Waste Sorting Robot Market

Waste Sorting Robot Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_707544 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

Waste Sorting Robot Market Size

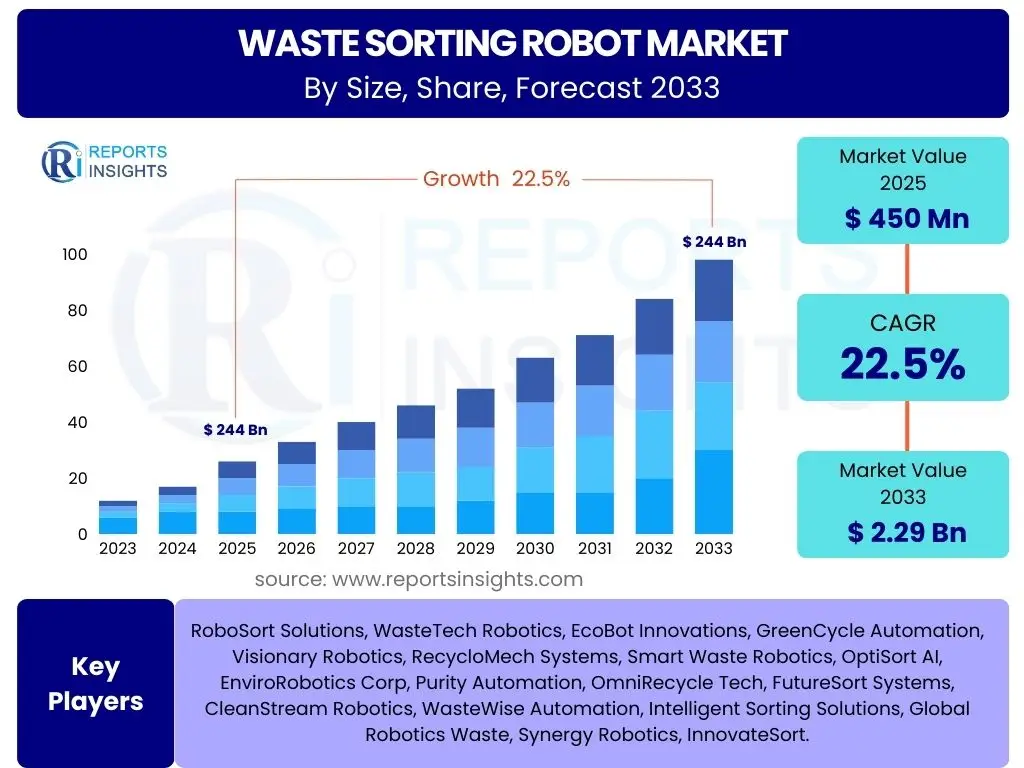

According to Reports Insights Consulting Pvt Ltd, The Waste Sorting Robot Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 22.5% between 2025 and 2033. The market is estimated at USD 450 Million in 2025 and is projected to reach USD 2.29 Billion by the end of the forecast period in 2033.

Key Waste Sorting Robot Market Trends & Insights

Common user inquiries regarding the waste sorting robot market frequently revolve around the adoption of advanced technologies, the shift towards sustainable waste management practices, and the increasing demand for automation in labor-intensive industries. These discussions highlight a collective interest in how robotic solutions are evolving to address complex waste streams, improve material recovery rates, and reduce operational costs. There is also significant curiosity about the integration of artificial intelligence and machine learning to enhance sorting precision and adaptability.

Furthermore, users often question the economic viability and environmental benefits of these systems, seeking data on return on investment and contributions to circular economy initiatives. The rising global waste generation coupled with stringent environmental regulations are consistently cited as primary drivers, leading to a strong trend towards automating the previously manual and often hazardous task of waste segregation. The market is witnessing a continuous push for more versatile and efficient robotic solutions capable of handling diverse materials with high accuracy.

- Integration of Artificial Intelligence and Machine Learning for enhanced material recognition and sorting accuracy.

- Development of collaborative robots (cobots) for safer and more flexible deployment in existing facilities.

- Increasing adoption of hyperspectral imaging and advanced sensor technologies for precise material identification.

- Growth in demand for sorting robots in diverse waste streams beyond municipal solid waste, including e-waste and construction debris.

- Emphasis on modular and scalable robotic systems to adapt to varying operational needs and capacities.

- Shift towards circular economy principles driving the need for higher purity recycled materials, boosting robot adoption.

AI Impact Analysis on Waste Sorting Robot

User questions regarding the impact of AI on waste sorting robots frequently center on how these intelligent systems can overcome current limitations, such as handling highly commingled waste or identifying subtle differences in material composition. There is keen interest in AI's role in improving the speed, accuracy, and adaptability of sorting processes, moving beyond traditional mechanical or optical methods. Users inquire about self-learning capabilities, predictive maintenance, and the potential for AI to optimize entire waste management workflows, from collection to final recycling.

The core expectations from AI integration include significantly higher recovery rates of valuable recyclables, a substantial reduction in contamination, and the ability of robots to adapt to new types of waste materials without extensive reprogramming. Concerns often relate to the cost of implementing such advanced systems, the availability of skilled personnel to manage them, and the ethical implications of automation on human labor. Ultimately, the discourse points towards AI as a transformative technology that promises to revolutionize waste sorting from a largely manual process into a highly efficient, data-driven, and autonomous operation.

- Enhanced material recognition: AI algorithms enable robots to identify and differentiate between complex materials, including various plastics, glass, metals, and organic matter, with higher accuracy than human sorters or traditional sensors.

- Adaptive learning capabilities: Robots equipped with AI can learn from new data, continuously improving their sorting efficiency and adapting to changes in waste streams or material compositions over time.

- Optimized sorting strategies: AI analyzes vast amounts of data to determine the most efficient sorting pathways, leading to higher throughput and reduced energy consumption.

- Reduced contamination rates: Precision sorting powered by AI minimizes the cross-contamination of materials, yielding higher quality recyclates that command better market prices.

- Predictive maintenance: AI can monitor robot performance and predict potential component failures, allowing for proactive maintenance and reducing downtime, thereby improving overall operational efficiency.

- Automation of complex tasks: AI allows robots to handle tasks previously deemed too complex for automation, such as sorting mixed plastics or delicate electronics, expanding the scope of robotic application in waste management.

Key Takeaways Waste Sorting Robot Market Size & Forecast

Common user questions regarding key takeaways from the Waste Sorting Robot market size and forecast often focus on the market's rapid growth trajectory, driven by global sustainability mandates and the economic pressures of waste management. Users are particularly interested in understanding the primary factors contributing to this expansion, such as increasing waste volumes, stringent environmental regulations, and the rising cost and scarcity of manual labor. The forecast highlights a significant shift towards automation as an essential solution for efficient resource recovery and waste diversion from landfills.

Furthermore, inquiries frequently touch upon the technological advancements, especially in AI and robotics, that underpin this growth, asking how these innovations are improving sorting accuracy and operational efficiency. The market's potential for significant financial returns for early adopters, coupled with its environmental benefits, positions it as a critical sector for investment and development. The sustained high Compound Annual Growth Rate (CAGR) underscores a robust market poised for considerable expansion throughout the forecast period, reflecting a growing global commitment to advanced waste processing solutions.

- The waste sorting robot market is set for substantial growth, driven by escalating global waste generation and increasing environmental consciousness.

- Technological advancements, particularly in AI and machine learning, are pivotal in enhancing robot capabilities, leading to higher sorting precision and efficiency.

- Economic factors such as rising labor costs and the demand for higher purity recycled materials are accelerating the adoption of robotic sorting solutions.

- Governments and industries worldwide are investing in automation to meet ambitious recycling targets and improve resource recovery rates.

- The market presents significant investment opportunities due to its strong CAGR and the growing imperative for sustainable waste management practices globally.

- Early adopters of waste sorting robot technology are likely to gain competitive advantages through improved operational efficiency and reduced long-term costs.

Waste Sorting Robot Market Drivers Analysis

The Waste Sorting Robot market is significantly propelled by several key factors globally. A primary driver is the escalating volume of waste generated worldwide, necessitating more efficient and scalable sorting solutions than manual methods can provide. Concurrently, increasingly stringent environmental regulations and ambitious recycling targets set by governments across regions are compelling waste management companies and industries to adopt advanced automation technologies to enhance material recovery and reduce landfill reliance. These regulatory pressures, combined with a growing global awareness of sustainability and the circular economy, are creating a robust demand for robotic sorting systems.

Furthermore, the rising labor costs associated with manual sorting, coupled with safety concerns for human workers in hazardous waste environments, make robotic solutions an attractive alternative. Robotics offers a consistent, tireless, and safer approach to waste segregation, addressing the labor shortage challenges faced by the waste management industry. The continuous advancements in artificial intelligence, computer vision, and robotic mechanics also act as significant drivers, improving the capabilities, accuracy, and cost-effectiveness of these robots, making them more viable for a broader range of applications and waste streams.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Waste Generation Volume Globally | +5.5% | Global, particularly Asia Pacific, North America | Long-term (2025-2033) |

| Stringent Environmental Regulations and Recycling Targets | +4.8% | Europe, North America, Japan, China | Mid-to-Long-term (2026-2033) |

| Rising Labor Costs and Shortage in Waste Management | +4.2% | North America, Europe, Australia | Short-to-Mid-term (2025-2029) |

| Technological Advancements in AI and Robotics | +3.5% | Global, particularly Developed Economies | Ongoing (2025-2033) |

| Growing Awareness of Circular Economy and Sustainability | +2.8% | Europe, North America, East Asia | Long-term (2027-2033) |

Waste Sorting Robot Market Restraints Analysis

Despite significant growth potential, the Waste Sorting Robot market faces several notable restraints. A major hurdle is the high initial capital investment required for purchasing and integrating these advanced robotic systems. Small to medium-sized waste management facilities or those with limited budgets may find it challenging to afford the upfront costs, which include not only the robots themselves but also the necessary infrastructure modifications, software integration, and operator training. This substantial financial outlay can significantly deter adoption, particularly in developing regions.

Another key restraint is the complexity and heterogeneity of waste streams. Waste composition varies significantly by region, season, and even within different types of facilities, making it challenging for robots to consistently and accurately sort a wide array of materials, especially highly commingled or contaminated waste. While AI is improving this, limitations in sensor technology and recognition algorithms can still lead to errors or reduced efficiency for highly complex or novel materials. Additionally, concerns regarding potential job displacement due to automation can lead to social and political resistance, further slowing down market penetration in some areas.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Capital Investment | -3.0% | Global, particularly Developing Economies | Short-to-Mid-term (2025-2030) |

| Complexity and Heterogeneity of Waste Streams | -2.5% | Global | Ongoing (2025-2033) |

| Lack of Standardized Infrastructure and Data | -1.8% | Varying by Region, less in Developed Countries | Long-term (2028-2033) |

| Concerns Over Job Displacement | -1.2% | Regions with strong labor unions, specific developing countries | Mid-term (2027-2031) |

| Maintenance and Operational Costs | -0.8% | Global | Ongoing (2025-2033) |

Waste Sorting Robot Market Opportunities Analysis

Significant opportunities abound in the Waste Sorting Robot market, driven by evolving waste streams and the increasing global emphasis on resource recovery. One major area of growth lies in the expansion into new types of waste, such as electronic waste (e-waste), hazardous waste, and specialized industrial waste. These streams often contain valuable materials that are difficult or dangerous to sort manually, making robotic solutions highly appealing. Developing specialized robots for these niche but high-value segments presents a substantial market opportunity, particularly as regulations around these waste types become more stringent.

Furthermore, emerging economies, particularly in Asia Pacific and Latin America, represent untapped markets with rapidly growing waste volumes and a nascent recycling infrastructure. These regions are increasingly seeking efficient and scalable waste management solutions, offering significant potential for market entry and expansion for robotic sorting system providers. Government initiatives, subsidies, and incentives aimed at promoting recycling and sustainable waste management practices also create fertile ground for market growth, encouraging both the adoption of existing technologies and the development of innovative solutions that cater to regional needs. Partnerships between technology providers, waste management companies, and research institutions can further accelerate innovation and market penetration, addressing specific challenges and unlocking new applications.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into E-waste and Hazardous Waste Sorting | +4.0% | Global, particularly developed nations with high tech consumption | Mid-to-Long-term (2027-2033) |

| Untapped Markets in Emerging Economies | +3.5% | Asia Pacific, Latin America, parts of Africa | Long-term (2028-2033) |

| Government Initiatives and Incentives for Recycling | +3.2% | Europe, North America, Japan, China, India | Ongoing (2025-2033) |

| Integration with Smart City and IoT Waste Management Systems | +2.5% | Developed Urban Centers Globally | Long-term (2029-2033) |

| Development of Modular and Customizable Solutions | +2.0% | Global | Short-to-Mid-term (2025-2029) |

Waste Sorting Robot Market Challenges Impact Analysis

The Waste Sorting Robot market faces several critical challenges that can impede its growth and widespread adoption. One significant challenge is the highly diverse and often unpredictable nature of waste streams. Robots must be able to recognize and differentiate an enormous variety of materials, including different types of plastics, metals, glass, and organic matter, often in varying states of contamination, wear, or degradation. This complexity demands highly sophisticated sensor technology and advanced AI algorithms, which are costly to develop and implement, and can still struggle with novel or highly commingled items.

Another major challenge involves the high operational costs associated with maintenance, spare parts, and the need for specialized technical expertise to manage these complex systems. Ensuring continuous uptime and peak performance requires regular calibration, software updates, and potential repairs, which can be expensive and require skilled technicians who are not always readily available in all regions. Additionally, the integration of robots into existing waste management infrastructures can be challenging, often requiring significant modifications to layouts, conveyor systems, and data management protocols, which adds to the overall cost and complexity of deployment.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complexity of Diverse and Contaminated Waste Streams | -2.8% | Global | Ongoing (2025-2033) |

| High Maintenance and Operational Costs | -2.2% | Global | Ongoing (2025-2033) |

| Integration Challenges with Existing Infrastructure | -1.5% | Global, particularly older facilities | Short-to-Mid-term (2025-2030) |

| Data Privacy and Security for Waste Composition Data | -1.0% | Europe, North America (due to stricter regulations) | Long-term (2029-2033) |

| Lack of Skilled Workforce for Operation and Maintenance | -0.7% | Developing Economies, Rural Areas | Mid-to-Long-term (2027-2033) |

Waste Sorting Robot Market - Updated Report Scope

This report provides a detailed and comprehensive analysis of the global Waste Sorting Robot market, offering an in-depth examination of market dynamics, growth drivers, restraints, opportunities, and challenges across various segments and key regions. It quantifies the market size and presents a precise forecast through 2033, enabling stakeholders to make informed strategic decisions. The scope covers technological advancements, the impact of artificial intelligence, competitive landscapes, and regional market specificities, designed to deliver actionable insights into the future trajectory of the waste sorting robotics industry.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 450 Million |

| Market Forecast in 2033 | USD 2.29 Billion |

| Growth Rate | 22.5% |

| Number of Pages | 255 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | RoboSort Solutions, WasteTech Robotics, EcoBot Innovations, GreenCycle Automation, Visionary Robotics, RecycloMech Systems, Smart Waste Robotics, OptiSort AI, EnviroRobotics Corp, Purity Automation, OmniRecycle Tech, FutureSort Systems, CleanStream Robotics, WasteWise Automation, Intelligent Sorting Solutions, Global Robotics Waste, Synergy Robotics, InnovateSort. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Waste Sorting Robot market is comprehensively segmented to provide a granular understanding of its diverse applications and technological nuances. This segmentation allows for detailed analysis of market performance across different robot types, sorting mechanisms, applications, end-users, and the specific types of materials being sorted. Understanding these segments is crucial for identifying niche markets, pinpointing specific technological demands, and tailoring solutions to meet varying operational requirements across the waste management value chain. Each segment represents distinct market dynamics influenced by regional regulations, economic conditions, and waste composition.

The categorization by robot type, such as articulated or collaborative robots, reflects the evolving engineering and design principles aimed at optimizing performance for different sorting speeds and accuracies. Similarly, segmenting by sorting mechanism, like optical or AI-powered vision systems, highlights the technological backbone driving efficiency. The application and end-user segments clarify where these robots are deployed most effectively, ranging from large-scale Material Recovery Facilities to specialized industrial waste processors. Finally, the material sorted segmentation underscores the growing versatility of these robots in handling an increasingly complex and valuable array of recyclables.

- By Robot Type: Articulated Robots, SCARA Robots, Delta Robots, Collaborative Robots (Cobots), Other Robot Types.

- By Sorting Mechanism: Optical Sorters, AI-Powered Vision Systems, Gripper-Based Sorters, Pneumatic Sorters, Magnetic Sorters.

- By Application: Municipal Solid Waste (MSW) Sorting, Commercial & Industrial Waste Sorting, Construction & Demolition (C&D) Waste Sorting, Electronic Waste (E-waste) Sorting, Hazardous Waste Sorting, Medical Waste Sorting, Other Waste Applications.

- By End-User: Material Recovery Facilities (MRFs), Recycling Plants, Waste Management Companies, Industrial Facilities, Government and Public Sector.

- By Material Sorted: Plastics (PET, HDPE, PVC, LDPE, PP, PS, Other Plastics), Metals (Ferrous, Non-Ferrous), Paper & Cardboard, Glass, Organics, Textiles, Wood, Rubber, Mixed Waste.

Regional Highlights

- North America: This region is a significant market for waste sorting robots, driven by high labor costs, increasing adoption of automation technologies, and stringent environmental regulations promoting recycling. The United States and Canada are leading in implementing advanced robotic solutions in MRFs and recycling facilities.

- Europe: Europe stands as a pioneering market due to its robust circular economy initiatives, ambitious recycling targets, and strong governmental support for sustainable waste management. Germany, France, and the UK are at the forefront of adopting sophisticated waste sorting robot technologies.

- Asia Pacific (APAC): Expected to be the fastest-growing region, fueled by rapid industrialization, urbanization, massive waste generation, and developing waste management infrastructure. China, Japan, South Korea, and India are investing heavily in modernizing their recycling capabilities, creating substantial demand.

- Latin America: This region presents emerging opportunities as countries like Brazil and Mexico grapple with growing waste volumes and are increasingly looking for cost-effective, efficient sorting solutions. Development of recycling infrastructure is a key driver for market entry.

- Middle East and Africa (MEA): While currently a smaller market, the MEA region is projected to experience growth as governments focus on economic diversification, sustainable development, and waste-to-energy initiatives, leading to increased investment in advanced waste processing technologies.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Waste Sorting Robot Market.- RoboSort Solutions

- WasteTech Robotics

- EcoBot Innovations

- GreenCycle Automation

- Visionary Robotics

- RecycloMech Systems

- Smart Waste Robotics

- OptiSort AI

- EnviroRobotics Corp

- Purity Automation

- OmniRecycle Tech

- FutureSort Systems

- CleanStream Robotics

- WasteWise Automation

- Intelligent Sorting Solutions

- Global Robotics Waste

- Synergy Robotics

- InnovateSort

Frequently Asked Questions

Analyze common user questions about the Waste Sorting Robot market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the projected growth of the waste sorting robot market?

The Waste Sorting Robot market is projected to grow at a Compound Annual Growth Rate (CAGR) of 22.5% between 2025 and 2033, reaching an estimated USD 2.29 Billion by 2033 from USD 450 Million in 2025.

How does AI enhance waste sorting robot capabilities?

AI significantly enhances capabilities by enabling superior material recognition, adaptive learning for various waste streams, optimized sorting strategies for higher throughput, reduced contamination rates, and predictive maintenance for operational efficiency.

What are the primary drivers for the waste sorting robot market?

Key drivers include the increasing global waste generation, stringent environmental regulations, rising labor costs and shortages in waste management, and continuous technological advancements in AI and robotics, coupled with a growing focus on the circular economy.

What challenges are faced in adopting waste sorting robots?

Challenges include high initial capital investment, the inherent complexity and heterogeneity of diverse waste streams, high ongoing maintenance and operational costs, integration difficulties with existing infrastructure, and concerns regarding potential job displacement.

Which regions are key players in the waste sorting robot market?

North America and Europe are leading markets due to strong regulatory frameworks and high automation adoption. Asia Pacific, particularly China and India, is poised for the fastest growth due to rapid urbanization and increasing waste volumes, alongside emerging opportunities in Latin America and MEA.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted