Bio Fouling Prevention Coating Market

Bio Fouling Prevention Coating Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703163 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

Bio Fouling Prevention Coating Market Size

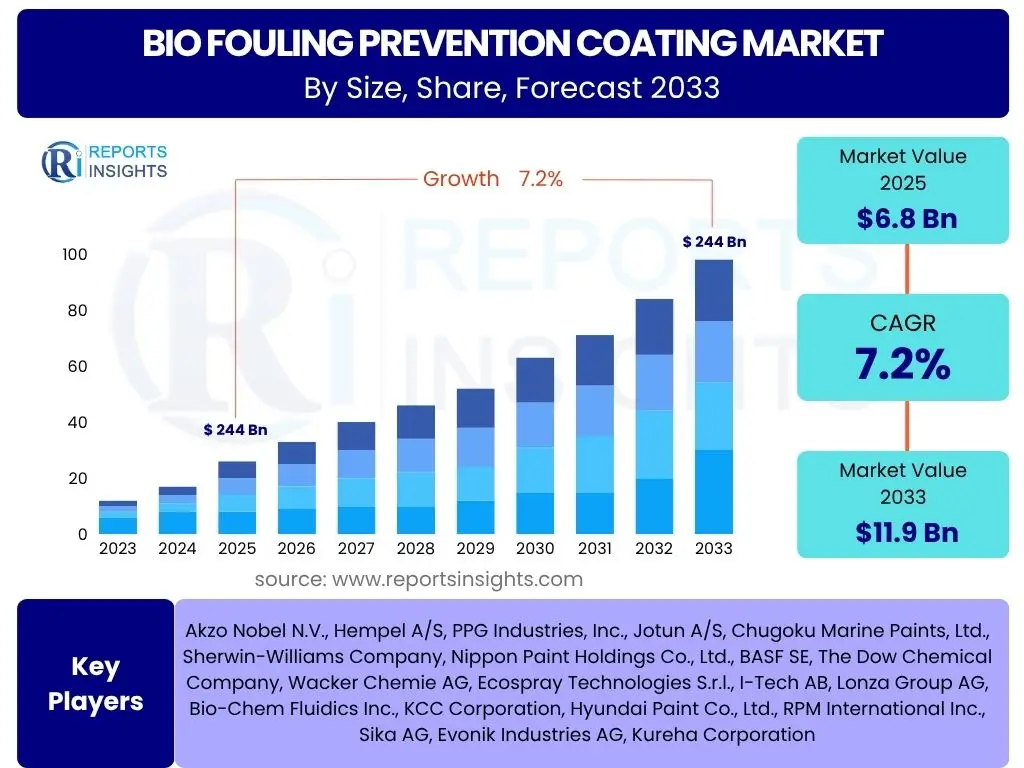

According to Reports Insights Consulting Pvt Ltd, The Bio Fouling Prevention Coating Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.2% between 2025 and 2033. The market is estimated at USD 6.8 billion in 2025 and is projected to reach USD 11.9 billion by the end of the forecast period in 2033.

Key Bio Fouling Prevention Coating Market Trends & Insights

The Bio Fouling Prevention Coating market is undergoing significant transformation driven by evolving environmental mandates and technological advancements. User inquiries frequently highlight the shift towards sustainable and eco-friendly solutions, particularly in response to stricter international maritime regulations aimed at protecting marine biodiversity. There is also considerable interest in innovative application methods and coating longevity, reflecting a desire for more cost-effective and efficient solutions that minimize reapplication frequency. Furthermore, the increasing global maritime trade and the expansion of offshore industries contribute to a continuous demand for advanced biofouling prevention strategies, prompting research into novel materials and smart coating technologies.

Consumers and industry stakeholders are keen to understand how anti-fouling technologies are adapting to the challenges posed by diverse aquatic environments, from freshwater to highly saline conditions, and how these coatings perform under varying operational stresses. This includes an emphasis on understanding the performance disparities between traditional biocide-based coatings and newer, non-toxic alternatives like fouling-release systems. The integration of advanced materials, such as nanotechnology and self-polishing copolymers, is a recurring theme in user questions, indicating a strong market pull for high-performance solutions that offer both efficacy and environmental compliance. The collective interest underscores a market poised for innovation, balancing economic viability with ecological responsibility.

- Growing demand for eco-friendly and biocide-free anti-fouling solutions driven by stringent environmental regulations.

- Technological advancements in nanotechnology and smart coatings leading to enhanced performance and longer durability.

- Increasing adoption of silicone-based fouling-release coatings due to their superior performance and environmental benefits.

- Expansion of global shipping activities and marine trade routes fueling demand for effective biofouling prevention.

- Rising investment in offshore oil and gas infrastructure and renewable energy installations requiring specialized coatings.

- Development of multi-functional coatings offering anti-fouling, corrosion protection, and drag reduction properties.

- Shift towards digital tools for monitoring coating performance and optimizing maintenance schedules.

AI Impact Analysis on Bio Fouling Prevention Coating

Common user questions regarding AI's influence on Bio Fouling Prevention Coating often revolve around its potential to revolutionize material discovery, optimize application processes, and enhance predictive maintenance. Users express interest in how artificial intelligence can accelerate the development of novel, high-performance coating formulations, particularly those that are environmentally benign and highly effective against a broad spectrum of biofoulants. There's a notable curiosity about AI's role in analyzing vast datasets related to marine environments, biofouling patterns, and coating performance to predict optimal coating selection and reapplication schedules, thereby reducing operational costs and environmental impact.

Furthermore, user queries frequently touch upon AI's capability to improve the efficiency and precision of coating application through robotic systems and smart sensors, minimizing waste and ensuring uniform coverage. The potential for AI-driven monitoring systems that can detect early signs of biofouling or coating degradation, enabling proactive maintenance, is another significant area of inquiry. Overall, the market anticipates AI as a transformative force that will not only streamline R&D and manufacturing but also enhance the in-service performance and sustainability of biofouling prevention coatings across various marine and industrial applications.

- Accelerated discovery and development of novel, eco-friendly coating materials through AI-driven molecular modeling and simulation.

- Optimization of coating formulations and application processes using machine learning algorithms for improved performance and reduced waste.

- Predictive analytics for marine vessel maintenance, allowing for data-driven scheduling of coating reapplication based on real-time environmental conditions and vessel usage.

- Enhanced monitoring of coating performance and biofouling accumulation through AI-powered sensor networks and image recognition.

- Streamlined supply chain and inventory management for coating manufacturers and applicators using AI-driven forecasting.

- Development of smart coatings with self-healing or self-cleaning properties, activated and optimized by embedded AI components.

- Improved quality control and fault detection during coating manufacturing via AI-powered inspection systems.

Key Takeaways Bio Fouling Prevention Coating Market Size & Forecast

Key takeaways from the Bio Fouling Prevention Coating market size and forecast consistently highlight the market's robust growth trajectory, driven primarily by an escalating global focus on environmental protection and the expansion of marine-dependent industries. Users frequently inquire about the segments expected to exhibit the highest growth rates, particularly those related to non-toxic or low-VOC (volatile organic compound) solutions, reflecting a strong market pull towards sustainability. The forecast underscores a sustained demand from the shipping and marine transport sector, which remains the largest end-use segment, continually seeking advanced solutions to improve vessel efficiency and comply with international regulations.

Another significant insight derived from market size and forecast inquiries is the increasing regional disparities in market growth, with Asia Pacific emerging as a dominant force due to its burgeoning shipbuilding and aquaculture industries. The shift towards innovative materials and application technologies, such as drone-based coating inspections and robotic application systems, signals a technologically progressive market. Overall, the market is characterized by a dynamic interplay of regulatory pressures, technological innovation, and economic incentives, all contributing to a healthy growth outlook for biofouling prevention coatings, with a clear emphasis on effective, durable, and environmentally sound solutions.

- The market is poised for significant expansion, driven by regulatory demands for environmental protection and efficiency in maritime operations.

- Asia Pacific is expected to remain a leading region for market growth, fueled by strong shipbuilding and aquaculture activities.

- Investments in research and development for sustainable and biocide-free coating technologies are critical for future market leadership.

- Fouling-release coatings and other eco-friendly alternatives will capture an increasing market share over the forecast period.

- Digitalization and automation in coating application and monitoring will enhance efficiency and extend product lifespan.

Bio Fouling Prevention Coating Market Drivers Analysis

The Bio Fouling Prevention Coating market is propelled by several critical drivers that collectively underscore its expansion and innovation. A primary driver is the stringent environmental regulations imposed by international bodies like the International Maritime Organization (IMO) and regional environmental agencies. These regulations aim to curb the spread of invasive aquatic species and reduce the release of harmful biocides into marine ecosystems, thereby mandating the adoption of more effective and eco-friendly anti-fouling solutions. This regulatory push compels industries, particularly maritime and aquaculture, to invest in advanced coatings that adhere to strict environmental standards while maintaining operational efficiency.

Another significant driver is the continuous growth in global maritime trade and the expansion of the shipbuilding industry, particularly in emerging economies. As more vessels navigate international waters, the need for efficient biofouling prevention becomes paramount to reduce fuel consumption, minimize maintenance costs, and extend the lifespan of marine assets. Furthermore, the increasing focus on energy efficiency across industries has led to a greater appreciation for how effective anti-fouling coatings can reduce hydrodynamic drag on vessels, directly translating into significant fuel savings and reduced carbon emissions. The burgeoning aquaculture sector, aiming to prevent biofouling on fish cages and nets, also contributes substantially to market demand, ensuring the health and productivity of farmed aquatic species.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent Environmental Regulations | +1.5% | Global, particularly Europe, North America, IMO Member States | Short to Medium Term (2025-2029) |

| Growth in Global Seaborne Trade & Shipbuilding | +1.2% | Asia Pacific (China, South Korea, Japan), Europe | Medium to Long Term (2027-2033) |

| Increasing Focus on Fuel Efficiency & Emissions Reduction | +0.8% | Global, especially major shipping routes | Short to Medium Term (2025-2029) |

| Expansion of Aquaculture Industry | +0.7% | Asia Pacific, Europe (Norway), Latin America | Medium Term (2026-2031) |

| Technological Advancements in Coating Formulations | +1.0% | Global, R&D Hubs (Germany, USA, Japan) | Medium to Long Term (2027-2033) |

Bio Fouling Prevention Coating Market Restraints Analysis

Despite significant growth drivers, the Bio Fouling Prevention Coating market faces several notable restraints that could impede its full potential. One significant restraint is the high initial cost associated with advanced anti-fouling and fouling-release coatings, which can be a deterrent for smaller shipping companies or those operating on tight budgets. While these coatings offer long-term benefits in terms of fuel savings and extended dry-docking intervals, the upfront investment can be substantial, limiting adoption, especially in price-sensitive markets. This cost factor often leads to a preference for traditional, less expensive but environmentally less favorable options, particularly in regions with less stringent regulatory enforcement.

Another major challenge revolves around the environmental concerns associated with traditional biocide-based coatings. Although regulations are pushing towards greener alternatives, some commonly used biocides, like copper-based compounds, continue to raise ecological concerns due to their potential toxicity to non-target marine organisms. This scrutiny necessitates continuous research and development into safer, yet equally effective, alternatives, which is a costly and time-consuming process. Furthermore, the limited lifespan of certain biofouling prevention coatings, requiring frequent reapplication, contributes to higher operational costs and downtime for marine vessels. The lack of standardized testing protocols and performance metrics across the globe also poses a challenge, making it difficult for end-users to compare and select the most suitable coating solutions, thus creating market fragmentation and hindering widespread adoption of premium products.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Cost of Advanced Coatings | -0.9% | Global, particularly developing economies | Short to Medium Term (2025-2029) |

| Environmental Concerns of Biocide Leaching | -0.7% | Global, especially Europe, North America | Short to Medium Term (2025-2030) |

| Need for Frequent Re-application for Some Coatings | -0.6% | Global, impacting operational costs | Medium Term (2026-2031) |

| Regulatory Hurdles and Compliance Complexity | -0.5% | Regional (e.g., California, EU), specific ports | Ongoing |

| Competition from Alternative Biofouling Management Methods | -0.4% | Global, particularly for niche applications | Long Term (2028-2033) |

Bio Fouling Prevention Coating Market Opportunities Analysis

The Bio Fouling Prevention Coating market presents numerous opportunities for innovation and growth, primarily driven by the imperative for sustainable and high-performance solutions. A significant opportunity lies in the development and commercialization of entirely eco-friendly and non-toxic coating formulations. This includes research into biomimetic surfaces, non-biocidal anti-fouling agents, and advanced fouling-release technologies that can effectively prevent marine growth without harming the environment. As environmental regulations become more pervasive and stringent globally, coatings that can meet zero-biocide discharge standards will command a premium and capture a larger market share, opening new avenues for companies focusing on green chemistry.

Furthermore, the expansion into niche applications beyond traditional shipping, such as offshore renewable energy infrastructure (wind turbines, tidal energy devices), subsea pipelines, aquaculture facilities, and even recreational boats, offers substantial growth potential. These segments have unique operational challenges and environmental considerations, necessitating specialized coating solutions tailored to their specific needs. The integration of smart technologies, including self-cleaning surfaces, autonomous monitoring systems, and coatings with embedded sensors for real-time performance tracking, represents another promising opportunity. These advancements not only enhance the efficacy and longevity of coatings but also provide valuable data for optimizing maintenance schedules and improving operational efficiency, thereby increasing their value proposition to end-users and fostering long-term strategic partnerships.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Eco-friendly, Non-Toxic Coatings | +1.3% | Global, especially Europe, North America, advanced R&D hubs | Medium to Long Term (2026-2033) |

| Expansion into Niche Applications (Offshore Renewables, Aquaculture) | +1.0% | Europe, Asia Pacific, North America coastal regions | Medium Term (2026-2031) |

| Integration of Smart Coatings and Sensor Technologies | +0.9% | Global, technology-driven economies | Long Term (2028-2033) |

| Market Penetration in Developing Economies | +0.7% | Asia Pacific, Latin America, Africa | Medium to Long Term (2027-2033) |

| Strategic Partnerships and Collaborations for R&D | +0.6% | Global, cross-industry (material science, marine, IT) | Short to Medium Term (2025-2029) |

Bio Fouling Prevention Coating Market Challenges Impact Analysis

The Bio Fouling Prevention Coating market faces significant challenges that demand innovative solutions and strategic adaptation from industry players. One critical challenge is achieving consistent long-term efficacy across diverse and dynamic marine environments. Coatings must perform optimally in varying water temperatures, salinity levels, water flow rates, and biological compositions, which is a complex technical hurdle. Many coatings, especially those relying on biocide leaching, experience a decline in performance over time, necessitating frequent reapplication or dry-docking, which adds to operational costs and vessel downtime. Developing a universal, durable, and truly long-lasting solution remains an elusive goal for the industry.

Another prominent challenge is the increasing regulatory complexity and the fragmented nature of global environmental standards. While regulations push for greener solutions, the specific requirements can vary significantly by region, country, or even port, creating compliance challenges for international shipping companies. This regulatory patchwork demands extensive R&D to develop coatings that meet multiple, often conflicting, environmental criteria, hindering product standardization and market entry. Furthermore, the high research and development costs associated with developing novel, environmentally compliant, and highly effective coating technologies, coupled with the extended time-to-market due to rigorous testing and approval processes, pose substantial financial burdens on manufacturers. Intense competition from alternative fouling management solutions, such as in-water cleaning technologies and mechanical removal, also presents a competitive pressure, compelling coating manufacturers to continuously innovate and demonstrate superior value proposition.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Achieving Long-Term Efficacy in Diverse Marine Environments | -0.8% | Global, all operational areas | Ongoing |

| High Research & Development Costs and Time-to-Market | -0.7% | Global, particularly for innovative products | Medium to Long Term (2026-2033) |

| Regulatory Divergence and Compliance Complexity | -0.6% | Global, affecting international fleets | Ongoing |

| Disposal and End-of-Life Management of Coated Waste | -0.5% | Coastal nations, shipbreaking yards | Medium Term (2027-2032) |

| Competition from Mechanical & Alternative Fouling Control Methods | -0.4% | Global, particularly for niche applications | Short to Medium Term (2025-2030) |

Bio Fouling Prevention Coating Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Bio Fouling Prevention Coating market, offering a detailed understanding of its current landscape, historical performance, and future growth trajectories. It covers key market dynamics including drivers, restraints, opportunities, and challenges, along with a thorough impact analysis of these factors on the market's Compound Annual Growth Rate (CAGR). The report delves into extensive segmentation analysis based on coating type, application, end-use industry, and substrate, providing granular insights into each segment's contribution to market growth. Furthermore, it includes a detailed regional analysis, highlighting market trends and opportunities across major geographical areas. The competitive landscape section profiles key players, outlining their strategies, product portfolios, and recent developments to provide a complete overview of the industry's competitive intensity.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 6.8 Billion |

| Market Forecast in 2033 | USD 11.9 Billion |

| Growth Rate | 7.2% |

| Number of Pages | 267 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Akzo Nobel N.V., Hempel A/S, PPG Industries, Inc., Jotun A/S, Chugoku Marine Paints, Ltd., Sherwin-Williams Company, Nippon Paint Holdings Co., Ltd., BASF SE, The Dow Chemical Company, Wacker Chemie AG, Ecospray Technologies S.r.l., I-Tech AB, Lonza Group AG, Bio-Chem Fluidics Inc., KCC Corporation, Hyundai Paint Co., Ltd., RPM International Inc., Sika AG, Evonik Industries AG, Kureha Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Bio Fouling Prevention Coating market is meticulously segmented to provide a granular understanding of its diverse components and their respective growth trajectories. These segmentations are critical for identifying key revenue streams, understanding specific market needs, and developing targeted strategies. The primary segments include categorization by coating type, application area, end-use industry, and the substrate material to which the coatings are applied. Each segment exhibits unique dynamics influenced by regulatory frameworks, technological advancements, and specific operational requirements.

Understanding these segments allows market participants to tailor their product offerings and marketing efforts to specific client needs, ranging from large commercial shipping fleets requiring high-performance anti-fouling solutions to aquaculture farms demanding environmentally benign coatings for their nets. The detailed breakdown provides insights into which technologies are gaining traction in particular niches, such as the growing adoption of biocide-free coatings for recreational vessels due to increasing environmental awareness among consumers. This comprehensive segmentation analysis serves as a foundational element for strategic planning and competitive positioning within the global biofouling prevention market.

- By Type:

- Anti-fouling Coatings: Traditional biocide-based coatings designed to release active substances to prevent marine growth.

- Fouling-Release Coatings: Non-toxic, silicone-based coatings that create a slippery surface, preventing organisms from adhering strongly and allowing them to be removed by water flow or simple cleaning.

- Biocide-Free Coatings: Innovative coatings employing physical or mechanical properties, or natural compounds, to deter fouling without releasing harmful chemicals.

- Other Coatings: Includes hybrid systems, self-polishing copolymers, and advanced materials still under development or niche applications.

- By Application:

- Ship Hulls: The largest application segment, critical for maintaining vessel speed, fuel efficiency, and structural integrity.

- Propellers & Rudders: Specialized coatings for these high-movement components to prevent performance degradation.

- Offshore Structures: Coatings for oil & gas rigs, offshore wind turbine foundations, and other fixed marine installations.

- Aquaculture Cages & Nets: Essential for preventing biofouling on fish and shellfish farming equipment, ensuring water flow and preventing disease.

- Subsea Pipelines: Coatings for underwater pipelines to prevent blockage and structural damage from marine growth.

- Moorings & Buoys: Protection for navigational aids and anchoring systems.

- Others: Includes recreational boats, pontoons, and coastal defense structures.

- By End-Use Industry:

- Marine Transport: Encompasses commercial shipping (cargo, tankers, cruise ships), naval vessels, and ferries.

- Oil & Gas: Primarily for offshore platforms, drilling rigs, and subsea infrastructure.

- Energy: Focused on renewable energy installations like offshore wind, wave, and tidal energy devices.

- Aquaculture: Addressing the needs of fish and shellfish farming operations.

- Recreational Marine: For yachts, sailboats, and other leisure craft.

- By Substrate:

- Metal: Coatings applied to steel, aluminum, and other metal components of marine structures.

- Composites: For fiberglass, carbon fiber, and other composite materials common in modern shipbuilding and recreational vessels.

- Others: Includes wood, concrete, and other specialized materials.

Regional Highlights

- Asia Pacific: This region dominates the bio fouling prevention coating market, primarily driven by its robust shipbuilding industry in countries like China, South Korea, and Japan. The rapid expansion of international trade and the burgeoning aquaculture sector, particularly in Southeast Asia, further fuel demand. Increasing environmental awareness and the gradual adoption of stricter regulations are also contributing to the shift towards advanced, eco-friendly coatings.

- Europe: A mature market characterized by stringent environmental regulations and a strong focus on sustainable solutions. European countries, including Norway, Denmark, and Germany, are at the forefront of adopting biocide-free and fouling-release technologies. The region's significant investments in offshore renewable energy and advanced maritime technologies also drive demand for high-performance coatings.

- North America: This market is driven by increasing maritime activity, including commercial shipping, offshore oil & gas exploration, and a substantial recreational marine sector. Regulatory bodies like the U.S. Environmental Protection Agency (EPA) are influencing the shift towards greener coatings. Technological innovation and the presence of key industry players also contribute to market growth in this region.

- Latin America: Expected to show steady growth, primarily due to expanding shipbuilding activities in Brazil and a growing focus on the fishing and aquaculture industries across the region. While environmental regulations are less stringent than in Europe or North America, increasing global trade and awareness are gradually pushing for better biofouling management.

- Middle East & Africa (MEA): This region is experiencing growth driven by investments in port infrastructure, expansion of the oil & gas industry, and strategic positioning along major shipping routes. While adoption of advanced coatings is still evolving, the long-term potential is significant as economic diversification and environmental consciousness increase.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Bio Fouling Prevention Coating Market.- Akzo Nobel N.V.

- Hempel A/S

- PPG Industries, Inc.

- Jotun A/S

- Chugoku Marine Paints, Ltd.

- Sherwin-Williams Company

- Nippon Paint Holdings Co., Ltd.

- BASF SE

- The Dow Chemical Company

- Wacker Chemie AG

- Ecospray Technologies S.r.l.

- I-Tech AB

- Lonza Group AG

- Bio-Chem Fluidics Inc.

- KCC Corporation

- Hyundai Paint Co., Ltd.

- RPM International Inc.

- Sika AG

- Evonik Industries AG

- Kureha Corporation

Frequently Asked Questions

What is biofouling and why is its prevention important?

Biofouling refers to the accumulation of marine organisms such as algae, barnacles, and mussels on submerged surfaces. Its prevention is crucial for marine vessels and structures as it significantly increases hydrodynamic drag, leading to higher fuel consumption (up to 40% more) and increased carbon emissions. Biofouling also accelerates corrosion, reduces the lifespan of marine assets, and can facilitate the transfer of invasive aquatic species across ecosystems, posing severe ecological threats.

What are the primary types of biofouling prevention coatings?

The primary types of biofouling prevention coatings include Anti-fouling Coatings, which typically release biocides to deter marine growth; Fouling-Release Coatings, which create a slick surface (often silicone-based) that prevents organisms from adhering strongly, allowing them to be removed by water flow; and Biocide-Free Coatings, which employ innovative physical or mechanical properties or natural extracts to prevent adhesion without toxic chemical release.

Which end-use industries are major consumers of biofouling prevention coatings?

The major end-use industries consuming biofouling prevention coatings are Marine Transport (including commercial shipping, naval vessels, and ferries), the Oil & Gas sector (for offshore platforms and subsea infrastructure), the Energy sector (specifically for offshore wind and other renewable energy installations), and the rapidly expanding Aquaculture industry for fish cages and nets.

What are the key drivers for the Bio Fouling Prevention Coating market's growth?

Key drivers include stringent environmental regulations imposed by international maritime organizations and national governments to reduce biocide leaching and invasive species transfer, the increasing global seaborne trade and expansion of the shipbuilding industry, and a growing emphasis on fuel efficiency and emissions reduction across marine operations. The burgeoning aquaculture industry's need for effective fouling control also plays a significant role.

What are the emerging trends in biofouling prevention coating technology?

Emerging trends include the intensified focus on developing eco-friendly and biocide-free solutions, the integration of nanotechnology for enhanced coating performance and durability, the rise of smart coatings with self-healing or sensor capabilities for real-time monitoring, and the increasing adoption of digital tools for optimizing coating application and maintenance schedules.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted