Bio based Polyethylene Market

Bio based Polyethylene Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703064 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

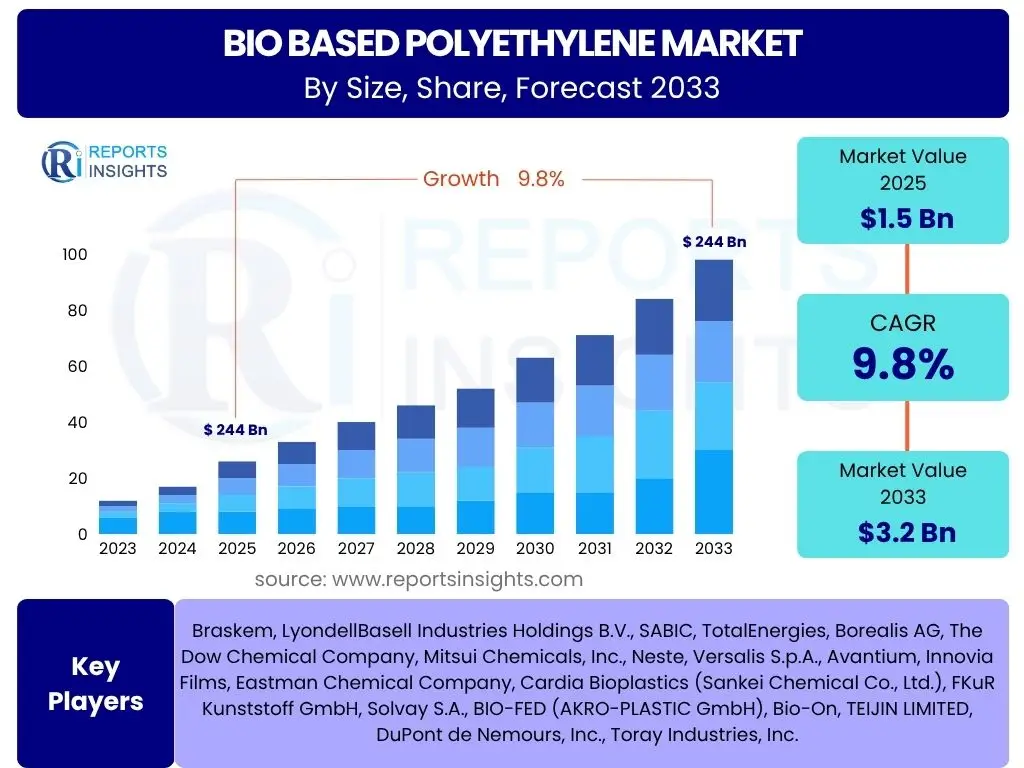

Bio based Polyethylene Market Size

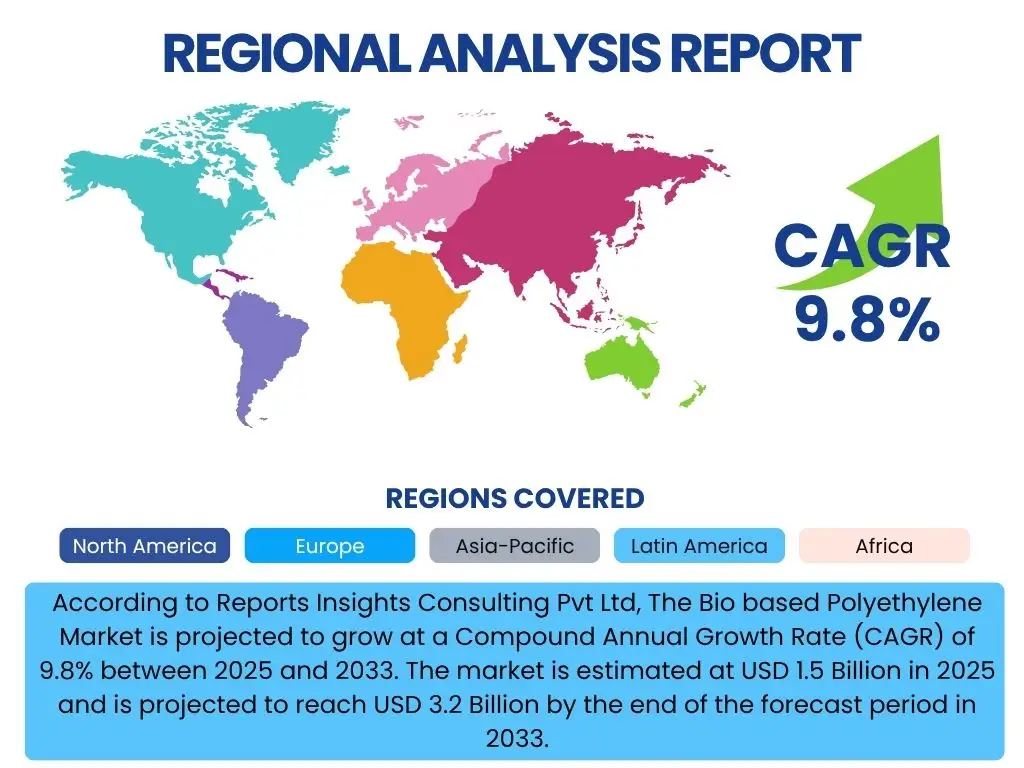

According to Reports Insights Consulting Pvt Ltd, The Bio based Polyethylene Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.8% between 2025 and 2033. The market is estimated at USD 1.5 Billion in 2025 and is projected to reach USD 3.2 Billion by the end of the forecast period in 2033.

Key Bio based Polyethylene Market Trends & Insights

The Bio based Polyethylene market is undergoing significant transformation driven by a global shift towards sustainable practices and increasing environmental consciousness. Key trends indicate a strong push for enhanced circularity, diverse feedstock sourcing beyond traditional sugarcane, and the integration of advanced processing technologies. Consumers and industries alike are prioritizing materials that reduce carbon footprint and support a greener economy, propelling innovation and adoption within this sector.

Furthermore, regulatory frameworks worldwide are increasingly incentivizing the production and use of bio-based plastics, creating a favorable market environment. This includes policies promoting biodegradable or compostable alternatives and those taxing virgin fossil-based plastics. The market also observes a growing trend in strategic collaborations and partnerships across the value chain, aiming to scale production, improve material properties, and reduce costs, thereby enhancing market accessibility and competitiveness.

- Increasing demand for sustainable packaging solutions across various industries.

- Diversification of feedstock sources to include agricultural waste, algae, and non-food crops.

- Technological advancements leading to improved material properties and cost-effectiveness.

- Growing regulatory support and government initiatives promoting bio-plastic adoption.

- Expansion of application areas beyond traditional packaging into automotive, consumer goods, and construction.

AI Impact Analysis on Bio based Polyethylene

Artificial intelligence is poised to significantly optimize various stages of the Bio based Polyethylene value chain, from feedstock cultivation and processing to material design and end-of-life management. Users are particularly interested in how AI can enhance efficiency in biorefinery operations, predict optimal yields from biomass, and reduce energy consumption in production processes. The application of AI algorithms can lead to more precise control over reaction conditions, minimizing waste and improving the purity of the final bio-polyethylene product.

Furthermore, AI offers substantial potential in accelerating the research and development of novel bio-based materials with enhanced performance characteristics. Machine learning models can analyze vast datasets of material properties and molecular structures, identifying promising new compositions or process parameters. This predictive capability can shorten development cycles and bring innovative bio-polyethylene grades to market more quickly, addressing specific industry needs and expanding market opportunities. AI also plays a crucial role in supply chain optimization, improving traceability, and ensuring the sustainable sourcing of bio-feedstock, thereby strengthening the overall market integrity and efficiency.

- AI-driven optimization of feedstock cultivation and biomass conversion processes.

- Enhanced predictive analytics for material property design and performance improvement.

- Automated quality control and process monitoring in bio-polyethylene manufacturing.

- Optimization of supply chain logistics for bio-feedstock and final products.

- Development of smart recycling and composting solutions for end-of-life management.

Key Takeaways Bio based Polyethylene Market Size & Forecast

The Bio based Polyethylene market is poised for robust growth, driven by an accelerating global shift towards sustainable materials and a heightened focus on environmental responsibility. Key takeaways highlight that the market's expansion is not merely incremental but represents a fundamental transformation in material science and industrial practices. The projected significant increase in market value reflects strong confidence in bio-polyethylene's role in future sustainable economies, positioning it as a critical component in meeting global climate goals and circular economy objectives.

This growth is underpinned by continuous innovation in production technologies, diversification of feedstock, and expanding application versatility across multiple industries. Moreover, the increasing integration of bio-based plastics into corporate sustainability strategies and the rising consumer preference for eco-friendly products are providing substantial momentum. These factors collectively indicate a promising outlook for the Bio based Polyethylene sector, emphasizing its potential for significant investment returns and widespread environmental benefits.

- Substantial market growth forecasted, indicating strong industry confidence and adoption.

- Driven by environmental regulations, corporate sustainability goals, and consumer demand.

- Technological advancements are crucial for cost reduction and performance enhancement.

- Packaging and consumer goods sectors are key early adopters, with expanding applications.

- The market represents a significant opportunity for sustainable innovation and investment.

Bio based Polyethylene Market Drivers Analysis

The increasing global emphasis on sustainability and circular economy principles is a primary driver for the Bio based Polyethylene market. Industries are under growing pressure from regulatory bodies, consumers, and investors to reduce their carbon footprint and minimize reliance on fossil resources. Bio based Polyethylene offers a compelling solution by utilizing renewable raw materials, leading to lower greenhouse gas emissions over its lifecycle compared to conventional polyethylene, thus aligning with global environmental objectives and corporate sustainability targets.

Additionally, the rising consumer awareness regarding environmental issues, coupled with a preference for eco-friendly products, is significantly influencing brand strategies. Companies are actively seeking ways to differentiate their products through sustainable packaging and materials, leading to increased adoption of bio-based polymers like polyethylene. Government incentives, subsidies, and favorable policies for bio-based products in various regions also provide crucial support, encouraging research, development, and commercialization efforts within the market.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Environmental Concerns & Sustainability Goals | +2.5% | Global, particularly Europe & North America | 2025-2033 |

| Favorable Government Regulations & Policies | +1.8% | Europe, Asia Pacific (e.g., China, Japan), Brazil | 2025-2033 |

| Increasing Consumer Demand for Eco-friendly Products | +2.0% | North America, Europe, Developed Asia Pacific | 2025-2033 |

| Brand Commitments to Reduce Carbon Footprint | +1.5% | Global, particularly major corporations | 2025-2033 |

Bio based Polyethylene Market Restraints Analysis

Despite its promising growth, the Bio based Polyethylene market faces significant restraints, primarily stemming from its higher production costs compared to conventional fossil-based polyethylene. The complex processes involved in converting biomass into bio-polyethylene, coupled with the capital intensity of setting up bio-refineries, often result in a price premium that can deter widespread adoption, especially in price-sensitive applications. This cost disparity makes it challenging for bio-PE to compete directly with its petroleum-derived counterparts, which benefit from established infrastructure and economies of scale.

Another key restraint is the limited availability and fluctuating prices of sustainable feedstock materials. While sugarcane and corn are common sources, concerns about competition with food crops and land use exist. Diversifying feedstock sources to non-food biomass or waste streams presents technical challenges and scalability issues. Additionally, some bio-based polyethylene grades may not yet fully match the performance characteristics or processability of traditional PE in all specialized applications, leading to slower adoption in demanding sectors requiring specific material properties and high durability.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Higher Production Costs than Conventional PE | -1.2% | Global | 2025-2029 |

| Limited Availability & Price Volatility of Feedstock | -0.8% | Global, particularly regions dependent on specific crops | 2025-2033 |

| Performance Limitations vs. Conventional PE in Niche Applications | -0.5% | Global, specific industrial sectors | 2025-2033 |

| Infrastructural Challenges for Collection & Processing | -0.4% | Developing Regions | 2025-2030 |

Bio based Polyethylene Market Opportunities Analysis

The Bio based Polyethylene market is rich with opportunities, particularly through the expansion into novel application areas previously dominated by conventional plastics. Emerging sectors like automotive interior components, durable consumer goods, and specialized construction materials are increasingly seeking sustainable alternatives, opening new avenues for bio-PE. The development of high-performance bio-polyethylene grades that closely match or even surpass the properties of fossil-based polymers will be crucial in unlocking these new market segments, providing solutions that meet stringent technical requirements while fulfilling sustainability mandates.

Furthermore, significant opportunities lie in diversifying feedstock sources beyond traditional sugarcane to include agricultural waste, forestry residues, and algae. This diversification not only addresses concerns about food vs. fuel but also enhances the resilience of the supply chain and reduces raw material costs in the long term. Strategic collaborations between bio-plastic manufacturers, technology providers, and end-use industries are also creating synergistic opportunities. These partnerships facilitate shared R&D, accelerate commercialization, and help in establishing robust supply chains and recycling infrastructures, paving the way for broader market acceptance and scalability.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into New Application Areas (e.g., Automotive, Construction) | +1.5% | Global | 2027-2033 |

| Development of Diverse & Sustainable Feedstock Sources | +1.0% | Global, particularly Asia Pacific & Latin America | 2025-2033 |

| Strategic Partnerships & Collaborations Across Value Chain | +0.8% | Global | 2025-2033 |

| Growing Focus on Circular Economy & Recycling Infrastructure | +0.7% | Europe, North America | 2026-2033 |

Bio based Polyethylene Market Challenges Impact Analysis

The Bio based Polyethylene market faces several critical challenges that could impede its growth trajectory. One significant hurdle is the volatility of bio-feedstock prices, which can be influenced by agricultural yields, climate conditions, and competition from other industries like biofuels. This price instability makes long-term planning and cost competitiveness difficult for manufacturers. Furthermore, ensuring the consistent quality and availability of sustainable feedstock at scale remains a logistical and technological challenge, especially as demand for bio-PE increases globally.

Another major challenge is the perception and education surrounding bio-based plastics. There is often confusion among consumers and even some industries regarding the differences between "bio-based," "biodegradable," and "compostable" materials. This lack of clarity can lead to skepticism, concerns about "greenwashing," and improper disposal, hindering the full environmental benefits of bio-PE. Lastly, the established infrastructure for fossil-based plastics, including mature supply chains and recycling systems, presents a formidable competitive barrier. Building comparable infrastructure for bio-based plastics requires substantial investment and coordinated efforts across the entire value chain, from production to waste management.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Price Volatility & Supply Chain Stability of Bio-Feedstock | -0.9% | Global | 2025-2030 |

| Consumer & Industry Misconceptions about Bio-plastics | -0.7% | Global | 2025-2033 |

| Scalability of Production Technologies | -0.5% | Global | 2025-2028 |

| Competition from Established Fossil-based Plastic Infrastructure | -0.4% | Global | 2025-2033 |

Bio based Polyethylene Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Bio based Polyethylene market, covering its size, growth trends, drivers, restraints, opportunities, and challenges across various segments and key regions. The report offers a strategic overview of the market landscape, highlighting the competitive environment and the impact of technological advancements, including artificial intelligence. It serves as an essential guide for stakeholders seeking to understand market dynamics, identify growth prospects, and formulate effective business strategies in the evolving bio-plastics industry.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.5 Billion |

| Market Forecast in 2033 | USD 3.2 Billion |

| Growth Rate | 9.8% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Braskem, LyondellBasell Industries Holdings B.V., SABIC, TotalEnergies, Borealis AG, The Dow Chemical Company, Mitsui Chemicals, Inc., Neste, Versalis S.p.A., Avantium, Innovia Films, Eastman Chemical Company, Cardia Bioplastics (Sankei Chemical Co., Ltd.), FKuR Kunststoff GmbH, Solvay S.A., BIO-FED (AKRO-PLASTIC GmbH), Bio-On, TEIJIN LIMITED, DuPont de Nemours, Inc., Toray Industries, Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Bio based Polyethylene market is comprehensively segmented to provide a detailed understanding of its dynamics across different product types, applications, feedstock sources, and end-use industries. This granular segmentation allows for a precise analysis of demand patterns, technological advancements, and regional preferences, offering valuable insights into key growth areas and potential market shifts. Understanding these segments is crucial for stakeholders to identify specific opportunities and tailor their strategies to address diverse market needs and regulatory landscapes effectively.

The segmentation by type, specifically HDPE, LDPE, and LLDPE, reflects the various performance characteristics and applications of bio-polyethylene, while the application segmentation highlights the key sectors driving demand. Furthermore, the breakdown by feedstock underscores the ongoing efforts to diversify raw material sources for enhanced sustainability and supply chain resilience. This multi-faceted segmentation ensures a holistic view of the market, enabling thorough competitive analysis and strategic planning.

- By Type: High-Density Polyethylene (HDPE), Low-Density Polyethylene (LDPE), Linear Low-Density Polyethylene (LLDPE)

- By Application: Packaging (Rigid, Flexible), Consumer Goods, Automotive, Construction, Textiles, Agriculture, Others

- By Feedstock: Sugarcane, Corn, Cellulosic Biomass, Algae, Others

- By End-Use Industry: Food & Beverage, Cosmetics & Personal Care, Healthcare & Pharmaceuticals, Automotive & Transportation, Building & Construction, Electrical & Electronics, Textile & Apparel, Agriculture, Industrial

Regional Highlights

- North America: This region demonstrates robust growth driven by increasing consumer awareness regarding sustainable packaging, stringent environmental regulations, and significant investments in research and development of bio-based materials. The presence of major consumer goods and automotive industries also contributes significantly to demand.

- Europe: A pioneering region in sustainability, Europe exhibits strong market leadership due to proactive government policies, the European Green Deal initiatives, and high consumer adoption of eco-friendly products. Germany, France, and the UK are key markets, focusing on circular economy principles and sustainable packaging solutions.

- Asia Pacific (APAC): Expected to be the fastest-growing market, primarily fueled by rapid industrialization, growing populations, rising disposable incomes, and increasing environmental concerns in countries like China, India, and Japan. Government support for green manufacturing and foreign investments in bio-based industries are also critical factors.

- Latin America: Brazil is a prominent player, largely due to its substantial sugarcane production, which serves as a key feedstock for bio-polyethylene. The region is witnessing growing interest in sustainable solutions, driven by local environmental policies and export opportunities to global markets.

- Middle East and Africa (MEA): While currently a smaller market, the region shows nascent growth, especially in countries with burgeoning packaging and consumer goods sectors. Increasing awareness about sustainability and diversification efforts away from fossil fuels are expected to spur future adoption.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Bio based Polyethylene Market.- Braskem

- LyondellBasell Industries Holdings B.V.

- SABIC

- TotalEnergies

- Borealis AG

- The Dow Chemical Company

- Mitsui Chemicals, Inc.

- Neste

- Versalis S.p.A.

- Avantium

- Innovia Films

- Eastman Chemical Company

- Cardia Bioplastics (Sankei Chemical Co., Ltd.)

- FKuR Kunststoff GmbH

- Solvay S.A.

- BIO-FED (AKRO-PLASTIC GmbH)

- Bio-On

- TEIJIN LIMITED

- DuPont de Nemours, Inc.

- Toray Industries, Inc.

Frequently Asked Questions

What is Bio based Polyethylene?

Bio based Polyethylene (Bio-PE) is a type of polyethylene plastic produced from renewable biomass sources, such as sugarcane, corn, or other plant materials, instead of traditional fossil fuels. Chemically, it is identical to conventional polyethylene, making it recyclable in existing infrastructure, but its production significantly reduces carbon emissions and reliance on finite resources.

How is Bio based Polyethylene made?

Bio based Polyethylene is typically produced through the fermentation of sugars derived from biomass into ethanol. This ethanol is then dehydrated to produce ethylene, which is subsequently polymerized into polyethylene. This process results in a plastic that performs identically to petroleum-based PE but has a significantly lower carbon footprint.

What are the primary applications of Bio based Polyethylene?

Bio based Polyethylene is widely used across various industries, primarily for packaging (both rigid and flexible), consumer goods like toys and housewares, automotive components, construction materials such as pipes and films, and agricultural applications. Its identical properties to conventional PE allow for seamless integration into existing manufacturing processes.

Is Bio based Polyethylene biodegradable or compostable?

No, Bio based Polyethylene is not inherently biodegradable or compostable. While it is derived from renewable sources, its chemical structure is identical to conventional polyethylene, meaning it behaves similarly in terms of degradation. It is, however, fully recyclable within existing PE recycling streams, contributing to a circular economy.

What are the key benefits of using Bio based Polyethylene?

The primary benefits of using Bio based Polyethylene include a significant reduction in greenhouse gas emissions and carbon footprint compared to fossil-based plastics, decreased reliance on finite petroleum resources, and its compatibility with existing recycling infrastructure. It offers a sustainable alternative without compromising on performance or recyclability.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted