Automotive Embedded Telematic Market

Automotive Embedded Telematic Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703231 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

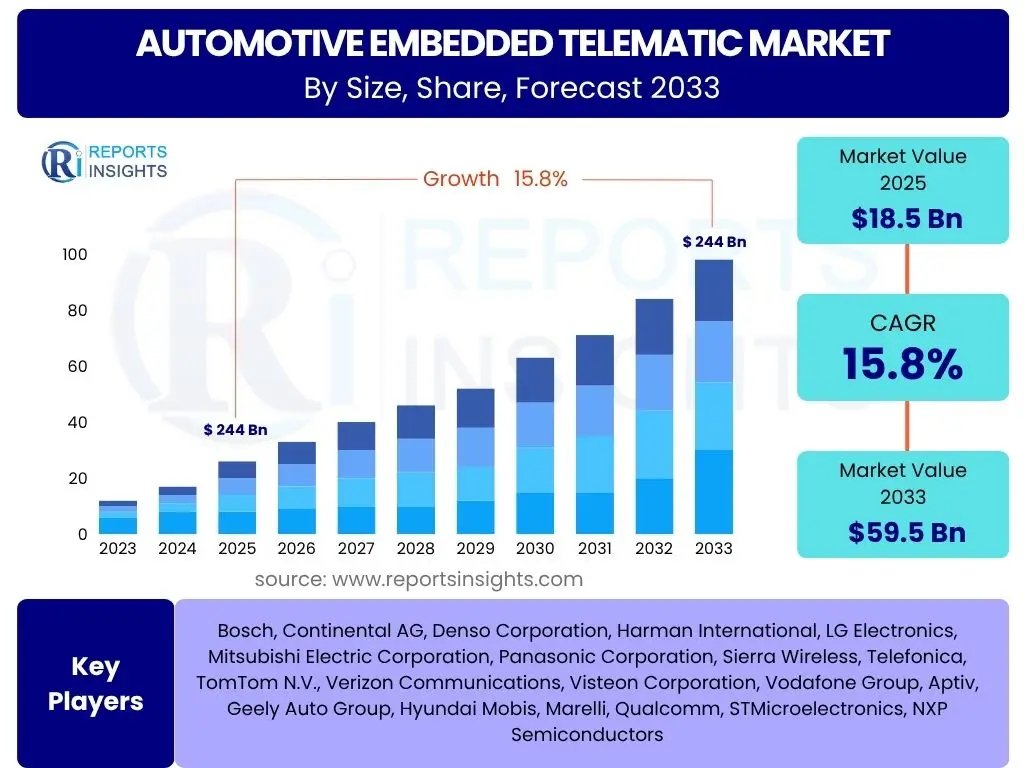

Automotive Embedded Telematic Market Size

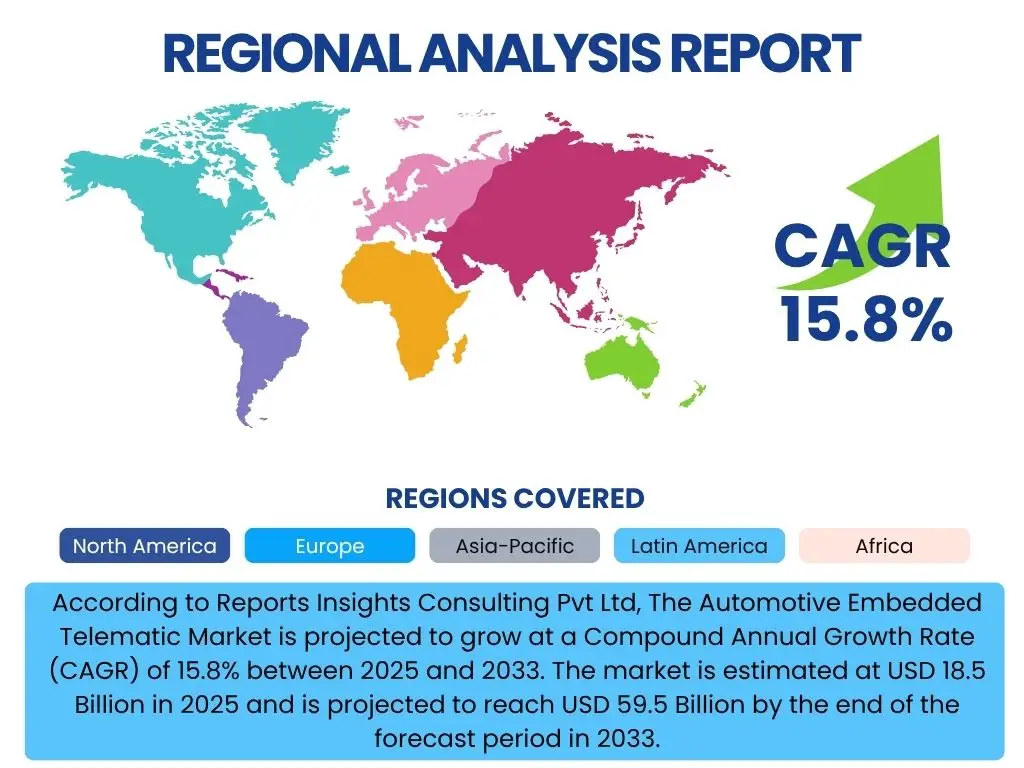

According to Reports Insights Consulting Pvt Ltd, The Automotive Embedded Telematic Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 15.8% between 2025 and 2033. The market is estimated at USD 18.5 Billion in 2025 and is projected to reach USD 59.5 Billion by the end of the forecast period in 2033.

Key Automotive Embedded Telematic Market Trends & Insights

The automotive embedded telematics market is experiencing a significant transformation driven by advancements in connectivity, data analytics, and regulatory mandates. Users frequently inquire about the integration of 5G technology, the expansion of V2X (Vehicle-to-Everything) communication capabilities, and the increasing focus on cybersecurity within connected vehicle ecosystems. There is also considerable interest in the shift towards subscription-based services and the monetization of vehicle data, indicating a move beyond basic navigation and emergency services to a more comprehensive digital automotive experience. These trends collectively underscore the industry's pivot towards creating safer, more efficient, and highly personalized driving environments.

The market is further influenced by the growing demand for advanced driver-assistance systems (ADAS) and autonomous driving features, which heavily rely on robust embedded telematics solutions for real-time data processing and communication. The convergence of hardware and software platforms is also a key trend, enabling over-the-air (OTA) updates and flexible feature deployments, thus future-proofing vehicles. Furthermore, environmental concerns and government initiatives promoting electric vehicles (EVs) are pushing for telematics solutions that support charging infrastructure management, battery monitoring, and route optimization, contributing to a greener automotive landscape. These elements are shaping the next generation of connected vehicles.

- Proliferation of 5G connectivity for enhanced data speeds and low latency.

- Expansion of Vehicle-to-Everything (V2X) communication for improved road safety and traffic management.

- Increasing integration of cloud-based platforms for data processing and service delivery.

- Growing emphasis on cybersecurity measures to protect vehicle systems and personal data.

- Shift towards subscription-based and on-demand connected car services.

- Development of advanced telematics for electric vehicles (EVs), including battery management and charging solutions.

- Rise of software-defined vehicles enabling over-the-air (OTA) updates and feature upgrades.

AI Impact Analysis on Automotive Embedded Telematic

Artificial intelligence is profoundly reshaping the automotive embedded telematics landscape, addressing user inquiries about how vehicles can become more intelligent, proactive, and personalized. AI's core impact lies in its ability to process vast amounts of real-time vehicle data, leading to enhanced predictive maintenance, optimized vehicle performance, and improved safety features. Users are keen to understand how AI algorithms analyze driving patterns, environmental conditions, and vehicle diagnostics to offer actionable insights, thereby minimizing downtime and enhancing overall reliability. Furthermore, AI is central to the development of highly sophisticated ADAS and autonomous driving systems, enabling vehicles to perceive, understand, and react to their surroundings with unprecedented accuracy.

The influence of AI extends to personalized in-car experiences, where algorithms learn user preferences for infotainment, climate control, and route planning, creating a truly tailored environment. Concerns often revolve around data privacy and the ethical implications of AI-driven decision-making in autonomous contexts, prompting developers to focus on robust, transparent, and secure AI frameworks. Moreover, AI-powered natural language processing is enhancing voice control interfaces within vehicles, making interactions more intuitive and reducing driver distraction. This comprehensive integration positions AI as a fundamental enabler for the next generation of connected and intelligent automotive embedded telematics solutions.

- Enabling predictive maintenance through real-time data analysis and anomaly detection.

- Enhancing advanced driver-assistance systems (ADAS) with superior object recognition and decision-making capabilities.

- Personalizing in-car experiences, including infotainment, navigation, and climate control, based on user behavior.

- Optimizing route planning and traffic management through AI-driven algorithms.

- Facilitating autonomous driving capabilities by processing sensor data and enabling complex decision-making.

- Improving vehicle cybersecurity by identifying and neutralizing potential threats in real time.

- Powering advanced voice recognition and natural language processing for intuitive in-car controls.

Key Takeaways Automotive Embedded Telematic Market Size & Forecast

The automotive embedded telematics market is poised for robust growth, driven by an increasing integration of advanced connectivity solutions and a rising demand for enhanced safety, convenience, and efficiency in vehicles. Common user questions highlight the market's trajectory, emphasizing its significant expansion from 2025 to 2033. This growth is underpinned by factors such as stringent regulatory mandates for eCall systems, the escalating adoption of electric vehicles, and the proliferation of sophisticated infotainment and navigation systems. The forecast indicates a substantial increase in market valuation, reflecting a fundamental shift in automotive design and consumer expectations towards digitally integrated and smart vehicles.

A crucial takeaway is the pervasive influence of digital transformation within the automotive industry, where embedded telematics acts as a central nervous system for connected cars. The market's expansion is not merely quantitative but also qualitative, involving the evolution of services from basic tracking to complex data analytics, remote diagnostics, and predictive functionalities. The compounding annual growth rate signals a sustained momentum, fueled by continuous innovation in communication technologies and the increasing willingness of consumers to embrace connected features. Ultimately, the market is transforming vehicles into mobile data hubs, promising a future of smarter, safer, and more personalized mobility experiences.

- Significant market expansion anticipated from USD 18.5 Billion in 2025 to USD 59.5 Billion by 2033.

- Compound Annual Growth Rate (CAGR) of 15.8% signifies strong, sustained market momentum.

- Growth driven by regulatory compliance, consumer demand for connectivity, and technological advancements.

- Shift towards advanced services like predictive maintenance, remote diagnostics, and infotainment.

- Increasing penetration of embedded telematics in both traditional and electric vehicle segments.

- Market evolution towards comprehensive digital ecosystems within the automotive sector.

Automotive Embedded Telematic Market Drivers Analysis

The automotive embedded telematics market is primarily propelled by a confluence of regulatory imperatives, the escalating demand for advanced vehicle features, and significant technological advancements in connectivity. Governments worldwide are increasingly mandating embedded telematics systems, particularly for emergency call services, which forms a foundational driver for market expansion. Furthermore, consumer expectations for enhanced safety, convenience, and infotainment options are pushing automotive manufacturers to integrate sophisticated telematics solutions into new vehicle models. This growing demand extends to features like real-time navigation, remote diagnostics, and vehicle tracking, making telematics an indispensable component of modern automobiles.

Technological innovation, particularly in areas like 5G network deployment and advanced sensor integration, is further fueling market growth. These advancements enable faster data transmission, lower latency, and more reliable communication between vehicles and infrastructure, unlocking new possibilities for connected services and autonomous driving capabilities. The global shift towards electric vehicles (EVs) also acts as a powerful driver, as embedded telematics plays a crucial role in monitoring battery health, optimizing charging, and managing range anxiety for EV owners. These multifaceted drivers collectively ensure a robust and sustained growth trajectory for the automotive embedded telematics market.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Government Regulations and Mandates (e.g., eCall) | +3.5% | Europe, Russia, Brazil, India | 2025-2033 |

| Growing Demand for Connected Car Services & Infotainment | +3.0% | North America, Europe, Asia Pacific (China, Japan) | 2025-2033 |

| Rising Adoption of Electric Vehicles (EVs) | +2.5% | Global, particularly China, Europe, North America | 2025-2033 |

| Advancements in 5G Technology and IoT Integration | +2.0% | Global | 2026-2033 | Increasing Focus on Vehicle Safety and Security Features | +1.8% | North America, Europe | 2025-2030 |

Automotive Embedded Telematic Market Restraints Analysis

Despite the strong growth prospects, the automotive embedded telematics market faces several significant restraints that could impede its full potential. A primary concern revolves around cybersecurity threats and data privacy issues. As vehicles become increasingly connected and generate vast amounts of personal and operational data, the risk of cyberattacks and unauthorized data access grows. This vulnerability creates a reluctance among some consumers to fully embrace connected services and requires substantial investment from manufacturers to develop robust security protocols, which can increase overall system costs and complexity.

Another key restraint is the high initial cost associated with integrating embedded telematics systems into vehicles, which can deter adoption, especially in price-sensitive market segments. Furthermore, the lack of standardized communication protocols and interoperability issues between different telematics systems and vehicle manufacturers poses challenges. This fragmentation can hinder seamless data exchange and create compatibility problems for third-party service providers. Additionally, limited telecommunications infrastructure in remote or underdeveloped regions can restrict the functionality and reach of embedded telematics services, thereby slowing market penetration in those areas. Overcoming these restraints requires collaborative efforts across the industry, regulatory bodies, and infrastructure providers.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Cybersecurity Concerns and Data Privacy Risks | -2.2% | Global | 2025-2033 |

| High Initial Cost of Implementation and Integration | -1.8% | Developing Economies, Price-Sensitive Markets | 2025-2030 |

| Lack of Standardization and Interoperability Issues | -1.5% | Global | 2025-2029 |

| Limited Telecommunications Infrastructure in Remote Areas | -1.0% | Africa, parts of Asia Pacific, Latin America | 2025-2033 |

Automotive Embedded Telematic Market Opportunities Analysis

The automotive embedded telematics market is ripe with opportunities, particularly in the expansion of value-added services and the integration with emerging mobility solutions. A significant opportunity lies in the proliferation of Usage-Based Insurance (UBI) and other data-driven insurance models, where telematics data can provide real-time insights into driving behavior, leading to personalized premiums and reduced risk for insurers. This not only benefits insurance providers but also incentivizes safer driving practices among consumers. Furthermore, the growth of shared mobility services and fleet management solutions presents a substantial avenue for telematics, enabling efficient vehicle tracking, maintenance scheduling, and operational optimization for large fleets.

The advent of Vehicle-to-Everything (V2X) communication, including V2I (Vehicle-to-Infrastructure) and V2N (Vehicle-to-Network), offers unprecedented opportunities for smart city integration and enhanced traffic management. Telematics systems are crucial for enabling vehicles to communicate with traffic signals, road sensors, and other infrastructure elements, paving the way for more efficient and safer urban environments. Moreover, the increasing adoption of over-the-air (OTA) updates for vehicle software and features presents an ongoing revenue stream for manufacturers and an opportunity to deliver continuous value to consumers. These opportunities underscore the market's potential for diversification and sustained growth beyond traditional telematics functionalities.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion of Usage-Based Insurance (UBI) and Data-Driven Services | +2.8% | North America, Europe, Asia Pacific | 2025-2033 |

| Growth in Shared Mobility and Fleet Management Solutions | +2.5% | Global, particularly urban centers | 2025-2033 |

| Development of V2X (Vehicle-to-Everything) Communication Infrastructure | +2.0% | North America, Europe, China | 2027-2033 |

| Increasing Adoption of Over-the-Air (OTA) Updates | +1.7% | Global | 2025-2033 |

| Integration with Smart City and Intelligent Transportation Systems | +1.5% | Global | 2028-2033 |

Automotive Embedded Telematic Market Challenges Impact Analysis

The automotive embedded telematics market faces several inherent challenges that demand strategic solutions to ensure sustainable growth. One significant challenge is managing the exponential increase in data generated by connected vehicles, leading to issues related to data storage, processing, and analytics capabilities. Ensuring the secure and efficient transmission of this vast amount of data, especially for real-time applications like autonomous driving, requires robust and scalable infrastructure, which can be costly and complex to implement. Furthermore, the regulatory landscape for data governance and privacy varies significantly across regions, posing compliance challenges for global automotive manufacturers and service providers.

Another major challenge is consumer acceptance and willingness to pay for connected services, particularly in markets where the perceived value might not yet justify the additional cost. Educating consumers about the benefits of telematics, beyond basic navigation, is crucial for wider adoption. Additionally, the rapid pace of technological evolution in communication technologies (e.g., from 4G to 5G and beyond) requires continuous investment in hardware and software updates, potentially leading to obsolescence issues for older systems. Addressing these challenges effectively will be key to unlocking the full potential of the automotive embedded telematics market and ensuring its long-term viability.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Managing Big Data and Data Analytics Complexity | -1.9% | Global | 2025-2033 |

| Ensuring Consumer Acceptance and Willingness to Pay | -1.7% | Emerging Markets, Price-Sensitive Demographics | 2025-2030 |

| Compliance with Evolving Data Governance and Privacy Regulations | -1.5% | Europe (GDPR), North America, Asia Pacific | 2025-2033 |

| Rapid Technological Obsolescence and Need for Continuous Updates | -1.2% | Global | 2025-2033 |

Automotive Embedded Telematic Market - Updated Report Scope

This market insights report provides a comprehensive analysis of the global Automotive Embedded Telematic Market, covering its current size, historical performance, and future growth projections up to 2033. The scope encompasses detailed segmentation by component, connectivity, application, vehicle type, and end-use, offering granular insights into various market dynamics. It also includes an in-depth examination of key market trends, growth drivers, restraints, opportunities, and challenges influencing the industry landscape. The report provides a robust framework for stakeholders to understand market behavior, identify growth avenues, and formulate strategic decisions within this rapidly evolving sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 18.5 Billion |

| Market Forecast in 2033 | USD 59.5 Billion |

| Growth Rate | 15.8% |

| Number of Pages | 267 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Bosch, Continental AG, Denso Corporation, Harman International, LG Electronics, Mitsubishi Electric Corporation, Panasonic Corporation, Sierra Wireless, Telefonica, TomTom N.V., Verizon Communications, Visteon Corporation, Vodafone Group, Aptiv, Geely Auto Group, Hyundai Mobis, Marelli, Qualcomm, STMicroelectronics, NXP Semiconductors |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The automotive embedded telematics market is comprehensively segmented across various dimensions to provide a detailed understanding of its diverse components and applications. These segmentations allow for a granular analysis of market dynamics, revealing specific growth drivers and challenges within each category. The market is primarily broken down by component, distinguishing between the hardware elements that enable connectivity, the software that processes and manages data, and the extensive range of services delivered through telematics systems. This layered approach helps identify where the most significant innovations and investments are occurring, from the core processing units to the sophisticated cloud-based applications that enhance user experience.

Further segmentation by connectivity type highlights the evolution from older 2G/3G networks to the high-speed, low-latency capabilities of 4G/LTE and emerging 5G technologies, as well as the niche role of satellite connectivity for global reach. Application-based segmentation reveals the diverse functionalities of telematics, ranging from critical safety and security features to advanced infotainment, vehicle management, and specialized insurance telematics. Analyzing the market by vehicle type, namely passenger and commercial vehicles, underscores the differing needs and adoption rates across these broad categories. Finally, the end-use segmentation differentiates between Original Equipment Manufacturers (OEMs) and the aftermarket, illustrating distinct distribution channels and business models within the industry. These classifications are vital for understanding the multifaceted structure and growth potential of the market.

- By Component:

- Hardware (Telematics Control Unit (TCU), GPS Modules, Communication Modules, Sensors)

- Software (Embedded Software, Cloud-based Software)

- Services (Connected Services, Emergency Services, Navigation Services, Fleet Management Services, Infotainment Services)

- By Connectivity:

- 2G/3G

- 4G/LTE

- 5G

- Satellite Connectivity

- By Application:

- Safety & Security (eCall/bCall, Roadside Assistance, Stolen Vehicle Recovery)

- Infotainment & Navigation (In-car Entertainment, Real-time Traffic Information, POI Search)

- Vehicle Management (Remote Diagnostics, Predictive Maintenance, Fuel Management, Fleet Tracking)

- Insurance Telematics (Usage-Based Insurance)

- Other Applications (e.g., V2X Communication, Autonomous Driving Data)

- By Vehicle Type:

- Passenger Vehicles

- Commercial Vehicles (Light Commercial Vehicles, Heavy Commercial Vehicles)

- By End Use:

- OEM

- Aftermarket

Regional Highlights

- North America: This region is a leading market for automotive embedded telematics, driven by early adoption of connected car technologies, a strong presence of major automotive OEMs, and increasing consumer demand for advanced safety and convenience features. Stringent regulatory frameworks for vehicle safety and the rapid rollout of 5G infrastructure further accelerate market growth. The region sees high penetration of services like remote diagnostics, navigation, and emergency assistance.

- Europe: Europe represents a mature market, significantly influenced by mandatory eCall regulations (mandating automatic crash notification systems in new cars since 2018), which have provided a strong impetus for telematics adoption. The region is also a hub for innovation in connected and autonomous driving technologies, with a strong focus on data privacy (GDPR) and cybersecurity, shaping the development of secure and compliant telematics solutions.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing market, primarily fueled by rapid urbanization, increasing disposable incomes, and the booming automotive manufacturing sector, particularly in China, Japan, and India. Government initiatives promoting smart cities and electric vehicles, coupled with a large and tech-savvy consumer base, are driving the demand for advanced telematics services and localized content.

- Latin America: This region is an emerging market for automotive embedded telematics, characterized by growing awareness of vehicle safety and security, especially concerning stolen vehicle recovery and fleet management. Economic development and improving telecommunications infrastructure are gradually paving the way for wider adoption, though price sensitivity remains a factor.

- Middle East and Africa (MEA): The MEA region is witnessing gradual adoption of telematics, driven by increasing sales of premium vehicles and the rising need for fleet management solutions in sectors like logistics and transportation. Investments in smart city initiatives and developing digital infrastructure in countries like UAE and Saudi Arabia are creating new opportunities, particularly for fleet tracking and asset management.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Automotive Embedded Telematic Market.- Robert Bosch GmbH

- Continental AG

- Denso Corporation

- Harman International (A Samsung Company)

- LG Electronics Inc.

- Mitsubishi Electric Corporation

- Panasonic Corporation

- Sierra Wireless, Inc.

- Telefonica S.A.

- TomTom N.V.

- Verizon Communications Inc.

- Visteon Corporation

- Vodafone Group Plc

- Aptiv PLC

- Geely Auto Group

- Hyundai Mobis Co., Ltd.

- Marelli Holdings Co., Ltd.

- Qualcomm Incorporated

- STMicroelectronics N.V.

- NXP Semiconductors N.V.

Frequently Asked Questions

What is automotive embedded telematics?

Automotive embedded telematics refers to the integrated systems within a vehicle that use telecommunications and informatics to provide functionalities such as navigation, safety, entertainment, and remote diagnostics. These systems typically comprise hardware, software, and services that enable communication between the vehicle and external networks, allowing for data exchange and the delivery of connected services.

How is AI impacting the automotive embedded telematics market?

AI is significantly impacting the market by enabling advanced analytics for predictive maintenance, enhancing ADAS capabilities with superior object recognition, personalizing in-car experiences based on user behavior, and optimizing route planning. It is crucial for developing autonomous driving functions and improving vehicle cybersecurity by detecting real-time threats.

What are the primary drivers of growth in this market?

Key growth drivers include increasing government regulations mandating emergency call systems (e.g., eCall), rising consumer demand for connected car services and advanced infotainment, the accelerating adoption of electric vehicles (EVs), and advancements in communication technologies like 5G and IoT integration in vehicles.

What are the main challenges facing the automotive embedded telematics market?

Major challenges include cybersecurity threats and data privacy concerns, the high initial cost of implementing and integrating telematics systems, a lack of standardization and interoperability issues between different systems, and the need to continuously manage and analyze vast amounts of vehicle data.

Which regions are leading in automotive embedded telematics adoption?

North America and Europe are currently leading regions due to strong regulatory support and high consumer demand for advanced features. The Asia Pacific region, particularly China, is expected to be the fastest-growing market, driven by rapid automotive production and technological adoption.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted