Unleaded Solder Paste Market

Unleaded Solder Paste Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705660 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

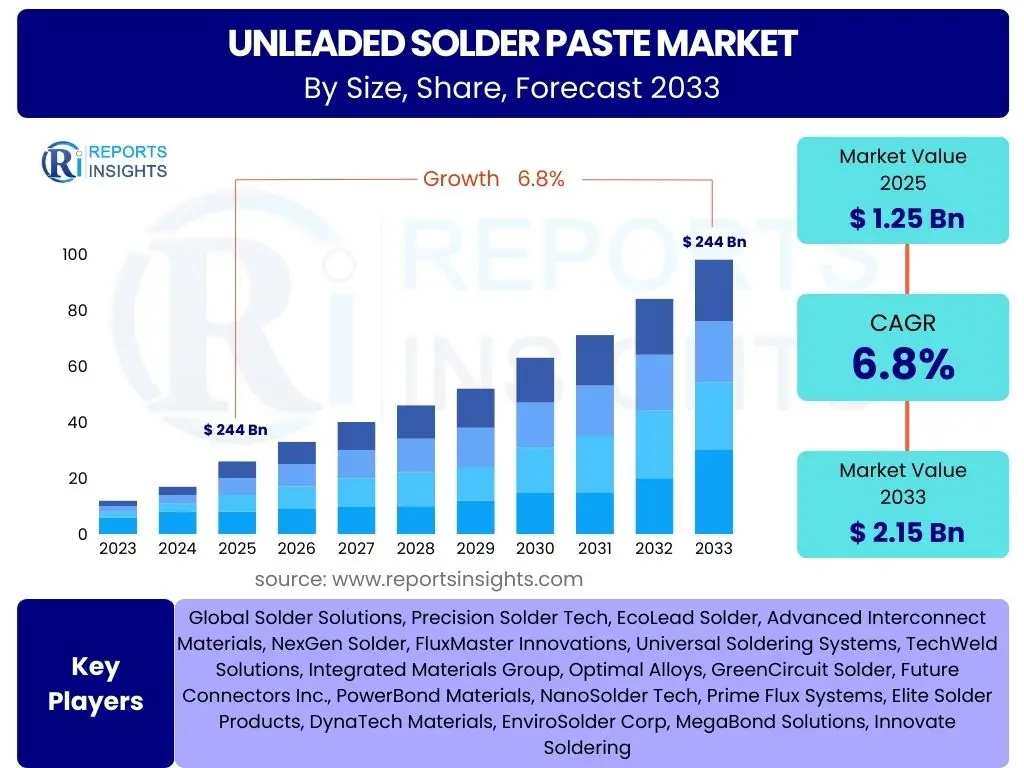

Unleaded Solder Paste Market Size

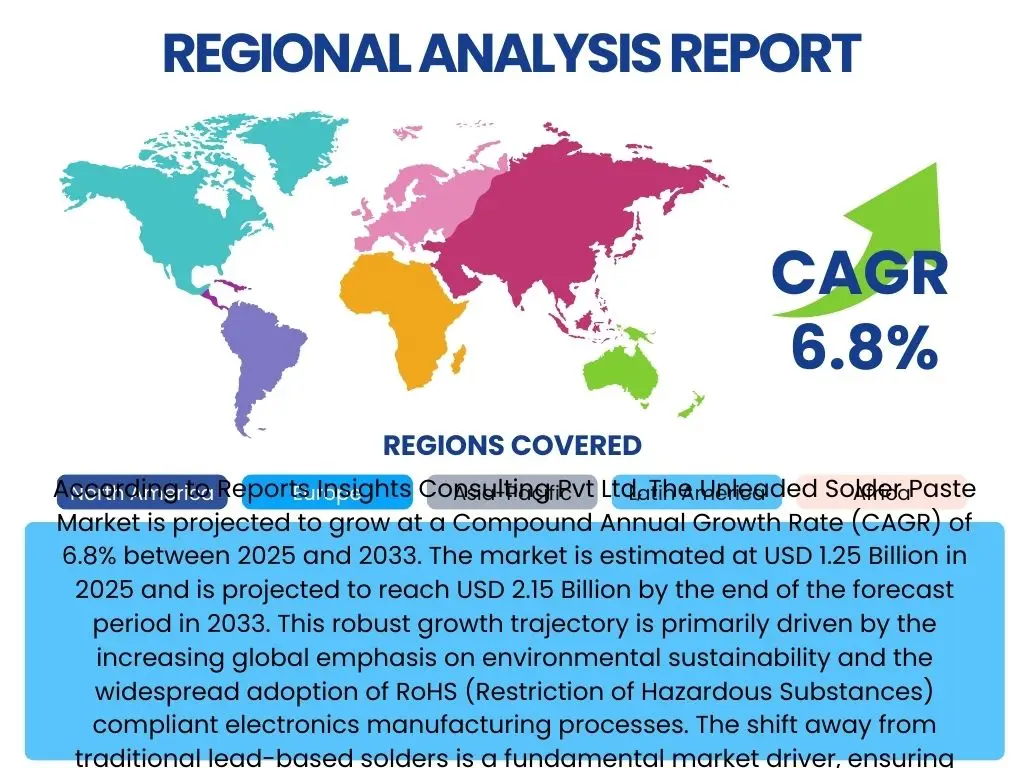

According to Reports Insights Consulting Pvt Ltd, The Unleaded Solder Paste Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 1.25 Billion in 2025 and is projected to reach USD 2.15 Billion by the end of the forecast period in 2033. This robust growth trajectory is primarily driven by the increasing global emphasis on environmental sustainability and the widespread adoption of RoHS (Restriction of Hazardous Substances) compliant electronics manufacturing processes. The shift away from traditional lead-based solders is a fundamental market driver, ensuring sustained demand for unleaded alternatives across various industries.

The expansion of key end-use industries, including consumer electronics, automotive, and telecommunications, significantly contributes to the market's upward trend. Miniaturization of electronic components and the continuous innovation in advanced packaging technologies necessitate high-performance, reliable solder pastes that meet stringent environmental standards. As global electronics production continues to decentralize and expand into emerging economies, the demand for unleaded solder paste is expected to witness substantial growth, supporting the projected market valuation.

Key Unleaded Solder Paste Market Trends & Insights

Common user inquiries about the Unleaded Solder Paste market frequently revolve around the latest technological advancements, regulatory pressures, and application-specific innovations. Users are particularly interested in how manufacturers are addressing performance challenges associated with lead-free alternatives, such as wettability, voiding, and thermal cycle reliability. There is a strong focus on sustainable manufacturing practices, with a growing demand for eco-friendly formulations and processes that align with global environmental mandates. Furthermore, the integration of smart manufacturing techniques and automation in assembly lines is a recurring theme, driving the need for solder pastes compatible with high-throughput production.

The industry is witnessing a significant trend towards the development of ultra-fine pitch solder pastes designed for high-density interconnects and miniaturized electronic devices. This includes formulations optimized for flip-chip, wafer-level packaging, and 3D stacking technologies, which are critical for next-generation electronics. Another prominent trend is the increasing diversification of alloy compositions beyond traditional tin-silver-copper (SAC) alloys, with researchers exploring bismuth, indium, and antimony additions to enhance specific properties like low-temperature soldering capabilities or improved mechanical strength. This diversification aims to cater to a broader range of applications and operational environments.

- Growing demand for halogen-free and low-residue solder paste formulations.

- Increased adoption in advanced packaging solutions like SiP and AiP modules.

- Focus on improved printability and extended stencil life for high-volume manufacturing.

- Development of low-temperature solder pastes for heat-sensitive components.

- Expansion of customized formulations for specific substrate materials and process conditions.

AI Impact Analysis on Unleaded Solder Paste

User questions concerning the impact of Artificial Intelligence (AI) on the Unleaded Solder Paste market primarily center on how AI can optimize manufacturing processes, enhance product quality, and accelerate research and development. There is keen interest in AI's potential to predict and prevent defects in soldering, improve material formulation, and streamline supply chain logistics. Users are also curious about the feasibility of AI-driven quality control systems that can ensure consistent performance of solder paste under various application conditions. Concerns often include the initial investment required for AI integration and the need for specialized data and expertise.

AI's influence is anticipated to revolutionize several aspects of the unleaded solder paste lifecycle. In manufacturing, AI algorithms can analyze vast datasets from production lines to identify optimal processing parameters, thereby reducing waste and improving yield. Predictive analytics powered by AI can forecast equipment failures, allowing for proactive maintenance and minimizing downtime. For product development, AI and machine learning can rapidly screen potential new alloy compositions and flux chemistries, dramatically shortening the R&D cycle for novel solder paste formulations with enhanced properties. Furthermore, AI can optimize inventory management and demand forecasting, leading to more efficient supply chain operations.

- AI-driven optimization of solder paste reflow profiles for superior joint reliability.

- Predictive quality control systems to detect and mitigate soldering defects in real-time.

- Accelerated discovery of novel unleaded alloy compositions and flux systems using machine learning.

- Enhanced supply chain visibility and demand forecasting through AI-powered analytics.

- Automation of visual inspection processes for solder paste deposition and post-reflow joints.

Key Takeaways Unleaded Solder Paste Market Size & Forecast

Common user questions regarding key takeaways from the Unleaded Solder Paste market size and forecast often focus on identifying the most critical growth drivers, the primary challenges to market expansion, and the regions poised for significant development. Users want to understand the overarching strategic implications for businesses operating within or looking to enter this market. Insights into future market direction, potential investment opportunities, and the long-term sustainability of unleaded solutions are also highly sought after. This encapsulates the desire for actionable intelligence derived from the market's quantitative projections and qualitative trends.

The market is set for sustained growth, predominantly propelled by stringent environmental regulations and the relentless innovation within the electronics sector. The imperative to replace lead-based solders globally ensures a foundational demand for unleaded alternatives, making compliance a significant market accelerator. While technological challenges related to performance equivalence with leaded solders persist, ongoing research and development efforts are steadily bridging this gap, offering more robust and application-specific unleaded solutions. The Asia Pacific region is expected to remain the dominant market, driven by its extensive electronics manufacturing base and burgeoning consumer demand, presenting substantial opportunities for market players.

- Global environmental regulations, particularly RoHS, are the primary long-term market catalysts.

- Asia Pacific is expected to maintain its leading position in market size and growth due to manufacturing concentration.

- Continuous innovation in alloy compositions and flux chemistries is crucial for overcoming performance challenges.

- The automotive and telecommunications sectors are key application areas driving high-performance unleaded solder paste demand.

- Investment in R&D for low-temperature and high-reliability formulations represents a significant strategic imperative.

Unleaded Solder Paste Market Drivers Analysis

The unleaded solder paste market is primarily driven by a confluence of regulatory mandates, technological advancements, and burgeoning demand from key end-use industries. Global environmental awareness has spurred the adoption of Restriction of Hazardous Substances (RoHS) directives, compelling electronics manufacturers worldwide to transition away from lead-based solders. This legislative push is a fundamental driver, creating a non-negotiable demand for lead-free alternatives. Moreover, the rapid evolution and miniaturization of electronic devices necessitate advanced interconnect materials that offer superior performance and reliability within compact designs, a requirement increasingly met by sophisticated unleaded solder paste formulations.

The relentless expansion of the consumer electronics market, coupled with the exponential growth in automotive electronics (driven by electric vehicles and advanced driver-assistance systems), telecommunications infrastructure (5G deployment), and the Internet of Things (IoT), significantly fuels the demand for unleaded solder paste. These sectors require high-reliability, long-lasting solder joints, pushing manufacturers to continuously innovate and refine unleaded solutions. The increasing complexity and performance demands of modern electronics, from smartphones to medical devices, create a sustained imperative for advanced, environmentally compliant soldering materials.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Strict Environmental Regulations (e.g., RoHS) | +2.5% | Global, particularly Europe, North America, APAC | Long-term (2025-2033) |

| Growth in Consumer Electronics & Miniaturization | +1.8% | Asia Pacific, North America, Europe | Mid to Long-term (2025-2033) |

| Expansion of Automotive Electronics (EVs, ADAS) | +1.5% | Europe, North America, China, Japan | Mid to Long-term (2025-2033) |

| Advancements in 5G and IoT Infrastructure | +0.8% | Global, especially China, USA, South Korea | Mid-term (2025-2030) |

| Demand for High-Performance & Reliability in Electronics | +0.5% | Global | Long-term (2025-2033) |

Unleaded Solder Paste Market Restraints Analysis

Despite the strong growth drivers, the Unleaded Solder Paste market faces several significant restraints that could temper its expansion. One primary concern is the relatively higher cost of production and raw materials compared to traditional leaded solder pastes. The specialized alloys and flux chemistries required for optimal unleaded performance often lead to increased material expenses, which can be a barrier for cost-sensitive manufacturers. Furthermore, the inherent performance differences, such as wetting characteristics, void formation, and reliability under certain stress conditions, continue to pose technical challenges that require continuous research and development to mitigate.

Another key restraint involves the complexity of process optimization when transitioning to unleaded solder pastes. Manufacturers often need to re-tool production lines, adjust reflow profiles, and invest in new equipment to achieve reliable solder joints, leading to significant upfront costs and potential downtime. Issues like tin whiskers, a unique reliability concern associated with lead-free solders, also require careful material selection and process control to prevent, adding another layer of complexity. Moreover, the volatility of raw material prices, particularly for tin, silver, and copper, can introduce instability in the supply chain and impact overall product pricing, affecting market predictability and profitability.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Higher Production & Raw Material Costs | -1.2% | Global, impacting SMEs | Long-term (2025-2033) |

| Performance Challenges (Wettability, Voiding) | -0.9% | Global | Mid-term (2025-2030) |

| Complexity of Process Optimization & Rework | -0.7% | Global, particularly smaller manufacturers | Mid-term (2025-2030) |

| Volatility in Key Raw Material Prices | -0.6% | Global | Short to Mid-term (2025-2028) |

| Risk of Tin Whiskers & Long-term Reliability Concerns | -0.4% | Global, high-reliability applications | Long-term (2025-2033) |

Unleaded Solder Paste Market Opportunities Analysis

The Unleaded Solder Paste market presents numerous opportunities for growth, driven by evolving technological landscapes and expanding applications. One significant avenue lies in the burgeoning demand from emerging economies, particularly in Southeast Asia and Latin America, where electronics manufacturing bases are rapidly expanding to meet domestic and export needs. These regions offer new markets for unleaded solutions as they adopt more stringent environmental standards and scale up their production capabilities. The continuous evolution of electronics, particularly in areas like advanced packaging technologies (e.g., System-in-Package, Chip-on-Board), creates a specific need for highly specialized and reliable unleaded solder pastes that can facilitate miniaturization and enhance device performance.

The exponential growth of the Electric Vehicle (EV) industry represents a substantial opportunity, as EVs require robust, high-reliability electronics capable of withstanding harsh operating conditions, for which unleaded solder is becoming the material of choice. Similarly, the medical device sector, with its stringent requirements for reliability, biocompatibility, and miniaturization, is increasingly adopting unleaded solder paste, offering a high-value niche market. Furthermore, the global push towards sustainable manufacturing practices and the circular economy opens doors for innovations in eco-friendly solder paste formulations, including those made from recycled materials or designed for easier disassembly and recycling, aligning with future regulatory trends and consumer preferences.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expanding Electronics Manufacturing in Emerging Economies | +1.5% | Southeast Asia, Latin America, Eastern Europe | Mid to Long-term (2025-2033) |

| Growth in Electric Vehicle (EV) & Automotive Electronics | +1.3% | Global, particularly China, Europe, North America | Long-term (2025-2033) |

| Development of Advanced Packaging Technologies | +1.0% | Global, high-tech manufacturing hubs | Long-term (2025-2033) |

| Increasing Demand from Medical Device Industry | +0.8% | North America, Europe, Japan | Mid to Long-term (2025-2033) |

| Focus on Sustainable & Eco-Friendly Formulations | +0.6% | Global, particularly developed markets | Long-term (2025-2033) |

Unleaded Solder Paste Market Challenges Impact Analysis

The Unleaded Solder Paste market encounters several critical challenges that require continuous innovation and strategic responses from manufacturers. A primary technical hurdle is achieving optimal wettability on diverse substrate finishes while minimizing voiding in solder joints, especially in miniaturized and high-density electronic assemblies. Voids can compromise mechanical strength, electrical conductivity, and thermal dissipation, thereby impacting the long-term reliability of electronic devices. Addressing these issues often necessitates complex material formulations and precise process control, adding to manufacturing complexities and costs.

Another significant challenge lies in managing the thermal properties of unleaded solder joints, particularly in high-power applications where efficient heat dissipation is crucial for component longevity. Differences in melting temperatures and thermal expansion coefficients compared to leaded solders can lead to new design and engineering considerations. Furthermore, the industry faces the challenge of standardizing material specifications and process guidelines across various applications and geographies, which can impede broader adoption and cross-compatibility. The ongoing need for skilled labor to manage advanced soldering processes and respond to rapid technological shifts also presents a human capital challenge within the market.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Achieving Optimal Wettability & Minimizing Voiding | -1.0% | Global, high-density applications | Long-term (2025-2033) |

| Thermal Management in High-Power Applications | -0.8% | Global, automotive, industrial electronics | Mid to Long-term (2025-2033) |

| Material Compatibility & Component Reliability | -0.7% | Global, particularly legacy systems | Mid-term (2025-2030) |

| Skilled Labor Shortage & Training Requirements | -0.5% | Global, especially developed economies | Long-term (2025-2033) |

| Supply Chain Disruptions & Raw Material Sourcing | -0.4% | Global, geopolitical hotspots | Short to Mid-term (2025-2028) |

Unleaded Solder Paste Market - Updated Report Scope

This report provides a comprehensive analysis of the Unleaded Solder Paste Market, delving into its current size, historical performance, and future growth projections up to 2033. It offers an in-depth exploration of market drivers, restraints, opportunities, and challenges, providing a holistic view of the factors influencing market dynamics. The scope includes detailed segmentation analysis by product type, alloy composition, application, and end-use industry, alongside a thorough regional assessment. Furthermore, the report identifies key market trends, the impact of emerging technologies like AI, and profiles leading market players to provide strategic insights for stakeholders.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.25 Billion |

| Market Forecast in 2033 | USD 2.15 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Solder Solutions, Precision Solder Tech, EcoLead Solder, Advanced Interconnect Materials, NexGen Solder, FluxMaster Innovations, Universal Soldering Systems, TechWeld Solutions, Integrated Materials Group, Optimal Alloys, GreenCircuit Solder, Future Connectors Inc., PowerBond Materials, NanoSolder Tech, Prime Flux Systems, Elite Solder Products, DynaTech Materials, EnviroSolder Corp, MegaBond Solutions, Innovate Soldering |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Unleaded Solder Paste market is extensively segmented to provide a granular understanding of its diverse components and their respective contributions to overall market dynamics. This segmentation facilitates a deeper analysis of specific product types, alloy compositions, application areas, and end-use industries, enabling stakeholders to identify niche opportunities and tailor strategies effectively. Each segment is influenced by distinct technological advancements, regulatory pressures, and market demands, showcasing the multifaceted nature of the unleaded solder paste landscape.

Understanding these segments is crucial for market players to optimize their product portfolios, target specific customer needs, and navigate competitive landscapes. For instance, the "No-Clean" type of solder paste is gaining traction due to its ability to reduce manufacturing costs and environmental impact, while "Tin-Silver-Copper (SAC) Alloys" remain dominant for high-reliability applications. The analysis further breaks down consumption across critical applications like Surface Mount Technology (SMT), which dominates modern electronics manufacturing, and various end-use industries, from high-volume consumer electronics to specialized medical devices and robust automotive systems.

- By Type:

- No-Clean Solder Paste

- Water-Soluble Solder Paste

- Rosin Mildly Activated (RMA) Solder Paste

- By Alloy Type:

- Tin-Silver-Copper (SAC) Alloys

- Tin-Copper (Sn-Cu) Alloys

- Tin-Bismuth (Sn-Bi) Alloys

- Other Alloys (e.g., Tin-Indium, Tin-Antimony)

- By Application:

- Surface Mount Technology (SMT)

- Through-Hole Technology (THT)

- Semiconductor Packaging

- LED Packaging

- Other Applications (e.g., Flex Circuits, Hybrid Microelectronics)

- By End-Use Industry:

- Consumer Electronics

- Automotive

- Telecommunications

- Industrial Electronics

- Medical Devices

- Aerospace & Defense

- Other End-Use Industries (e.g., Home Appliances, Lighting)

Regional Highlights

- Asia Pacific (APAC): Dominates the unleaded solder paste market due to its extensive electronics manufacturing base, including countries like China, Japan, South Korea, Taiwan, and Southeast Asian nations. The region benefits from high production volumes of consumer electronics, telecommunications equipment, and automotive components, coupled with growing adoption of lead-free regulations. Significant investment in advanced packaging and semiconductor industries further fuels demand.

- North America: Exhibits strong growth driven by increasing demand from high-reliability applications in automotive electronics, medical devices, and aerospace & defense sectors. Strict environmental regulations and a focus on technological innovation also contribute to the adoption of advanced unleaded solder paste formulations. Research and development activities for next-generation electronic components are a key driver.

- Europe: A significant market characterized by stringent environmental directives and a robust automotive industry, alongside strong industrial electronics and telecommunications sectors. Countries like Germany, France, and the UK are at the forefront of adopting sustainable manufacturing practices and advanced soldering solutions. The region's emphasis on high-quality and long-lasting electronic products drives demand for premium unleaded solder pastes.

- Latin America: Emerging as a growing market for unleaded solder paste, primarily due to expanding electronics manufacturing operations and increasing consumer demand for electronic devices. Brazil and Mexico are key contributors, benefiting from foreign investments and developing domestic electronics industries. The region is gradually aligning with global environmental standards, fostering a transition to lead-free materials.

- Middle East & Africa (MEA): Represents an emerging market with gradual adoption of unleaded solder paste, driven by infrastructure development and increasing electronics assembly activities. Growth is expected to be steady, albeit from a smaller base, as industrialization and technological advancements encourage local manufacturing and the implementation of international environmental standards.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Unleaded Solder Paste Market.- Global Solder Solutions

- Precision Solder Tech

- EcoLead Solder

- Advanced Interconnect Materials

- NexGen Solder

- FluxMaster Innovations

- Universal Soldering Systems

- TechWeld Solutions

- Integrated Materials Group

- Optimal Alloys

- GreenCircuit Solder

- Future Connectors Inc.

- PowerBond Materials

- NanoSolder Tech

- Prime Flux Systems

- Elite Solder Products

- DynaTech Materials

- EnviroSolder Corp

- MegaBond Solutions

- Innovate Soldering

Frequently Asked Questions

What is unleaded solder paste and why is it important?

Unleaded solder paste is a specialized mixture of powdered lead-free solder alloy, flux, and a paste binder, used to create electrical connections in electronics manufacturing. It is crucial due to global environmental regulations, particularly the Restriction of Hazardous Substances (RoHS) directives, which mandate the elimination of lead from electronic products, promoting a safer and more sustainable manufacturing process.

What are the primary applications of unleaded solder paste?

Unleaded solder paste is widely used across various electronics manufacturing applications. Its primary uses include Surface Mount Technology (SMT) for attaching components to printed circuit boards, semiconductor packaging, LED packaging, and specialized applications in consumer electronics, automotive electronics, telecommunications equipment, medical devices, and industrial control systems.

What are the main challenges associated with using unleaded solder paste?

Key challenges include achieving optimal wetting on component pads and minimizing void formation in solder joints, which can affect reliability. Other challenges involve higher material costs compared to leaded solders, the need for precise process optimization (e.g., reflow profiles), and specific reliability concerns like tin whisker growth in certain unleaded alloy compositions.

How does unleaded solder paste differ from traditional leaded solder paste?

The primary difference is the absence of lead in unleaded formulations, typically replaced by tin-based alloys often mixed with silver, copper, or bismuth. This necessitates higher processing temperatures, different reflow profiles, and unique material properties, such as changes in wettability, mechanical strength, and potential for tin whiskers, all of which require specific considerations in manufacturing.

Which regions are leading the adoption of unleaded solder paste?

The Asia Pacific (APAC) region currently leads the adoption of unleaded solder paste, driven by its expansive electronics manufacturing industry and increasing adherence to global environmental standards. North America and Europe also demonstrate significant adoption due to stringent regulatory frameworks, technological advancements, and strong demand from high-reliability sectors like automotive and medical electronics.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted