Aerospace and Defense Market

Aerospace and Defense Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705290 | Last Updated : August 11, 2025 |

Format : ![]()

![]()

![]()

![]()

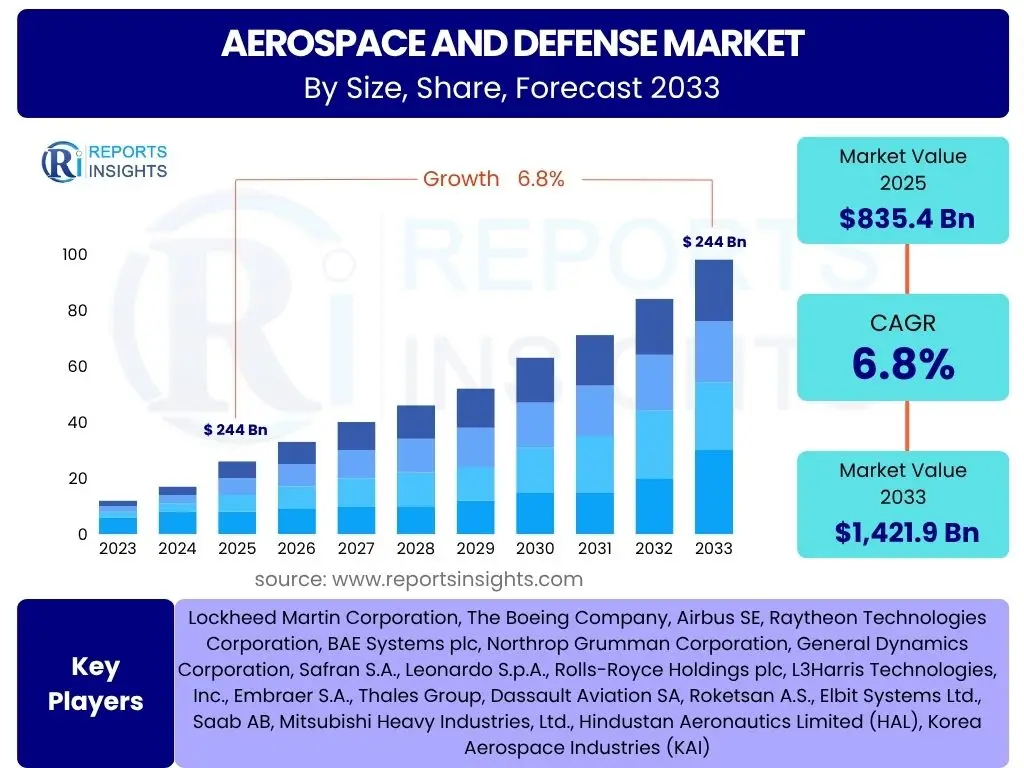

Aerospace and Defense Market Size

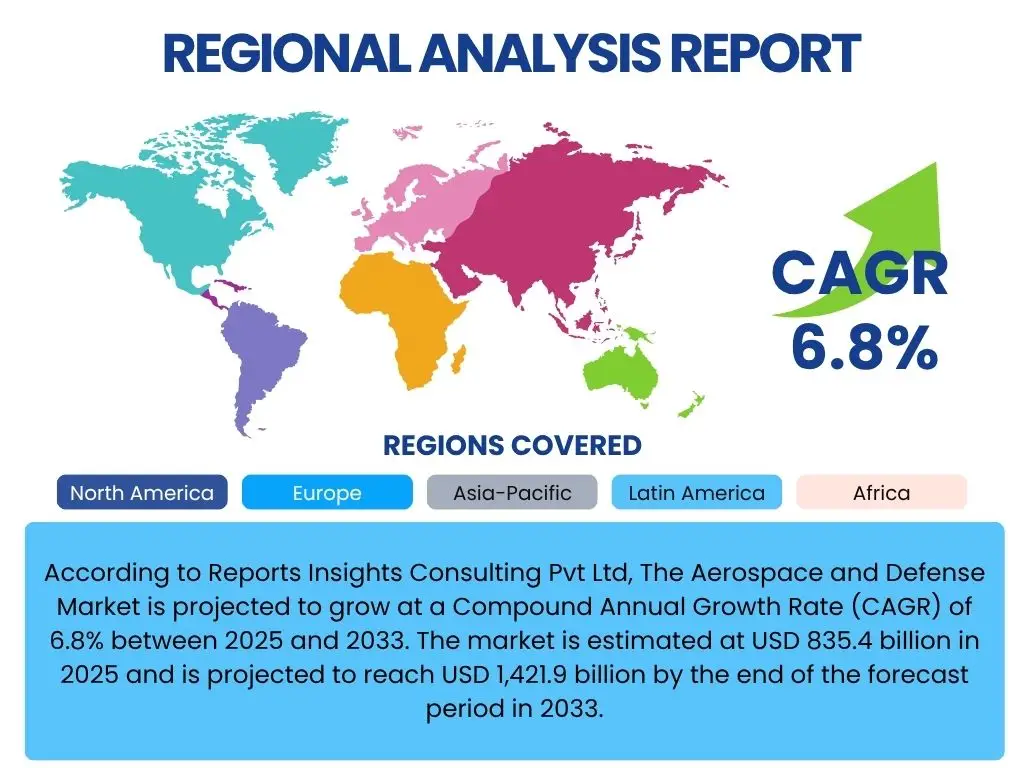

According to Reports Insights Consulting Pvt Ltd, The Aerospace and Defense Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 835.4 billion in 2025 and is projected to reach USD 1,421.9 billion by the end of the forecast period in 2033.

Key Aerospace and Defense Market Trends & Insights

The Aerospace and Defense (A&D) market is currently undergoing a transformative period, driven by a confluence of technological advancements, evolving geopolitical landscapes, and increasing demands for sustainability. Key user inquiries frequently center on understanding how digitalization, autonomous systems, and new material sciences are reshaping operational capabilities and defense strategies. Stakeholders are keen to identify the most impactful innovations and their potential for integration across various segments, from commercial aviation to military applications, emphasizing efficiency, safety, and performance enhancements.

Furthermore, there is significant interest in the long-term implications of these trends, particularly regarding supply chain resilience and the shift towards more sustainable manufacturing and operational practices. The increasing focus on reducing carbon footprints in commercial aerospace, coupled with the imperative for rapid technological iteration in defense, highlights a dual pressure on the industry. This necessitates continuous investment in research and development, alongside strategic partnerships to accelerate the adoption of cutting-edge solutions.

The geopolitical climate remains a dominant factor, influencing defense spending and the urgency for advanced surveillance, intelligence, and combat capabilities. Nations are prioritizing modernization programs, focusing on cyber defense, missile defense systems, and networked warfare, creating a robust demand for innovative A&D solutions. This translates into a competitive environment where companies must not only deliver superior technology but also demonstrate compliance with stringent regulatory frameworks and ethical considerations regarding defense applications.

- Digitalization and Industry 4.0 adoption across manufacturing and operations.

- Increased focus on sustainable aviation fuels (SAFs) and eco-friendly propulsion systems.

- Proliferation of unmanned aerial vehicles (UAVs) and autonomous systems.

- Enhanced cybersecurity measures and robust data protection protocols.

- Growing demand for advanced materials and additive manufacturing.

- Space commercialization and increased satellite deployment for communication and surveillance.

AI Impact Analysis on Aerospace and Defense

User questions regarding Artificial Intelligence's (AI) impact on the Aerospace and Defense sector frequently revolve around its practical applications in enhancing operational efficiency, decision-making, and autonomous capabilities. There is a strong interest in how AI can revolutionize areas such as predictive maintenance for aircraft, real-time data analysis for intelligence gathering, and the development of next-generation autonomous combat systems. Users are keen to understand the tangible benefits AI offers in reducing human error, optimizing resource allocation, and accelerating mission critical processes, while also considering the associated ethical and regulatory challenges.

The integration of AI is expected to significantly improve the accuracy and speed of threat detection, target recognition, and logistical planning in defense. In commercial aerospace, AI algorithms are being deployed for optimizing flight paths, managing air traffic control, and improving passenger experience through personalized services and predictive insights for maintenance. This widespread adoption underscores AI's role as a fundamental enabler for future innovation, moving beyond conceptual discussions to practical, deployable solutions that promise substantial improvements in safety, efficiency, and strategic advantage.

Furthermore, common inquiries often touch upon the cybersecurity implications of AI deployment, the need for robust AI governance frameworks, and the potential impact on workforce development. As AI systems become more sophisticated and interconnected, safeguarding them from malicious attacks and ensuring their ethical use becomes paramount. The industry is actively investing in AI talent and infrastructure to address these complex challenges, recognizing that the successful integration of AI is critical for maintaining a competitive edge and addressing the evolving demands of both commercial and military clients.

- Enhanced predictive maintenance and fault detection for aircraft and defense systems.

- Development of advanced autonomous navigation and operational capabilities for UAVs and combat vehicles.

- Improved data analytics for intelligence, surveillance, and reconnaissance (ISR) applications.

- Optimization of supply chain logistics and inventory management.

- Augmented human decision-making in complex operational environments.

- Advanced cybersecurity for critical infrastructure and defense networks.

Key Takeaways Aerospace and Defense Market Size & Forecast

Analysis of common user questions concerning the Aerospace and Defense market size and forecast consistently highlights themes of sustained growth, technological innovation as a primary driver, and the pervasive influence of global geopolitical dynamics. Users are primarily interested in understanding the resilience of this market amidst economic fluctuations and how ongoing advancements in areas like AI, hypersonics, and space technologies will contribute to its expansion. The forecast indicates a robust trajectory, suggesting that investment in cutting-edge capabilities and modernization programs will continue to be a priority for nations worldwide.

A significant takeaway is the dual-faceted nature of market growth, driven equally by commercial aerospace recovery and escalating defense expenditures. While commercial aviation rebounds from past disruptions with new aircraft orders and increased air travel, the defense sector is experiencing elevated spending due to persistent global instabilities and the need to upgrade existing military assets. This synergistic growth provides a stable foundation for the overall market, fostering continuous innovation across both segments, from advanced manufacturing processes to highly sophisticated digital systems.

Moreover, the market's future is inextricably linked to the industry's ability to adapt to new challenges, including supply chain vulnerabilities, environmental sustainability mandates, and the demand for a skilled workforce. The long-term forecast underscores a strategic imperative for companies to invest in resilient supply chains, embrace green technologies, and foster talent development to navigate these complexities effectively. Success in the Aerospace and Defense market will depend not only on technological superiority but also on operational agility and a commitment to responsible industrial practices, ensuring enduring growth and market leadership.

- The market is poised for significant growth, driven by both commercial recovery and defense modernization.

- Technological advancements, particularly in AI, autonomy, and advanced materials, are key growth enablers.

- Geopolitical tensions and national security priorities will continue to fuel defense spending.

- Sustainability initiatives, including SAFs and electric propulsion, are increasingly influencing commercial aerospace.

- Supply chain resilience and digital transformation are critical for future market stability and efficiency.

Aerospace and Defense Market Drivers Analysis

The Aerospace and Defense market is propelled by a multitude of factors that collectively foster its expansion and innovation. A primary driver is the escalating global geopolitical instability, which compels nations to invest heavily in modernizing their defense capabilities and enhancing national security infrastructure. This heightened focus on defense readiness directly translates into increased procurement of advanced aircraft, missile systems, naval vessels, and sophisticated surveillance technologies, thereby fueling market growth across various defense segments.

Another significant driver stems from the resurgence and continued growth in commercial aviation. The global demand for air travel, particularly in emerging economies, drives new aircraft orders, fleet expansions, and ongoing maintenance, repair, and overhaul (MRO) activities. As air passenger traffic recovers and surpasses pre-pandemic levels, airlines are investing in fuel-efficient and technologically advanced aircraft, which creates a sustained demand for components, systems, and services within the commercial aerospace sector, stimulating research and development in areas like sustainable aviation and advanced avionics.

Furthermore, rapid technological advancements, including artificial intelligence, autonomous systems, advanced materials, and satellite communication, act as powerful catalysts for market development. These innovations are not only enhancing the performance and efficiency of existing platforms but also enabling the creation of entirely new capabilities, such as advanced reconnaissance drones, networked combat systems, and more efficient propulsion technologies. The imperative to maintain a technological edge drives significant research and development investments, contributing substantially to the market's dynamic growth and fostering a competitive landscape where innovation is key to market leadership and strategic advantage.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Geopolitical Tensions & Conflicts | +1.5-2.0% | Global, particularly Europe, Asia Pacific, Middle East | Short- to Mid-Term (2025-2030) |

| Modernization of Military Fleets & Defense Spending | +1.0-1.5% | North America, Europe, Asia Pacific | Mid- to Long-Term (2026-2033) |

| Growth in Commercial Air Travel & Freight | +0.8-1.2% | Global, especially Asia Pacific, North America | Mid- to Long-Term (2027-2033) |

| Technological Advancements (AI, Hypersonics, Space) | +0.7-1.0% | Global | Continuous, Short- to Long-Term |

| Expansion of Space Exploration & Satellite Deployment | +0.5-0.8% | North America, Europe, Asia Pacific | Mid-Term (2026-2031) |

Aerospace and Defense Market Restraints Analysis

Despite robust growth prospects, the Aerospace and Defense market faces several significant restraints that can temper its expansion. One prominent challenge is the persistent issue of budgetary constraints and fiscal austerity measures adopted by various governments. While defense spending may increase in certain regions due to geopolitical tensions, other nations or sectors within the A&D industry might experience reduced allocations, impacting procurement plans, research funding, and the overall pace of modernization. This fiscal unpredictability often leads to delays in contracts and a more cautious approach to new investments, directly influencing market volume.

Supply chain disruptions represent another critical restraint, particularly evident in recent years. The global A&D supply chain is highly complex, reliant on a vast network of specialized manufacturers and suppliers for intricate components, raw materials, and advanced technologies. Geopolitical events, pandemics, trade disputes, and natural disasters can severely disrupt this delicate balance, leading to production delays, increased costs, and challenges in meeting delivery schedules. The intricate nature of these supply chains means even minor disruptions can have cascading effects, impeding the smooth flow of production and potentially limiting market growth.

Furthermore, stringent regulatory frameworks and lengthy certification processes impose considerable burdens on market players. The A&D sector is one of the most heavily regulated industries, with rigorous standards for safety, environmental compliance, and national security. While necessary, these regulations often involve extensive testing, documentation, and approval cycles that can significantly delay product launches and market entry for new technologies or systems. The high cost of compliance and the time required to navigate these regulatory landscapes can deter innovation and increase operational expenses, acting as a notable restraint on the market's potential for rapid development and commercialization.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Government Budgetary Constraints & Fiscal Austerity | -0.8-1.2% | Global, varies by national economic health | Short- to Mid-Term (2025-2028) |

| Supply Chain Disruptions & Material Shortages | -0.7-1.0% | Global, interconnected | Short- to Mid-Term (2025-2027) |

| Stringent Regulatory & Certification Processes | -0.6-0.9% | Global, particularly North America, Europe | Long-Term (Ongoing) |

| Environmental Regulations & Sustainability Pressures | -0.5-0.7% | Global, particularly Europe, North America | Mid- to Long-Term (2027-2033) |

| Skilled Labor Shortages & Talent Acquisition Challenges | -0.4-0.6% | Global, particularly developed economies | Long-Term (Ongoing) |

Aerospace and Defense Market Opportunities Analysis

The Aerospace and Defense market is ripe with opportunities driven by technological innovation and evolving global demands. One significant area of opportunity lies in the burgeoning market for unmanned systems, including advanced drones, autonomous vehicles, and robotic platforms for both military and commercial applications. As these technologies mature, their capabilities extend beyond surveillance to include logistics, combat roles, and even urban air mobility, opening up vast new avenues for development, manufacturing, and service provision. The increasing adoption across diverse sectors, from agriculture to defense, ensures sustained investment and market expansion for companies specializing in these advanced systems.

Another substantial opportunity emerges from the growing emphasis on sustainable aviation solutions. With increasing environmental concerns and stricter emission regulations, there is immense pressure and incentive for the industry to innovate in areas such as Sustainable Aviation Fuels (SAFs), electric and hybrid-electric propulsion systems, and more efficient aerodynamic designs. This paradigm shift not only addresses environmental responsibilities but also creates new market segments for clean technologies, attracting investments and partnerships focused on developing the next generation of eco-friendly aircraft and operational practices. Companies at the forefront of this transition stand to gain significant market share and competitive advantage.

Furthermore, the digitalization of the aerospace and defense ecosystem presents a transformative opportunity. The widespread adoption of Industry 4.0 technologies—such as Artificial Intelligence, Big Data analytics, cloud computing, and the Internet of Things (IoT)—enables enhanced operational efficiency, predictive maintenance, and cybersecurity. Companies offering digital solutions, from advanced simulation software to secure data management platforms, can capitalize on the industry's drive towards smart manufacturing, networked defense systems, and optimized asset performance. This digital transformation provides a pathway for companies to offer value-added services, streamline processes, and create more resilient and responsive defense and commercial aerospace operations, unlocking new revenue streams and fostering a more integrated value chain.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion of Unmanned Systems & Autonomous Technologies | +1.0-1.5% | Global, particularly North America, Asia Pacific, Europe | Mid- to Long-Term (2026-2033) |

| Development & Adoption of Sustainable Aviation Solutions | +0.8-1.2% | Global, particularly Europe, North America | Mid- to Long-Term (2027-2033) |

| Digital Transformation & Cybersecurity Integration | +0.7-1.0% | Global | Continuous, Short- to Long-Term |

| Growth in Commercial Space & Satellite Services | +0.6-0.9% | North America, Europe, Asia Pacific | Mid-Term (2026-2031) |

| Increasing Demand for MRO (Maintenance, Repair, Overhaul) Services | +0.5-0.8% | Global | Continuous, Long-Term |

Aerospace and Defense Market Challenges Impact Analysis

The Aerospace and Defense market, while experiencing significant growth, is not without its formidable challenges that can impede progress and profitability. One major challenge is the inherent long product development cycles and high research and development costs associated with aerospace and defense technologies. Developing new aircraft, complex weapon systems, or advanced propulsion technologies requires enormous capital investment over many years, often before any return on investment is realized. This lengthy timeline and financial burden can be a barrier to entry for new players and place significant strain on established companies, particularly when unforeseen technical hurdles or regulatory changes arise.

Another critical challenge stems from the increasing complexity of cybersecurity threats and intellectual property theft. As defense systems and commercial aircraft become more interconnected and reliant on digital technologies, they become increasingly vulnerable to sophisticated cyberattacks from state-sponsored actors, criminal organizations, or rogue elements. Protecting sensitive design specifications, operational data, and mission-critical systems is paramount, yet the evolving nature of these threats requires constant vigilance and significant investment in cybersecurity infrastructure and expertise. The potential for IP theft also poses a substantial risk, compromising competitive advantage and national security.

Furthermore, the Aerospace and Defense industry faces significant challenges related to talent acquisition and retention. The demand for highly specialized engineers, scientists, skilled technicians, and cybersecurity experts far outstrips the available supply. The aging workforce, coupled with a perceived decline in interest in STEM fields among younger generations in some regions, exacerbates this issue. This talent gap can lead to delays in innovation, increased labor costs, and difficulties in scaling production, posing a long-term threat to the industry's capacity for growth and its ability to maintain technological leadership in a rapidly evolving global landscape.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Long Product Development Cycles & High R&D Costs | -0.7-1.0% | Global | Long-Term (Ongoing) |

| Increasing Cybersecurity Threats & IP Theft | -0.6-0.9% | Global, particularly technologically advanced regions | Continuous, Short- to Long-Term |

| Talent Shortages & Workforce Development | -0.5-0.8% | Global, particularly developed economies | Long-Term (Ongoing) |

| Supply Chain Resilience & Geopolitical Dependencies | -0.4-0.7% | Global, interconnected | Short- to Mid-Term (2025-2028) |

| Navigating Complex International Trade Regulations | -0.3-0.5% | Global, especially regions with strict export controls | Continuous, Long-Term |

Aerospace and Defense Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the Aerospace and Defense market, detailing its current size, historical trends, and future growth projections from 2025 to 2033. It examines the critical drivers, restraints, opportunities, and challenges shaping the industry landscape, offering strategic insights for stakeholders. The scope encompasses detailed segmentation analysis by various factors, comprehensive regional breakdowns, and profiles of key market players, delivering a holistic view necessary for informed decision-making and strategic planning within this dynamic sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 835.4 billion |

| Market Forecast in 2033 | USD 1,421.9 billion |

| Growth Rate | 6.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Lockheed Martin Corporation, The Boeing Company, Airbus SE, Raytheon Technologies Corporation, BAE Systems plc, Northrop Grumman Corporation, General Dynamics Corporation, Safran S.A., Leonardo S.p.A., Rolls-Royce Holdings plc, L3Harris Technologies, Inc., Embraer S.A., Thales Group, Dassault Aviation SA, Roketsan A.S., Elbit Systems Ltd., Saab AB, Mitsubishi Heavy Industries, Ltd., Hindustan Aeronautics Limited (HAL), Korea Aerospace Industries (KAI) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Aerospace and Defense market is extensively segmented to provide a granular understanding of its diverse components and applications, enabling precise market analysis and strategic targeting. These segmentations allow for a detailed examination of demand drivers, technological shifts, and competitive landscapes across specific product types, end-use sectors, and operational domains. Such a segmented approach is crucial for identifying niche opportunities, understanding value chain dynamics, and developing tailored market strategies that resonate with distinct customer needs in both commercial and military spheres.

Further granularity within these segments reveals varying growth rates and adoption patterns. For instance, within commercial aviation, passenger aircraft and cargo aircraft exhibit different trajectories influenced by air travel demand and global trade volumes, respectively. Similarly, military aviation segments, like combat aircraft versus transport aircraft, respond to distinct national defense priorities and modernization cycles. The detailed breakdown extends to components and end-use, providing insights into the supply side and the aftermarket services, which are critical for the long-term sustainability and operational readiness of aerospace and defense assets globally.

- By Application: The market is segmented into Commercial Aviation, Military Aviation, Space, Naval, and Land & Missile Defense, reflecting the core operational areas.

- By Component: Key components analyzed include Aerostructures, Avionics, Engines, Landing Gear, Hydraulics, Electrical Systems, Actuators, Communication Systems, Navigation Systems, Weapon Systems, and Propulsion Systems, highlighting the technological building blocks.

- By Type: Segmentation by Fixed-Wing Aircraft, Rotary-Wing Aircraft, Unmanned Systems, Spacecraft, Weapon Systems, and Vehicles & Equipment categorizes platforms based on their design and function.

- By End-Use: The market is divided into OEM (Original Equipment Manufacturer) and Aftermarket (Maintenance, Repair, Overhaul), differentiating between new sales and ongoing support services.

Regional Highlights

The global Aerospace and Defense market exhibits significant regional variations in terms of size, growth drivers, and strategic importance, primarily influenced by geopolitical dynamics, economic development, and technological advancements. North America, particularly the United States, holds a dominant position due to its substantial defense budget, robust technological infrastructure, and the presence of leading aerospace and defense manufacturers. The region is a hub for innovation in AI, autonomous systems, and advanced materials, driving both military modernization and commercial aerospace advancements. The ongoing investment in next-generation aircraft, space technologies, and cybersecurity solutions underscores its continued leadership.

Asia Pacific is projected to be the fastest-growing region, driven by increasing defense expenditures from countries like China and India, coupled with rapid urbanization and a surging demand for commercial air travel. This region is witnessing significant investment in domestic defense manufacturing capabilities, fleet modernization, and the expansion of commercial airline fleets to cater to growing passenger traffic. Europe, while a mature market, remains a critical player with strong R&D capabilities, particularly in sustainable aviation and collaborative defense programs. Countries such as France, the UK, and Germany are leaders in both commercial aircraft manufacturing and sophisticated defense systems. Latin America, the Middle East, and Africa (MEA) are emerging markets, characterized by increasing demand for defense equipment due to regional conflicts and a growing need for air connectivity, prompting investments in both military and civil aviation infrastructure and procurement.

- North America: Dominant market share due to high defense spending, advanced R&D, and major industry players (U.S., Canada).

- Europe: Significant market driven by defense modernization, collaborative projects, and strong commercial aerospace manufacturing base (UK, France, Germany, Italy).

- Asia Pacific (APAC): Fastest-growing region, fueled by rising defense budgets, increasing commercial air travel demand, and domestic manufacturing capabilities (China, India, Japan, South Korea).

- Latin America: Emerging market with growing demand for military upgrades and commercial aircraft fleet expansion (Brazil, Mexico).

- Middle East and Africa (MEA): Increased defense spending driven by regional instabilities and investments in civil aviation infrastructure (UAE, Saudi Arabia, South Africa).

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Aerospace and Defense Market.- Lockheed Martin Corporation

- The Boeing Company

- Airbus SE

- Raytheon Technologies Corporation

- BAE Systems plc

- Northrop Grumman Corporation

- General Dynamics Corporation

- Safran S.A.

- Leonardo S.p.A.

- Rolls-Royce Holdings plc

- L3Harris Technologies, Inc.

- Embraer S.A.

- Thales Group

- Dassault Aviation SA

- Roketsan A.S.

- Elbit Systems Ltd.

- Saab AB

- Mitsubishi Heavy Industries, Ltd.

- Hindustan Aeronautics Limited (HAL)

- Korea Aerospace Industries (KAI)

Frequently Asked Questions

Analyze common user questions about the Aerospace and Defense market and generate a concise list of summarized FAQs reflecting key topics and concerns.What are the primary drivers of growth in the Aerospace and Defense market?

The primary drivers include escalating global geopolitical tensions, necessitating increased defense spending and military modernization programs worldwide. Simultaneously, the robust recovery and sustained growth in commercial air travel demand lead to significant new aircraft orders and fleet expansions. Furthermore, continuous technological advancements, particularly in areas such as artificial intelligence, autonomous systems, advanced materials, and space exploration, fuel innovation and enhance capabilities across both commercial and military sectors, thereby propelling market expansion and fostering strategic investments in cutting-edge solutions.

How is Artificial Intelligence (AI) impacting the Aerospace and Defense industry?

AI is profoundly impacting the Aerospace and Defense industry by enhancing operational efficiency, decision-making, and autonomous capabilities. In defense, AI enables advanced intelligence, surveillance, and reconnaissance (ISR), predictive maintenance for critical systems, and the development of next-generation autonomous combat vehicles. For commercial aerospace, AI optimizes flight paths, manages air traffic control, and improves maintenance schedules, leading to reduced costs and increased safety. AI integration also strengthens cybersecurity, automating threat detection and response, although it also introduces new ethical considerations and a demand for specialized AI talent within the sector.

What are the main challenges faced by the Aerospace and Defense market?

The Aerospace and Defense market confronts several significant challenges, including long product development cycles and exceptionally high research and development costs, which demand substantial capital investment and time before realizing returns. The industry also grapples with the escalating complexity of cybersecurity threats and the constant risk of intellectual property theft, necessitating continuous and significant investment in robust defense mechanisms. Moreover, a persistent shortage of skilled labor, particularly specialized engineers and technicians, poses a long-term challenge to innovation, production capacity, and overall growth within the sector.

Which regions are leading the Aerospace and Defense market, and why?

North America, primarily driven by the United States, leads the Aerospace and Defense market due to its substantial defense budget, extensive research and development investments, and the presence of numerous global aerospace and defense giants. This region is at the forefront of technological innovation and military modernization. Asia Pacific is the fastest-growing region, fueled by increasing defense expenditures from emerging economies like China and India, coupled with rapid growth in commercial aviation demand. Europe also maintains a significant market presence, particularly through advanced manufacturing capabilities and collaborative defense programs, consistently contributing to global market trends.

What are the key trends shaping the future of commercial aviation?

The future of commercial aviation is being shaped by several transformative trends. A primary focus is on sustainability, with increasing adoption of Sustainable Aviation Fuels (SAFs) and accelerated development of electric and hybrid-electric propulsion systems to reduce carbon emissions. Digitalization and automation are also paramount, optimizing flight operations, enhancing air traffic management, and improving passenger experiences through advanced analytics and connectivity. Furthermore, the development of urban air mobility (UAM) and advanced air mobility (AAM) concepts, alongside the continuous innovation in lightweight materials and aerodynamic designs, are poised to redefine air travel efficiency and accessibility in the coming years.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted