Automotive Air Suspension System Market

Automotive Air Suspension System Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703844 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

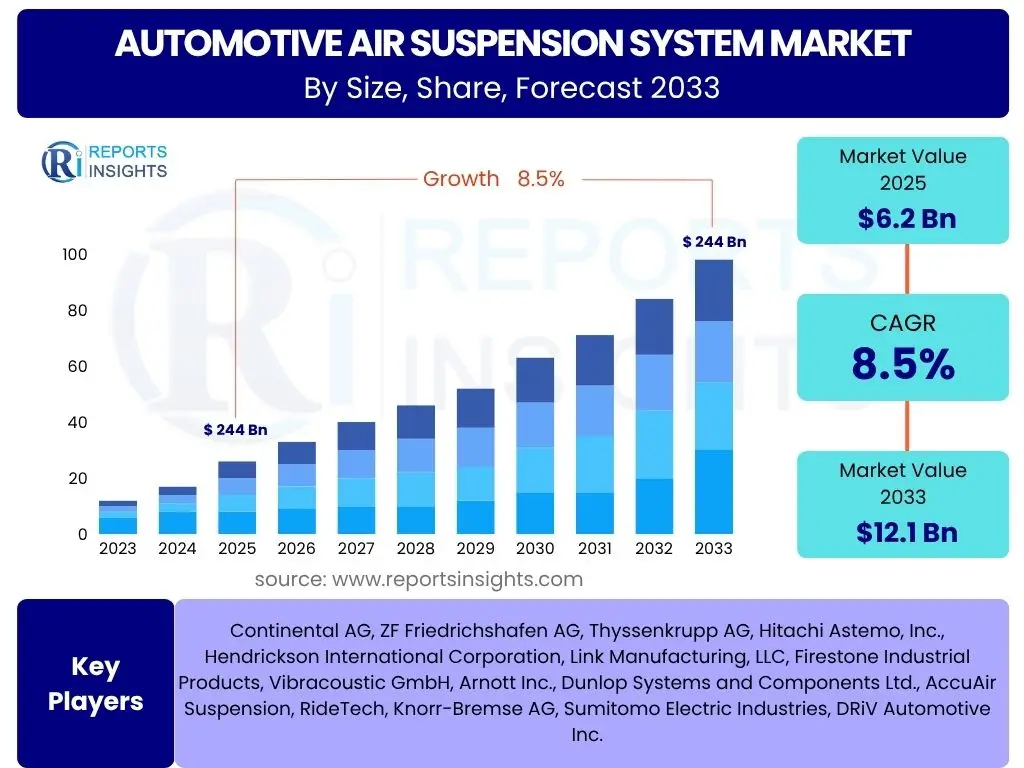

Automotive Air Suspension System Market Size

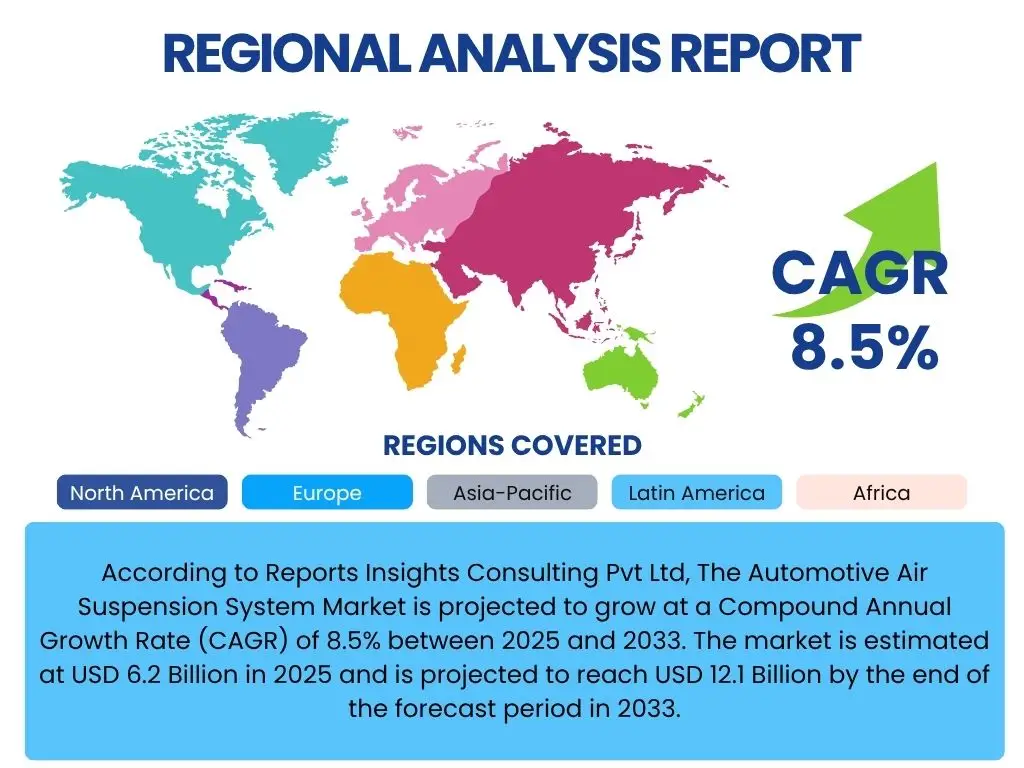

According to Reports Insights Consulting Pvt Ltd, The Automotive Air Suspension System Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2025 and 2033. The market is estimated at USD 6.2 Billion in 2025 and is projected to reach USD 12.1 Billion by the end of the forecast period in 2033.

Key Automotive Air Suspension System Market Trends & Insights

User queries regarding market trends in the automotive air suspension system sector frequently center on technological advancements, the influence of vehicle electrification, and evolving consumer preferences for superior ride comfort and handling. Common questions explore how innovative materials are enhancing durability, the integration of advanced electronics for real-time adaptability, and the expansion of these systems beyond luxury vehicles into broader segments. There is also significant interest in the adoption rate of these systems in emerging economies and the impact of stringent safety and emissions regulations on their design and functionality.

Analysis reveals a robust trend towards integrated and intelligent suspension systems that can adapt to varying road conditions and driving styles, significantly enhancing both safety and passenger experience. The increasing market penetration of electric vehicles (EVs) is a critical driver, as air suspension systems can compensate for the added weight of battery packs and optimize aerodynamic performance to extend range. Furthermore, rising disposable incomes in developing regions are fueling demand for premium vehicle features, including advanced suspension technologies. This combination of technological push and market pull indicates a dynamic and evolving landscape for automotive air suspension.

- Integration of advanced electronics for real-time adaptability and enhanced ride comfort.

- Increasing adoption in electric vehicles (EVs) to manage battery weight and optimize aerodynamics.

- Expansion of air suspension systems beyond luxury and premium segments into mid-range and commercial vehicles.

- Development of lightweight materials and compact designs for improved efficiency and packaging.

- Growing focus on predictive maintenance and diagnostic capabilities to reduce downtime and costs.

AI Impact Analysis on Automotive Air Suspension System

Common user questions related to the impact of AI on the Automotive Air Suspension System primarily revolve around how artificial intelligence can enhance system performance, enable predictive maintenance, and facilitate seamless integration with advanced driver-assistance systems (ADAS) and autonomous driving functionalities. Users are keen to understand if AI can make these systems more responsive, proactive, and efficient, potentially leading to unprecedented levels of ride comfort, vehicle stability, and safety. There is also curiosity about AI's role in optimizing manufacturing processes and supply chain management for air suspension components.

Based on this analysis, AI is poised to revolutionize automotive air suspension systems by enabling sophisticated adaptive capabilities. AI algorithms can process vast amounts of data from sensors in real-time, including road conditions, vehicle speed, steering angle, and passenger load, to dynamically adjust suspension parameters for optimal performance. This predictive capability allows the system to anticipate changes, such as upcoming bumps or turns, and prepare the suspension accordingly, delivering a consistently smooth and controlled ride. Moreover, AI-driven diagnostics can monitor component health, predict potential failures before they occur, and schedule maintenance proactively, thereby minimizing vehicle downtime and extending the lifespan of the suspension system.

Furthermore, AI facilitates the integration of air suspension with other vehicle systems. For instance, in autonomous vehicles, AI can coordinate suspension adjustments with navigation data and ADAS inputs to ensure maximum stability and comfort during automated driving maneuvers. This intelligent integration can contribute significantly to the overall perception of safety and reliability in advanced vehicles. In manufacturing, AI can optimize production lines, improve quality control, and enhance supply chain efficiency, leading to cost reductions and faster innovation cycles for air suspension technologies.

- Enhanced real-time adaptability: AI algorithms process sensor data to dynamically adjust suspension settings for optimal ride comfort and handling.

- Predictive maintenance: AI analyzes system performance data to anticipate component failures, enabling proactive servicing and reducing downtime.

- Integration with ADAS and autonomous driving: AI coordinates suspension responses with navigation, braking, and steering systems for improved stability and safety.

- Optimized energy efficiency: AI can manage compressor usage and air reservoir pressure to minimize energy consumption.

- Personalized ride profiles: AI learns driver preferences and passenger loads to automatically adjust suspension characteristics for a tailored experience.

Key Takeaways Automotive Air Suspension System Market Size & Forecast

User inquiries about key takeaways from the Automotive Air Suspension System market size and forecast consistently highlight questions about the primary growth catalysts, the segments poised for the most significant expansion, and the long-term strategic implications for manufacturers and suppliers. Users are keen to understand what fundamental factors underpin the projected growth, whether it is driven more by technological advancements or by shifting consumer demands, and how competitive dynamics are expected to evolve within this expanding market. There is a strong interest in identifying the most lucrative opportunities and potential challenges over the forecast period.

The core insight from the market forecast is the substantial and sustained growth projected for automotive air suspension systems, driven primarily by an increasing consumer demand for premium comfort, enhanced safety features, and the rapid electrification of the automotive industry. This growth is not merely an incremental increase but reflects a fundamental shift in vehicle design and consumer expectations, moving air suspension from a niche luxury feature to a more widely adopted technology. The market is also benefiting from continuous technological advancements that improve system efficiency, reliability, and cost-effectiveness, making it more appealing for broader vehicle segments. This trajectory indicates a robust market with numerous opportunities for innovation and market penetration.

- Significant market expansion: The market is projected to nearly double in size by 2033, indicating robust growth potential.

- Electrification as a key driver: The surge in EV production necessitates advanced suspension for weight management and range optimization.

- Premiumization trend: Growing consumer preference for superior ride comfort and vehicle dynamics boosts demand across vehicle segments.

- Technological innovation focus: Ongoing R&D in smart, adaptive, and lightweight systems will be critical for competitive advantage.

- Strategic opportunities in aftermarket: Post-sales service and replacement parts represent a substantial and growing revenue stream.

Automotive Air Suspension System Market Drivers Analysis

The automotive air suspension system market is significantly propelled by several key factors that converge to increase its adoption across various vehicle types. A primary driver is the rising consumer demand for superior ride comfort, enhanced vehicle handling, and improved safety features, particularly in premium and luxury vehicle segments. As consumer expectations for a smooth and controlled driving experience elevate, manufacturers are increasingly integrating air suspension systems to differentiate their offerings and meet these demands. These systems provide exceptional vibration damping and ride leveling, which are highly valued by occupants.

Furthermore, the global shift towards electric vehicles (EVs) presents a substantial growth opportunity for air suspension systems. EVs often carry heavy battery packs, which can impact vehicle dynamics and ride quality. Air suspension systems effectively compensate for this added weight, maintaining optimal vehicle height and balance, thereby enhancing stability, efficiency, and comfort. The increasing focus on vehicle performance and fuel efficiency also contributes to the market's growth, as air suspension can optimize aerodynamics by adjusting ride height, leading to better fuel economy or extended EV range. Regulatory pressures for improved vehicle safety and stability, particularly for commercial vehicles, further incentivize the adoption of these advanced suspension technologies.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing demand for luxury and premium vehicles | +0.8% | North America, Europe, Asia Pacific (China, India) | Short to Mid-term (2025-2030) |

| Increasing adoption of Electric Vehicles (EVs) | +1.2% | Global, particularly China, Europe, North America | Mid to Long-term (2027-2033) |

| Advancements in suspension technology and smart systems | +0.7% | Global, especially developed markets | Short to Mid-term (2025-2030) |

| Focus on enhanced vehicle safety and stability | +0.5% | Europe, North America, emerging Asian markets | Short to Mid-term (2025-2030) |

Automotive Air Suspension System Market Restraints Analysis

Despite the optimistic growth trajectory, the automotive air suspension system market faces several significant restraints that could impede its expansion. One of the primary limiting factors is the relatively high manufacturing cost associated with these systems compared to conventional coil spring or leaf spring suspensions. The complexity of the components, including air springs, compressors, reservoirs, electronic control units (ECUs), and various sensors, contributes to higher production expenses. This elevated cost often translates to a higher price point for the end consumer, making air suspension a less viable option for budget-conscious vehicle segments and acting as a barrier to mass market adoption.

Another considerable restraint is the perceived complexity and maintenance requirements of air suspension systems. While modern designs have improved reliability, historical perceptions of higher failure rates or more intricate repair procedures compared to passive systems persist among some consumers and mechanics. The specialized tools and diagnostic equipment often required for servicing can deter independent repair shops, pushing consumers towards more expensive authorized service centers. Furthermore, fluctuations in raw material prices, such as rubber, plastics, and various metals used in component manufacturing, can impact production costs and overall market stability, presenting a challenge for manufacturers in maintaining competitive pricing.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High manufacturing and installation costs | -1.0% | Global, particularly price-sensitive markets | Short to Mid-term (2025-2030) |

| Perceived complexity and maintenance challenges | -0.7% | Global, especially for older models | Short to Mid-term (2025-2030) |

| Volatility in raw material prices | -0.5% | Global, impacting supply chains worldwide | Short-term (2025-2027) |

| Aftermarket component availability and cost | -0.4% | Emerging markets, cost-conscious regions | Mid-term (2027-2030) |

Automotive Air Suspension System Market Opportunities Analysis

The automotive air suspension system market is characterized by several promising opportunities that are poised to accelerate its growth and innovation. One significant opportunity lies in the burgeoning aftermarket segment. As the installed base of vehicles with air suspension systems grows, so does the demand for replacement parts, repair services, and performance upgrades. This offers a lucrative avenue for both original equipment manufacturers (OEMs) and independent aftermarket suppliers to capitalize on the increasing need for maintenance and customization, providing a steady revenue stream beyond initial vehicle sales. The expansion of vehicle lifecycles and a focus on cost-effective repairs further fuel this segment.

Another substantial opportunity is the expanding application of air suspension systems into new vehicle categories, particularly light commercial vehicles (LCVs), heavy-duty trucks, and buses. These vehicles can significantly benefit from the load-leveling capabilities, improved stability, and enhanced comfort that air suspension offers, especially for transporting sensitive cargo or a high volume of passengers. As regulations tighten regarding driver comfort and vehicle safety, the adoption of air suspension in these segments is expected to surge. Furthermore, the development of smart, adaptive, and fully active air suspension systems, often integrated with advanced sensor technology and AI, presents a strong innovation opportunity to create more sophisticated and responsive products, driving premiumization and technological leadership within the market.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion in aftermarket sales and services | +0.9% | Global, particularly North America, Europe | Mid to Long-term (2027-2033) |

| Increased adoption in commercial vehicles (LCVs, trucks, buses) | +1.1% | Asia Pacific (China, India), Europe, North America | Mid to Long-term (2027-2033) |

| Technological advancements in smart and adaptive systems | +0.8% | Developed markets (Europe, North America, Japan) | Short to Mid-term (2025-2030) |

| Emerging markets demand for enhanced comfort and luxury | +0.6% | Asia Pacific, Latin America, Middle East & Africa | Mid-term (2027-2030) |

Automotive Air Suspension System Market Challenges Impact Analysis

The automotive air suspension system market, while promising, is not without its challenges that could impact its growth trajectory. Intense competition among existing players and the potential entry of new component manufacturers pose a significant challenge, leading to pricing pressures and reduced profit margins. Companies must continuously innovate and differentiate their products to maintain market share, which often requires substantial investments in research and development. This competitive landscape demands agile business strategies and a strong focus on cost optimization without compromising quality or performance.

Another critical challenge involves the stringent regulatory standards and diverse regional requirements concerning vehicle safety, emissions, and component durability. Compliance with these evolving regulations necessitates continuous product adaptation and extensive testing, adding to development costs and time-to-market. Supply chain disruptions, often exacerbated by geopolitical tensions or global events, present a formidable challenge, impacting the availability of critical components and raw materials, leading to production delays and increased operational costs. Moreover, the need for skilled labor, both in manufacturing and particularly in the specialized installation and maintenance of these complex systems, represents a growing concern, especially in regions with developing automotive infrastructure. Addressing these challenges requires strategic planning, robust supply chain management, and investment in workforce training.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense market competition and pricing pressures | -0.9% | Global | Short to Mid-term (2025-2030) |

| Stringent regulatory and compliance standards | -0.6% | Europe, North America, China | Mid-term (2027-2030) |

| Supply chain vulnerabilities and raw material fluctuations | -0.8% | Global | Short-term (2025-2027) |

| Need for specialized manufacturing and maintenance expertise | -0.5% | Emerging markets, regions with limited technical infrastructure | Mid to Long-term (2027-2033) |

Automotive Air Suspension System Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global Automotive Air Suspension System market, encompassing historical data from 2019 to 2023, current market estimations for 2024, and detailed projections through 2033. The report offers critical insights into market size, growth drivers, restraints, opportunities, and challenges, leveraging extensive primary and secondary research. It includes a thorough segmentation analysis by vehicle type, component, technology, and sales channel, alongside a detailed regional outlook. The study also profiles key market players, providing a competitive landscape assessment and strategic recommendations for stakeholders navigating this evolving sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 6.2 Billion |

| Market Forecast in 2033 | USD 12.1 Billion |

| Growth Rate | 8.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Continental AG, ZF Friedrichshafen AG, Thyssenkrupp AG, Hitachi Astemo, Inc., Hendrickson International Corporation, Link Manufacturing, LLC, Firestone Industrial Products, Vibracoustic GmbH, Arnott Inc., Dunlop Systems and Components Ltd., AccuAir Suspension, RideTech, Knorr-Bremse AG, Sumitomo Electric Industries, DRiV Automotive Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Automotive Air Suspension System market is broadly segmented to provide a granular view of its dynamics and growth prospects across various dimensions. This segmentation helps in understanding the specific drivers, opportunities, and challenges pertinent to each category, allowing stakeholders to develop targeted strategies. The market is primarily categorized based on vehicle type, reflecting the varying adoption rates and system requirements across different automotive applications. Further segmentation by component highlights the critical parts that constitute the air suspension system, offering insights into their individual market contributions and technological advancements. Technology-based segmentation differentiates between various levels of system sophistication, from passive to fully active solutions, while the sales channel segmentation distinguishes between OEM installations and the expanding aftermarket.

Each segment holds unique growth potential. For instance, the Passenger Cars segment remains the largest due to increasing demand for luxury and comfort features, while the Commercial Vehicles segment, including light and heavy-duty trucks and buses, is anticipated to witness significant growth driven by regulatory compliance for driver comfort and efficient load management. Component-wise, air springs and compressors are fundamental, seeing continuous innovation in materials and efficiency. The shift towards electronically controlled and fully active systems signifies the market's technological progression, aiming for enhanced adaptability and performance. The robust growth in the aftermarket reflects the long-term service needs and opportunities for component replacement and upgrades, forming a crucial part of the overall market ecosystem.

- By Vehicle Type: Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles, Buses, Other Commercial Vehicles

- By Component: Air Springs, Air Compressors, Air Reservoir, Electronic Control Unit (ECU), Sensors, Solenoid Valves, Air Lines and Fittings

- By Technology: Electronically Controlled Air Suspension (ECAS), Semi-Active Air Suspension, Fully Active Air Suspension, Passive Air Suspension

- By Sales Channel: Original Equipment Manufacturers (OEM), Aftermarket

Regional Highlights

- North America: This region is a significant market for automotive air suspension systems, driven by the presence of a strong luxury and premium vehicle segment, high consumer disposable income, and increasing adoption of advanced automotive technologies. The growing demand for SUVs and light trucks, often equipped with air suspension for enhanced ride comfort and towing capabilities, further contributes to market growth. Stringent safety regulations and a robust aftermarket presence also support market expansion.

- Europe: Europe represents a mature and technologically advanced market, characterized by stringent emission norms and a strong emphasis on vehicle performance, safety, and comfort. Germany, in particular, leads in the adoption of air suspension systems due to its prominent luxury automotive manufacturing base and high consumer preference for sophisticated vehicle features. The region is also at the forefront of EV adoption, which directly boosts the demand for air suspension.

- Asia Pacific (APAC): The APAC region is projected to be the fastest-growing market, primarily due to the rapid expansion of the automotive industry in countries like China, India, Japan, and South Korea. Rising disposable incomes, increasing urbanization, and a growing middle class are fueling the demand for premium and luxury vehicles. Furthermore, the burgeoning commercial vehicle sector in these economies, coupled with government initiatives for modernizing public transport fleets, is driving the adoption of air suspension for improved load capacity and passenger comfort.

- Latin America: This region presents emerging opportunities for the automotive air suspension market. While smaller in comparison to North America or Europe, countries like Brazil and Mexico are experiencing growth in their automotive manufacturing sectors and increasing consumer preference for more comfortable and safer vehicles. The commercial vehicle segment, especially for public transport and logistics, is also beginning to integrate more advanced suspension systems.

- Middle East and Africa (MEA): The MEA region is witnessing steady growth, primarily influenced by investments in luxury automotive infrastructure in the Middle East and the expanding commercial vehicle sector in parts of Africa. The demand for robust suspension systems capable of handling diverse terrains and heavy loads is a key factor, particularly in the utility and commercial vehicle segments. Economic diversification and infrastructure development are expected to foster continued market evolution.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Automotive Air Suspension System Market.- Continental AG

- ZF Friedrichshafen AG

- Thyssenkrupp AG

- Hitachi Astemo, Inc.

- Hendrickson International Corporation

- Link Manufacturing, LLC

- Firestone Industrial Products

- Vibracoustic GmbH

- Arnott Inc.

- Dunlop Systems and Components Ltd.

- AccuAir Suspension

- RideTech

- Knorr-Bremse AG

- Sumitomo Electric Industries

- DRiV Automotive Inc.

- Trelleborg AB

- BWI Group

- Anssen Suspension

- Suncore Industries

- Goodyear Tire & Rubber Company (for air springs)

Frequently Asked Questions

What is an Automotive Air Suspension System?

An automotive air suspension system replaces traditional steel springs with air springs, which are essentially durable rubber bladders inflated by an electric air compressor. This system allows for dynamic adjustment of the vehicle's ride height and damping characteristics, providing superior ride comfort, enhanced vehicle stability, and variable load leveling capabilities compared to conventional suspension setups.

How does an Automotive Air Suspension System work?

The system comprises air springs, an air compressor, an air reservoir, an electronic control unit (ECU), and various sensors. The compressor inflates the air springs to raise the vehicle or maintain desired ride height, while the ECU processes data from level and pressure sensors to continuously adjust air pressure in the springs. This allows the system to adapt to road conditions, vehicle speed, and load variations, optimizing performance and comfort.

What are the key benefits of Automotive Air Suspension Systems?

Key benefits include significantly improved ride comfort by absorbing road imperfections more effectively, enhanced handling and stability through active ride height and damping control, automatic load leveling for consistent performance regardless of cargo or passenger weight, and the ability to adjust ride height for better aerodynamics at high speeds or increased ground clearance on rough terrain. They also reduce noise, vibration, and harshness (NVH).

Which types of vehicles commonly use Automotive Air Suspension Systems?

Automotive air suspension systems are primarily found in luxury and premium passenger cars, high-end SUVs, and increasingly in electric vehicles (EVs) to manage battery weight. They are also widely adopted in commercial vehicles such as heavy-duty trucks, buses, and trailers, where load leveling, stability, and driver comfort are crucial. Their application is expanding into more mainstream vehicle segments due to technological advancements and decreasing costs.

What is the future outlook for the Automotive Air Suspension System Market?

The market's future outlook is highly positive, driven by the global surge in electric vehicle adoption, increasing consumer demand for advanced comfort and safety features, and continuous innovation in smart and adaptive suspension technologies. Integration with AI and ADAS, expansion into new vehicle segments (e.g., last-mile delivery vans), and robust growth in the aftermarket segment are expected to fuel sustained expansion through 2033.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted