Anisotropic Conductive Paste Market

Anisotropic Conductive Paste Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700589 | Last Updated : July 25, 2025 |

Format : ![]()

![]()

![]()

![]()

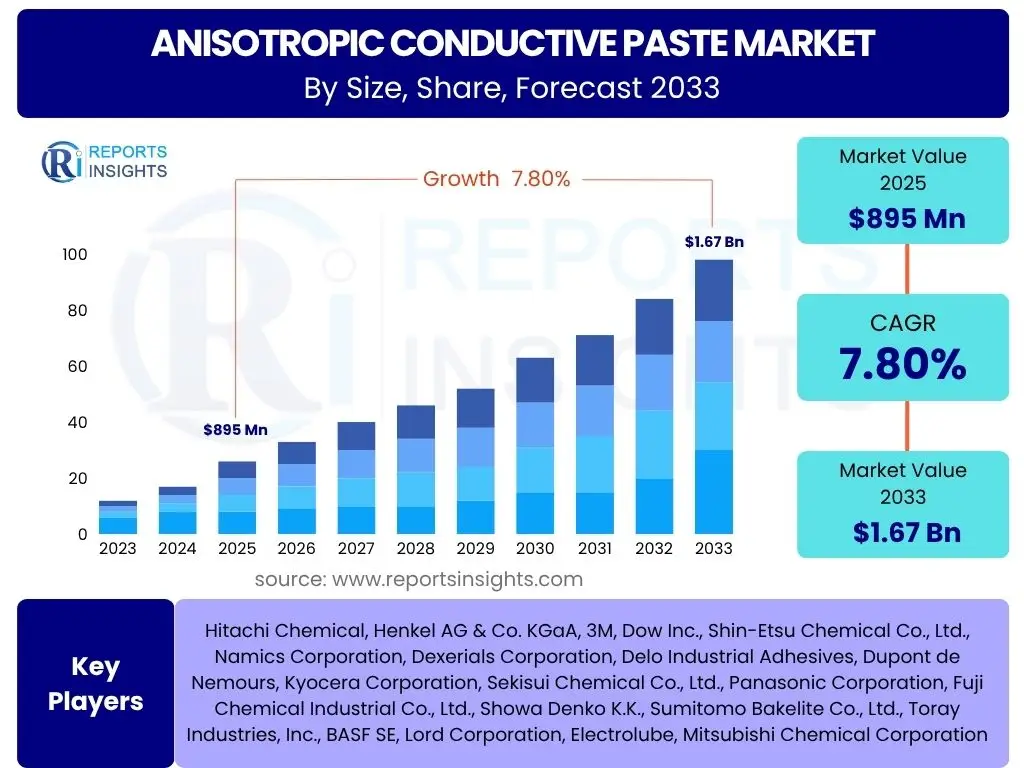

Anisotropic Conductive Paste Market Size

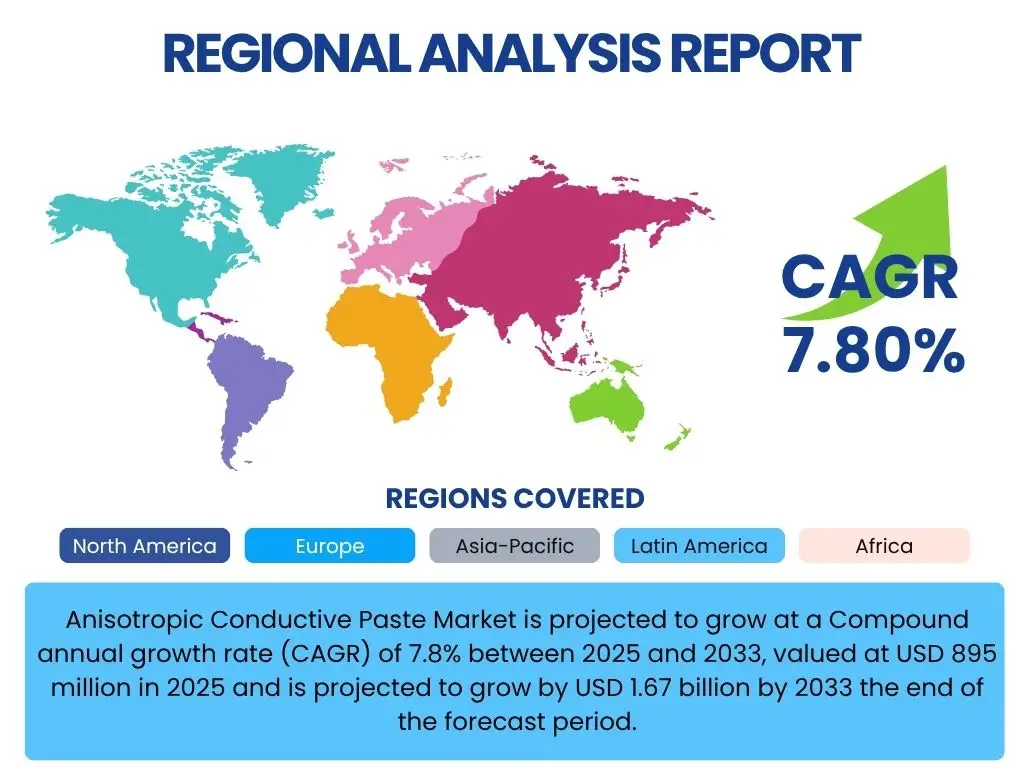

Anisotropic Conductive Paste Market is projected to grow at a Compound annual growth rate (CAGR) of 7.8% between 2025 and 2033, valued at USD 895 million in 2025 and is projected to grow by USD 1.67 billion by 2033 the end of the forecast period.

Key Anisotropic Conductive Paste Market Trends & Insights

The Anisotropic Conductive Paste (ACP) market is currently experiencing significant transformative trends driven by the rapid evolution of electronics and manufacturing technologies. Key insights highlight the increasing demand for miniaturization and high-density packaging, particularly in consumer electronics and advanced display technologies. Innovations in material science are leading to the development of more robust and reliable ACP formulations, capable of meeting stringent performance requirements for next-generation devices. The integration of ACP in flexible electronics and wearable technology is also a prominent trend, pushing the boundaries of traditional circuit interconnectivity. Furthermore, the automotive sector's shift towards electric vehicles and autonomous driving systems is creating new avenues for ACP applications, emphasizing durability and performance in harsh environments. The growing adoption of 5G infrastructure and IoT devices further fuels demand for efficient and compact interconnections, positioning ACP as a critical enabler for future technological advancements.

- Miniaturization and high-density packaging advancements.

- Growing adoption in flexible and wearable electronics.

- Increased demand from the automotive electronics sector (EVs, ADAS).

- Expansion of 5G and IoT device infrastructure.

- Development of advanced, more reliable ACP formulations.

- Shift towards lead-free and environmentally friendly materials.

- Rising demand for fine pitch interconnections in displays.

AI Impact Analysis on Anisotropic Conductive Paste

Artificial Intelligence (AI) is set to significantly influence the Anisotropic Conductive Paste (ACP) market across various stages, from research and development to manufacturing and quality control. AI's capabilities in data analysis and pattern recognition enable faster and more efficient material discovery, accelerating the development of novel ACP formulations with enhanced properties such as improved conductivity, adhesion, and reliability. In manufacturing, AI-driven predictive maintenance and process optimization can lead to higher production yields, reduced waste, and increased operational efficiency, thereby lowering manufacturing costs. Furthermore, AI-powered vision systems are revolutionizing quality inspection, allowing for precise detection of defects in ACP applications, ensuring higher product quality and reliability. The impact extends to supply chain management, where AI can optimize logistics and inventory, mitigating risks and ensuring a consistent supply of raw materials. This transformative influence positions AI as a crucial tool for innovation and efficiency within the ACP industry, driving future growth and competitiveness.

- Accelerated material discovery and formulation optimization through AI algorithms.

- Enhanced manufacturing efficiency via AI-driven process control and predictive analytics.

- Improved quality assurance and defect detection using AI-powered vision systems.

- Optimized supply chain management and inventory forecasting with AI.

- Reduced R&D cycles and time-to-market for new ACP products.

- Potential for personalized ACP solutions based on specific application requirements.

Key Takeaways Anisotropic Conductive Paste Market Size & Forecast

- The Anisotropic Conductive Paste (ACP) market is projected for robust growth, driven by pervasive electronics miniaturization.

- Significant CAGR of 7.8% anticipated between 2025 and 2033, reaching USD 1.67 billion by 2033.

- Consumer electronics, automotive, and advanced displays are key application segments fueling demand.

- AI integration is set to revolutionize material development, manufacturing efficiency, and quality control in the ACP sector.

- Emerging opportunities lie in flexible electronics, wearable devices, and IoT expansion.

- Market expansion is global, with APAC leading in production and consumption.

- Challenges include high manufacturing costs and competition from alternative bonding methods.

Anisotropic Conductive Paste Market Drivers Analysis

The Anisotropic Conductive Paste (ACP) market is propelled by a confluence of technological advancements and increasing industrial demands. The relentless pursuit of device miniaturization across various electronic sectors is a primary driver, as ACP offers fine pitch interconnection capabilities essential for compact designs where traditional soldering is impractical. The rapid proliferation of flexible and wearable electronic devices, requiring robust yet flexible bonding solutions, further boosts ACP adoption. Moreover, the global rollout of 5G technology and the expansion of the Internet of Things (IoT) ecosystem necessitates high-frequency, reliable interconnections, which ACP effectively provides. The automotive industry's transformative shift towards electric vehicles (EVs), advanced driver-assistance systems (ADAS), and in-cabin electronics significantly increases the demand for durable and heat-resistant ACP solutions. Furthermore, advancements in display technologies, including OLED and micro-LED, mandate ultra-fine pitch bonding for high-resolution screens, positioning ACP as a critical enabling material.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Miniaturization of Electronic Devices | +2.5% | Global, especially Asia Pacific (APAC) | Long-term (2025-2033) |

| Rising Demand for Flexible & Wearable Electronics | +1.8% | North America, Europe, Asia Pacific | Mid to Long-term (2026-2033) |

| Expansion of 5G Technology & IoT Devices | +1.5% | Global, particularly China, US, South Korea | Mid-term (2025-2030) |

| Growth in Automotive Electronics (EVs, ADAS) | +1.2% | Europe, North America, Japan, China | Long-term (2027-2033) |

| Advancements in Display Technologies (OLED, Micro-LED) | +0.8% | Asia Pacific (South Korea, China, Japan) | Mid to Long-term (2026-2033) |

Anisotropic Conductive Paste Market Restraints Analysis

Despite significant growth drivers, the Anisotropic Conductive Paste (ACP) market faces several critical restraints that could impede its expansion. One major challenge is the relatively high manufacturing cost associated with producing high-performance ACPs, which often utilize precious metal fillers and require precise formulation, leading to higher unit costs compared to conventional bonding methods like soldering. Furthermore, ACPs generally exhibit lower electrical conductivity and mechanical strength compared to solder joints in certain applications, which can limit their adoption in power-intensive or high-stress environments. Concerns regarding the long-term reliability and repairability of ACP connections, particularly in terms of moisture resistance and thermal cycling performance, also pose a significant restraint for critical applications. The availability and continuous development of alternative bonding technologies, such as non-conductive pastes (NCPs) or advanced soldering techniques, present a competitive threat. Additionally, the complexity of processing and application requirements for ACPs, often demanding specialized equipment and controlled environmental conditions, can deter smaller manufacturers or those lacking the necessary infrastructure.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Manufacturing Cost of ACP | -1.5% | Global, especially emerging markets | Long-term (2025-2033) |

| Lower Conductivity and Mechanical Strength vs. Solders | -1.0% | Global, high-performance applications | Long-term (2025-2033) |

| Reliability Concerns and Limited Repairability | -0.8% | Global, critical applications (e.g., automotive, aerospace) | Mid-term (2025-2030) |

| Availability of Alternative Bonding Technologies | -0.7% | Global | Mid-term (2025-2030) |

| Complexity of Processing and Application | -0.5% | Small and medium enterprises (SMEs) | Short to Mid-term (2025-2028) |

Anisotropic Conductive Paste Market Opportunities Analysis

The Anisotropic Conductive Paste (ACP) market is poised for significant expansion, driven by several emerging opportunities that capitalize on its unique properties and technological advancements. The burgeoning market for wearable electronics and advanced biomedical devices presents a substantial opportunity, as these applications demand highly flexible, discreet, and reliable interconnections that ACP can readily provide. The continuous expansion of the Internet of Things (IoT) ecosystem, coupled with the increasing need for integrated sensors in various industries, creates a strong demand for miniature, high-performance bonding solutions. Furthermore, the adoption of additive manufacturing techniques, such as 3D printing for electronics, opens new avenues for ACP, enabling complex circuit designs and customized device fabrication. The development of advanced packaging technologies like System-in-Package (SiP) and Chip-on-Wafer (CoW) for high-performance computing and data centers will increasingly rely on ACP for ultra-fine pitch and robust interconnections. Additionally, the ongoing research and development in smart textiles and flexible displays are creating niche markets where ACP's unique anisotropic properties are indispensable, fostering innovative product development and application diversification.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand in Wearable Electronics & Biomedical Devices | +1.5% | North America, Europe, Asia Pacific | Mid to Long-term (2026-2033) |

| Integration in IoT Devices and Advanced Sensor Modules | +1.2% | Global | Mid-term (2025-2030) |

| Expansion of Additive Manufacturing for Electronics | +0.9% | Global, R&D focused regions | Long-term (2027-2033) |

| Adoption in Advanced Packaging Technologies (SiP, CoW) | +0.7% | Global, especially semiconductor hubs | Mid to Long-term (2026-2033) |

| Emergence of Smart Textiles and Flexible Displays | +0.5% | Asia Pacific, Europe | Long-term (2028-2033) |

Anisotropic Conductive Paste Market Challenges Impact Analysis

The Anisotropic Conductive Paste (ACP) market, while promising, faces several inherent challenges that demand strategic responses from industry players. Significant supply chain disruptions, particularly regarding the availability and price volatility of key raw materials like precious metal fillers (e.g., gold, silver, nickel), pose a constant threat to production consistency and cost stability. The need for continuous substantial research and development (R&D) investments to enhance ACP performance, reduce costs, and develop novel applications puts pressure on manufacturers, especially smaller entities. A lack of standardized testing methods and material specifications across the industry can lead to compatibility issues and hinder widespread adoption, as manufacturers struggle to ensure consistent performance. Furthermore, evolving environmental regulations globally, particularly concerning hazardous substances and waste disposal, necessitate ongoing compliance efforts and may require costly reformulations. Intense competition from alternative bonding techniques, such as reflow soldering, wire bonding, and non-conductive pastes (NCPs), continually pushes ACP manufacturers to innovate and differentiate their products to maintain market share, compelling constant technological superiority.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Supply Chain Volatility and Raw Material Price Fluctuations | -1.0% | Global | Short to Mid-term (2025-2028) |

| High R&D Investment Requirements | -0.8% | Global, especially for new entrants | Long-term (2025-2033) |

| Lack of Standardized Testing and Material Specifications | -0.6% | Global | Mid-term (2025-2030) |

| Evolving Environmental Regulations | -0.5% | Europe, North America, specific Asian countries | Long-term (2027-2033) |

| Intense Competition from Alternative Bonding Methods | -0.4% | Global | Long-term (2025-2033) |

Anisotropic Conductive Paste Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Anisotropic Conductive Paste (ACP) market, offering detailed insights into its size, growth trends, competitive landscape, and future outlook. It includes a thorough examination of market drivers, restraints, opportunities, and challenges that shape the industry, alongside a quantitative forecast from 2025 to 2033. The report segments the market by product type, filler material, application, and end-use industry, providing a granular view of market dynamics across key regions. Key company profiles and a detailed competitive analysis help stakeholders understand the market structure and strategic initiatives of leading players. This updated scope ensures a holistic understanding for strategic decision-making in this evolving technological landscape.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 895 million |

| Market Forecast in 2033 | USD 1.67 billion |

| Growth Rate | 7.8% from 2025 to 2033 |

| Number of Pages | 255 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Hitachi Chemical, Henkel AG & Co. KGaA, 3M, Dow Inc., Shin-Etsu Chemical Co., Ltd., Namics Corporation, Dexerials Corporation, Delo Industrial Adhesives, Dupont de Nemours, Kyocera Corporation, Sekisui Chemical Co., Ltd., Panasonic Corporation, Fuji Chemical Industrial Co., Ltd., Showa Denko K.K., Sumitomo Bakelite Co., Ltd., Toray Industries, Inc., BASF SE, Lord Corporation, Electrolube, Mitsubishi Chemical Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Anisotropic Conductive Paste (ACP) market is comprehensively segmented to provide a detailed understanding of its diverse applications and material compositions. This segmentation allows for precise market sizing and forecasting, identifying key growth areas and niche opportunities across various sectors. Analyzing the market by its distinct segments offers valuable insights into consumer preferences, technological demands, and regional adoption patterns, enabling businesses to tailor their strategies effectively. This multi-faceted breakdown facilitates a granular understanding of the market dynamics, helping stakeholders identify high-potential segments and allocate resources strategically for maximum impact and competitive advantage.

- By Type: This segment differentiates between Anisotropic Conductive Film (ACF) and Anisotropic Conductive Paste (ACP). While both serve similar purposes in anisotropic conduction, films are typically pre-applied and offer ease of handling for mass production, whereas pastes provide flexibility for custom applications and reworkability.

- Anisotropic Conductive Film (ACF)

- Anisotropic Conductive Paste (ACP)

- By Filler Material: This segment categorizes ACP based on the conductive particles embedded within the paste. The choice of filler material significantly impacts conductivity, cost, and specific application performance.

- Gold (Au): Offers excellent conductivity and corrosion resistance, often used in high-reliability applications.

- Nickel (Ni): Cost-effective with good conductivity, suitable for various general electronic applications.

- Silver (Ag): High conductivity, widely used, but susceptible to migration issues in some conditions.

- Carbon: Increasingly used for cost-sensitive or specific flexible electronic applications.

- Others: Include various alloys, copper, or composite materials tailored for specific performance characteristics.

- By Application: This segment focuses on the primary uses of ACP across different electronic assembly processes. Each application has distinct requirements for paste properties such as curing temperature, adhesion, and fine pitch capability.

- Flip Chip Packaging: Critical for high-density, high-performance semiconductor integration.

- Chip-on-Glass (COG): Essential for bonding driver ICs directly onto display panels.

- Chip-on-Flex (COF): Used for connecting ICs to flexible circuits in compact designs.

- Flexible Printed Circuit (FPC) Bonding: For robust and reliable connections in flexible electronics.

- Display Modules: Pervasive in LCD, OLED, and micro-LED screen manufacturing for fine pitch interconnects.

- PCB Assembly: Utilized in specialized areas of printed circuit board manufacturing where soldering is not viable.

- Others: Includes applications in sensor integration, memory devices, and optical modules.

- By End-use Industry: This segment delineates the major industries that integrate ACP into their products, highlighting the diverse market penetration and specific industry demands.

- Consumer Electronics: Dominant sector including smartphones, tablets, laptops, wearables, and smart home devices, demanding miniaturization and high performance.

- Automotive: Growing sector encompassing electric vehicles (EVs), advanced driver-assistance systems (ADAS), infotainment systems, and lighting, requiring high reliability and thermal stability.

- Healthcare: Utilized in compact medical devices, diagnostic equipment, and wearable health monitors where precision and biocompatibility are crucial.

- Aerospace & Defense: Applications requiring extreme reliability, light weight, and performance under harsh environmental conditions.

- Industrial Electronics: Includes industrial controls, automation equipment, and power modules, where robust and durable connections are necessary.

- Telecommunications: Critical for 5G infrastructure, network equipment, and communication modules, demanding high-frequency performance.

- Others: Comprising applications in renewable energy, security systems, and various niche electronic components.

Regional Highlights

The global Anisotropic Conductive Paste (ACP) market exhibits distinct regional dynamics, largely influenced by the concentration of electronics manufacturing, technological innovation, and end-use industry growth. Understanding these regional highlights is crucial for market participants to identify lucrative opportunities and formulate targeted expansion strategies.

- Asia Pacific (APAC): This region dominates the Anisotropic Conductive Paste market, primarily due to the presence of major electronics manufacturing hubs in countries like China, South Korea, Japan, and Taiwan. These nations are at the forefront of producing consumer electronics, displays (LCD, OLED, micro-LED), and advanced semiconductor components, which are significant consumers of ACP. The robust investment in 5G infrastructure, rapid urbanization, and a large consumer base further fuel the demand for compact and high-performance electronic devices, making APAC the highest growth potential region for ACP.

- North America: Characterized by strong research and development capabilities and a thriving automotive industry, North America represents a significant market for ACP. The region's focus on advanced driver-assistance systems (ADAS), electric vehicles (EVs), and aerospace and defense applications drives the demand for high-reliability ACP solutions. Furthermore, the presence of leading technology companies and continuous innovation in IoT and wearable electronics contribute to market growth.

- Europe: Europe is a key market for Anisotropic Conductive Paste, driven by its advanced manufacturing sector, particularly in automotive electronics, industrial automation, and medical devices. Countries like Germany, France, and the UK are investing heavily in smart manufacturing and Industry 4.0 initiatives, which require sophisticated electronic interconnections. Strict environmental regulations also push for the adoption of lead-free and sustainable ACP formulations, fostering innovation in this region.

- Latin America: While a smaller market compared to APAC or North America, Latin America shows promising growth due to increasing industrialization and rising disposable incomes. The expanding consumer electronics market and nascent automotive manufacturing activities in countries like Brazil and Mexico contribute to the demand for ACP, albeit at a slower pace.

- Middle East and Africa (MEA): The MEA region is an emerging market for Anisotropic Conductive Paste, with growth primarily driven by infrastructure development, increasing adoption of consumer electronics, and investments in telecommunications. While the overall market size is currently modest, long-term potential exists with diversified economic initiatives and technological advancements in certain countries.

Top Key Players:

The market research report covers the analysis of key stake holders of the Anisotropic Conductive Paste Market. Some of the leading players profiled in the report include -:- Hitachi Chemical

- Henkel AG & Co. KGaA

- 3M

- Dow Inc.

- Shin-Etsu Chemical Co., Ltd.

- Namics Corporation

- Dexerials Corporation

- Delo Industrial Adhesives

- Dupont de Nemours

- Kyocera Corporation

- Sekisui Chemical Co., Ltd.

- Panasonic Corporation

- Fuji Chemical Industrial Co., Ltd.

- Showa Denko K.K.

- Sumitomo Bakelite Co., Ltd.

- Toray Industries, Inc.

- BASF SE

- Lord Corporation

- Electrolube

- Mitsubishi Chemical Corporation

Frequently Asked Questions:

What is Anisotropic Conductive Paste (ACP)?

Anisotropic Conductive Paste (ACP) is an advanced adhesive material containing conductive particles that facilitate electrical conduction in only one direction (z-axis) while providing electrical insulation in the planar (x-y) direction. It is primarily used for fine pitch interconnections in electronic devices, offering a lead-free and compact alternative to traditional soldering methods.

What are the primary applications of Anisotropic Conductive Paste?

The primary applications of Anisotropic Conductive Paste include flip chip packaging, Chip-on-Glass (COG) bonding for LCD and OLED displays, Chip-on-Flex (COF) bonding, and Flexible Printed Circuit (FPC) bonding. It is widely used in consumer electronics, automotive electronics, and advanced display modules due to its ability to create fine pitch, reliable connections in space-constrained designs.

What factors are driving the growth of the Anisotropic Conductive Paste market?

The growth of the Anisotropic Conductive Paste market is primarily driven by the increasing miniaturization of electronic devices, the rising demand for flexible and wearable electronics, the expansion of 5G technology and IoT devices, and the significant growth in automotive electronics, particularly electric vehicles and advanced driver-assistance systems (ADAS).

What are the main challenges faced by the Anisotropic Conductive Paste market?

Key challenges for the Anisotropic Conductive Paste market include the relatively high manufacturing cost compared to conventional bonding methods, limitations in conductivity and mechanical strength in certain applications, concerns regarding long-term reliability and repairability, and intense competition from alternative bonding technologies like traditional solders and non-conductive pastes (NCPs).

What is the projected market size and growth rate for Anisotropic Conductive Paste?

The Anisotropic Conductive Paste market is projected to grow from USD 895 million in 2025 to USD 1.67 billion by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of 7.8% during the forecast period from 2025 to 2033. This growth is underpinned by continuous technological advancements and increasing demand across various end-use industries.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted