Gallium Nitride Semiconductor Device Market

Gallium Nitride Semiconductor Device Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_707522 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

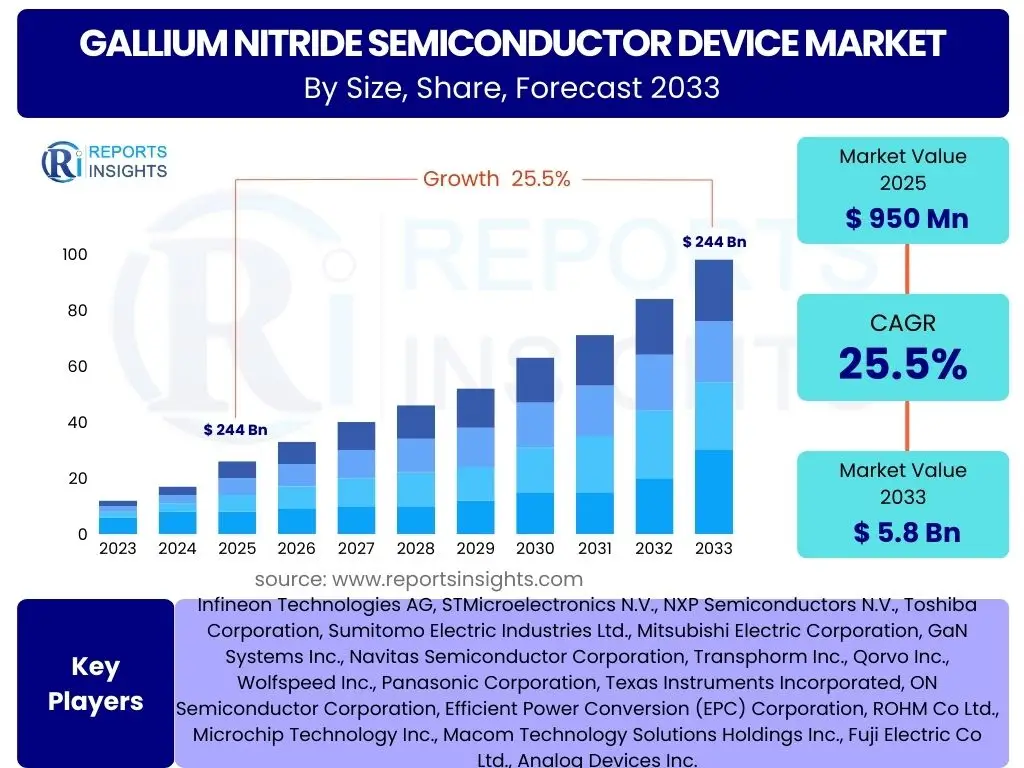

Gallium Nitride Semiconductor Device Market Size

According to Reports Insights Consulting Pvt Ltd, The Gallium Nitride Semiconductor Device Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 25.5% between 2025 and 2033. The market is estimated at USD 950 Million in 2025 and is projected to reach USD 5.8 Billion by the end of the forecast period in 2033.

Key Gallium Nitride Semiconductor Device Market Trends & Insights

User queries regarding market trends in Gallium Nitride (GaN) semiconductor devices consistently highlight the increasing demand for energy-efficient power solutions and the pervasive integration of advanced communication technologies. The market is experiencing a significant shift from traditional silicon-based devices due to GaN's superior performance characteristics, such as higher power density, faster switching speeds, and reduced energy losses. This transition is further accelerated by advancements in manufacturing processes, making GaN devices more cost-effective and scalable for various applications.

Another prominent trend involves the miniaturization of electronic components, particularly in consumer electronics and power adapters. GaN enables the design of smaller, lighter, and more powerful devices, directly addressing consumer preferences for portability and performance. Furthermore, the expansion of 5G networks globally is a critical driver, as GaN technology is essential for the high-frequency and high-power requirements of 5G base stations and associated infrastructure. The automotive sector's pivot towards electric vehicles (EVs) and hybrid electric vehicles (HEVs) also represents a substantial growth avenue, leveraging GaN for efficient onboard chargers, DC-DC converters, and traction inverters, contributing to improved vehicle range and performance.

- Growing adoption in power electronics for increased efficiency and reduced form factor.

- Rapid expansion fueled by 5G network infrastructure deployment.

- Significant integration into consumer electronics, particularly fast chargers and adapters.

- Increasing application in electric vehicles (EVs) for power conversion and management.

- Continuous advancements in GaN-on-Si technology, lowering production costs.

AI Impact Analysis on Gallium Nitride Semiconductor Device

User inquiries about Artificial Intelligence's (AI) impact on Gallium Nitride semiconductor devices frequently explore how AI can optimize design processes, enhance manufacturing efficiency, and unlock new application areas. AI-driven simulation and modeling tools are revolutionizing the design phase, allowing engineers to predict device performance more accurately, identify potential failure points, and optimize material structures for enhanced power efficiency and thermal management. This leads to faster development cycles and the creation of more robust and reliable GaN products, significantly reducing the time-to-market for complex designs.

In manufacturing, AI and machine learning algorithms are being employed for predictive maintenance, quality control, and process optimization within GaN fabrication facilities. By analyzing vast datasets from production lines, AI can detect anomalies, fine-tune equipment settings, and reduce waste, thereby improving yield rates and lowering overall production costs. Beyond manufacturing, AI applications themselves are driving demand for high-performance GaN devices. Data centers supporting AI workloads require immense power, and GaN power management units offer the efficiency and density needed to sustain these energy-intensive operations. Furthermore, the integration of AI into advanced robotics, autonomous systems, and edge computing devices creates new opportunities for compact, high-power-density GaN components.

- AI-driven design optimization for improved GaN device performance and efficiency.

- Enhanced manufacturing processes through AI for yield improvement and cost reduction.

- Increased demand for GaN power solutions in AI data centers and high-performance computing.

- AI integration in smart grid management leveraging GaN for efficient power distribution.

- Development of intelligent power modules incorporating GaN for autonomous systems.

Key Takeaways Gallium Nitride Semiconductor Device Market Size & Forecast

Common user questions regarding key takeaways from the Gallium Nitride semiconductor device market forecast highlight the impressive growth trajectory and the underlying drivers that will sustain this expansion. A primary insight is the market's robust compound annual growth rate, significantly outpacing many other semiconductor segments. This growth is not merely speculative but is anchored by tangible demand from high-growth industries such as 5G, electric vehicles, and high-efficiency power adapters for consumer electronics. The technological superiority of GaN over silicon in specific applications, coupled with continuous advancements in cost reduction and manufacturing scalability, positions it for long-term market penetration.

Another crucial takeaway revolves around the strategic investments being made by major semiconductor players and emerging startups in GaN technology. This includes research and development into new materials, packaging solutions, and integrated circuit designs, indicating a strong commitment to expanding GaN's capabilities and applications. The forecast also suggests a global diversification of demand, with significant growth projected across North America, Europe, and especially the Asia Pacific region, driven by large-scale infrastructure projects and manufacturing hubs. Understanding these geographical hotspots and the specific application segments driving their growth is vital for market participants seeking to capitalize on the emerging opportunities within the GaN ecosystem.

- The GaN market exhibits exceptional growth potential, driven by technological advantages and diverse applications.

- Strong demand from sectors like 5G telecommunications, electric vehicles, and consumer electronics is foundational to market expansion.

- Ongoing innovation in GaN-on-silicon technology is critical for reducing manufacturing costs and expanding market adoption.

- Geographic diversification of growth is expected, with APAC, North America, and Europe leading in adoption and investment.

- Strategic partnerships and investments in research and development are accelerating GaN's market penetration and maturity.

Gallium Nitride Semiconductor Device Market Drivers Analysis

The Gallium Nitride (GaN) semiconductor device market is propelled by a confluence of technological advancements and increasing demands for energy efficiency across various industries. A significant driver is the widespread deployment of 5G infrastructure, which necessitates high-frequency, high-power, and highly efficient power amplifiers and base station components that GaN can uniquely provide. Simultaneously, the global push towards electric vehicles (EVs) and hybrid electric vehicles (HEVs) is fueling demand for GaN-based power electronics due to their ability to enhance power conversion efficiency, reduce component size and weight, and extend battery range. These factors collectively underscore GaN's pivotal role in enabling next-generation technologies while addressing critical energy conservation goals.

The consumer electronics segment also plays a vital role, particularly with the proliferation of fast chargers for smartphones, laptops, and other portable devices. GaN allows for the creation of smaller, lighter, and more efficient power adapters, meeting consumer preferences for compact designs and rapid charging capabilities. Furthermore, the increasing focus on green energy solutions and smart grid applications globally is driving the adoption of GaN in renewable energy systems, such as solar inverters and energy storage systems, where high efficiency and reliability are paramount. These diverse applications, coupled with ongoing innovations that reduce manufacturing costs and improve device performance, form the bedrock of the GaN market's vigorous expansion.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing 5G Infrastructure Deployment | +5.5% | Global, particularly APAC (China, South Korea), North America | 2025-2033 |

| Rising Adoption in Electric Vehicles (EVs) | +4.8% | Europe (Germany, Norway), North America (USA), APAC (China, Japan) | 2026-2033 |

| Demand for High-Efficiency Power Electronics | +4.2% | Global, especially Consumer Electronics (China, USA), Industrial (Germany, Japan) | 2025-2033 |

| Miniaturization in Consumer Electronics | +3.9% | APAC (China, South Korea), North America (USA) | 2025-2030 |

| Advancements in Renewable Energy Systems | +3.1% | Europe (Germany), APAC (China, India), North America (USA) | 2027-2033 |

Gallium Nitride Semiconductor Device Market Restraints Analysis

Despite its significant advantages, the Gallium Nitride (GaN) semiconductor device market faces several restraints that could potentially temper its growth. One primary challenge is the relatively high manufacturing cost associated with GaN devices compared to established silicon-based counterparts. While prices are decreasing, the initial investment in GaN fabrication facilities and the complexity of certain epitaxy processes can still pose a barrier to widespread adoption, particularly in cost-sensitive applications. This cost differential often leads manufacturers to weigh the performance benefits against the economic feasibility of transitioning from mature silicon technologies, especially for applications where silicon still offers acceptable performance.

Another significant restraint is the ongoing competition from silicon carbide (SiC) devices, particularly in high-power and high-voltage applications like electric vehicle powertrains and industrial power supplies. While GaN excels in high-frequency applications, SiC often holds an advantage in extremely high-voltage and high-current scenarios, creating a competitive landscape where both wide-bandgap materials vie for market share. Furthermore, a perceived lack of standardization in GaN device packaging and reliability testing methodologies can create hesitancy among some potential adopters, as industry players seek established, robust, and universally accepted frameworks for integration and deployment. Addressing these cost, competition, and standardization issues is crucial for accelerating GaN's market penetration.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Higher Manufacturing Costs Compared to Silicon | -2.5% | Global, particularly in emerging economies | 2025-2028 |

| Competition from Silicon Carbide (SiC) Devices | -1.8% | Global, specifically in high-power EV and industrial applications | 2025-2033 |

| Perceived Reliability and Qualification Concerns | -1.5% | Global, especially among conservative industries (e.g., aerospace, defense) | 2025-2029 |

| Limited Public Awareness and Design Expertise | -1.0% | Developing regions, smaller enterprises | 2025-2027 |

Gallium Nitride Semiconductor Device Market Opportunities Analysis

The Gallium Nitride (GaN) semiconductor device market is ripe with opportunities stemming from emerging technological requirements and expanding application areas. A significant opportunity lies in the development of highly integrated GaN power ICs that combine power switches, drivers, and control logic onto a single chip. This integration reduces component count, simplifies design, and further enhances the performance and efficiency of power conversion systems, making GaN solutions even more appealing for compact and high-density applications across various sectors, including data centers and enterprise power supplies. Such advancements cater to the growing demand for smaller, more efficient, and easier-to-implement power solutions.

Another promising avenue involves the expansion of GaN applications into new, high-growth markets beyond its current primary uses. This includes the aerospace and defense sector, where GaN's radiation hardness and high-temperature performance are valuable for satellite communications and radar systems. Furthermore, the medical device industry presents opportunities for GaN in portable diagnostic equipment and high-frequency power supplies for imaging, leveraging GaN's compact size and efficiency. The ongoing investment in GaN-on-silicon technology also represents a critical opportunity, as it leverages existing silicon foundries to significantly scale production and further drive down costs, accelerating the transition from silicon and expanding the overall addressable market for GaN devices globally.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Integrated GaN Power ICs | +4.0% | Global, particularly North America, APAC (Japan, South Korea) | 2026-2033 |

| Expansion into New High-Growth Markets (Aerospace, Medical) | +3.5% | North America, Europe, APAC | 2027-2033 |

| Advancements in GaN-on-Silicon Technology | +3.2% | Global, especially in regions with strong semiconductor manufacturing (APAC, USA) | 2025-2031 |

| Government Initiatives for Energy Efficiency and Green Technology | +2.8% | Europe, North America, China | 2025-2033 |

Gallium Nitride Semiconductor Device Market Challenges Impact Analysis

The Gallium Nitride (GaN) semiconductor device market, while promising, faces several inherent challenges that require innovative solutions for sustained growth. One significant hurdle is the technical complexity associated with manufacturing high-quality GaN epitaxial layers on large-diameter substrates, particularly for GaN-on-silicon technology. Achieving uniform material properties and minimizing crystal defects across larger wafers is critical for high-volume production and yield improvement, and ongoing research is necessary to overcome these material science limitations. This complexity can affect consistency and lead to higher defect rates if not managed effectively.

Another challenge is the relatively limited ecosystem of design tools, packaging solutions, and testing methodologies specifically optimized for GaN devices compared to the mature silicon ecosystem. This can slow down the design and adoption cycle for new GaN applications as engineers require specialized expertise and infrastructure. Furthermore, the supply chain for GaN raw materials and specialized processing equipment can be less diversified and more vulnerable to disruptions than that for silicon, posing risks to production continuity and cost stability. Addressing these technical, ecosystem, and supply chain challenges is crucial for unlocking the full potential and ensuring the long-term viability of the GaN semiconductor market.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Technical Challenges in Material Growth and Epitaxy | -2.0% | Global, affecting all manufacturing regions | 2025-2029 |

| Supply Chain Vulnerabilities for GaN Substrates and Materials | -1.7% | Global, dependent on key material suppliers | 2025-2027 |

| Lack of Standardized Design and Packaging Solutions | -1.3% | Global, impacting wider adoption | 2025-2028 |

| Talent Shortage in GaN-Specific Engineering Expertise | -1.0% | North America, Europe, parts of APAC | 2025-2030 |

Gallium Nitride Semiconductor Device Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global Gallium Nitride (GaN) semiconductor device market, offering a detailed segmentation and regional breakdown. It covers the market's historical performance, current size, and future growth projections, alongside a thorough examination of key trends, drivers, restraints, opportunities, and challenges influencing the industry. The report also highlights the impact of emerging technologies like AI and profiles leading market players to provide a holistic view for strategic decision-making.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 950 Million |

| Market Forecast in 2033 | USD 5.8 Billion |

| Growth Rate | 25.5% |

| Number of Pages | 267 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Infineon Technologies AG, STMicroelectronics N.V., NXP Semiconductors N.V., Toshiba Corporation, Sumitomo Electric Industries Ltd., Mitsubishi Electric Corporation, GaN Systems Inc., Navitas Semiconductor Corporation, Transphorm Inc., Qorvo Inc., Wolfspeed Inc., Panasonic Corporation, Texas Instruments Incorporated, ON Semiconductor Corporation, Efficient Power Conversion (EPC) Corporation, ROHM Co Ltd., Microchip Technology Inc., Macom Technology Solutions Holdings Inc., Fuji Electric Co Ltd., Analog Devices Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Gallium Nitride (GaN) semiconductor device market is comprehensively segmented to provide a detailed understanding of its diverse applications and product types. This segmentation allows for precise market analysis, identifying high-growth areas and key technological advancements within each category. The primary segmentation involves device types, distinguishing between power semiconductors, RF devices, and opto-semiconductors, each catering to distinct performance requirements and end-use applications.

Further granularity is achieved by segmenting based on wafer size, which reflects manufacturing capabilities and cost efficiencies, with a growing trend towards larger wafer diameters like 8-inch for higher volume production. Application-based segmentation provides insight into where GaN technology is making the most significant impact, ranging from ubiquitous consumer electronics to highly specialized aerospace and defense systems. Finally, the end-use industry segmentation provides a macro view of the sectors driving adoption, highlighting the profound shift towards GaN in IT & Telecom, Automotive, and Renewable Energy industries due to its superior efficiency and performance attributes.

- By Device Type: Power Semiconductors (Transistors (HEMTs, MIS-HEMTs, SGTs), Diodes (Schottky, PN Junction)), RF Devices (Amplifiers, Switches, Filters), Opto-semiconductors (LEDs, Lasers)

- By Wafer Size: 2-inch, 4-inch, 6-inch, 8-inch, Others (12-inch)

- By Application: Power Supply & Conversion, RF & Microwave, Lighting & Displays, Automotive & EV, Consumer Electronics, Industrial, Telecommunications, Aerospace & Defense, Medical, Data Centers, Others

- By End-Use Industry: IT & Telecom, Automotive, Consumer Electronics, Industrial & Power, Medical, Aerospace & Defense, Renewable Energy, Data Communication, Military

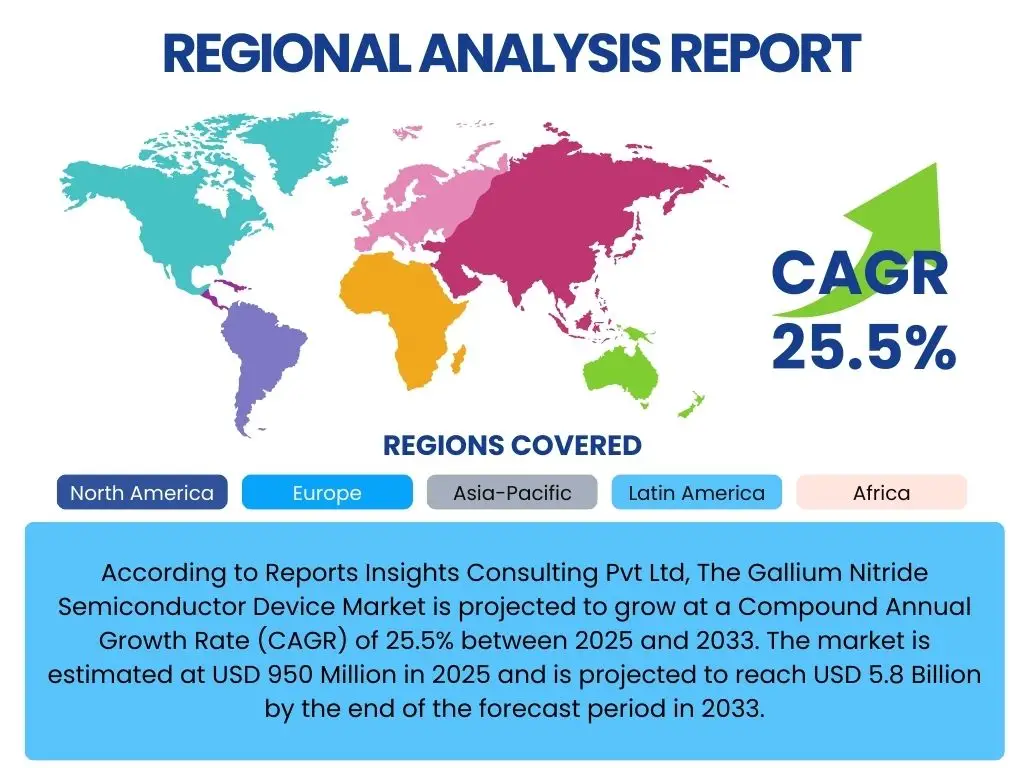

Regional Highlights

The global Gallium Nitride (GaN) semiconductor device market exhibits significant regional variations in terms of adoption, production capabilities, and strategic investments. Asia Pacific (APAC) is projected to dominate the market, primarily driven by robust economic growth, extensive investments in 5G infrastructure, and a thriving consumer electronics manufacturing base, particularly in China, South Korea, and Japan. These countries are at the forefront of GaN technology adoption for fast chargers, data centers, and telecommunication equipment. The region also benefits from a large automotive manufacturing sector that is increasingly integrating GaN into Electric Vehicles (EVs) for enhanced power efficiency and extended range. Government initiatives promoting domestic semiconductor industries and energy efficiency further bolster market growth in this region.

North America is another key market, characterized by strong research and development activities, significant defense and aerospace expenditures, and a growing demand for high-performance computing and data center solutions. The United States leads in innovation for GaN in RF applications, especially for radar and military communications. The region's increasing focus on renewable energy and the development of smart grid technologies also contribute to the adoption of GaN power devices. Europe is steadily expanding its GaN market share, propelled by stringent energy efficiency regulations, a strong automotive industry emphasizing EV innovation, and significant investments in industrial power applications. Countries like Germany and France are particularly active in adopting GaN for industrial power supplies and renewable energy systems.

Latin America and the Middle East & Africa (MEA) are emerging markets for GaN technology, albeit at a slower pace compared to the developed regions. Growth in these areas is primarily driven by increasing investments in telecommunications infrastructure, especially the rollout of 5G networks, and a gradual shift towards adopting more energy-efficient power solutions in industrial and commercial sectors. While currently smaller in market size, these regions present long-term growth opportunities as their technological infrastructure develops and awareness of GaN's benefits increases, particularly in areas requiring robust and efficient power management for expanding urban and industrial developments.

- Asia Pacific (APAC): Dominant market share driven by 5G rollout, consumer electronics manufacturing hubs (China, South Korea), and expanding EV production (China, Japan).

- North America: Strong growth due to R&D investments, defense and aerospace applications (USA), and demand from data centers and high-performance computing.

- Europe: Significant adoption fueled by strict energy efficiency standards, robust automotive industry (Germany, France), and industrial power applications.

- Latin America & Middle East & Africa (MEA): Emerging markets with increasing investments in telecommunications infrastructure (5G) and gradual adoption in industrial and commercial power sectors.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Gallium Nitride Semiconductor Device Market.- Infineon Technologies AG

- STMicroelectronics N.V.

- NXP Semiconductors N.V.

- Toshiba Corporation

- Sumitomo Electric Industries Ltd.

- Mitsubishi Electric Corporation

- GaN Systems Inc.

- Navitas Semiconductor Corporation

- Transphorm Inc.

- Qorvo Inc.

- Wolfspeed Inc.

- Panasonic Corporation

- Texas Instruments Incorporated

- ON Semiconductor Corporation

- Efficient Power Conversion (EPC) Corporation

- ROHM Co Ltd.

- Microchip Technology Inc.

- Macom Technology Solutions Holdings Inc.

- Fuji Electric Co Ltd.

- Analog Devices Inc.

Frequently Asked Questions

Analyze common user questions about the Gallium Nitride Semiconductor Device market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is Gallium Nitride (GaN) and how does it differ from Silicon?

Gallium Nitride (GaN) is a wide-bandgap semiconductor material offering superior electronic properties compared to traditional Silicon. It can operate at higher temperatures and voltages, switch much faster, and handle more power in a smaller footprint. Unlike Silicon, which has a smaller bandgap, GaN's larger bandgap enables higher breakdown voltage and lower on-resistance, leading to significantly reduced energy losses and greater efficiency in power conversion.

What are the primary applications of Gallium Nitride semiconductor devices?

GaN semiconductor devices are primarily used in applications requiring high efficiency, high power density, and high-frequency operation. Key applications include fast chargers and power adapters for consumer electronics, power conversion systems in electric vehicles (EVs), 5G telecommunications infrastructure (e.g., base stations, RF amplifiers), solar inverters for renewable energy, data center power supplies, and various industrial power electronics. Its versatility enables significant performance improvements across these diverse sectors.

What are the main advantages of using GaN over Silicon in power electronics?

The main advantages of GaN over Silicon in power electronics include significantly higher switching speeds, leading to smaller passive components and reduced system size. GaN devices also exhibit lower conduction losses and superior thermal performance, resulting in higher power efficiency and less heat generation. This translates to smaller, lighter, more energy-efficient, and often more cost-effective power solutions at the system level, despite a potentially higher component cost.

What challenges does the GaN semiconductor device market face?

Despite its advantages, the GaN market faces challenges such as relatively higher manufacturing costs compared to mature silicon technologies, competition from other wide-bandgap materials like Silicon Carbide (SiC) in specific high-power applications, and the need for further standardization in packaging and reliability testing. Additionally, technical complexities in material growth and a less established supply chain compared to silicon can pose hurdles for widespread adoption and scalability.

What is the future outlook for the Gallium Nitride semiconductor device market?

The future outlook for the Gallium Nitride semiconductor device market is highly positive, projecting robust growth driven by continuous technological advancements and expanding adoption across critical industries. Innovations in GaN-on-silicon technology are expected to further reduce manufacturing costs and enhance scalability. The increasing global demand for energy-efficient solutions, coupled with the rapid deployment of 5G networks and the accelerating electrification of the automotive sector, positions GaN as a pivotal technology for next-generation power and RF applications.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted