Atomic Layer Deposition Equipment Market

Atomic Layer Deposition Equipment Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701110 | Last Updated : July 29, 2025 |

Format : ![]()

![]()

![]()

![]()

Atomic Layer Deposition Equipment Market Size

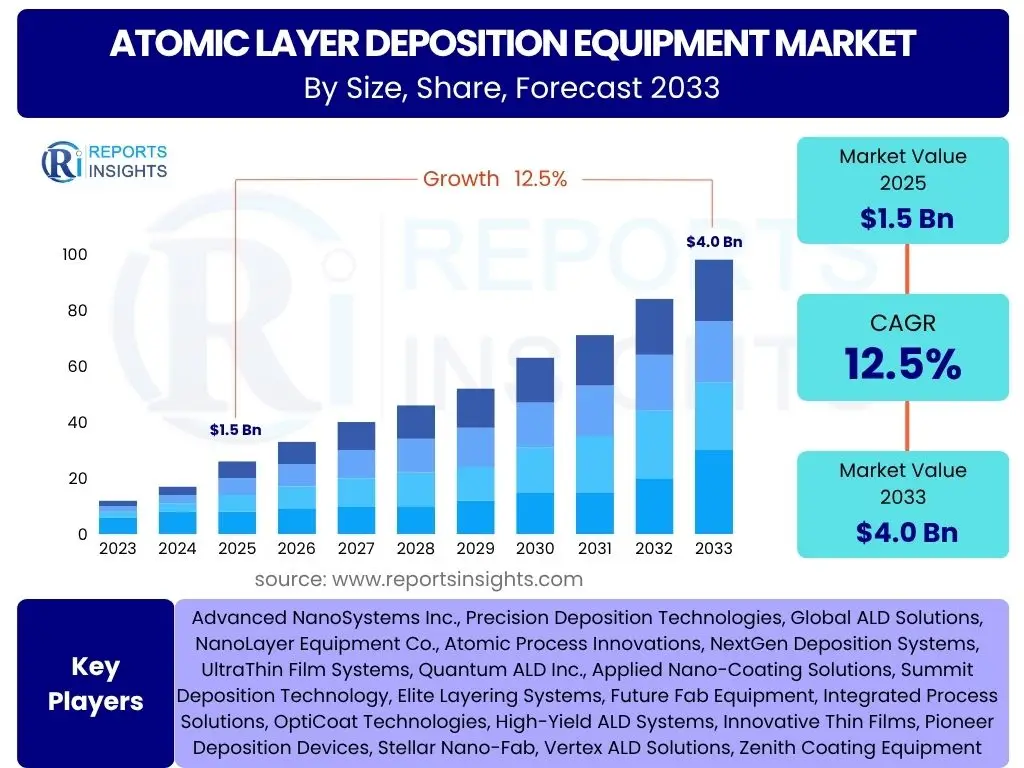

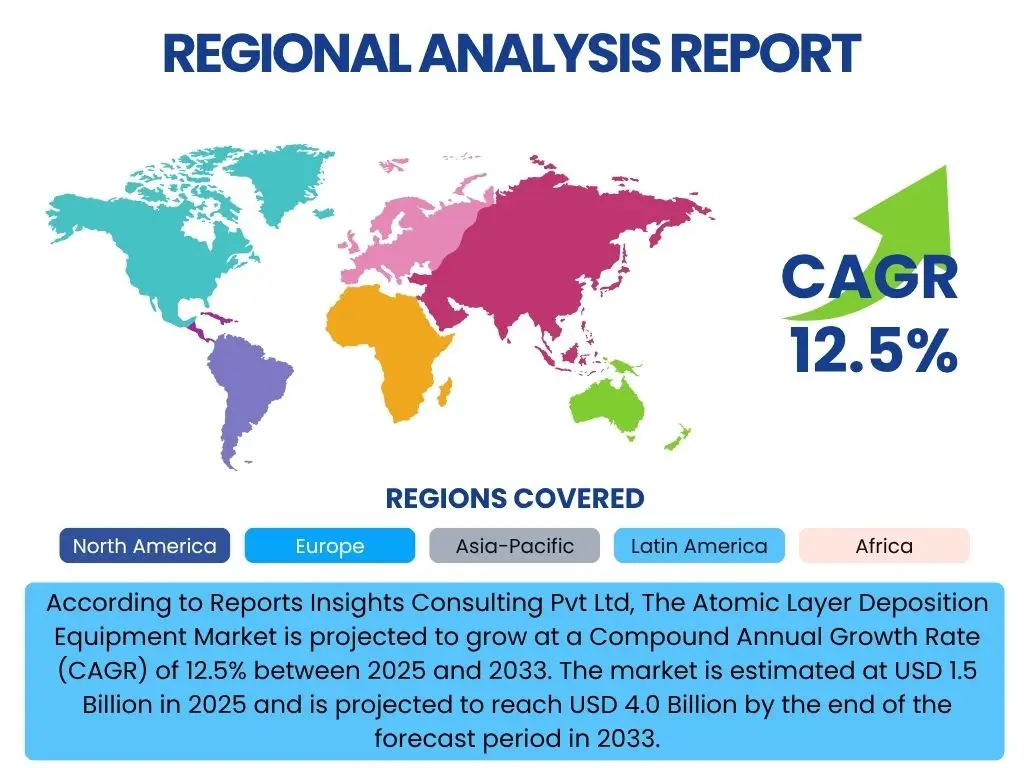

According to Reports Insights Consulting Pvt Ltd, The Atomic Layer Deposition Equipment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.5% between 2025 and 2033. The market is estimated at USD 1.5 Billion in 2025 and is projected to reach USD 4.0 Billion by the end of the forecast period in 2033.

Key Atomic Layer Deposition Equipment Market Trends & Insights

User inquiries frequently highlight the rapid advancements and increasing adoption of Atomic Layer Deposition (ALD) technology across diverse industries. A primary trend observed is the relentless miniaturization in semiconductor manufacturing, driving the demand for ultra-thin, highly conformal films with precise control over thickness and composition, which ALD excels at providing. The advent of advanced packaging technologies and 3D device architectures, such as 3D NAND and FinFETs, further amplifies this need, pushing equipment manufacturers to innovate for higher throughput and larger wafer sizes while maintaining atomic-level precision.

Another significant trend is the expansion of ALD applications beyond traditional semiconductors. There is growing interest and investment in leveraging ALD for flexible electronics, transparent conductors, advanced optics, energy storage devices like solid-state batteries, and even biomedical coatings. This diversification is fueled by ALD's unique ability to deposit functional materials with tailored properties at low temperatures, making it suitable for thermally sensitive substrates and complex geometries. Furthermore, the development of novel precursors and advanced process controls, including plasma-enhanced ALD (PEALD) and spatial ALD, are key technological trends enhancing deposition rates, film quality, and material versatility, thereby addressing throughput limitations and opening up new industrial avenues for ALD equipment.

- Miniaturization and 3D architecture in semiconductors driving demand.

- Diversification of ALD applications into flexible electronics, energy, and biomedical fields.

- Advancements in PEALD and spatial ALD for improved throughput and material versatility.

- Development of novel ALD precursors for enhanced film properties and broader material palette.

- Increasing integration of ALD in high-volume manufacturing lines.

AI Impact Analysis on Atomic Layer Deposition Equipment

Common user questions regarding AI's impact on Atomic Layer Deposition Equipment revolve around how artificial intelligence and machine learning can enhance process efficiency, predictive maintenance, and overall material science innovation. Users are keen to understand if AI can optimize complex ALD recipes, reduce experimental iterations, and improve film quality consistency. The core expectation is that AI algorithms can analyze vast datasets generated during ALD processes – including precursor flow rates, temperature profiles, pressure, and resulting film characteristics – to identify optimal parameters that human operators might overlook, thereby accelerating research and development cycles and improving manufacturing yields.

Furthermore, there is a strong interest in AI's role in predictive maintenance for ALD equipment. Given the high cost and sensitivity of these machines, unexpected downtime can be extremely detrimental. AI-powered diagnostic tools can monitor equipment performance in real-time, detect subtle anomalies, and predict potential failures before they occur, enabling proactive maintenance and minimizing operational disruptions. This extends to supply chain optimization for precursors and consumables, where AI can forecast demand and manage inventory more efficiently. While the integration of AI is still nascent in some areas of ALD, its potential for automating complex process tuning, enhancing quality control through in-situ monitoring, and driving a more data-driven approach to materials engineering is a significant area of focus for equipment manufacturers and end-users alike.

- AI-driven optimization of ALD process parameters for enhanced film quality and efficiency.

- Predictive maintenance and anomaly detection in ALD equipment to minimize downtime.

- Accelerated material discovery and recipe development through machine learning algorithms.

- Enhanced quality control and real-time process monitoring using AI-powered analytics.

- Automation of complex ALD operations, reducing human intervention and error.

Key Takeaways Atomic Layer Deposition Equipment Market Size & Forecast

User inquiries frequently focus on understanding the core drivers behind the projected growth of the Atomic Layer Deposition Equipment market and what critical factors will shape its trajectory over the forecast period. A primary takeaway is the undeniable link between the expansion of the semiconductor industry, particularly in advanced nodes and novel device architectures, and the escalating demand for ALD solutions. The relentless pursuit of higher performance, greater energy efficiency, and increased integration in electronic devices necessitates deposition techniques that offer atomic-scale precision, which ALD uniquely provides. This foundational demand ensures a robust growth outlook for the ALD equipment sector.

Beyond semiconductors, a significant insight is the increasing diversification of ALD applications into emerging fields, which acts as a crucial secondary growth engine. As industries like flexible electronics, advanced displays, renewable energy (e.g., solar cells, solid-state batteries), and biomedical devices seek to integrate high-performance functional films, ALD’s capabilities become indispensable. The market's growth is therefore not solely reliant on one sector but is propelled by a broader adoption across multiple high-growth technology areas. This diversification, coupled with continuous innovation in ALD precursor chemistry, equipment design for enhanced throughput, and the integration of smart manufacturing principles, positions the Atomic Layer Deposition Equipment market for sustained and substantial expansion throughout the forecast period.

- Strong growth driven by advanced semiconductor manufacturing, particularly 3D structures.

- Significant expansion into new application areas beyond traditional electronics.

- Continuous technological advancements in ALD processes and precursors enhancing market potential.

- Increasing R&D investments by governments and private entities supporting ALD innovation.

- Market resilience due to indispensable role in producing high-performance, ultra-thin films.

Atomic Layer Deposition Equipment Market Drivers Analysis

The Atomic Layer Deposition Equipment market is fundamentally driven by the escalating demand for advanced materials and high-performance electronic devices, where atomic-scale precision in film deposition is paramount. The semiconductor industry remains the primary catalyst, with the continuous pursuit of miniaturization, higher integration densities, and the development of complex 3D architectures like FinFETs, 3D NAND, and advanced packaging solutions. These technological shifts necessitate ultra-thin, highly conformal films with superior electrical and mechanical properties, areas where ALD technology excels. Beyond semiconductors, the expanding applications of ALD in diverse sectors such as advanced displays, solar cells, medical devices, and energy storage further fuel market growth by opening new avenues for specialized equipment.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing demand for advanced semiconductors (3D ICs, FinFETs) | +3.5% | Asia Pacific (South Korea, Taiwan, China), North America | Short to Mid-term (2025-2029) |

| Increasing adoption in emerging applications (flexible electronics, MEMS) | +2.8% | Asia Pacific, Europe, North America | Mid to Long-term (2027-2033) |

| Rising investments in R&D for advanced materials | +2.0% | Global, particularly North America, Europe, Asia Pacific | Short to Mid-term (2025-2030) |

| Technological advancements in ALD processes and precursors | +1.7% | Global | Continuous |

Atomic Layer Deposition Equipment Market Restraints Analysis

Despite its significant advantages, the Atomic Layer Deposition Equipment market faces several restraints that could impede its growth trajectory. One primary concern is the high capital investment required for ALD equipment. The sophisticated nature of the technology, coupled with the need for precise control systems and specialized vacuum components, translates into substantial upfront costs for manufacturers and research institutions. This high entry barrier can limit adoption, particularly for smaller enterprises or those with limited capital. Additionally, the relatively lower throughput of certain ALD processes compared to traditional deposition techniques, especially for large-scale production, remains a challenge that can deter its widespread use in high-volume applications where speed is critical. While advancements are being made to address this, it continues to be a point of consideration for potential adopters.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High capital cost of ALD equipment | -1.2% | Global, particularly emerging economies | Short to Mid-term (2025-2030) |

| Relatively low throughput for certain applications | -0.9% | Global | Mid-term (2026-2031) |

| Complex process optimization and maintenance | -0.7% | Global | Short to Mid-term (2025-2029) |

Atomic Layer Deposition Equipment Market Opportunities Analysis

The Atomic Layer Deposition Equipment market is poised for significant opportunities driven by technological innovation and the expansion into novel application areas. The continuous development of new ALD precursors and chemistries represents a major opportunity, enabling the deposition of a wider array of materials with tailored properties for specific industry needs. This includes the exploration of 2D materials, complex oxides, and nitrides for next-generation devices. Furthermore, the rising demand for flexible and wearable electronics presents a unique growth avenue, as ALD's low-temperature processing capabilities are ideally suited for delicate, flexible substrates. The increasing focus on sustainability also creates opportunities for ALD, as it offers precise material utilization and reduced waste compared to some alternative deposition methods, aligning with green manufacturing initiatives and opening doors for environmentally conscious applications.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of new ALD precursors and chemistries | +1.5% | Global, R&D focused regions | Mid to Long-term (2027-2033) |

| Expansion into flexible and wearable electronics | +1.3% | Asia Pacific, North America, Europe | Mid to Long-term (2028-2033) |

| Demand for ALD in energy storage and renewable energy sectors | +1.0% | Global | Long-term (2029-2033) |

Atomic Layer Deposition Equipment Market Challenges Impact Analysis

The Atomic Layer Deposition Equipment market faces several formidable challenges that can influence its growth trajectory. One significant challenge is the inherent technical complexity involved in ALD processes, particularly in achieving uniform deposition over large substrate areas and intricate 3D structures. Maintaining precise control over reaction parameters, precursor delivery, and chamber conditions across varied industrial scales demands highly sophisticated engineering and stringent quality control, which can be difficult to scale efficiently. Another challenge is the competition from established alternative deposition techniques like Chemical Vapor Deposition (CVD) and Physical Vapor Deposition (PVD), which, while lacking ALD's atomic-scale precision, often offer higher throughput and lower operational costs for certain applications. This necessitates continuous innovation from ALD equipment manufacturers to justify the higher investment and complexity, demonstrating clear performance advantages to secure market share. Furthermore, the skilled labor shortage required for operating and maintaining these advanced systems poses an ongoing challenge, impacting adoption rates and operational efficiency across various regions.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Technical complexity in process scaling and uniformity | -0.8% | Global | Short to Mid-term (2025-2029) |

| Competition from alternative deposition technologies | -0.6% | Global | Short to Mid-term (2025-2030) |

| High operational costs and specific precursor requirements | -0.5% | Global | Short to Mid-term (2025-2028) |

Atomic Layer Deposition Equipment Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the Atomic Layer Deposition Equipment market, offering a detailed segmentation, regional insights, competitive landscape, and future growth projections. It covers market dynamics, including key drivers, restraints, opportunities, and challenges, providing a holistic view of the industry from 2019 to 2033. The report also integrates the impact of emerging technologies like AI and addresses frequently asked questions to offer a complete understanding for stakeholders.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.5 Billion |

| Market Forecast in 2033 | USD 4.0 Billion |

| Growth Rate | 12.5% CAGR |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Advanced NanoSystems Inc., Precision Deposition Technologies, Global ALD Solutions, NanoLayer Equipment Co., Atomic Process Innovations, NextGen Deposition Systems, UltraThin Film Systems, Quantum ALD Inc., Applied Nano-Coating Solutions, Summit Deposition Technology, Elite Layering Systems, Future Fab Equipment, Integrated Process Solutions, OptiCoat Technologies, High-Yield ALD Systems, Innovative Thin Films, Pioneer Deposition Devices, Stellar Nano-Fab, Vertex ALD Solutions, Zenith Coating Equipment |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Atomic Layer Deposition Equipment market is broadly segmented by type, application, and end-user, reflecting the diverse technological approaches and vast application spectrum of ALD. Understanding these segments is crucial for identifying specific growth opportunities and market dynamics. Each segment represents distinct technological requirements, material needs, and market demands, influencing the design and adoption of ALD equipment globally. The segmentation provides a granular view, allowing for targeted strategic planning and investment decisions within this highly specialized market.

- By Type: This segment categorizes equipment based on the energy source and processing method employed for atomic layer deposition.

- Thermal ALD Equipment: Utilizes heat to drive chemical reactions on the substrate surface.

- Plasma Enhanced ALD (PEALD) Equipment: Employs plasma to activate precursors, allowing for lower deposition temperatures and broader material compatibility.

- Spatial ALD Equipment: Features separated precursor flows, enabling higher throughput for certain applications.

- Other ALD Equipment: Includes niche or evolving ALD techniques like roll-to-roll ALD for flexible substrates.

- By Application: This segment defines the various industries and end-products where ALD technology is implemented.

- Semiconductor Industry: The largest application, covering logic, memory, and advanced packaging.

- Solar Energy: For enhancing efficiency and stability of photovoltaic cells.

- Displays: For barrier films, passivation layers, and transparent conductive films in advanced displays.

- Medical Devices: For biocompatible coatings and drug delivery systems.

- Energy Storage: For electrodes, electrolytes, and separators in batteries and fuel cells.

- Optics & Photonics: For anti-reflective coatings and optical filters.

- Other Applications: Includes catalysis, flexible electronics, corrosion protection, and protective coatings.

- By End-User: This segment identifies the primary entities that purchase and operate ALD equipment.

- Integrated Device Manufacturers (IDMs): Companies that design, manufacture, and sell their own integrated circuits.

- Foundries: Companies that specialize in the manufacturing of integrated circuits for other fabless companies.

- Research & Development Institutions: Universities, national labs, and corporate R&D centers.

- Original Equipment Manufacturers (OEMs): Manufacturers integrating ALD equipment into their own systems for specific applications.

Regional Highlights

- North America: This region is a significant market for Atomic Layer Deposition Equipment, driven by robust R&D activities in advanced materials, semiconductors, and nanotechnology. The presence of leading technology companies, prominent research institutions, and substantial government funding for innovation contributes to the adoption of advanced ALD solutions. Early adoption of cutting-edge technologies in areas like artificial intelligence, quantum computing, and biomedical devices also fuels demand for high-precision deposition techniques.

- Europe: Europe exhibits steady growth in the ALD equipment market, largely influenced by its strong automotive, industrial electronics, and research sectors. Countries like Germany, France, and the Netherlands are at the forefront of advanced manufacturing and materials science research, fostering the development and application of ALD technology. The region's emphasis on sustainable technologies and smart manufacturing also contributes to the demand for efficient and precise deposition solutions.

- Asia Pacific (APAC): APAC is projected to be the largest and fastest-growing market for Atomic Layer Deposition Equipment. This growth is predominantly driven by the region's dominance in semiconductor manufacturing, particularly in South Korea, Taiwan, China, and Japan, which host major foundries and IDMs. Rapid expansion in consumer electronics, advanced displays, and solar energy production also contributes significantly to the demand for ALD equipment. Government support and substantial investments in high-tech manufacturing further accelerate market expansion in this region.

- Latin America: While a nascent market compared to other regions, Latin America shows potential for growth, primarily through increasing foreign investments in manufacturing and a growing focus on technological advancements in countries like Brazil and Mexico. The adoption of ALD technology here is gradual, largely driven by expanding industrial applications and a push for localized production of electronic components.

- Middle East and Africa (MEA): The MEA region is an emerging market for ALD equipment, with growth prospects tied to diversification efforts away from oil-dependent economies. Investments in renewable energy projects, smart cities, and localized manufacturing capabilities, particularly in the UAE and Saudi Arabia, are expected to slowly drive the demand for advanced material deposition techniques. Research and academic collaborations also play a role in fostering ALD adoption in the long term.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Atomic Layer Deposition Equipment Market.- Advanced NanoSystems Inc.

- Precision Deposition Technologies

- Global ALD Solutions

- NanoLayer Equipment Co.

- Atomic Process Innovations

- NextGen Deposition Systems

- UltraThin Film Systems

- Quantum ALD Inc.

- Applied Nano-Coating Solutions

- Summit Deposition Technology

- Elite Layering Systems

- Future Fab Equipment

- Integrated Process Solutions

- OptiCoat Technologies

- High-Yield ALD Systems

- Innovative Thin Films

- Pioneer Deposition Devices

- Stellar Nano-Fab

- Vertex ALD Solutions

- Zenith Coating Equipment

Frequently Asked Questions

Analyze common user questions about the Atomic Layer Deposition Equipment market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is Atomic Layer Deposition (ALD) Equipment?

Atomic Layer Deposition (ALD) equipment refers to highly specialized tools used to deposit ultra-thin, highly conformal films onto substrates one atomic layer at a time. This precision is achieved through sequential, self-limiting gas-phase chemical reactions, making ALD ideal for creating films with exceptional uniformity and precise thickness control, critical for advanced semiconductor devices and other nanotechnology applications.

Why is ALD technology important in modern manufacturing?

ALD technology is crucial due to its ability to produce films with atomic-level precision, superior conformality, and excellent material properties, even on complex 3D structures. This enables the fabrication of smaller, more powerful, and energy-efficient electronic devices, alongside innovative applications in fields like medical devices, energy storage, and flexible electronics, where traditional deposition methods fall short.

What are the primary applications of Atomic Layer Deposition Equipment?

The primary applications of ALD equipment are in the semiconductor industry for manufacturing advanced logic and memory chips, gate dielectrics, and capacitor films. Beyond semiconductors, it is increasingly used in solar energy (passivation layers), displays (barrier films), medical devices (biocompatible coatings), and energy storage (battery electrodes and solid-state electrolytes).

What are the key drivers for the growth of the ALD Equipment market?

Key drivers include the relentless demand for miniaturization and 3D device architectures in the semiconductor industry, the expansion of ALD into new high-growth applications like flexible electronics and advanced displays, and continuous research and development investments in novel materials and ALD chemistries.

What challenges does the Atomic Layer Deposition Equipment market face?

Challenges for the ALD equipment market include the high capital cost of the machinery, relatively lower throughput compared to some conventional deposition methods, the technical complexities involved in process optimization and scaling for uniform deposition over large areas, and competition from other established thin-film deposition technologies.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted