | 2025-2033 (Long-term) |

| Product Recalls & Food Safety Concerns | -0.4% | Global | Ongoing (Short-term impact, long-term brand effect) |

Pet Dry Food Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global Pet Dry Food Market, offering critical insights into its current status and future projections. The scope encompasses market sizing, growth forecasts, identification of key market trends, and a detailed examination of drivers, restraints, opportunities, and challenges influencing the industry. It also includes a thorough segmentation analysis and highlights regional dynamics, providing a holistic view for strategic decision-making.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 69.2 Billion |

| Market Forecast in 2033 | USD 117.8 Billion |

| Growth Rate | 6.8% CAGR |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Mars Petcare Inc., Nestlé Purina PetCare, Hill's Pet Nutrition (Colgate-Palmolive), Blue Buffalo Pet Products Inc. (General Mills), Diamond Pet Foods, Inc., Spectrum Brands Holdings, Inc. (United Pet Group), J.M. Smucker Company (Big Heart Pet Brands), WellPet LLC, Pet Food Express, Freshpet, Inc., Whitebridge Pet Brands, Inspired Pet Nutrition, Harringtons (PDSA), Simmons Pet Food, Schell & Kampeter, Inc. (Canidae), Central Garden & Pet Company, Sunshine Mills, Inc., Almo Nature S.p.A., Rolf C. Hagen Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Pet Dry Food Market is intricately segmented based on several key parameters, allowing for a granular understanding of consumer preferences, product innovation, and market dynamics across different categories. This segmentation is crucial for stakeholders to identify high-growth areas and tailor their strategies to specific consumer needs, animal types, and distribution channels. The market's complexity necessitates a detailed breakdown to highlight the various influences on purchasing decisions and product development.

Understanding these segments reveals distinct consumer behaviors and market opportunities. For instance, the 'By Animal Type' segment clearly differentiates the dominant dog and cat food markets, each with unique nutritional requirements and product innovations. The 'By Ingredient Type' segment reflects evolving consumer demand for specific protein sources or plant-based alternatives, driven by health and sustainability concerns. Similarly, segmentation by 'Life Stage' ensures that products are formulated to meet the precise needs of pets from puppyhood/kittenhood through their senior years, while 'Distribution Channel' highlights the growing importance of online retail alongside traditional brick-and-mortar stores. This detailed segmentation analysis provides a comprehensive framework for navigating the diverse landscape of the pet dry food industry and identifying areas ripe for strategic investment.

- By Animal Type:

- Dog Food

- Cat Food

- Other Pet Food (e.g., Bird, Small Animal)

- By Ingredient Type:

- Animal-derived (Meat, Poultry, Fish)

- Plant-derived (Grains, Vegetables, Fruits)

- Novel Proteins (e.g., Insect-based, Cultured Meat)

- Additives (Vitamins, Minerals, Supplements)

- By Product Type:

- Premium & Super-Premium

- Mid-Priced

- Economy

- By Life Stage:

- Puppy/Kitten

- Adult

- Senior

- All Life Stages

- By Distribution Channel:

- Supermarkets/Hypermarkets

- Pet Specialty Stores

- Online Retailers (E-commerce)

- Veterinary Clinics & Pharmacies

- Other Channels (e.g., Discount Stores, Farm Supply Stores)

- By Flavor:

- Chicken

- Beef

- Fish & Seafood

- Lamb

- Other Animal Proteins

- Vegetarian/Vegan

- Mixed Flavors

- By Form:

- Kibble

- Pellets

- Crisps

- By Special Diet:

- Grain-Free

- Limited Ingredient Diets (LID)

- Weight Management

- Sensitive Stomach & Digestion

- Hypoallergenic

- Oral Health

- Joint & Mobility Support

- Skin & Coat Health

Regional Highlights

- North America: This region holds a dominant share of the pet dry food market, driven by high pet ownership rates, strong humanization trends, and a mature market for premium and specialized pet nutrition. Consumers in the U.S. and Canada are highly attuned to ingredient quality, natural formulations, and products catering to specific health conditions. The widespread availability of diverse distribution channels, including large pet specialty chains and a thriving e-commerce sector, further supports market growth. Innovation in grain-free, limited ingredient, and functional diets is a continuous trend.

- Europe: Europe represents a significant and steadily growing market, characterized by stringent pet food regulations and a strong emphasis on pet welfare. Western European countries, such as Germany, the UK, and France, lead in consumption, driven by increasing disposable incomes and a preference for natural, organic, and ethically sourced pet food. The market also sees rising demand for sustainable packaging and alternative protein sources, reflecting broader consumer environmental concerns. Eastern Europe is emerging as a growth region, fueled by rising pet adoption rates and increasing awareness of premium pet nutrition.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing region in the pet dry food market, primarily driven by rapid urbanization, increasing disposable incomes, and a significant rise in pet adoption rates, particularly in China, India, Japan, and Australia. The shift from traditional homemade diets to commercial pet food, combined with growing awareness of pet health, propels demand for dry food. While premiumization is a growing trend, affordability and accessibility remain key factors, leading to a diverse market with both economy and high-end segments experiencing growth. E-commerce platforms are playing a crucial role in market expansion and consumer reach.

- Latin America: This region is experiencing considerable growth in the pet dry food market, attributed to rising pet ownership, improving economic conditions, and a growing middle class. Brazil and Mexico are leading the market, with increasing consumer spending on pet care products, including dry food. While price sensitivity remains a factor, there is a gradual shift towards mid-priced and premium dry food options, reflecting a growing appreciation for pet nutrition. Local manufacturers and international brands are actively expanding their presence to cater to this expanding market.

- Middle East and Africa (MEA): The MEA region represents a nascent but promising market for pet dry food. Growth is primarily driven by increasing urbanization, rising disposable incomes, and the gradual adoption of pet ownership as a cultural trend in certain countries, particularly in the UAE, Saudi Arabia, and South Africa. The market is currently dominated by international brands, with a growing demand for basic and mid-priced dry food. As awareness of pet health and nutrition increases, there is potential for growth in the premium segment, though cultural and economic factors will continue to shape market development.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Pet Dry Food Market.- Mars Petcare Inc.

- Nestlé Purina PetCare

- Hill's Pet Nutrition (Colgate-Palmolive)

- Blue Buffalo Pet Products Inc. (General Mills)

- Diamond Pet Foods, Inc.

- Spectrum Brands Holdings, Inc. (United Pet Group)

- J.M. Smucker Company (Big Heart Pet Brands)

- WellPet LLC

- Freshpet, Inc.

- Whitebridge Pet Brands

- Inspired Pet Nutrition

- Harringtons (PDSA)

- Simmons Pet Food

- Schell & Kampeter, Inc. (Canidae)

- Central Garden & Pet Company

- Sunshine Mills, Inc.

- Almo Nature S.p.A.

- Rolf C. Hagen Inc.

- Yamamoto Corporation

- ADM Animal Nutrition

Frequently Asked Questions

What is the projected growth rate of the Pet Dry Food Market?

The Pet Dry Food Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033, reaching USD 117.8 billion by the end of the forecast period.

What are the primary drivers for the Pet Dry Food Market?

Key drivers include the increasing humanization of pets, rising global pet ownership, growing awareness of pet health and nutrition, increasing disposable incomes, and the expansion of e-commerce and online retail channels.

How is AI impacting the Pet Dry Food Market?

AI is influencing the market through enhanced ingredient sourcing, personalized nutrition formulation, optimized manufacturing processes, improved supply chain efficiency, and AI-driven consumer engagement tools for product recommendations.

What are the main challenges faced by the Pet Dry Food Market?

Challenges include intense market competition and saturation, volatile raw material prices, potential supply chain disruptions, evolving consumer preferences, and concerns related to product recalls and food safety.

Which regions are key contributors to the Pet Dry Food Market?

North America holds a dominant market share, while Europe is a significant and mature market. Asia Pacific is projected to be the fastest-growing region, with Latin America and MEA also showing considerable growth potential.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted