Alternative Lending Market

Alternative Lending Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700974 | Last Updated : July 29, 2025 |

Format : ![]()

![]()

![]()

![]()

Alternative Lending Market Size

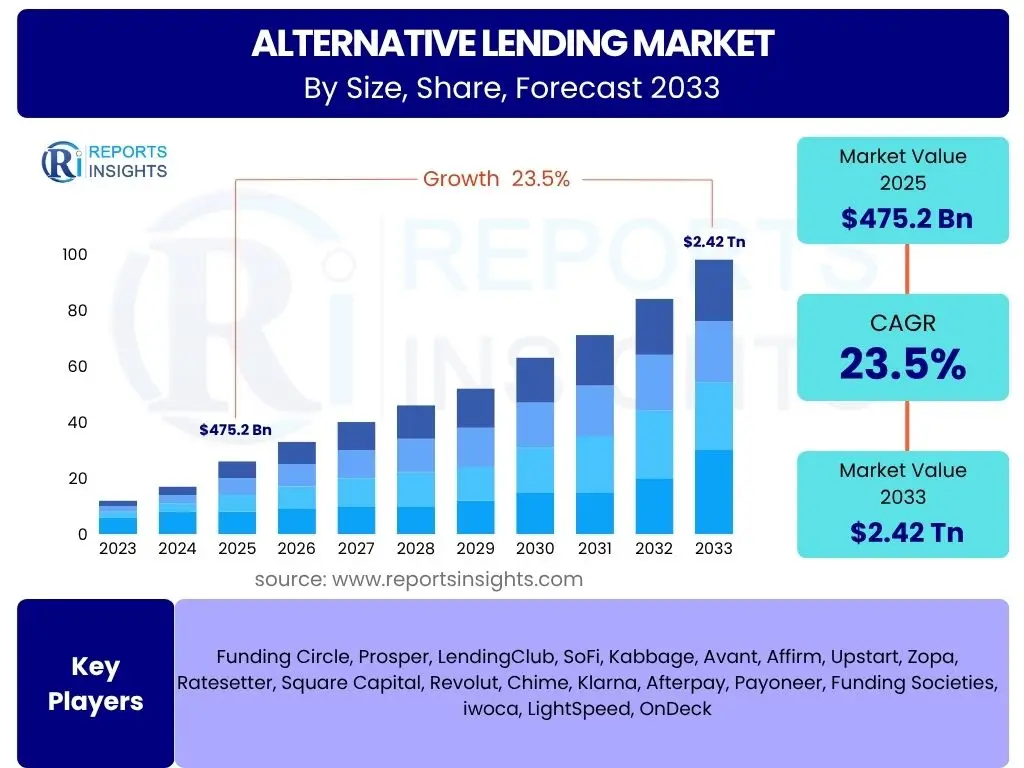

According to Reports Insights Consulting Pvt Ltd, The Alternative Lending Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 23.5% between 2025 and 2033. The market is estimated at USD 475.2 Billion in 2025 and is projected to reach USD 2.42 Trillion by the end of the forecast period in 2033.

Key Alternative Lending Market Trends & Insights

The alternative lending market is currently experiencing a profound transformation, driven by technological advancements and evolving borrower needs. Common inquiries from users highlight a keen interest in understanding the underlying forces shaping this sector, particularly the shift towards digital-first solutions and the emergence of new financing models. These trends indicate a market moving rapidly beyond traditional banking paradigms, focusing on speed, accessibility, and personalization for both individual and business borrowers.

A significant trend observed is the increasing adoption of data-driven decision-making, moving beyond conventional credit scores to leverage alternative data points. This allows lenders to serve a broader demographic, including the unbanked or underbanked, and small and medium-sized enterprises (SMEs) often overlooked by traditional institutions. Furthermore, the market is seeing a convergence of financial technology (FinTech) and lending, leading to innovative product offerings and streamlined application processes that cater to instant gratification in financial transactions. The regulatory landscape is also adapting, creating both opportunities for innovation and challenges related to consumer protection and market stability.

- Accelerated Digitalization and Mobile-First Strategies

- Expansion of Embedded Finance Solutions

- Diversification of Lending Products (e.g., Revenue-Based Financing)

- Increased Focus on Underserved and Niche Markets

- Strategic Partnerships Between FinTechs and Traditional Banks

- Growing Demand for Speed and Seamless User Experience

- Evolution of Regulatory Frameworks and Compliance

AI Impact Analysis on Alternative Lending

The impact of Artificial Intelligence (AI) on the alternative lending sector is a frequently discussed topic, with users often inquiring about its benefits in credit assessment, operational efficiency, and personalized customer experiences. There's a strong focus on how AI can democratize access to credit by offering more nuanced risk assessments, moving beyond traditional FICO scores. Users also express interest in AI's role in fraud detection and streamlining the lending process from application to disbursement, indicating an expectation for faster and more secure transactions.

However, concerns regarding algorithmic bias and data privacy are also prominent. Users want to understand how AI models are trained to avoid discrimination and ensure fairness, especially when evaluating individuals or businesses with limited credit history. The expectation is that AI will not only enhance profitability and reduce risk for lenders but also lead to more equitable and transparent lending practices for borrowers. This balance between innovation and ethical considerations defines the user's perception of AI's influence in alternative lending.

- Enhanced Credit Scoring and Risk Assessment leveraging Alternative Data

- Automated Loan Origination and Processing

- Improved Fraud Detection and Prevention

- Personalized Product Offerings and Customer Experience

- Operational Efficiency and Cost Reduction for Lenders

- Real-time Monitoring of Loan Performance

- Challenges in Addressing Algorithmic Bias and Explainability

Key Takeaways Alternative Lending Market Size & Forecast

The alternative lending market is poised for significant expansion, as evidenced by its robust projected growth rate. Common user questions regarding market size and forecast often revolve around identifying the primary drivers of this growth and understanding where the most substantial opportunities lie. The overarching insight is that the market's trajectory is driven by unmet demand from traditional financial institutions, coupled with technological innovation that enables faster, more flexible, and more accessible financing solutions. This indicates a paradigm shift where convenience and inclusivity are becoming paramount.

A key takeaway is the market's increasing diversification, with various lending models catering to specific segments, from small businesses seeking quick capital to individuals requiring flexible personal loans. The forecast indicates that while North America and Europe will remain significant contributors, the Asia Pacific region is expected to demonstrate exponential growth, fueled by a large underserved population and rapid digital adoption. This signals a global rebalancing of financial services, where alternative lenders play a crucial role in economic development and financial inclusion across diverse geographies.

- Strong double-digit growth driven by digital transformation.

- Significant market share shift from traditional banking.

- SMEs and unbanked populations represent substantial growth segments.

- Asia Pacific emerging as a key growth engine.

- Technology adoption (AI, Blockchain) critical for competitive advantage.

- Regulatory evolution will shape market dynamics.

Alternative Lending Market Drivers Analysis

The alternative lending market's growth is fundamentally propelled by the increasing demand for accessible and swift financing options, particularly from segments historically underserved by traditional banks. Small and medium-sized enterprises (SMEs), for instance, often struggle to secure conventional loans due to stringent requirements, lengthy application processes, and a lack of collateral. Alternative lenders, leveraging technology, offer a lifeline to these businesses, providing tailored financial products with quicker approval times and more flexible terms, thereby filling a critical market gap.

Technological advancements, especially in data analytics, artificial intelligence, and cloud computing, are also powerful drivers. These technologies enable alternative lenders to process vast amounts of data, assess creditworthiness more accurately using alternative data points, and automate various stages of the lending process. This not only reduces operational costs for lenders but also enhances the customer experience by providing seamless, digital-first interactions. The convenience and speed offered by these platforms are increasingly attractive to a generation accustomed to on-demand services, fostering widespread adoption.

Furthermore, evolving consumer expectations for personalized and immediate financial services push the market forward. Borrowers today seek transparent processes, competitive rates, and the ability to apply for and manage loans entirely online or via mobile applications. The regulatory environment in some regions is also becoming more accommodative towards FinTech innovation, fostering a conducive ecosystem for alternative lending platforms to thrive, albeit with an increasing focus on consumer protection and financial stability.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Digital Transformation & Technology Adoption | +5.5% | Global, particularly North America, APAC | Short to Mid-term (2025-2030) |

| Gap in SME & Consumer Financing by Traditional Banks | +4.8% | Global, particularly Emerging Markets, Europe | Mid to Long-term (2025-2033) |

| Increasing Demand for Faster & Convenient Financing | +4.2% | Global | Short-term (2025-2028) |

| Growth of e-commerce & Online Businesses | +3.5% | APAC, North America, Europe | Mid-term (2026-2031) |

| Favorable Regulatory Sandboxes & FinTech Support | +2.7% | UK, Singapore, Australia, UAE | Mid to Long-term (2027-2033) |

| Lower Operating Costs for Alternative Lenders | +2.0% | Global | Short to Mid-term (2025-2030) |

| Rising Financial Inclusion Initiatives | +1.8% | Developing Economies (APAC, LATAM, MEA) | Long-term (2028-2033) |

Alternative Lending Market Restraints Analysis

Despite its significant growth potential, the alternative lending market faces several notable restraints that could temper its expansion. Regulatory uncertainty and evolving compliance frameworks represent a primary challenge. As the sector grows and gains prominence, governments and financial authorities are increasingly scrutinizing alternative lending models to ensure consumer protection, prevent fraud, and maintain financial stability. Implementing new regulations can be costly and complex for lenders, potentially stifling innovation or increasing operational overheads, thereby impacting profitability and market entry for smaller players.

Another significant restraint is the inherent credit risk associated with lending to segments that are often deemed higher risk by traditional institutions. While alternative lenders leverage advanced analytics, the risk of default, especially during economic downturns, remains a critical concern. Managing large portfolios of small, higher-risk loans requires robust risk management frameworks and capital reserves, which can be challenging to maintain. Perceptions of risk among investors funding these platforms can also fluctuate, impacting the availability and cost of capital for alternative lenders.

Furthermore, competition from traditional banks, which are increasingly adopting FinTech solutions and launching their own digital lending arms, poses a competitive threat. Established banks possess vast customer bases, lower cost of capital, and deep trust, allowing them to potentially offer competitive rates or integrate alternative lending features into their existing services. Data security and privacy concerns also act as a restraint; with an increasing reliance on digital platforms and personal data, the threat of cyberattacks and data breaches can erode consumer trust and lead to significant financial and reputational damages for alternative lenders.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Regulatory Scrutiny & Compliance Costs | -3.9% | Global, particularly EU, US | Mid to Long-term (2026-2033) |

| Economic Volatility & Credit Risk Management | -3.5% | Global | Short to Mid-term (2025-2030) |

| Data Security & Privacy Concerns | -3.2% | Global | Short to Mid-term (2025-2030) |

| Competition from Traditional Banks & Large Tech Firms | -2.8% | North America, Europe | Mid-term (2026-2031) |

| Consumer Awareness & Trust Deficit | -2.0% | Emerging Markets | Long-term (2028-2033) |

| Scalability Challenges for Niche Lenders | -1.5% | Global | Mid-term (2026-2031) |

Alternative Lending Market Opportunities Analysis

The alternative lending market presents numerous opportunities for sustained expansion and innovation. A significant avenue lies in the vast underserved markets, including individuals with limited or no credit history and small businesses in developing economies that lack access to traditional credit. By leveraging alternative data points and mobile penetration, alternative lenders can tap into these segments, fostering financial inclusion and creating new revenue streams. This focus on financial empowerment not only addresses a critical societal need but also opens up substantial growth trajectories for market participants.

The increasing trend of embedded finance offers another lucrative opportunity. Integrating lending solutions directly into non-financial platforms, such as e-commerce sites, point-of-sale systems, or business management software, enables seamless access to credit at the moment of need. This strategy significantly reduces customer acquisition costs for lenders and enhances the convenience for borrowers, creating a more intuitive and less friction-filled borrowing experience. Partnerships with major tech companies and industry platforms can accelerate this integration, expanding reach and market penetration.

Furthermore, the diversification of alternative lending products beyond standard personal or business loans provides a fertile ground for innovation. Niche lending segments, such as revenue-based financing for SaaS companies, specialized financing for specific industries (e.g., healthcare, education), or green loans for sustainable projects, can cater to specific market demands. The adoption of advanced technologies like blockchain for transparency and efficiency, or hyper-personalization through AI, offers competitive advantages. Global expansion into new geographies, particularly in Asia Pacific and Latin America, where digital financial services are rapidly gaining traction, also represents a substantial growth opportunity for established players.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into Underserved & Emerging Markets | +4.7% | APAC, LATAM, MEA | Long-term (2028-2033) |

| Growth of Embedded Finance & BNPL Models | +4.0% | Global, particularly North America, Europe | Short to Mid-term (2025-2030) |

| Development of Niche Lending Products & Services | +3.5% | Global | Mid-term (2026-2031) |

| Leveraging Blockchain for Transparency & Efficiency | +2.8% | Global | Long-term (2028-2033) |

| Strategic Partnerships & Collaborations | +2.2% | Global | Short to Mid-term (2025-2030) |

| Data-Driven Personalization & Customer Experience | +1.8% | Global | Mid-term (2026-2031) |

Alternative Lending Market Challenges Impact Analysis

The alternative lending market, while promising, faces significant challenges that demand strategic responses from market participants. Managing credit risk, particularly with non-traditional borrowers, remains a paramount concern. Accurately assessing the creditworthiness of individuals or SMEs without extensive credit histories requires sophisticated analytical models and constant refinement. Economic downturns or unexpected market shocks can quickly exacerbate default rates, posing a substantial threat to the financial stability of alternative lenders and their investors, necessitating robust provisioning and diversified funding sources.

Regulatory compliance is another complex and evolving challenge. As the industry matures, regulators globally are introducing stricter rules regarding data privacy, consumer protection, anti-money laundering (AML), and fair lending practices. Navigating these diverse and often overlapping regulatory landscapes across different jurisdictions can be resource-intensive and expensive for alternative lenders, potentially slowing down innovation or increasing operational overheads. Non-compliance can lead to severe penalties, reputational damage, and loss of operating licenses, highlighting the critical importance of a proactive compliance strategy.

Furthermore, maintaining public trust and ensuring transparent operations are ongoing challenges. Incidents of predatory lending, data breaches, or algorithmic bias can quickly erode consumer confidence and attract negative media attention, impacting the entire sector. Customer acquisition costs can also be high in a crowded market, requiring significant investment in marketing and branding. Attracting and retaining top talent with expertise in both finance and cutting-edge technology is also a persistent hurdle, as competition for such skills remains fierce. These challenges underscore the need for continuous investment in technology, risk management, and ethical practices to ensure sustainable growth.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Managing High Credit Risk & Default Rates | -4.2% | Global | Short to Mid-term (2025-2030) |

| Navigating Complex & Evolving Regulatory Landscape | -3.8% | Global, particularly EU, US | Mid to Long-term (2026-2033) |

| Ensuring Data Privacy & Cybersecurity | -3.5% | Global | Short to Mid-term (2025-2030) |

| Building & Maintaining Consumer Trust | -2.9% | Global | Long-term (2028-2033) |

| High Customer Acquisition Costs | -2.4% | North America, Europe | Mid-term (2026-2031) |

| Talent Shortage in FinTech & AI Expertise | -1.9% | Global | Long-term (2028-2033) |

Alternative Lending Market - Updated Report Scope

This comprehensive report delves into the intricate dynamics of the global Alternative Lending market, providing an in-depth analysis of its current size, historical performance, and future growth projections from 2025 to 2033. It meticulously examines key market trends, significant drivers, formidable restraints, and emerging opportunities shaping the industry landscape. The report also highlights the profound impact of artificial intelligence and advanced technologies on market evolution, offering detailed segmentation analyses by type, end-use, and technology. Furthermore, it provides critical regional insights, identifying high-growth markets and the competitive strategies of leading players, thereby equipping stakeholders with actionable intelligence for strategic decision-making.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 475.2 Billion |

| Market Forecast in 2033 | USD 2.42 Trillion |

| Growth Rate | 23.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Funding Circle, Prosper, LendingClub, SoFi, Kabbage, Avant, Affirm, Upstart, Zopa, Ratesetter, Square Capital, Revolut, Chime, Klarna, Afterpay, Payoneer, Funding Societies, iwoca, LightSpeed, OnDeck |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Alternative Lending Market is broadly segmented based on the type of lending service, the end-use application, and the underlying technology platform utilized. This granular segmentation provides a comprehensive view of the market's diverse ecosystem, highlighting the various innovative models that cater to specific financial needs and technological advancements that enable these services. Each segment represents a unique value proposition, addressing different facets of the credit landscape and serving distinct borrower demographics.

The "By Type" segment showcases the various models of alternative financing that have emerged, each with its unique structure and target audience. "By End-Use" delineates the primary beneficiaries of these lending services, illustrating how alternative lending has permeated both consumer and business finance. Finally, the "By Technology" segment underscores the critical role of cutting-edge innovations in transforming traditional lending paradigms, driving efficiency, and enabling smarter credit decisions. Understanding these segments is crucial for identifying market niches and strategic growth opportunities within the dynamic alternative lending landscape.

- By Type:

- P2P Lending (Peer-to-Peer Lending)

- Crowdfunding

- Equity Crowdfunding

- Reward-Based Crowdfunding

- Donation-Based Crowdfunding

- Debt Crowdfunding

- Invoice Factoring

- Merchant Cash Advances

- Revenue-Based Financing

- Micro-lending

- Supply Chain Finance

- Equipment Financing

- By End-Use:

- Individuals

- Personal Loans

- Student Loans

- Mortgages

- Small & Medium Enterprises (SMEs)

- Large Enterprises

- Individuals

- By Technology:

- Artificial Intelligence (AI) & Machine Learning (ML)

- Blockchain

- Big Data Analytics

- Cloud Computing

- Application Programming Interfaces (APIs)

- By Platform:

- Online Platforms

- Mobile Applications

Regional Highlights

- North America: This region dominates the alternative lending market, driven by a mature FinTech ecosystem, high digital adoption rates, and a strong culture of innovation. The United States, in particular, leads in the adoption of P2P lending, merchant cash advances, and online personal loans, supported by significant venture capital investment and a receptive regulatory environment for financial innovation. Canada is also experiencing steady growth, focusing on SME financing and consumer credit.

- Europe: The European market is characterized by diverse regulatory approaches and a growing emphasis on financial inclusion and open banking initiatives (e.g., PSD2). The UK remains a key hub for alternative lending, particularly in P2P and crowdfunding. Countries like Germany, France, and the Netherlands are seeing increasing adoption, driven by strong SME sectors and a push towards digitalization in financial services. Cross-border lending opportunities are also emerging across the Eurozone.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing region, fueled by a massive unbanked and underbanked population, rapid smartphone penetration, and supportive government initiatives for FinTech. China, India, and Southeast Asian countries (e.g., Indonesia, Singapore) are witnessing exponential growth in micro-lending, mobile-first loan applications, and innovative payment solutions. The region's large SME sector further propels demand for alternative financing, making it a critical market for future expansion.

- Latin America: This region presents significant opportunities for financial inclusion, with a large portion of the population lacking access to traditional banking services. Mobile technology and digital payments are driving the adoption of alternative lending solutions, particularly in countries like Brazil, Mexico, and Argentina. The focus here is often on microfinance, personal loans, and financing for small businesses, leveraging alternative data for credit assessment.

- Middle East and Africa (MEA): The MEA market is still nascent but shows promising growth potential, driven by government diversification efforts, increasing digital literacy, and a young, tech-savvy population. Countries in the GCC (Gulf Cooperation Council) are investing heavily in FinTech infrastructure, while parts of Africa are experiencing a boom in mobile money and micro-lending, addressing critical financial gaps and fostering economic development.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Alternative Lending Market.- Funding Circle

- Prosper

- LendingClub

- SoFi

- Kabbage

- Avant

- Affirm

- Upstart

- Zopa

- Ratesetter

- Square Capital

- Revolut

- Chime

- Klarna

- Afterpay

- Payoneer

- Funding Societies

- iwoca

- LightSpeed

- OnDeck

Frequently Asked Questions

Analyze common user questions about the Alternative Lending market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is alternative lending?

Alternative lending refers to financial services provided by non-traditional lenders, offering credit solutions outside conventional banks. These include peer-to-peer lending, crowdfunding, invoice factoring, and merchant cash advances, often leveraging technology for faster, more flexible, and accessible financing.

How does alternative lending differ from traditional banking?

Alternative lending primarily differs from traditional banking in its use of technology, diversified funding sources, and often more flexible credit assessment models that leverage alternative data. This results in quicker loan approvals, simpler application processes, and greater accessibility for underserved individuals and small businesses compared to stringent traditional bank criteria.

What are the key advantages of alternative lending for borrowers?

For borrowers, the main advantages of alternative lending include faster access to funds, streamlined online application processes, more flexible eligibility criteria (often accepting lower credit scores or limited financial history), and tailored financial products that cater to specific needs, such as short-term business capital or unsecured personal loans.

What are the primary risks associated with alternative lending?

Key risks in alternative lending include potentially higher interest rates compared to traditional loans, less regulatory oversight leading to varying levels of consumer protection, increased vulnerability to economic downturns impacting repayment, and risks associated with data privacy and cybersecurity due to the reliance on digital platforms.

How is technology shaping the future of alternative lending?

Technology, particularly AI, machine learning, and big data analytics, is profoundly shaping alternative lending by enabling more accurate credit risk assessment, automating loan origination and servicing, enhancing fraud detection, and facilitating hyper-personalized loan products. This drives operational efficiency, reduces costs, and expands financial inclusion by reaching new segments of borrowers.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted