Blade Server Market

Blade Server Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703951 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

Blade Server Market Size

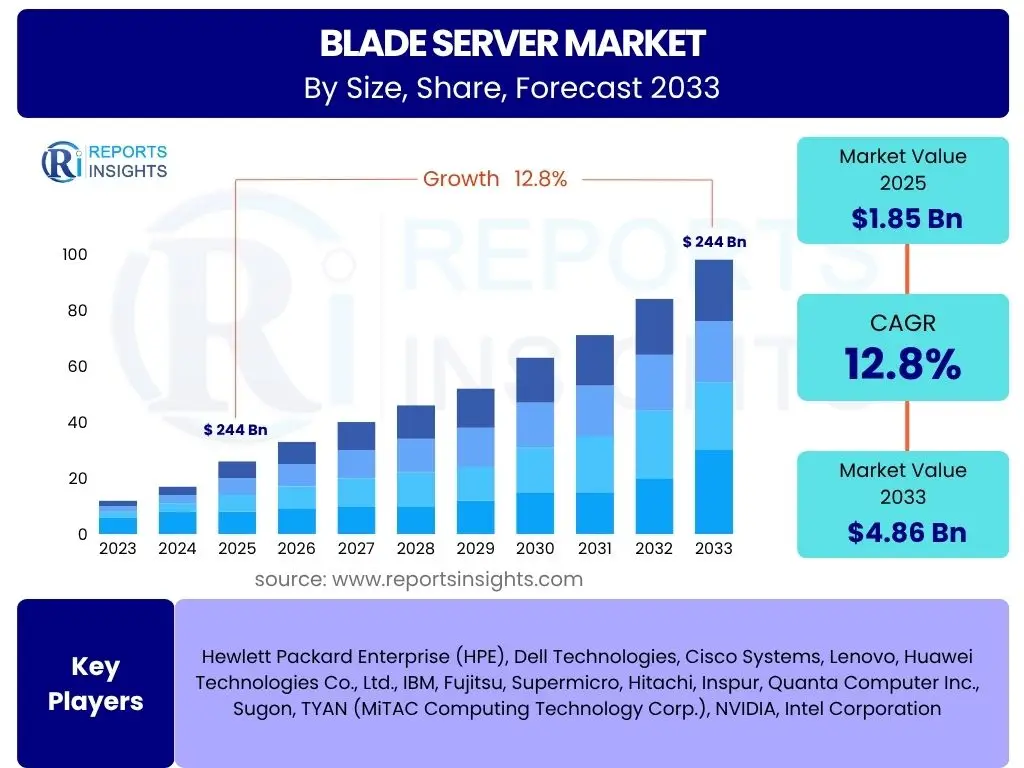

According to Reports Insights Consulting Pvt Ltd, The Blade Server Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.8% between 2025 and 2033. The market is estimated at USD 1.85 Billion in 2025 and is projected to reach USD 4.86 Billion by the end of the forecast period in 2033.

Key Blade Server Market Trends & Insights

The Blade Server market is experiencing significant transformation driven by the escalating demand for high-density computing and optimized data center infrastructure. Current trends indicate a strong focus on modularity, energy efficiency, and enhanced manageability, reflecting a broader industry shift towards more sustainable and scalable IT solutions. Organizations are increasingly seeking solutions that can support complex workloads while minimizing physical footprint and operational costs, making blade servers a compelling option for a wide array of applications.

User queries frequently highlight interest in next-generation blade designs, the integration of advanced cooling technologies, and the evolution of software-defined infrastructure within blade environments. There is a clear emphasis on how blade servers can adapt to future computing paradigms, including artificial intelligence and edge deployments, necessitating innovations in form factor, power delivery, and connectivity. This forward-looking perspective suggests that the market will continue to prioritize flexibility and performance density in its development.

- Increased adoption of high-density computing architectures for data centers.

- Growing demand for energy-efficient server solutions to reduce operational costs.

- Expansion of modular and scalable infrastructure for cloud and enterprise environments.

- Integration of advanced liquid cooling technologies to manage higher thermal loads.

- Emphasis on software-defined networking and storage within blade ecosystems.

- Development of specialized blade configurations for AI, ML, and HPC workloads.

AI Impact Analysis on Blade Server

The proliferation of Artificial Intelligence (AI) and Machine Learning (ML) workloads profoundly impacts the Blade Server market by driving demand for specialized, high-performance computing capabilities. AI applications, particularly deep learning models, necessitate immense computational power, often requiring thousands of processing cores and significant memory bandwidth. Blade servers, with their ability to consolidate substantial compute resources, including multiple GPUs and specialized accelerators, within a compact chassis, are uniquely positioned to meet these demanding requirements. This has led to a surge in the development of AI-optimized blade configurations featuring enhanced power delivery and thermal management solutions.

Common user questions revolve around the suitability of blade servers for AI, the integration of AI accelerators, and the future role of blade servers in AI-driven data centers. Users are keen to understand how blade infrastructure can facilitate efficient AI model training and inference at scale. Furthermore, AI's influence extends to the operational aspects of blade servers, enabling smarter resource orchestration, predictive maintenance, and autonomous workload management, thereby improving overall data center efficiency and reliability. The convergence of AI with blade server technology is creating new opportunities for high-density, intelligent infrastructure solutions.

- Increased demand for GPU-accelerated blade servers to handle AI/ML workloads.

- Development of specialized blade architectures optimized for AI inference and training.

- Enhanced power and cooling solutions within blade chassis to support high-density AI components.

- AI-driven optimization of resource allocation and workload scheduling in blade environments.

- Emergence of blade server deployments at the edge for localized AI processing.

- Demand for integrated management platforms to monitor and manage AI workloads on blade systems.

Key Takeaways Blade Server Market Size & Forecast

The forecast for the Blade Server market underscores a period of sustained growth, driven primarily by the ongoing need for data center modernization and the relentless expansion of digital services. Enterprises and cloud providers are increasingly migrating towards consolidated, high-density computing solutions to manage complex workloads efficiently. This trend is a clear indicator that blade servers, despite competition from other form factors, remain a critical component for organizations prioritizing space, power, and operational efficiency within their IT infrastructure.

A significant takeaway is the strategic importance of blade servers in supporting emerging technologies such as AI, edge computing, and 5G. Their modular design and ability to integrate specialized processors position them as a foundational technology for future-ready data centers. Stakeholders should focus on innovation in energy efficiency, thermal management, and software-defined capabilities to capitalize on this growth trajectory and address evolving customer requirements for agility and performance.

- The Blade Server market is poised for robust growth through 2033, driven by data center consolidation and digital transformation initiatives.

- High-density computing and operational efficiency remain primary motivators for blade server adoption across various industries.

- Integration with emerging technologies like AI, IoT, and edge computing presents significant expansion opportunities.

- Continuous innovation in power management, cooling solutions, and modular design is crucial for market competitiveness.

- Market participants should focus on delivering comprehensive solutions that include hardware, software, and managed services.

Blade Server Market Drivers Analysis

The Blade Server market is significantly propelled by several key drivers that reflect the evolving demands of modern IT infrastructure. The increasing need for data center consolidation and virtualization remains a primary catalyst, as organizations seek to reduce physical footprint, power consumption, and cooling costs while maximizing computational density. This drive for efficiency and optimized resource utilization inherently favors the modular, high-density design of blade servers, enabling businesses to deploy more computing power in less space.

Furthermore, the escalating demand for high-performance computing (HPC) across various sectors, including scientific research, financial modeling, and engineering simulations, is fueling blade server adoption. These applications require substantial processing capabilities and low-latency interconnects, which blade architectures are designed to provide. The growth of cloud computing and the deployment of hybrid cloud strategies also contribute to market expansion, as cloud service providers and enterprises leverage blade servers for their scalability and simplified management in dynamic environments.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Data Center Consolidation & Virtualization | +2.1% | North America, Europe, Asia Pacific | Short-term (2025-2027) |

| Rising Demand for High-Performance Computing (HPC) | +1.8% | Global, particularly developed economies | Medium-term (2028-2030) |

| Increasing Adoption of Cloud & Hybrid Cloud Models | +1.5% | Global | Medium-term (2028-2030) |

| Focus on Energy Efficiency & Reduced TCO | +1.2% | Global | Long-term (2031-2033) |

| Growth of Big Data Analytics & AI/ML Workloads | +2.0% | Global | Medium-term (2028-2030) |

Blade Server Market Restraints Analysis

Despite the numerous advantages, the Blade Server market faces several significant restraints that could temper its growth trajectory. One of the primary concerns for potential adopters is the high initial capital expenditure associated with implementing a comprehensive blade server infrastructure. While offering long-term operational efficiencies, the upfront cost of chassis, blades, networking modules, and management software can be substantial, particularly for small to medium-sized enterprises (SMEs) with limited IT budgets.

Another notable restraint is the perceived complexity of managing and integrating blade server environments, especially for organizations without specialized IT staff. While modern blade systems offer centralized management tools, the initial setup, configuration, and ongoing maintenance of these integrated systems can present a steeper learning curve compared to traditional rack servers. Furthermore, the increasing popularity of hyper-converged infrastructure (HCI) and containerization technologies, which offer similar benefits of consolidation and simplified management, poses a competitive challenge, potentially diverting investments away from dedicated blade solutions.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Capital Expenditure | -1.5% | Global, particularly emerging markets | Short-term (2025-2027) |

| Management Complexity & Specialized Skill Requirements | -1.0% | Global | Medium-term (2028-2030) |

| Competition from Hyper-Converged Infrastructure (HCI) | -1.3% | North America, Europe | Ongoing |

| Vendor Lock-in Concerns | -0.8% | Global | Long-term (2031-2033) |

| Rapid Technological Obsolescence | -0.7% | Global | Ongoing |

Blade Server Market Opportunities Analysis

The Blade Server market is ripe with opportunities driven by technological advancements and evolving enterprise needs. The advent of edge computing presents a significant growth avenue, as organizations increasingly require compact, high-performance, and remotely manageable computing solutions closer to data sources. Blade servers, with their integrated design and centralized management capabilities, are ideally suited for deploying compute infrastructure in distributed and resource-constrained edge environments, providing lower latency and reduced bandwidth requirements for real-time applications.

Another prominent opportunity lies in the continued integration of specialized processors and accelerators for emerging workloads, particularly in Artificial Intelligence (AI) and Machine Learning (ML). As AI applications become more sophisticated, the demand for high-density GPU-enabled blades and specialized AI inference engines will surge. Furthermore, the increasing adoption of sustainable IT practices and the push for greener data centers offer opportunities for innovation in energy-efficient blade designs and advanced cooling solutions, allowing manufacturers to differentiate their offerings and appeal to environmentally conscious customers seeking to optimize their power usage effectiveness (PUE).

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into Edge Computing Deployments | +1.8% | Global, developing regions | Medium-term (2028-2030) |

| Integration with AI/ML & Specialized Workloads | +2.2% | Global | Medium-term (2028-2030) |

| Development of Advanced Liquid Cooling Solutions | +1.0% | North America, Europe, Asia Pacific | Long-term (2031-2033) |

| Growth in Niche Applications (Telco, Defense, Healthcare) | +1.3% | Global | Ongoing |

| Managed Services & Hybrid IT Solutions | +1.1% | Global | Short-term (2025-2027) |

Blade Server Market Challenges Impact Analysis

The Blade Server market confronts several challenges that necessitate strategic responses from industry players. One significant hurdle is managing the escalating power and cooling demands within high-density blade environments. As processor power and component density increase, so does the heat output, requiring more sophisticated and often costly cooling infrastructure, which can offset some of the inherent space-saving benefits of blade systems. Ensuring efficient thermal management without significantly increasing operational expenses remains a critical challenge for wider adoption.

Another challenge stems from interoperability issues and potential vendor lock-in. While blade server ecosystems offer deep integration, they often rely on proprietary chassis, management software, and networking components, which can limit flexibility and choice for organizations. This can make it difficult to mix and match components from different vendors or to easily migrate away from a specific blade platform. Furthermore, the rapid pace of technological innovation in the server market, including the emergence of new processor architectures and server form factors, requires continuous R&D investment to maintain competitiveness, posing a financial and strategic challenge for manufacturers.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Managing Power & Cooling Density Limitations | -1.4% | Global | Ongoing |

| Interoperability & Vendor Lock-in Issues | -1.2% | Global | Short-term (2025-2027) |

| Competition from Converged/Hyper-Converged Infrastructure | -1.6% | North America, Europe | Ongoing |

| Skilled Workforce Shortage for Complex Deployments | -0.9% | Global | Medium-term (2028-2030) |

| Balancing Cost-Effectiveness with Performance | -0.8% | Global | Ongoing |

Blade Server Market - Updated Report Scope

This report provides an in-depth analysis of the global Blade Server market, offering comprehensive insights into market size, growth trends, key drivers, restraints, opportunities, and challenges across various segments and regions. It includes a detailed competitive landscape, profiling key industry players and their strategies, alongside a robust forecast period from 2025 to 2033. The report is designed to assist stakeholders in understanding market dynamics, identifying growth avenues, and making informed strategic decisions within the evolving server infrastructure landscape.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.85 Billion |

| Market Forecast in 2033 | USD 4.86 Billion |

| Growth Rate | 12.8% CAGR |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Hewlett Packard Enterprise (HPE), Dell Technologies, Cisco Systems, Lenovo, Huawei Technologies Co., Ltd., IBM, Fujitsu, Supermicro, Hitachi, Inspur, Quanta Computer Inc., Sugon, TYAN (MiTAC Computing Technology Corp.), NVIDIA, Intel Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Blade Server market is comprehensively segmented to provide a granular view of its various components, applications, and technological specifications. This segmentation enables a detailed understanding of market dynamics, allowing for targeted analysis of specific product types, end-user industries, and regional adoption patterns. Understanding these segments is crucial for stakeholders to identify niche opportunities, assess competitive landscapes, and tailor their product development and marketing strategies to specific market demands.

The breakdown by component helps in analyzing the revenue contribution and growth of distinct parts of a blade system, from the core server blades to the necessary supporting infrastructure like chassis, networking, and management software. Application-based segmentation highlights the primary industries driving demand for blade servers, indicating where these high-density solutions offer the most value. Furthermore, processor type segmentation reflects the technological preferences and architectural trends influencing hardware choices within the blade server ecosystem, offering insights into the evolving performance and power efficiency demands across different computing environments.

- By Component:

- Server Chassis

- Server Blades

- Network Blades

- Storage Blades

- Management Software & Tools

- Power & Cooling Systems

- By Processor Type:

- Intel-based

- AMD-based

- ARM-based

- Others

- By Application:

- Enterprise Data Centers

- Cloud Service Providers

- Telecommunications

- Government & Defense

- BFSI (Banking, Financial Services, and Insurance)

- Healthcare

- Media & Entertainment

- Manufacturing

- Research & Academia

- Others

- By Blade Height:

- Half-height Blades

- Full-height Blades

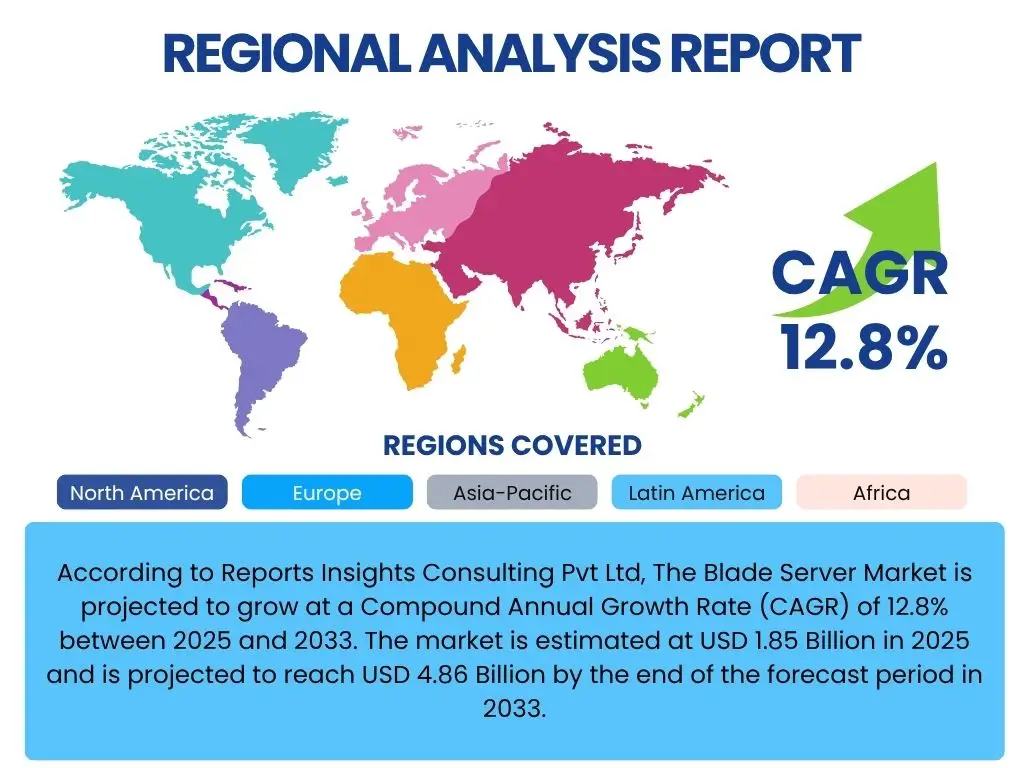

Regional Highlights

- North America: This region holds a significant share of the Blade Server market, characterized by early technology adoption, the presence of major cloud service providers, and a high concentration of large enterprise data centers. The continuous demand for data center modernization, adoption of virtualization, and the increasing push for high-performance computing in sectors like finance and healthcare drive market growth.

- Europe: The European market is marked by a strong emphasis on data privacy regulations and sustainability initiatives, driving demand for energy-efficient and secure blade server solutions. Germany, the UK, and France are key contributors, with growth fueled by digital transformation across various industries and expanding cloud infrastructure.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing region, owing to rapid digital transformation, increasing internet penetration, and significant investments in data center infrastructure, particularly in emerging economies like China, India, and Southeast Asian countries. The expansion of e-commerce, cloud computing, and smart city initiatives further boosts market demand.

- Latin America: The market in Latin America is witnessing steady growth, primarily driven by increasing digitalization across enterprises and government sectors. Brazil and Mexico are key markets, with growing investments in cloud services and IT infrastructure upgrades contributing to the adoption of blade servers.

- Middle East and Africa (MEA): The MEA region is experiencing gradual growth, propelled by government initiatives aimed at economic diversification and technological advancements. Investments in smart cities, development of telecommunication infrastructure, and expansion of data centers, especially in the GCC countries and South Africa, are fostering blade server deployments.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Blade Server Market.- Hewlett Packard Enterprise (HPE)

- Dell Technologies

- Cisco Systems

- Lenovo

- Huawei Technologies Co., Ltd.

- IBM

- Fujitsu

- Supermicro

- Hitachi

- Inspur

- Quanta Computer Inc.

- Sugon

- TYAN (MiTAC Computing Technology Corp.)

- NVIDIA

- Intel Corporation

Frequently Asked Questions

What is a blade server?

A blade server is a stripped-down server computer designed to minimize the use of physical space and energy. It is essentially a single circuit board, or "blade," that contains processors, memory, and often integrated network controllers, storage, and other essential components. Multiple blades are inserted into a chassis that provides shared power, cooling, networking, and management infrastructure, allowing for high-density computing in a compact form factor.

Why are blade servers used?

Blade servers are primarily used in data centers and enterprise environments to achieve high computational density, reduce physical footprint, and optimize energy consumption. They are ideal for consolidating IT infrastructure, supporting virtualization, and running demanding applications like high-performance computing (HPC), database management, and cloud services where space and power efficiency are critical.

What are the advantages of blade servers?

Key advantages of blade servers include superior space efficiency due to their compact design, reduced power consumption and cooling requirements per unit of computation, centralized management for easier administration of multiple servers, and simplified cabling. Their modularity allows for flexible scaling and easy replacement or upgrade of individual components, leading to lower total cost of ownership (TCO) over time in suitable environments.

What are the disadvantages of blade servers?

Disadvantages of blade servers can include a higher initial capital expenditure compared to traditional rack servers, potential vendor lock-in due to proprietary chassis and management systems, and a learning curve for IT staff unfamiliar with their integrated architecture. While efficient, their high density can also lead to significant heat generation, requiring robust cooling solutions in the data center.

How do blade servers differ from rack servers?

Blade servers differ from rack servers primarily in their form factor and integration. Rack servers are standalone units, each with its own power supply, cooling, and network connections, mounted individually in a rack. Blade servers are modular components that share a common chassis providing power, cooling, and network connectivity, allowing for much higher density and centralized management within a single enclosure, making them more efficient for large-scale deployments.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted