OPC Server Software Market

OPC Server Software Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705573 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

OPC Server Software Market Size

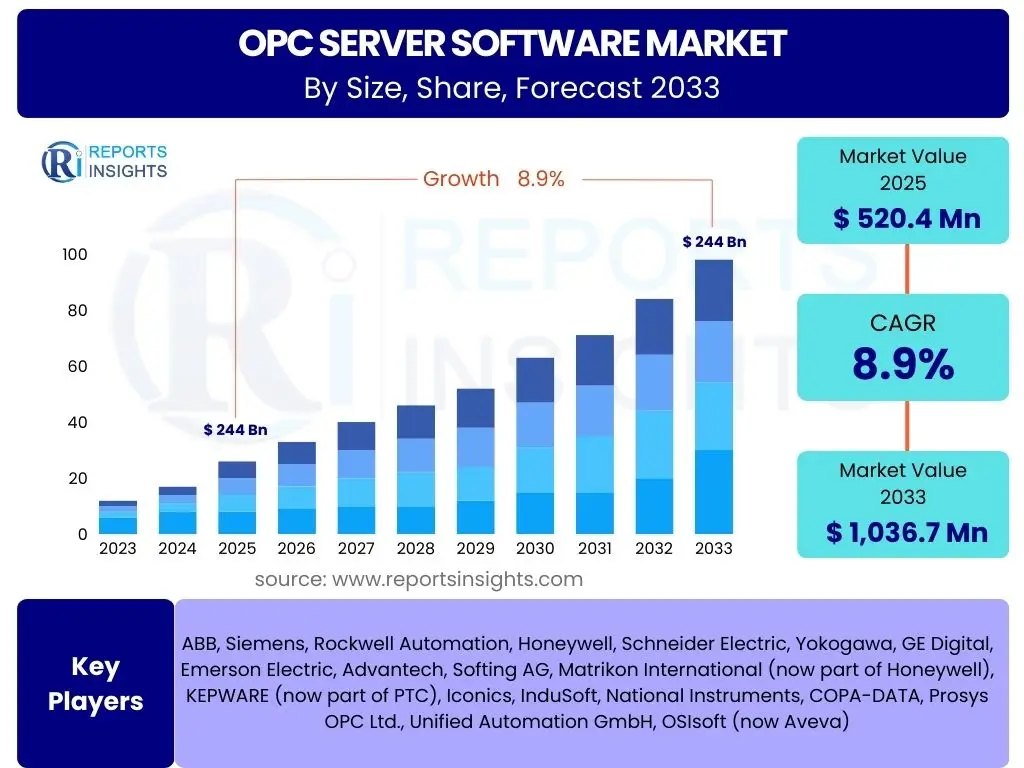

According to Reports Insights Consulting Pvt Ltd, The OPC Server Software Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.9% between 2025 and 2033. The market is estimated at USD 520.4 million in 2025 and is projected to reach USD 1,036.7 million by the end of the forecast period in 2033. This growth is primarily driven by the escalating demand for industrial automation, the proliferation of Industry 4.0 initiatives, and the critical need for seamless data exchange across diverse operational technology (OT) and information technology (IT) systems within manufacturing and process industries globally.

Key OPC Server Software Market Trends & Insights

The OPC Server Software market is undergoing significant transformation, driven by advancements in industrial connectivity and data management. Users are increasingly seeking solutions that offer enhanced interoperability, robust security, and seamless integration with emerging technologies. A major trend is the widespread adoption of OPC Unified Architecture (OPC UA) as the industry standard, moving beyond classic OPC specifications due to its platform independence, built-in security features, and expanded data modeling capabilities. This shift addresses long-standing challenges related to data silos and communication complexities in heterogeneous industrial environments.

Another prominent trend is the increasing demand for cloud-based and hybrid OPC solutions. Organizations are exploring how OPC Servers can facilitate data transfer from edge devices and on-premise systems to cloud platforms for advanced analytics, remote monitoring, and enterprise-level visibility. This move is driven by the need for greater flexibility, scalability, and reduced infrastructure overhead. Additionally, the integration of OPC Server Software with analytics platforms and Artificial Intelligence (AI) solutions is gaining traction, enabling predictive maintenance, operational optimization, and real-time decision-making for enhanced industrial efficiency and productivity.

- Dominance of OPC Unified Architecture (OPC UA) for future-proof connectivity.

- Rising adoption of cloud and hybrid deployment models for scalability and remote access.

- Enhanced focus on cybersecurity features within OPC implementations.

- Integration with advanced analytics, Big Data, and Artificial Intelligence (AI) platforms.

- Expansion of OPC into new industrial verticals beyond traditional manufacturing.

- Growth in edge computing architectures driving localized OPC deployments.

- Demand for standardized data modeling and information exchange across enterprises.

AI Impact Analysis on OPC Server Software

The integration of Artificial Intelligence (AI) is fundamentally reshaping the capabilities and applications of OPC Server Software, addressing common user questions about how AI can enhance operational intelligence. Users are keenly interested in how AI can move OPC beyond basic data transfer to enable proactive insights and autonomous operations. AI algorithms, when applied to data collected via OPC Servers, can identify complex patterns, predict equipment failures, and optimize production processes. This transition from reactive troubleshooting to predictive and prescriptive maintenance is a significant value proposition, allowing industries to minimize downtime, reduce operational costs, and improve overall asset utilization.

Furthermore, AI-driven analytics layered on OPC-collected data facilitates real-time decision-making and adaptive control. For instance, machine learning models can analyze historical and live OPC data streams to suggest optimal control parameters, adjust process flows, or detect anomalies that human operators might miss. This capability supports the development of more intelligent and autonomous industrial systems, enhancing efficiency and safety. While concerns exist regarding data privacy, computational overhead, and the complexity of AI model deployment, the overarching expectation among users is that AI will unlock new levels of performance and insight from their industrial data, making OPC Servers indispensable components of next-generation smart factories and interconnected industrial ecosystems.

- Enables predictive maintenance by analyzing real-time OPC data for anomaly detection.

- Optimizes industrial processes through AI-driven insights and adaptive control.

- Facilitates intelligent decision-making by providing actionable insights from operational data.

- Enhances cybersecurity by detecting unusual patterns in OPC communication.

- Supports autonomous operations and self-optimizing systems.

- Improves energy efficiency through AI-informed resource management.

Key Takeaways OPC Server Software Market Size & Forecast

The OPC Server Software market is poised for robust growth, reflecting its indispensable role in the evolving industrial landscape. Common inquiries revolve around the factors underpinning this growth and the long-term viability of OPC technology. The market's expansion is intrinsically linked to the global acceleration of digital transformation initiatives, the increasing complexity of industrial operations, and the pervasive adoption of smart manufacturing concepts. Businesses recognize that efficient and secure data exchange is foundational to achieving operational excellence, driving sustained investment in OPC solutions. The forecast indicates a steady upward trajectory, demonstrating the technology's continued relevance and adaptability to new industrial paradigms.

A significant takeaway is the pivotal shift towards OPC UA, which addresses critical enterprise-level requirements such as security, scalability, and semantic interoperability. This evolution ensures that OPC remains at the forefront of industrial communication standards, facilitating the convergence of OT and IT systems. The market's resilience is also attributed to its ability to support legacy systems while providing a pathway to advanced technologies like cloud computing, edge analytics, and AI. As industries continue to seek greater efficiency, flexibility, and data-driven insights, OPC Server Software will remain a cornerstone technology, underpinning the connectivity and intelligence required for modern industrial operations.

- Market demonstrates strong, sustained growth driven by digital transformation.

- OPC UA is the primary growth driver due to its advanced features and future compatibility.

- Investment in industrial automation and smart factories directly fuels market expansion.

- Critical for bridging the gap between operational technology (OT) and information technology (IT) systems.

- Demand for real-time data exchange and interoperability will continue to increase.

OPC Server Software Market Drivers Analysis

The OPC Server Software market is primarily propelled by the accelerating adoption of Industry 4.0 initiatives across various industrial sectors. This global movement emphasizes interconnectedness, real-time data exchange, and smart automation, all of which heavily rely on robust and standardized communication protocols. OPC Server Software, especially OPC UA, serves as a crucial enabler for these initiatives by providing the necessary interoperability between diverse industrial control systems, sensors, and enterprise applications. The demand for seamless data flow from the shop floor to the top floor drives organizations to invest in OPC solutions to unlock the full potential of their digital transformation strategies.

Furthermore, the escalating need for real-time data for operational efficiency and decision-making significantly contributes to market growth. Industries are increasingly recognizing that immediate access to accurate operational data is vital for optimizing production processes, enhancing asset performance, and implementing predictive maintenance strategies. OPC Servers facilitate this by enabling high-speed, secure, and reliable data acquisition from various industrial devices and systems. This capability empowers businesses to monitor, analyze, and control their operations with unprecedented granularity, leading to improved productivity, reduced downtime, and more informed strategic planning. The continuous drive for operational excellence across manufacturing, energy, and other critical infrastructure sectors underpins the sustained demand for OPC Server Software.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Industry 4.0 and Smart Manufacturing Initiatives | +1.5% | Global (Strong in Europe, APAC, North America) | Long-term (2025-2033) |

| Increasing Demand for Real-Time Data and Automation | +1.2% | Global | Medium-term (2025-2030) |

| Growth in IoT and Industrial IoT (IIoT) Deployment | +1.0% | Global (Emerging in APAC, Latin America) | Medium-term (2025-2030) |

| Need for Interoperability between OT and IT Systems | +0.8% | Global | Short to Medium-term (2025-2028) |

OPC Server Software Market Restraints Analysis

Despite the strong growth drivers, the OPC Server Software market faces certain restraints that could impede its expansion. One significant challenge is the complexity of integrating OPC solutions, particularly OPC UA, into existing legacy systems. Many industrial environments still operate with older proprietary systems and classic OPC DA/HDA/A&E implementations. Migrating or integrating these diverse systems with modern OPC UA frameworks can be costly, time-consuming, and require specialized expertise. This complexity often leads to resistance from companies hesitant to undertake significant overhauls of their operational infrastructure, thereby slowing down the adoption of newer OPC technologies and limiting market growth in certain segments.

Another notable restraint is the persistent concern regarding cybersecurity risks associated with interconnected industrial systems. As OPC Servers facilitate extensive data exchange between previously isolated networks and potentially with cloud environments, they become potential entry points for cyber threats. Data breaches, unauthorized access, and denial-of-service attacks pose significant risks to critical infrastructure and intellectual property. While OPC UA inherently includes robust security features, the proper implementation and ongoing management of these security measures require specialized knowledge and continuous vigilance. The fear of cybersecurity vulnerabilities can deter some organizations from fully embracing OPC-driven connectivity, especially in highly sensitive sectors, thereby acting as a brake on broader market penetration.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complexity of Integration with Legacy Systems | -0.7% | Global (More pronounced in mature industrial economies) | Medium-term (2025-2030) |

| Concerns over Cybersecurity Vulnerabilities | -0.6% | Global | Long-term (2025-2033) |

| Lack of Skilled Workforce for Implementation and Maintenance | -0.4% | Global (Especially in developing regions) | Short to Medium-term (2025-2028) |

OPC Server Software Market Opportunities Analysis

The OPC Server Software market is ripe with opportunities, particularly driven by the growing trend towards cloud-based industrial applications and edge computing. As industries increasingly seek to leverage the scalability and flexibility of cloud platforms for data storage, analytics, and remote monitoring, OPC Servers are emerging as crucial gateways for securely transferring operational technology (OT) data to the cloud. This trend creates new avenues for OPC software providers to offer integrated cloud-ready solutions, enabling businesses to unlock deeper insights from their vast industrial datasets without significant on-premise infrastructure investments. The convergence of OT and IT in the cloud presents a substantial opportunity for innovative OPC deployments.

Another significant opportunity lies in the expansion of OPC Server Software into new and emerging industrial verticals and applications. While traditionally strong in discrete and process manufacturing, OPC is finding new relevance in smart cities, renewable energy management, smart agriculture, and healthcare automation. These sectors increasingly require robust, standardized, and secure data exchange capabilities to manage complex interconnected systems. Furthermore, the burgeoning demand for highly granular data for Artificial Intelligence and Machine Learning applications, predictive analytics, and digital twin initiatives provides a fertile ground for OPC Server solutions that can reliably deliver high-fidelity data streams. As industries continue to innovate and adopt advanced digital technologies, the scope for OPC Server Software broadens significantly, promising sustained market expansion.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into Cloud-based and Edge Computing Solutions | +1.3% | Global | Long-term (2025-2033) |

| Integration with AI and Advanced Analytics Platforms | +1.1% | Global (Strong in developed economies) | Medium-term (2025-2030) |

| Untapped Markets in Smart Cities and New Industrial Verticals | +0.9% | Emerging Economies (APAC, Latin America, MEA) | Long-term (2025-2033) |

OPC Server Software Market Challenges Impact Analysis

The OPC Server Software market encounters several challenges that necessitate strategic responses from industry players. One key challenge is ensuring seamless interoperability across the vast and continuously expanding ecosystem of industrial devices, systems, and software from different vendors. While OPC UA aims to standardize communication, the practical implementation often involves navigating proprietary interfaces, varying data models, and legacy equipment. This complexity can lead to integration hurdles, extended deployment times, and increased costs, particularly for enterprises with highly heterogeneous operational environments. Addressing these interoperability complexities effectively is crucial for broader market acceptance and streamlining adoption.

Another significant challenge revolves around the rapidly evolving cybersecurity threat landscape. As industrial control systems become more connected via OPC, they become more vulnerable to sophisticated cyber-attacks. Protecting sensitive operational data and ensuring the integrity and availability of industrial processes is paramount. This requires continuous investment in advanced security features, regular updates, and robust incident response planning for OPC Server solutions. Additionally, the talent gap in industrial IT and cybersecurity further exacerbates this challenge, as organizations struggle to find skilled professionals capable of implementing, managing, and securing complex OPC infrastructures. Overcoming these challenges will be vital for sustained market growth and building trust in interconnected industrial systems.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Maintaining Interoperability Across Diverse Vendor Ecosystems | -0.8% | Global | Long-term (2025-2033) |

| Addressing Evolving Cybersecurity Threats and Regulations | -0.7% | Global (More stringent in regulated industries) | Long-term (2025-2033) |

| Managing Data Volume and Complexity in Large-Scale Deployments | -0.5% | Global (Especially in large enterprises) | Medium-term (2025-2030) |

OPC Server Software Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the OPC Server Software market, encompassing historical data, current market dynamics, and future projections. The report offers a detailed segmentation analysis, regional insights, competitive landscape, and the impact of emerging technologies like AI and cloud computing. It aims to equip stakeholders with actionable intelligence to make informed strategic decisions regarding market entry, product development, and geographic expansion.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 520.4 Million |

| Market Forecast in 2033 | USD 1,036.7 Million |

| Growth Rate | 8.9% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | ABB, Siemens, Rockwell Automation, Honeywell, Schneider Electric, Yokogawa, GE Digital, Emerson Electric, Advantech, Softing AG, Matrikon International (now part of Honeywell), KEPWARE (now part of PTC), Iconics, InduSoft, National Instruments, COPA-DATA, Prosys OPC Ltd., Unified Automation GmbH, OSIsoft (now Aveva) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The OPC Server Software market is meticulously segmented to provide a granular view of its various facets, enabling stakeholders to identify specific growth opportunities and market dynamics. The segmentation is primarily driven by the evolving technical landscape of OPC protocols, diverse deployment preferences, the wide array of industrial applications, and the types of components and services offered. Analyzing these segments helps understand the varying demand across industries and technological preferences, from traditional on-premise solutions to modern cloud-native architectures.

The segmentation by type, particularly highlighting the transition from classic OPC (DA, HDA, A&E) to OPC UA, reflects the industry's shift towards a more robust, secure, and interoperable standard. Deployment models, encompassing on-premise, cloud-based, and hybrid solutions, signify the increasing flexibility and scalability sought by modern enterprises. Furthermore, the application-based segmentation showcases the widespread adoption of OPC Server Software across a multitude of industrial sectors, underscoring its foundational role in disparate operational environments and its adaptability to specific industry requirements and complexities.

- By Type: OPC DA, OPC HDA, OPC A&E, OPC UA

- By Deployment: On-Premise, Cloud-based, Hybrid

- By Application/Industry: Manufacturing (Discrete, Process), Energy & Utilities, Oil & Gas, Chemicals, Pharmaceuticals & Life Sciences, Automotive, Food & Beverage, Mining & Metals, Building Automation, SCADA Systems, DCS Systems, MES Systems, Other Industrial Applications

- By Component: Software/Platform, Services (Integration, Consulting, Support, Training)

- By Operating System: Windows, Linux, Other OS

Regional Highlights

Geographically, the OPC Server Software market exhibits distinct growth patterns and maturity levels across different regions. North America and Europe are traditionally dominant markets, characterized by advanced industrial infrastructure, early adoption of automation technologies, and significant investments in Industry 4.0 initiatives. These regions lead in the adoption of cutting-edge OPC UA solutions, particularly in discrete manufacturing, automotive, and energy sectors, driven by the need for efficiency, regulatory compliance, and cybersecurity. The presence of key market players and a robust R&D ecosystem further bolsters market growth in these areas.

Asia Pacific (APAC) is projected to be the fastest-growing region, fueled by rapid industrialization, burgeoning manufacturing sectors, and increasing government initiatives supporting smart factory development in countries like China, India, Japan, and South Korea. The region's expanding industrial base and growing appetite for digital transformation solutions provide fertile ground for OPC Server Software adoption. Latin America, the Middle East, and Africa (MEA) are emerging markets, showing gradual but consistent growth, primarily driven by investments in infrastructure, oil and gas, and mining sectors, alongside a rising awareness of the benefits of industrial connectivity and automation. Each region's unique industrial landscape and technological priorities shape its specific demand for OPC Server Software solutions.

- North America: Leading market due to high adoption of automation, robust industrial infrastructure, and focus on Industry 4.0 across manufacturing and energy sectors.

- Europe: Strong market driven by mature industrial base, stringent regulatory standards, and continuous innovation in smart manufacturing and process optimization.

- Asia Pacific (APAC): Fastest-growing region, propelled by rapid industrialization, digital transformation initiatives, and increasing investments in smart factories, particularly in China, India, and Southeast Asian countries.

- Latin America: Emerging market with growth driven by infrastructure development, natural resource industries, and increasing awareness of industrial IoT benefits.

- Middle East and Africa (MEA): Growing market due to investments in oil & gas, utilities, and infrastructure projects, coupled with a focus on diversifying industrial capabilities.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the OPC Server Software Market.- ABB

- Siemens

- Rockwell Automation

- Honeywell

- Schneider Electric

- Yokogawa

- GE Digital

- Emerson Electric

- Advantech

- Softing AG

- Matrikon International

- KEPWARE

- Iconics

- InduSoft

- National Instruments

- COPA-DATA

- Prosys OPC Ltd.

- Unified Automation GmbH

- OSIsoft

Frequently Asked Questions

What is OPC Server Software?

OPC Server Software facilitates standardized communication between industrial hardware devices (like PLCs, sensors, and RTUs) and software applications (such as HMIs, SCADA systems, and MES). It acts as a universal translator, enabling seamless and interoperable data exchange across diverse industrial automation components from different manufacturers, thus unifying operational data for analysis and control.

What are the primary benefits of using OPC Server Software?

The main benefits of OPC Server Software include enhanced interoperability across disparate systems, improved data accessibility for real-time monitoring and analytics, reduced integration complexity and costs, increased operational efficiency through better data flow, and improved decision-making capabilities due to a unified view of industrial processes.

How does OPC UA differ from classic OPC specifications?

OPC UA (Unified Architecture) is a platform-independent, service-oriented, and secure evolution of classic OPC (DA, HDA, A&E). Unlike classic OPC which relies on Microsoft's COM/DCOM, OPC UA uses modern internet technologies, offers built-in security (encryption, authentication), complex data modeling capabilities, and is scalable from embedded devices to the cloud, making it suitable for Industry 4.0 and IIoT environments.

Which industries extensively utilize OPC Server Software?

OPC Server Software is extensively utilized across a wide range of industries including discrete manufacturing (e.g., automotive, electronics), process manufacturing (e.g., chemicals, pharmaceuticals, food & beverage), energy & utilities, oil & gas, mining & metals, building automation, and critical infrastructure sectors for data acquisition and control.

What are the future trends impacting the OPC Server Software market?

Future trends impacting the OPC Server Software market include the accelerating adoption of OPC UA as the universal standard, increased integration with cloud computing and edge analytics for remote operations and scalability, the growing influence of Artificial Intelligence (AI) and Machine Learning (ML) for predictive insights, and a stronger emphasis on cybersecurity and data integrity within industrial networks.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted