Advanced Packaging Market

Advanced Packaging Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701322 | Last Updated : July 29, 2025 |

Format : ![]()

![]()

![]()

![]()

Advanced Packaging Market Size

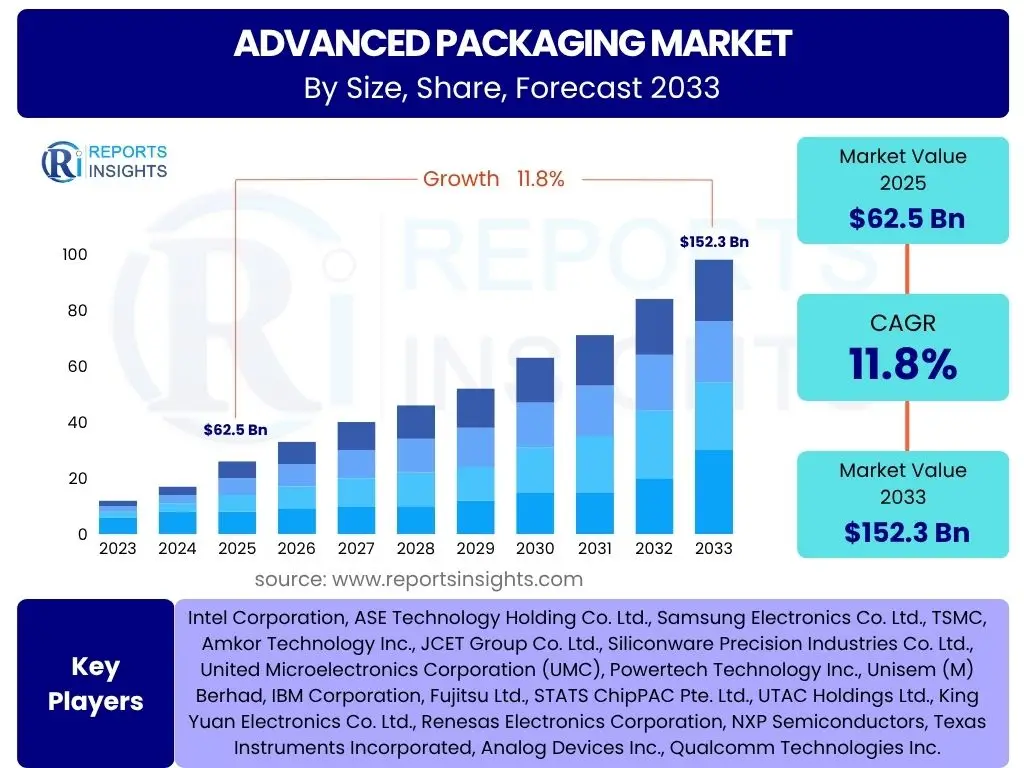

According to Reports Insights Consulting Pvt Ltd, The Advanced Packaging Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 11.8% between 2025 and 2033. The market is estimated at USD 62.5 billion in 2025 and is projected to reach USD 152.3 billion by the end of the forecast period in 2033.

Key Advanced Packaging Market Trends & Insights

The Advanced Packaging market is experiencing transformative shifts driven by the escalating demand for high-performance, compact, and energy-efficient electronic devices. Users frequently inquire about the underlying forces shaping this evolution. A primary trend involves the widespread adoption of heterogeneous integration, which allows for the combination of disparate semiconductor components into a single package, enabling enhanced functionality and performance beyond what monolithic integration can achieve. This approach is critical for supporting the complex requirements of artificial intelligence, high-performance computing (HPC), and 5G communication.

Another significant trend is the continuous push for miniaturization and increased interconnect density. This is propelling the development of advanced packaging technologies such as 2.5D/3D ICs, fan-out wafer-level packaging (FOWLP), and system-in-package (SiP) solutions. These technologies address the limitations of traditional packaging methods by offering improved electrical performance, reduced form factors, and better thermal management. Furthermore, the automotive sector's rapid embrace of advanced driver-assistance systems (ADAS) and autonomous driving, alongside the proliferation of Internet of Things (IoT) devices, is fueling specific demands for robust, reliable, and cost-effective advanced packaging solutions capable of operating in harsh environments.

Sustainability and supply chain resilience are also emerging as crucial considerations. The industry is exploring greener materials and more energy-efficient manufacturing processes to reduce its environmental footprint. Simultaneously, geopolitical factors and recent global events have highlighted the importance of diversifying supply chains and investing in localized manufacturing capabilities, influencing investment patterns and strategic partnerships within the advanced packaging ecosystem.

- Heterogeneous integration for enhanced functionality and performance.

- Miniaturization and increased interconnect density driven by 2.5D/3D ICs and FOWLP.

- Rising adoption in automotive (ADAS, autonomous driving) and IoT sectors.

- Emphasis on sustainable materials and energy-efficient manufacturing processes.

- Strategic focus on supply chain diversification and regional manufacturing resilience.

AI Impact Analysis on Advanced Packaging

The integration of artificial intelligence (AI) profoundly impacts the Advanced Packaging sector, a common area of user inquiry focusing on how AI influences design, manufacturing, and demand. AI's primary influence stems from its role as both a driver of demand for advanced packaging and a tool for optimizing its development. The exponential growth of AI applications, from cloud-based AI training to edge AI inference, necessitates semiconductor devices with unprecedented levels of processing power, memory bandwidth, and low latency. This directly translates into a critical need for advanced packaging solutions that can efficiently integrate multiple high-performance chips, manage significant power consumption, and dissipate intense heat generated by AI accelerators.

Beyond demand generation, AI is revolutionizing the design and manufacturing processes of advanced packaging. AI-driven simulation and optimization tools are being employed to accelerate the design cycle for complex 2.5D/3D packages, predicting performance characteristics, thermal behavior, and potential yield issues with greater accuracy than traditional methods. Machine learning algorithms are also enhancing manufacturing efficiency by enabling predictive maintenance for packaging equipment, optimizing process parameters in real-time to reduce defects, and improving overall yield rates. This data-driven approach allows manufacturers to achieve higher precision and consistency in intricate packaging operations, crucial for advanced designs.

Furthermore, AI facilitates new material discovery and characterization, identifying novel substrates and interconnect materials that can withstand the extreme conditions of advanced packaging while offering improved electrical and thermal properties. The continuous feedback loop between AI applications requiring higher performance and AI tools optimizing packaging techniques creates a virtuous cycle, driving innovation and pushing the boundaries of what is possible in semiconductor integration. As AI models become more complex and pervasive, their reliance on sophisticated packaging will only intensify, solidifying AI's foundational role in the future of the advanced packaging market.

- Increased demand for high-performance, integrated chips for AI workloads.

- AI-driven optimization of packaging design, simulation, and validation processes.

- Machine learning for enhanced manufacturing efficiency, predictive maintenance, and yield improvement.

- AI-assisted discovery and characterization of advanced packaging materials.

- Acceleration of heterogeneous integration and 3D stacking techniques to meet AI power and performance demands.

Key Takeaways Advanced Packaging Market Size & Forecast

Users frequently seek clear insights into the core implications of the Advanced Packaging market's projected growth and overall trajectory. A key takeaway is the significant expansion anticipated in this sector, primarily driven by the insatiable demand for computing power across diverse applications. The projected double-digit CAGR underscores the critical role advanced packaging plays in overcoming traditional scaling limitations, enabling the next generation of electronic devices. This growth is not uniform across all technologies, with specific innovations like 2.5D/3D packaging and fan-out solutions experiencing accelerated adoption due to their ability to deliver superior performance and integration density.

Another crucial insight is the strategic importance of this market in the broader semiconductor ecosystem. Advanced packaging is no longer merely an assembly process but a key differentiator, enabling new product functionalities and performance benchmarks. Companies investing heavily in R&D for advanced packaging technologies are positioning themselves for leadership, as the ability to efficiently integrate disparate dies and manage complex thermal challenges becomes paramount. The market's robust growth also signals sustained capital expenditure in advanced manufacturing facilities and equipment, driven by increasing foundry and OSAT (Outsourced Semiconductor Assembly and Test) capabilities.

Finally, the market forecast highlights the increasing geopolitical and economic focus on semiconductor manufacturing capabilities. As advanced packaging becomes more vital, countries and regions are prioritizing investments to secure their positions in the global supply chain, fostering innovation and talent development. This emphasis on domestic capacity building and technological self-reliance will likely shape the competitive landscape, leading to further diversification of manufacturing hubs and a focus on resilient supply networks to support the continued expansion of high-end electronics.

- The Advanced Packaging market is set for substantial growth, driven by escalating demands for high-performance computing.

- Specific technologies like 2.5D/3D and fan-out packaging are critical growth engines due to superior integration and performance.

- Advanced packaging is a strategic differentiator, essential for next-generation electronic device functionality.

- Significant capital expenditure in R&D and manufacturing capacity is expected to continue.

- Geopolitical focus on semiconductor self-reliance will drive regional investments and supply chain diversification.

Advanced Packaging Market Drivers Analysis

The Advanced Packaging market's expansion is fundamentally propelled by several interconnected factors that create a persistent demand for innovative integration solutions. The pervasive drive towards device miniaturization across consumer electronics, medical devices, and industrial applications necessitates packaging technologies that can house more functionality in smaller footprints. Simultaneously, the ever-increasing need for higher performance in computing, driven by artificial intelligence, machine learning, and data centers, demands solutions that improve signal integrity, reduce power consumption, and enhance thermal dissipation beyond what traditional packaging can offer. These twin pressures for smaller size and greater capability are the primary catalysts for advanced packaging adoption.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for High-Performance Computing (HPC) and AI | +3.5% | Global, particularly North America, Asia Pacific (Taiwan, South Korea) | Short-term to Long-term |

| Miniaturization and Integration Trends in Consumer Electronics | +2.8% | Asia Pacific (China, Japan), North America, Europe | Mid-term to Long-term |

| Proliferation of 5G Technology and Internet of Things (IoT) Devices | +2.5% | Global, especially China, North America, Europe | Short-term to Mid-term |

| Growth in Automotive Electronics (ADAS, Electric Vehicles) | +1.8% | Europe, North America, Asia Pacific (Japan, South Korea) | Mid-term to Long-term |

| Adoption of Heterogeneous Integration Technologies | +1.2% | Global, focused on leading semiconductor hubs | Short-term to Mid-term |

Advanced Packaging Market Restraints Analysis

Despite robust growth, the Advanced Packaging market faces several significant restraints that can impede its full potential. The inherent complexity of advanced packaging processes, such as 3D stacking and chiplet integration, leads to higher manufacturing costs and extended development cycles compared to conventional packaging. This high capital expenditure for advanced equipment, coupled with the need for highly specialized technical expertise, can act as a barrier to entry for new players and limit the widespread adoption of the most cutting-edge solutions, particularly for smaller volume applications or markets sensitive to cost.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Manufacturing Costs and Capital Expenditure | -2.0% | Global, impacts emerging economies more | Short-term to Mid-term |

| Complexity of Advanced Packaging Processes and Yield Challenges | -1.5% | Global, particularly new technology adopters | Short-term |

| Lack of Standardization Across Different Packaging Technologies | -1.0% | Global | Mid-term |

| Intellectual Property (IP) and Supply Chain Vulnerabilities | -0.8% | Global, impacts regions with geopolitical tensions | Mid-term to Long-term |

| Skilled Workforce Shortage | -0.7% | North America, Europe, parts of Asia Pacific | Short-term to Mid-term |

Advanced Packaging Market Opportunities Analysis

The Advanced Packaging market is ripe with opportunities driven by technological convergence and emerging application areas. The continuous evolution of AI and quantum computing presents a vast untapped potential for highly integrated and specialized packaging solutions that can handle extreme processing demands and unique operational environments. Furthermore, the expansion of the automotive sector, especially with the rapid adoption of electric vehicles (EVs) and sophisticated in-car electronics, creates new avenues for robust, reliable, and thermally efficient packaging solutions designed for demanding conditions and long lifecycles. These sectors require unprecedented levels of integration and performance, directly aligning with advanced packaging capabilities.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of New Computing Paradigms (AI, Quantum Computing) | +2.0% | Global, particularly North America, Europe, Asia Pacific (leading research hubs) | Mid-term to Long-term |

| Increasing Applications in Automotive, Medical, and Industrial Sectors | +1.8% | Europe, North America, Asia Pacific | Short-term to Mid-term |

| Development of Advanced Materials and Manufacturing Techniques | +1.5% | Global | Short-term to Long-term |

| Rise of Chiplet Architectures and Modular Design | +1.2% | Global, focused on leading semiconductor designers/foundries | Short-term to Mid-term |

| Investments in Domestic Semiconductor Manufacturing Capabilities | +1.0% | North America, Europe, Japan, India | Mid-term to Long-term |

Advanced Packaging Market Challenges Impact Analysis

The Advanced Packaging market faces several significant challenges that necessitate ongoing innovation and strategic adaptation. One primary challenge is the escalating complexity of designing and manufacturing packages that integrate multiple dies with incredibly fine pitches and high interconnect densities. This complexity leads to difficulties in ensuring high yield rates and robust reliability, particularly as thermal management and power delivery become more critical concerns for high-performance applications. The intricate nature of these processes requires continuous investment in advanced simulation tools and sophisticated manufacturing equipment, contributing to higher operational costs and a longer time to market for new solutions.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Thermal Management and Power Delivery for High-Performance Chips | -1.8% | Global, especially for HPC and AI applications | Short-term to Mid-term |

| Maintaining High Yield Rates for Complex 3D and Heterogeneous Integration | -1.5% | Global, impacts new technology adoption | Short-term |

| Escalating R&D Costs and Extended Development Cycles | -1.2% | Global, particularly for smaller players | Mid-term |

| Geopolitical Tensions and Supply Chain Disruptions | -1.0% | Global, impacts regions with high dependency | Short-term to Mid-term |

| Lack of Interoperability Standards Across Different Vendor Solutions | -0.8% | Global | Mid-term to Long-term |

Advanced Packaging Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Advanced Packaging market, covering historical data, current market dynamics, and future projections. It delves into various packaging technologies, applications, and end-user industries, offering a granular view of market segmentation and regional performance. The report includes detailed profiles of key market players, competitive landscape analysis, and an assessment of market drivers, restraints, opportunities, and challenges, providing a holistic understanding of the market's trajectory and strategic insights for stakeholders. The analysis incorporates the impact of emerging technologies and evolving industry trends on market growth and evolution.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 62.5 billion |

| Market Forecast in 2033 | USD 152.3 billion |

| Growth Rate | 11.8% CAGR |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Intel Corporation, ASE Technology Holding Co. Ltd., Samsung Electronics Co. Ltd., TSMC, Amkor Technology Inc., JCET Group Co. Ltd., Siliconware Precision Industries Co. Ltd., United Microelectronics Corporation (UMC), Powertech Technology Inc., Unisem (M) Berhad, IBM Corporation, Fujitsu Ltd., STATS ChipPAC Pte. Ltd., UTAC Holdings Ltd., King Yuan Electronics Co. Ltd., Renesas Electronics Corporation, NXP Semiconductors, Texas Instruments Incorporated, Analog Devices Inc., Qualcomm Technologies Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Advanced Packaging market is extensively segmented by packaging type, application, end-user, and process technology to provide a detailed and granular understanding of its diverse facets. This segmentation allows for precise analysis of market dynamics, growth drivers, and opportunities within specific niches. By examining each segment, stakeholders can identify high-growth areas, understand competitive landscapes, and tailor their strategies to specific market demands. The varied technological approaches within packaging types reflect the industry's response to different performance, cost, and form factor requirements across myriad electronic applications.

- By Packaging Type: This segment includes Flip-Chip CSP, Flip-Chip BGA, Wafer Level CSP, 3D TSV, 2.5D/3D IC, Fan-Out WLP, and System-in-Package (SiP). Each type offers distinct advantages in terms of integration density, electrical performance, and thermal management, catering to specific application needs.

- By Application: Key applications include Consumer Electronics (smartphones, wearables), Automotive (ADAS, infotainment), Healthcare (medical devices), Industrial (automation, robotics), IT & Telecommunication (data centers, networking equipment), and Aerospace & Defense. These sectors drive demand for robust and high-performance packaging.

- By End-User: The market participants are categorized into Foundries (fabricating wafers), IDMs (Integrated Device Manufacturers, handling design to packaging), and OSAT (Outsourced Semiconductor Assembly and Test) companies, reflecting the complex supply chain structure.

- By Process Technology: This covers the materials and processes involved, such as Dielectric Materials, Substrates, Bonding Wires, Leadframes, Ceramic Packages, and Organic Substrates, which are crucial for the performance and reliability of advanced packages.

Regional Highlights

- Asia Pacific (APAC): Dominates the Advanced Packaging market, driven by its robust semiconductor manufacturing ecosystem, including major foundries and OSAT providers in Taiwan, South Korea, China, and Japan. The region benefits from high demand for consumer electronics, automotive components, and significant government investments in semiconductor R&D and manufacturing. China's growing domestic demand for high-performance computing and 5G infrastructure further fuels this growth, making APAC the primary hub for advanced packaging innovation and production.

- North America: A significant market player, characterized by strong demand from high-performance computing, artificial intelligence, and aerospace & defense sectors. The region is home to leading semiconductor design companies and is investing heavily in reshoring manufacturing capabilities and R&D for cutting-edge packaging technologies, particularly in areas like 3D integration and chiplet architectures. Innovation in materials science and advanced manufacturing techniques is a key driver.

- Europe: Exhibits steady growth, primarily fueled by the strong automotive industry's adoption of advanced electronics for ADAS and electric vehicles, as well as industrial automation and medical device sectors. European countries are focusing on developing specialized packaging solutions for high-reliability applications and are increasing investments in collaborative research initiatives to enhance their position in the global semiconductor supply chain.

- Latin America: Represents an emerging market with gradual adoption of advanced packaging, driven by increasing industrialization and expanding consumer electronics markets. While smaller in scale compared to other regions, there is a growing interest in local manufacturing and assembly capabilities.

- Middle East and Africa (MEA): Currently a smaller market, but with potential for growth driven by digital transformation initiatives, increasing infrastructure development, and growing demand for telecommunication and IoT devices. Investments in data centers and smart city projects are expected to drive future adoption of advanced packaging solutions.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Advanced Packaging Market.- Intel Corporation

- ASE Technology Holding Co. Ltd.

- Samsung Electronics Co. Ltd.

- TSMC

- Amkor Technology Inc.

- JCET Group Co. Ltd.

- Siliconware Precision Industries Co. Ltd.

- United Microelectronics Corporation (UMC)

- Powertech Technology Inc.

- Unisem (M) Berhad

- IBM Corporation

- Fujitsu Ltd.

- STATS ChipPAC Pte. Ltd.

- UTAC Holdings Ltd.

- King Yuan Electronics Co. Ltd.

- Renesas Electronics Corporation

- NXP Semiconductors

- Texas Instruments Incorporated

- Analog Devices Inc.

- Qualcomm Technologies Inc.

Frequently Asked Questions

Analyze common user questions about the Advanced Packaging market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is Advanced Packaging in the semiconductor industry?

Advanced Packaging refers to innovative techniques and technologies that enhance the performance, integration, and functionality of semiconductor devices beyond traditional methods. It involves intricate processes like 2.5D/3D stacking, fan-out wafer-level packaging (FOWLP), and heterogeneous integration, allowing multiple chips to be combined into a single, compact, and highly efficient package.

What are the primary drivers of the Advanced Packaging market growth?

The market's growth is primarily driven by the escalating demand for high-performance computing (HPC), artificial intelligence (AI), and data center applications, along with the continuous push for miniaturization in consumer electronics, 5G technology adoption, and the expansion of automotive electronics for ADAS and electric vehicles.

How does AI impact the Advanced Packaging sector?

AI significantly impacts advanced packaging by driving demand for highly integrated and powerful chips for AI workloads. Furthermore, AI tools optimize packaging design, simulate performance, and enhance manufacturing processes through machine learning, leading to improved yield rates, predictive maintenance, and accelerated development cycles.

Which regions are leading the Advanced Packaging market?

Asia Pacific (APAC) currently dominates the Advanced Packaging market, primarily due to its robust semiconductor manufacturing infrastructure in countries like Taiwan, South Korea, and China. North America and Europe also hold significant market shares, driven by strong R&D, high-performance computing demands, and specialized automotive applications.

What are the key challenges faced by the Advanced Packaging market?

Major challenges include the high manufacturing costs and capital expenditures for advanced equipment, the complexity of 3D integration and maintaining high yield rates, managing thermal dissipation in high-performance packages, the lack of industry-wide standardization, and geopolitical tensions impacting global supply chains.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted