Biopharmaceutical Buffer Market

Biopharmaceutical Buffer Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705254 | Last Updated : August 11, 2025 |

Format : ![]()

![]()

![]()

![]()

Biopharmaceutical Buffer Market Size

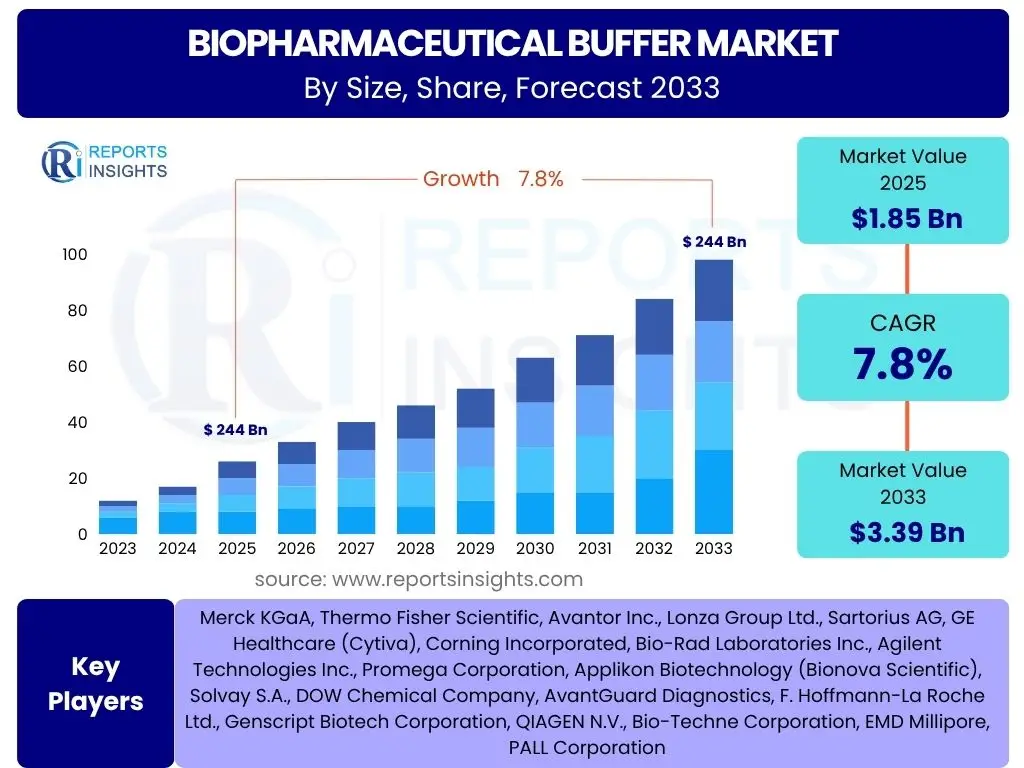

According to Reports Insights Consulting Pvt Ltd, The Biopharmaceutical Buffer Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2033. The market is estimated at USD 1.85 Billion in 2025 and is projected to reach USD 3.39 Billion by the end of the forecast period in 2033.

Key Biopharmaceutical Buffer Market Trends & Insights

The biopharmaceutical buffer market is experiencing dynamic shifts driven by advancements in bioprocessing and a burgeoning pipeline of biologic drugs. A prominent trend involves the increasing adoption of pre-made and customized buffer solutions, which streamline manufacturing processes, reduce preparation errors, and enhance reproducibility. This move away from in-house buffer preparation aligns with the industry's push for greater efficiency and compliance. Furthermore, the growing emphasis on single-use technologies within biomanufacturing facilities is directly influencing buffer market trends, as single-use bags and systems require specific, ready-to-use buffer formulations.

Another significant insight revolves around the rising demand for high-concentration buffer formulations, particularly for downstream processing and formulation of highly concentrated biologics. This trend is driven by the need to reduce manufacturing footprints, improve patient compliance through smaller injection volumes, and optimize storage and transportation. Additionally, sustainability considerations are gaining traction, prompting manufacturers to explore greener buffer chemistries and more efficient production methods, including those that reduce water consumption and waste generation. The ongoing innovation in cell and gene therapies also creates a distinct demand for specialized buffer systems that can maintain the stability and viability of delicate biological materials throughout the manufacturing process.

- Increasing adoption of pre-made and customized buffer solutions.

- Rising integration of single-use bioprocessing technologies.

- Growing demand for high-concentration buffer formulations.

- Emergence of sustainable buffer chemistries and production methods.

- Development of specialized buffers for cell and gene therapies.

- Focus on buffer standardization for global regulatory compliance.

- Expansion of biomanufacturing capacity globally.

AI Impact Analysis on Biopharmaceutical Buffer

The integration of Artificial intelligence (AI) is set to revolutionize various aspects of the biopharmaceutical buffer market, addressing common user inquiries about efficiency, precision, and quality control. Users often question how AI can optimize buffer preparation and formulation. AI-driven algorithms can analyze vast datasets from past experiments, predicting optimal buffer compositions for specific bioprocessing steps, thereby reducing trial-and-error, saving time, and minimizing material waste. This predictive capability enhances the consistency and reproducibility of buffer solutions, critical for maintaining product quality in sensitive biologic manufacturing.

Furthermore, AI and machine learning are poised to improve quality assurance and regulatory compliance within buffer manufacturing. By employing real-time monitoring and predictive analytics, AI systems can detect deviations in buffer parameters, anticipate potential stability issues, and ensure adherence to stringent regulatory guidelines. This proactive approach minimizes batch failures and accelerates validation processes. Users are also keen to understand AI's role in supply chain management for buffer components. AI can optimize inventory levels, forecast demand fluctuations, and identify potential supply chain disruptions, ensuring a steady and reliable supply of critical raw materials for buffer production, thereby mitigating risks and improving operational resilience.

- AI-driven optimization of buffer formulation and preparation.

- Enhanced predictive analytics for buffer stability and shelf-life.

- Automation and robotic integration in buffer manufacturing processes.

- Improved quality control and real-time monitoring of buffer parameters.

- Streamlined supply chain management for buffer raw materials.

- Accelerated R&D for novel buffer systems and applications.

Key Takeaways Biopharmaceutical Buffer Market Size & Forecast

The biopharmaceutical buffer market is poised for robust expansion, driven primarily by the escalating demand for advanced biologic drugs, including monoclonal antibodies, vaccines, and cell and gene therapies. A key takeaway is the market's trajectory towards increased complexity and specialization, necessitating a shift from generic buffer salts to tailored, high-performance buffer systems. The forecast indicates significant growth, underscoring the indispensable role of buffers in maintaining the stability, purity, and efficacy of biopharmaceutical products throughout their lifecycle, from upstream processing to final formulation and storage.

Another crucial insight is the accelerating adoption of pre-mixed and custom-blend buffer solutions, reflecting a strategic move by biomanufacturers to enhance operational efficiency, reduce labor costs, and mitigate risks associated with in-house preparation. This trend is particularly evident as companies scale up production and seek to standardize processes globally. Furthermore, the regional dynamics highlight Asia Pacific as a rapidly expanding market, fueled by growing biomanufacturing capacities and increasing investments in pharmaceutical R&D, positioning it as a pivotal growth engine alongside established markets in North America and Europe.

- Significant market growth driven by the rising demand for biologics and biosimilars.

- Increasing preference for pre-mixed and custom-formulated buffer solutions.

- Crucial role of buffers in ensuring stability and efficacy of biopharmaceutical products.

- Asia Pacific emerging as a high-growth region for market expansion.

- Technological advancements in bioprocessing influencing buffer product development.

- Focus on quality, consistency, and regulatory compliance as key competitive factors.

Biopharmaceutical Buffer Market Drivers Analysis

The biopharmaceutical buffer market is significantly propelled by the burgeoning global biopharmaceutical industry, particularly the accelerating research and development activities in biologics and biosimilars. As more complex and sensitive molecules enter the drug pipeline, the critical role of buffers in maintaining their stability and integrity throughout the manufacturing process becomes paramount. The increasing prevalence of chronic and infectious diseases globally drives the demand for innovative therapeutic solutions, directly translating into a higher demand for high-quality biopharmaceutical buffers essential for drug discovery, development, and production.

Furthermore, the expansion of biomanufacturing capabilities and the adoption of advanced bioprocessing technologies worldwide contribute substantially to market growth. Facilities are increasingly opting for pre-made, ready-to-use buffer solutions to enhance efficiency, reduce contamination risks, and streamline production cycles. This shift, coupled with the rising investments in contract research and manufacturing organizations (CROs and CMOs) that require standardized and reliable buffer supplies, reinforces the market's positive trajectory. The continuous innovation in areas like cell and gene therapy, which demand extremely precise and specialized buffer environments, also acts as a powerful driver, pushing the boundaries of buffer technology and expanding its application scope.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Biologics & Biosimilars Market | +1.2% | Global, particularly North America, Europe, APAC | Short to Mid-term (2025-2029) |

| Increasing R&D in Biopharmaceuticals | +1.0% | Global, especially US, Germany, China, Japan | Short to Mid-term (2025-2029) |

| Expansion of Biomanufacturing Facilities | +0.8% | APAC, North America | Mid to Long-term (2027-2033) |

| Adoption of Single-Use Technologies | +0.7% | North America, Europe | Mid-term (2026-2030) |

| Rising Demand for Pre-made Buffers | +0.9% | Global | Short-term (2025-2027) |

Biopharmaceutical Buffer Market Restraints Analysis

Despite the robust growth, the biopharmaceutical buffer market faces several restraints that could impede its full potential. One significant challenge is the high cost associated with high-purity raw materials required for buffer manufacturing. These specialized reagents often have stringent quality requirements and are sourced from a limited number of suppliers, leading to higher production costs which can be passed on to end-users. This cost sensitivity can become a deterrent, especially for smaller biopharmaceutical companies or those operating in cost-constrained markets, potentially encouraging them to seek more economical, albeit less optimized, in-house solutions or alternative suppliers.

Another major restraint involves stringent regulatory hurdles and quality control requirements. Biopharmaceutical buffers must adhere to strict pharmacopoeial standards and Good Manufacturing Practices (GMP), necessitating extensive testing, documentation, and validation. This adds complexity and cost to the manufacturing process, requiring significant investments in quality assurance systems and trained personnel. Furthermore, the inherent variability in raw material quality and supply chain complexities can lead to inconsistencies in buffer performance, posing risks to bioprocess integrity and product stability, thereby creating a significant constraint on market expansion and widespread adoption of outsourced buffer solutions.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Cost of Raw Materials | -0.8% | Global | Short to Mid-term (2025-2029) |

| Stringent Regulatory Requirements | -0.7% | Global, particularly highly regulated markets (US, EU) | Ongoing |

| Supply Chain Vulnerabilities | -0.6% | Global, particularly during geopolitical instability | Short-term (2025-2027) |

| Availability of In-house Preparation | -0.5% | Global | Mid-term (2026-2030) |

Biopharmaceutical Buffer Market Opportunities Analysis

Significant opportunities are emerging within the biopharmaceutical buffer market, driven by the rapid growth of advanced therapies and expanding global healthcare access. The burgeoning field of cell and gene therapies, for instance, requires highly specialized and ultrapure buffer systems to ensure the viability and efficacy of sensitive cellular materials and viral vectors. This niche, yet high-value segment, presents a lucrative avenue for buffer manufacturers to innovate and develop tailored solutions that meet the unique demands of these groundbreaking therapeutic modalities, moving beyond conventional protein-based biopharmaceuticals.

Furthermore, the increasing focus on bioprocess intensification and continuous manufacturing paradigms offers substantial market opportunities. These modern manufacturing approaches demand highly stable, consistent, and concentrated buffer solutions that can withstand extended processing times and higher throughputs. Manufacturers that can develop and supply such advanced buffer formulations will gain a competitive edge. Additionally, the expansion of biopharmaceutical manufacturing into emerging economies, particularly in Asia Pacific and Latin America, represents a significant growth opportunity. These regions are investing heavily in new facilities and seeking reliable, high-quality buffer supplies to support their growing domestic and export-oriented bioproduction, creating new customer bases and market penetration possibilities.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth of Cell & Gene Therapies | +1.1% | North America, Europe, China | Mid to Long-term (2027-2033) |

| Emerging Markets Expansion | +0.9% | APAC (China, India), Latin America | Mid-term (2026-2030) |

| Demand for Customized & High-Concentration Buffers | +0.8% | Global | Short to Mid-term (2025-2029) |

| Focus on Sustainable Bioprocessing | +0.7% | Europe, North America | Long-term (2028-2033) |

Biopharmaceutical Buffer Market Challenges Impact Analysis

The biopharmaceutical buffer market faces significant challenges, particularly concerning maintaining consistent quality and purity across varied production scales and global supply chains. One major hurdle is the variability in raw material sourcing, which can directly impact the final buffer's performance and lead to batch-to-batch inconsistencies. Ensuring the absence of contaminants, endotoxins, and nucleases in bulk buffer ingredients is critical but complex, requiring rigorous analytical testing and quality control measures at every stage. This challenge is amplified by the sheer volume of buffers used in large-scale biomanufacturing, where even minor variations can compromise entire drug batches, leading to substantial financial losses and delays.

Another prominent challenge relates to the complex regulatory landscape and the need for continuous adaptation to evolving guidelines. As biopharmaceutical regulations become more stringent, particularly regarding extractables and leachables from single-use components, buffer manufacturers must continually invest in R&D to ensure their products comply with the latest global standards. Furthermore, managing the logistics and storage of large volumes of buffer solutions, especially liquid forms, presents a significant operational challenge. Issues such as stability over long shipping distances, potential for leakage, and maintaining appropriate temperature ranges contribute to the overall cost and complexity of the supply chain, pushing companies to consider more compact powder forms or concentrated solutions.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Maintaining Quality & Consistency | -0.9% | Global | Ongoing |

| Supply Chain & Logistics Complexities | -0.8% | Global, especially cross-border | Short to Mid-term (2025-2029) |

| Waste Management & Environmental Concerns | -0.6% | Europe, North America | Mid to Long-term (2027-2033) |

| Competition from In-house Production | -0.5% | Global | Short-term (2025-2027) |

Biopharmaceutical Buffer Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the Biopharmaceutical Buffer Market, offering detailed insights into market dynamics, segmentation, regional trends, and competitive landscape. The scope encompasses a thorough examination of market size and growth projections from 2025 to 2033, alongside an assessment of key drivers, restraints, opportunities, and challenges influencing market trajectory. It highlights emerging trends, including the impact of AI and the shift towards advanced buffer solutions, providing stakeholders with critical intelligence for strategic decision-making.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.85 Billion |

| Market Forecast in 2033 | USD 3.39 Billion |

| Growth Rate | 7.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Merck KGaA, Thermo Fisher Scientific, Avantor Inc., Lonza Group Ltd., Sartorius AG, GE Healthcare (Cytiva), Corning Incorporated, Bio-Rad Laboratories Inc., Agilent Technologies Inc., Promega Corporation, Applikon Biotechnology (Bionova Scientific), Solvay S.A., DOW Chemical Company, AvantGuard Diagnostics, F. Hoffmann-La Roche Ltd., Genscript Biotech Corporation, QIAGEN N.V., Bio-Techne Corporation, EMD Millipore, PALL Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The biopharmaceutical buffer market is comprehensively segmented to provide a granular understanding of its diverse components and their respective contributions to the overall market landscape. This segmentation allows for targeted analysis of different product types, forms, applications, and end-users, highlighting specific growth areas and market dynamics within each category. Understanding these segments is crucial for stakeholders to identify niche opportunities, develop tailored products, and formulate effective market entry and expansion strategies in the highly specialized biopharmaceutical sector.

The segmentation by type elucidates the dominance and growth trajectories of various chemical compositions like Phosphate Buffer Saline (PBS) and Tris Buffer, which are fundamental in numerous bioprocessing steps, alongside emerging specialized buffers. Segmentation by form differentiates between liquid and powder buffers, reflecting industry preferences for convenience, stability, and transportation efficiency. Application-based segmentation reveals critical demand drivers across upstream and downstream processing, drug discovery, and diagnostics, illustrating where buffer consumption is most intensive. Finally, end-use segmentation provides insights into purchasing patterns and specific requirements of key industry players, including biopharmaceutical companies, CROs, and academic institutions, allowing for a comprehensive market perspective.

- By Type:

- Phosphate Buffer Saline (PBS)

- Tris Buffer

- Acetate Buffer

- Citrate Buffer

- HEPES Buffer

- Others (e.g., Glycine, MOPS, Bicarbonate)

- By Form:

- Liquid Buffers

- Powder Buffers

- By Application:

- Upstream Processing (Cell Culture, Fermentation)

- Downstream Processing (Purification, Filtration, Chromatography)

- Drug Discovery (Screening, Assays)

- Diagnostics (Reagent Preparation, Assay Buffers)

- Research & Development

- Others (e.g., Formulation, Storage)

- By End-use:

- Biopharmaceutical Companies

- Contract Research Organizations (CROs)

- Academic & Research Institutes

- Diagnostic Laboratories

Regional Highlights

Geographically, the biopharmaceutical buffer market exhibits significant regional disparities influenced by varying levels of biopharmaceutical R&D, manufacturing capabilities, and regulatory frameworks. North America, particularly the United States, holds a dominant position due to its robust biopharmaceutical industry, extensive research infrastructure, high investments in drug discovery, and a large number of established biopharmaceutical companies. The early adoption of advanced bioprocessing technologies and the strong presence of key market players further solidify its leading market share. The continuous demand for novel biologics and the rapid expansion of cell and gene therapy research contribute substantially to market growth in this region.

Europe also represents a substantial market share, driven by strong government support for biotechnology research, a well-established pharmaceutical industry, and increasing R&D activities in countries like Germany, the UK, and Switzerland. The region's stringent regulatory environment ensures a high demand for quality-compliant buffer solutions. Meanwhile, the Asia Pacific region is projected to be the fastest-growing market, propelled by escalating investments in biomanufacturing facilities, a burgeoning biosimilars market, and improving healthcare infrastructure in countries such as China, India, and South Korea. The cost-effectiveness of manufacturing in these regions, coupled with increasing outsourcing activities, is attracting significant foreign investments and fueling rapid market expansion. Latin America, the Middle East, and Africa are also showing nascent growth, driven by increasing healthcare expenditure and developing biopharmaceutical capabilities, albeit at a slower pace compared to the established and rapidly emerging markets.

- North America: Dominant market share due to strong R&D, advanced biomanufacturing infrastructure, and high adoption of innovative biopharmaceuticals.

- Europe: Significant market presence, supported by robust pharmaceutical industries, government funding for biotech research, and stringent quality standards.

- Asia Pacific (APAC): Fastest-growing region, driven by increasing biomanufacturing capacities, rising R&D investments, and expansion of the biosimilars market in countries like China, India, and South Korea.

- Latin America: Emerging market with growing investments in healthcare and biopharma, though market penetration for advanced buffers is still developing.

- Middle East & Africa (MEA): Nascent market, with increasing focus on healthcare infrastructure development and gradual adoption of modern bioprocessing techniques.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Biopharmaceutical Buffer Market.- Merck KGaA

- Thermo Fisher Scientific

- Avantor Inc.

- Lonza Group Ltd.

- Sartorius AG

- Cytiva (formerly GE Healthcare Life Sciences)

- Corning Incorporated

- Bio-Rad Laboratories Inc.

- Agilent Technologies Inc.

- Promega Corporation

- Bionova Scientific (Applikon Biotechnology)

- Solvay S.A.

- DOW Chemical Company

- AvantGuard Diagnostics

- F. Hoffmann-La Roche Ltd.

- Genscript Biotech Corporation

- QIAGEN N.V.

- Bio-Techne Corporation

- EMD Millipore

- PALL Corporation

Frequently Asked Questions

Analyze common user questions about the Biopharmaceutical Buffer market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is a biopharmaceutical buffer and why is it important?

A biopharmaceutical buffer is a solution that resists changes in pH when small amounts of acid or base are added, maintaining a stable environment for sensitive biological molecules. It is crucial in biopharmaceutical manufacturing to ensure the stability, purity, and activity of proteins, enzymes, and other biomolecules throughout various processing steps, from cell culture to final drug formulation.

What are the primary types of buffers used in biopharmaceutical applications?

The primary types of buffers include Phosphate Buffer Saline (PBS), Tris (Tris-hydroxymethyl aminomethane) Buffer, Acetate Buffer, Citrate Buffer, and HEPES (4-(2-hydroxyethyl)-1-piperazineethanesulfonic acid) Buffer. Each type is selected based on its specific pH range, ionic strength, compatibility with target molecules, and suitability for particular upstream or downstream processes.

How do single-use technologies impact the biopharmaceutical buffer market?

Single-use technologies significantly impact the buffer market by increasing the demand for pre-mixed, ready-to-use liquid buffers supplied in sterile, disposable bags. This shift reduces the need for in-house buffer preparation, minimizes cleaning validation requirements, lowers contamination risks, and enhances operational flexibility, driving the market towards pre-formulated and customized buffer solutions.

What role does AI play in biopharmaceutical buffer development and manufacturing?

AI is increasingly being utilized to optimize buffer formulation, predict stability, and enhance quality control. AI algorithms can analyze complex experimental data to identify ideal buffer compositions, streamline R&D, improve consistency, and enable real-time monitoring of buffer parameters, leading to more efficient and reliable bioprocessing.

What are the key drivers for growth in the biopharmaceutical buffer market?

Key drivers include the burgeoning global demand for biologics and biosimilars, increasing investments in biopharmaceutical R&D, the expansion of biomanufacturing facilities, and the growing adoption of single-use and pre-mixed buffer solutions. The emergence of advanced therapies like cell and gene therapy also contributes significantly to market growth.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted