Building Water Shut Off Valve Market

Building Water Shut Off Valve Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708976 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

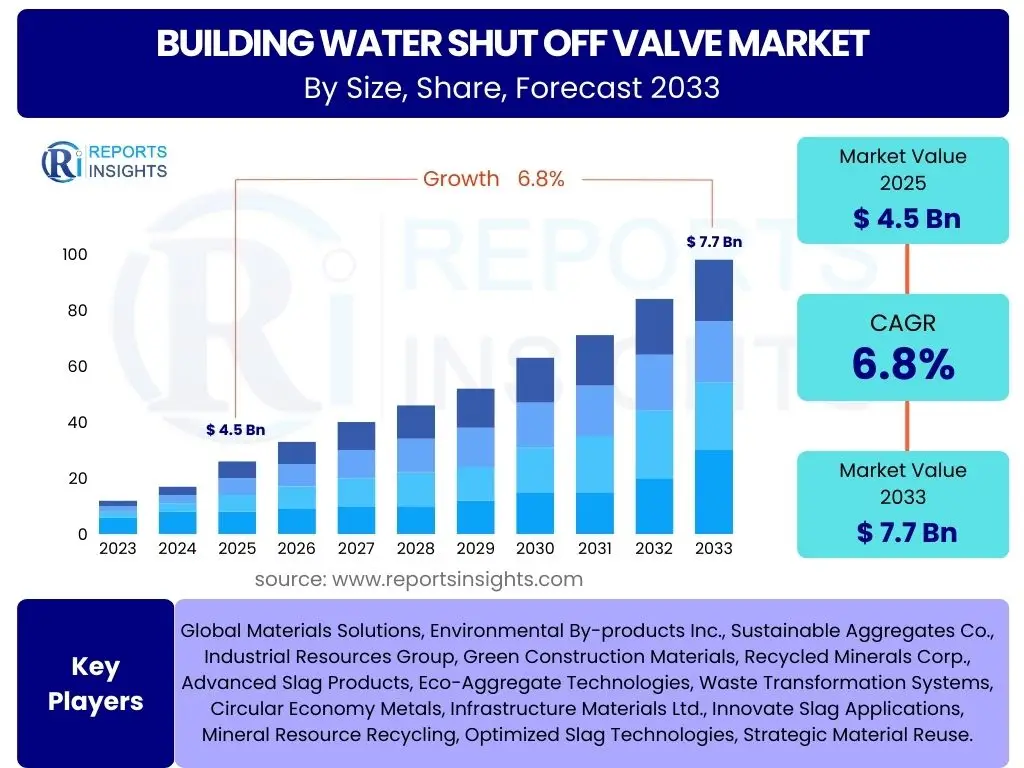

Building Water Shut Off Valve Market Size

According to Reports Insights Consulting Pvt Ltd, The Building Water Shut Off Valve Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 4.5 Billion in 2025 and is projected to reach USD 7.7 Billion by the end of the forecast period in 2033.

Key Building Water Shut Off Valve Market Trends & Insights

The Building Water Shut Off Valve market is currently experiencing significant evolution driven by several key factors. User queries frequently center on the integration of smart technologies, the increasing focus on water conservation, and the regulatory push for enhanced safety and leak prevention in both residential and commercial structures. There is a discernible demand for more efficient, durable, and user-friendly valve solutions that can mitigate water damage and optimize building management.

Furthermore, evolving construction practices and the growing emphasis on sustainable building solutions are shaping product development. Users are interested in understanding how these trends translate into tangible benefits like reduced operational costs, improved property protection, and enhanced resource management. The market is also seeing a rise in demand for specialized valves that can withstand aggressive water conditions and provide long-term reliability in diverse applications, from high-rise buildings to industrial facilities. This shift underscores a broader industry move towards advanced engineering and value-added functionalities beyond basic shut-off capabilities.

- Smart Valve Integration: Increasing adoption of IoT-enabled and automated shut-off valves for leak detection and remote control.

- Sustainable Building Practices: Growing demand for durable, lead-free, and environmentally compliant valve materials.

- Water Conservation Focus: Development of valves designed to minimize water waste through precise flow control and rapid shut-off mechanisms.

- Modular Construction Trends: Demand for pre-assembled valve solutions that simplify installation in modern construction methods.

- Enhanced Safety Regulations: Stricter building codes and insurance requirements driving the adoption of reliable and certified shut-off valves.

- Do-It-Yourself (DIY) Market Growth: Expansion of user-friendly and easy-to-install valve options for homeowners.

AI Impact Analysis on Building Water Shut Off Valve

The influence of Artificial Intelligence (AI) on the Building Water Shut Off Valve market is rapidly expanding, with common user questions frequently exploring its potential for predictive maintenance, enhanced leak detection, and integration within larger smart building ecosystems. Users are keen to understand how AI can move these systems from reactive to proactive, minimizing costly water damage and optimizing maintenance schedules. This often involves queries about the accuracy of AI algorithms in identifying subtle anomalies in water flow and pressure, and the reliability of automated responses.

Moreover, there is considerable interest in AI's role in data analytics for water usage patterns, enabling building managers to identify inefficiencies and implement conservation strategies. The convergence of AI with IoT sensors in water systems is viewed as a game-changer, offering unprecedented levels of control and insight. Concerns often revolve around data privacy, cybersecurity risks associated with networked systems, and the initial investment required for AI-powered solutions. Nevertheless, the overarching expectation is that AI will significantly improve the intelligence, efficiency, and resilience of building water infrastructure.

- Predictive Maintenance: AI algorithms analyze water flow data to predict potential valve failures or leaks before they occur, enabling proactive repairs.

- Enhanced Leak Detection: AI-powered sensors can distinguish between normal water usage and abnormal flow patterns indicative of leaks, triggering automated shut-offs.

- Automated Shut-Off Systems: Integration with AI allows for intelligent, rapid, and localized water shut-off in response to detected issues, minimizing damage.

- Water Usage Optimization: AI analyzes consumption patterns, identifying areas of inefficiency and suggesting adjustments for better water conservation.

- Smart Building Integration: AI facilitates seamless communication between water shut-off valves and other building management systems (BMS), enhancing overall operational efficiency.

- Remote Monitoring and Control: AI-driven platforms provide real-time insights and remote control capabilities, improving responsiveness and reducing manual oversight.

Key Takeaways Building Water Shut Off Valve Market Size & Forecast

The Building Water Shut Off Valve market is poised for robust growth, with key user inquiries highlighting the critical role these components play in modern infrastructure and risk management. The increasing awareness of water damage costs, coupled with advancements in smart home and building technologies, is fundamentally reshaping market dynamics. A significant takeaway is the accelerating demand for solutions that offer both preventative measures against leaks and real-time control, underscoring a shift from traditional manual systems to automated, intelligent ones.

Furthermore, the market forecast underscores the expanding application across diverse building types, from residential complexes to large-scale commercial and industrial facilities. This growth is heavily influenced by regulatory pressures to enhance building safety and sustainability, alongside the economic incentives for property owners to mitigate potential liabilities. The continued innovation in materials, design, and connectivity is expected to drive market expansion, providing opportunities for manufacturers focusing on reliability, efficiency, and smart integration.

- Consistent Market Growth: Steady CAGR indicates a healthy and expanding market driven by essential building needs and technological advancements.

- Increasing Investment in Smart Solutions: Significant capital allocation towards smart, connected shut-off valves due to their value proposition in leak prevention and water management.

- Resilience in Construction Sector: Market growth is closely tied to global construction activities and infrastructure development.

- Regulatory Compliance as a Driver: Evolving building codes and insurance standards mandate higher quality and more reliable shut-off systems.

- Focus on Water Damage Mitigation: A primary driver is the reduction of property damage and associated costs through effective water control.

- Long-term Value Proposition: Emphasis on durable, low-maintenance, and efficient valves that offer significant long-term operational savings.

Building Water Shut Off Valve Market Drivers Analysis

The Building Water Shut Off Valve market is significantly propelled by an escalating awareness of the substantial costs and inconveniences associated with water damage in residential, commercial, and industrial buildings. Property owners and insurers are increasingly seeking proactive measures to prevent catastrophic leaks, driving the adoption of more reliable and advanced valve systems. This heightened consciousness is coupled with the continuous growth in global construction activities, particularly in urban centers, which directly translates into a higher demand for essential building components like water shut-off valves.

Moreover, the integration of smart home and building automation technologies is serving as a powerful catalyst for market expansion. The desire for enhanced control, remote monitoring, and automated safety features, such as automatic leak detection and shut-off, is pushing manufacturers to innovate. Stringent building codes and regulations mandating specific valve types and installation standards, aimed at improving safety and energy efficiency, further reinforce the market's upward trajectory, ensuring consistent demand for compliant and high-performance solutions.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Awareness of Water Damage Costs | +1.5-2.0% | Global | Short to Mid-term (2025-2030) |

| Growth in Construction Sector & Urbanization | +1.0-1.5% | Asia Pacific, North America, Europe | Mid to Long-term (2025-2033) |

| Technological Advancements in Smart Building Systems | +0.8-1.2% | North America, Europe, Asia Pacific (Developed Economies) | Short to Mid-term (2025-2030) |

| Stringent Building Codes & Safety Regulations | +0.5-0.8% | Europe, North America | Ongoing |

| Focus on Water Conservation & Sustainability Initiatives | +0.3-0.5% | Global | Mid to Long-term (2025-2033) |

Building Water Shut Off Valve Market Restraints Analysis

Despite the positive growth trajectory, the Building Water Shut Off Valve market faces several notable restraints that could temper its expansion. One significant factor is the relatively high upfront cost associated with advanced and smart shut-off valve systems, which can deter adoption, especially in budget-sensitive projects or existing structures where retrofitting costs are substantial. This economic barrier often leads to the continued preference for traditional, less expensive, and manually operated valves, particularly in developing regions.

Another restraint involves the complexity of installation and maintenance for sophisticated valve technologies. Integrating smart valves into existing plumbing and building management systems can require specialized expertise and extensive modifications, posing challenges for contractors and end-users alike. Additionally, a lack of standardized protocols for smart home devices and interoperability issues among different manufacturers' systems can create fragmentation and hinder widespread adoption. Market saturation in certain mature segments, coupled with the long lifespan of traditional valves, further limits the replacement market in some regions.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Upfront Cost of Smart & Advanced Valves | -0.7-1.0% | Global, particularly Developing Regions | Short to Mid-term (2025-2030) |

| Complexity of Installation & Integration | -0.5-0.8% | North America, Europe (Retrofit Market) | Short to Mid-term (2025-2030) |

| Lack of Standardization & Interoperability Issues | -0.3-0.5% | Global | Mid-term (2025-2030) |

| Durability & Long Lifespan of Traditional Valves | -0.2-0.4% | Mature Markets (Europe, North America) | Long-term (2028-2033) |

Building Water Shut Off Valve Market Opportunities Analysis

The Building Water Shut Off Valve market presents significant opportunities for growth and innovation, particularly in the realm of smart technology and enhanced functionality. The ongoing digital transformation in building management offers a fertile ground for manufacturers to develop and integrate IoT-enabled valves that provide predictive analytics, remote diagnostics, and automated responses. This focus on intelligent water management systems caters to the increasing demand for efficiency, cost savings, and proactive maintenance, creating a substantial avenue for market expansion in both new constructions and retrofitting projects.

Furthermore, the burgeoning market for sustainable and environmentally friendly building solutions opens doors for lead-free, corrosion-resistant, and energy-efficient valve materials. Developing regions, characterized by rapid urbanization and infrastructure development, represent untapped potential where the adoption of modern plumbing standards is accelerating. Collaborations with smart home platform providers, insurance companies, and utility providers can also unlock new distribution channels and incentivize wider adoption, transforming the market landscape by offering value-added services beyond the physical product.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Integration with IoT & Smart Building Platforms | +1.2-1.8% | Global, particularly North America, Europe, Asia Pacific | Short to Mid-term (2025-2030) |

| Expansion in Developing & Emerging Economies | +0.8-1.2% | Asia Pacific, Latin America, MEA | Mid to Long-term (2027-2033) |

| Development of Sustainable & Advanced Materials | +0.5-0.9% | Global | Mid-term (2025-2030) |

| Partnerships with Insurance & Utility Providers | +0.4-0.7% | North America, Europe | Mid to Long-term (2026-2033) |

| Retrofit Market for Existing Buildings | +0.3-0.6% | Mature Markets (Europe, North America) | Ongoing |

Building Water Shut Off Valve Market Challenges Impact Analysis

The Building Water Shut Off Valve market faces several significant challenges that could impede its growth and widespread adoption of advanced solutions. One primary challenge is the cybersecurity risk associated with internet-connected smart valves. As more devices integrate into smart building networks, they become potential targets for cyber threats, which could compromise system integrity or even lead to malicious manipulation of water supplies. This concern necessitates robust security protocols and continuous updates, adding complexity and cost to product development and maintenance.

Another major obstacle is the resistance to change from traditional plumbing practices and the limited technical expertise among installers and end-users regarding advanced valve systems. The industry often relies on conventional methods, and the learning curve for new, complex technologies can be steep, leading to improper installation or underutilization of smart features. Furthermore, intense price competition from low-cost manufacturers, particularly in conventional valve segments, pressures profit margins and can hinder investment in research and development for innovative solutions. Navigating diverse regulatory landscapes across different regions also adds a layer of complexity for global market players.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Cybersecurity Risks for Smart Valves | -0.6-0.9% | Global | Short to Mid-term (2025-2030) |

| Technical Expertise & Training Requirements | -0.4-0.7% | Global | Short to Mid-term (2025-2030) |

| Intense Price Competition | -0.3-0.5% | Asia Pacific, Latin America (Traditional Segments) | Ongoing |

| Regulatory Hurdles & Compliance Across Regions | -0.2-0.4% | Global | Ongoing |

Building Water Shut Off Valve Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Building Water Shut Off Valve market, offering detailed insights into market size, growth drivers, restraints, opportunities, and challenges across various segments and regions. The report encompasses historical data from 2019 to 2023, establishing a robust baseline for future projections, and provides a forward-looking forecast up to 2033. It meticulously examines the impact of technological advancements, regulatory changes, and evolving consumer preferences on market dynamics, highlighting key trends such as the integration of smart technologies and sustainable practices. The scope includes a thorough segmentation analysis, regional deep-dives, and profiles of leading market players, offering a holistic view for strategic decision-making.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 4.5 Billion |

| Market Forecast in 2033 | USD 7.7 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Fluidmaster Inc., Reliance Worldwide Corporation (RWC), Zurn Industries, Apollo Valves (Conbraco Industries), Watts Water Technologies, Inc., Nibco Inc., Viega LLC, Moen Inc., Masco Corporation (Delta Faucet), Uponor Corporation, Honeywell International Inc., Emerson Electric Co., Schluter Systems, Aquor Water Systems, Sioux Chief Manufacturing, Boshart Industries, Wilkins (Zurn Industries), Dormont Manufacturing, Matco-Norca, Anvil International |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Building Water Shut Off Valve market is comprehensively segmented to provide granular insights into its diverse components, offering a detailed understanding of product types, materials, operational mechanisms, and applications. This segmentation allows for precise market sizing and forecasting, identifying specific growth areas and competitive landscapes within each sub-segment. Analyzing these distinct categories helps stakeholders to tailor product development, marketing strategies, and regional focus based on specific demand patterns and regulatory requirements across the global market. The dynamic interplay between these segments often dictates the overall market trajectory, especially with the rise of integrated smart solutions impacting multiple traditional categories simultaneously.

- By Type: Includes essential categories such as Ball Valves (known for quick shut-off), Gate Valves (for full flow applications), Globe Valves (for throttling flow), Butterfly Valves (compact and quick operation), Check Valves (prevent backflow), Pressure Reducing Valves, Zone Valves, Mixing Valves, and various other specialized types catering to specific building water management needs.

- By Material: Covers common materials like Brass (durability, corrosion resistance), Bronze (similar to brass, often used in marine applications), Plastic (PVC, PEX for affordability and ease of installation), Stainless Steel (high corrosion resistance), Cast Iron (robust for large pipes), and other composite materials chosen for specific performance characteristics and regulatory compliance (e.g., lead-free).

- By Operation: Distinguishes between Manual operation (traditional, hand-operated valves) and Automatic operation, which includes Electric (motorized), Hydraulic, Pneumatic, and increasingly sophisticated Smart/IoT Enabled valves that offer remote control, sensor-based automation, and predictive capabilities.

- By Application: Categorizes usage across various building types, including Residential Buildings (single-family homes, multi-family apartments), Commercial Buildings (offices, retail, hospitality, healthcare facilities, educational institutions), Industrial Buildings (factories, warehouses), and Public & Municipal Buildings, each having unique demands for valve performance and reliability.

- By End-Use: Differentiates demand arising from New Construction projects (initial installations in newly built structures) versus Renovation & Replacement projects (upgrades or replacements in existing buildings, often driven by maintenance, technology upgrades, or regulatory mandates).

Regional Highlights

- North America: Exhibits a mature market characterized by robust building codes, high adoption rates of smart home technologies, and a strong emphasis on water damage prevention. The region is a significant adopter of advanced and automated shut-off valve systems, driven by consumer awareness and insurance incentives.

- Europe: A technologically advanced region with strict environmental regulations and high standards for building efficiency and water conservation. Germany, the UK, and France are key markets, showing growing demand for lead-free valves and integrated building management solutions.

- Asia Pacific (APAC): Represents the fastest-growing market due to rapid urbanization, increasing infrastructure development, and a booming construction sector, particularly in countries like China, India, Japan, and Australia. Rising disposable incomes and increasing awareness of water management are fueling demand for modern valve solutions.

- Latin America: Shows steady growth, with increasing investments in residential and commercial construction, particularly in Brazil and Mexico. The market is gradually transitioning from traditional to more efficient and durable valve systems.

- Middle East and Africa (MEA): Experiencing significant growth driven by large-scale construction projects, especially in the GCC countries. Water scarcity issues are also prompting investment in efficient water management systems, including advanced shut-off valves.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Building Water Shut Off Valve Market.- Watts Water Technologies, Inc.

- Zurn Industries, LLC (a part of Zurn Elkay Water Solutions)

- Reliance Worldwide Corporation (RWC)

- Apollo Valves (Conbraco Industries, Inc.)

- NIBCO Inc.

- Viega LLC

- Fluidmaster Inc.

- Moen Inc. (part of Fortune Brands Home & Security)

- Masco Corporation (Delta Faucet Company)

- Uponor Corporation

- Honeywell International Inc.

- Emerson Electric Co.

- GF Piping Systems (Georg Fischer Ltd.)

- IMI Hydronic Engineering (part of IMI plc)

- Mueller Water Products, Inc.

- Victaulic Company

- Danfoss A/S

- Sioux Chief Manufacturing Co. Inc.

- A.Y. McDonald Mfg. Co.

- SharkBite (part of RWC)

Frequently Asked Questions

Analyze common user questions about the Building Water Shut Off Valve market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the projected growth rate for the Building Water Shut Off Valve market?

The market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033, driven by increasing construction activities and demand for smart water management solutions.

What key trends are influencing the Building Water Shut Off Valve market?

Key trends include the integration of smart, IoT-enabled valves for remote control and leak detection, the adoption of sustainable and lead-free materials, and a growing emphasis on water conservation and enhanced safety regulations in buildings.

How is AI impacting the Building Water Shut Off Valve sector?

AI significantly impacts the sector through predictive maintenance, advanced leak detection, automated shut-off systems, and optimization of water usage patterns, leading to more efficient and resilient building water infrastructure.

Which regions are expected to show the most significant growth in this market?

The Asia Pacific region, particularly countries like China and India, is expected to exhibit the most significant growth due to rapid urbanization, infrastructure development, and increasing adoption of modern plumbing standards. North America and Europe also remain strong markets for advanced solutions.

What are the main challenges faced by the Building Water Shut Off Valve market?

Primary challenges include the high upfront cost of advanced smart valves, the complexity of installation and integration with existing systems, cybersecurity risks associated with connected devices, and the need for specialized technical expertise among installers and end-users.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted