3D Display Market

3D Display Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702771 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

3D Display Market Size

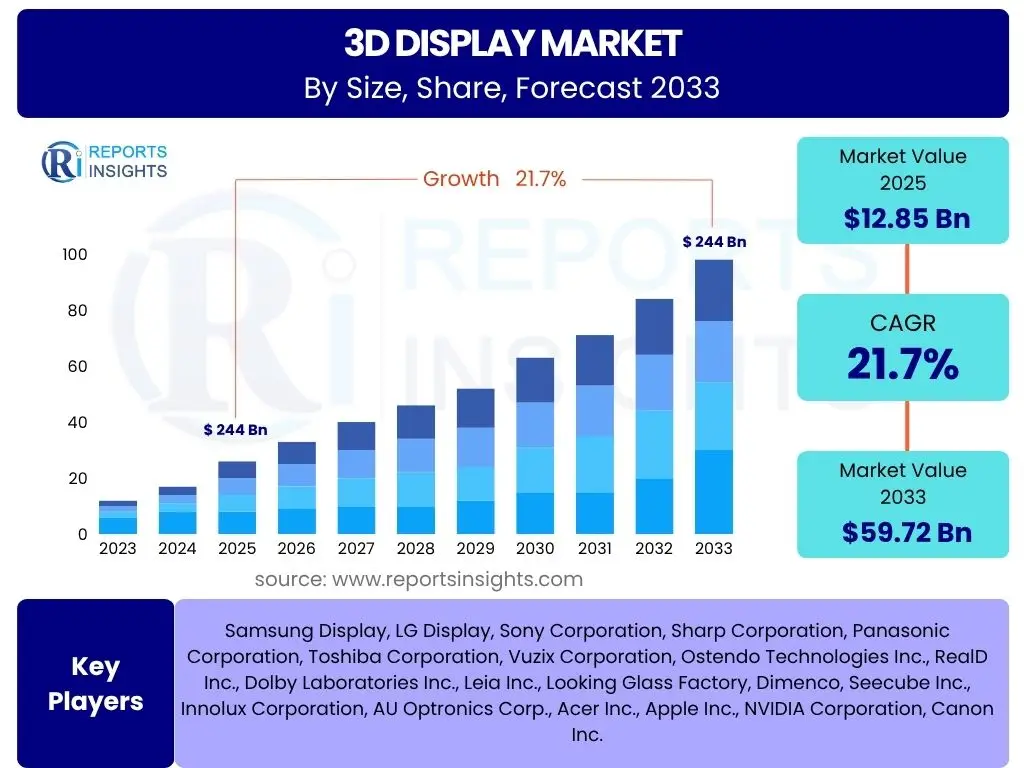

According to Reports Insights Consulting Pvt Ltd, The 3D Display Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 21.7% between 2025 and 2033. This robust growth trajectory is driven by escalating demand across various end-use industries, including entertainment, healthcare, automotive, and industrial design. The convergence of advanced display technologies with evolving consumer preferences for immersive visual experiences is a significant catalyst.

The market is estimated at USD 12.85 Billion in 2025 and is projected to reach USD 59.72 Billion by the end of the forecast period in 2033. This substantial expansion reflects increasing investments in research and development by key players, aiming to overcome technological hurdles such as eye fatigue and limited viewing angles. Furthermore, the continuous decline in manufacturing costs for 3D display components contributes to broader market accessibility and adoption across diverse applications.

Key 3D Display Market Trends & Insights

The 3D Display market is undergoing significant transformation, driven by technological advancements and evolving application landscapes. Users frequently inquire about the integration of 3D displays into everyday devices, the impact of augmented and virtual reality, and the feasibility of glasses-free 3D. Current trends indicate a strong push towards autostereoscopic technologies, reducing the need for specialized eyewear and enhancing user comfort. Furthermore, the development of light field displays promises even more realistic and interactive 3D experiences, moving beyond traditional stereoscopy.

Another key trend revolves around the expansion of 3D display applications beyond conventional entertainment into more niche and high-value sectors such as medical imaging, industrial design, automotive head-up displays (HUDs), and specialized training simulations. The growing demand for enhanced visualization in these professional fields is fostering innovation in display resolution, brightness, and real-time content rendering. User interest is also high regarding the standardization of 3D content formats and the availability of diverse content libraries to fully leverage the capabilities of these advanced displays.

- Increasing adoption of autostereoscopic (glasses-free) 3D technology.

- Convergence with Augmented Reality (AR) and Virtual Reality (VR) ecosystems.

- Expansion of 3D display applications in healthcare, automotive, and industrial sectors.

- Development of advanced light field and holographic display solutions.

- Focus on high-resolution, high-brightness, and wide viewing angle displays.

- Growth in 3D content creation tools and platforms.

AI Impact Analysis on 3D Display

The integration of Artificial intelligence (AI) is poised to revolutionize the 3D Display market, addressing several long-standing challenges and unlocking new capabilities. Common user inquiries often revolve around how AI can improve 3D content creation, enhance display rendering, and personalize user experiences. AI algorithms are increasingly being employed to automate and optimize the generation of 3D content, reducing the time and cost associated with manual modeling and animation. This includes AI-powered tools for converting 2D images or videos into 3D, intelligent scene reconstruction, and dynamic asset generation.

Furthermore, AI significantly impacts the real-time rendering and optimization of 3D visuals on display devices. AI-driven upscaling and super-resolution techniques can enhance the perceived quality of 3D content, even on lower-resolution displays, while AI-powered foveated rendering can optimize processing power by rendering only the user's focal point at high resolution. Users are keen to understand how AI can reduce common issues like eye strain and motion sickness by dynamically adjusting display parameters based on user gaze, head tracking, and environmental conditions. The potential for AI to create truly adaptive and personalized 3D viewing experiences is a major area of interest and development.

- AI-driven optimization of 3D content creation and conversion processes.

- Enhanced real-time rendering and performance through AI-powered algorithms.

- Personalized viewing experiences via AI-based eye-tracking and adaptive display adjustments.

- Improved resolution and visual fidelity with AI upscaling and super-resolution.

- Development of intelligent algorithms to minimize eye strain and discomfort in 3D viewing.

- AI integration for dynamic scene generation and interactive 3D environments.

Key Takeaways 3D Display Market Size & Forecast

Users frequently seek concise summaries of market projections, key growth drivers, and factors influencing the future trajectory of the 3D Display market. The overarching takeaway is the anticipated rapid expansion of the market, driven by a confluence of technological innovations and diversified application areas. The transition towards glasses-free 3D technologies is a pivotal development, promising to democratize access and usage across consumer and professional segments. This shift addresses a primary user concern regarding the inconvenience and limitations of traditional stereoscopic viewing.

Another significant insight is the increasing penetration of 3D displays into high-value sectors like medical diagnostics, automotive infotainment, and industrial prototyping, which are expected to generate substantial revenue streams. While challenges such as content scarcity and high initial costs persist, the market is poised to overcome these hurdles through continuous R&D and strategic industry collaborations. The forecast indicates that the 3D display market is not just growing, but evolving into a more versatile and integral component of various digital ecosystems, making it a critical area for investment and innovation.

- Market projected to grow substantially at a CAGR of 21.7% from 2025 to 2033, reaching USD 59.72 Billion.

- Autostereoscopic technology is a primary driver for wider adoption and consumer appeal.

- Diversification of applications beyond entertainment, into healthcare, automotive, and industrial use.

- Technological advancements, including AI integration, are improving content creation and viewing comfort.

- Significant opportunities exist in emerging fields such as the metaverse and advanced simulation.

3D Display Market Drivers Analysis

The 3D Display market is propelled by several robust drivers, each contributing significantly to its projected growth. A primary driver is the burgeoning demand for immersive and realistic visual experiences across various sectors, including gaming, entertainment, and professional visualization. Consumers and industries are increasingly seeking enhanced visual fidelity that conventional 2D displays cannot provide. This demand is further amplified by the proliferation of 3D content, from blockbuster movies to virtual reality applications, necessitating advanced display technologies capable of rendering these complex visuals.

Technological advancements, particularly in autostereoscopic and light-field display technologies, are also critical drivers. These innovations are addressing historical limitations such as the need for glasses and narrow viewing angles, making 3D displays more user-friendly and accessible. Additionally, the integration of 3D displays into new application areas like medical imaging for surgical planning, automotive heads-up displays for navigation and safety, and industrial design for product prototyping, is opening up vast new revenue streams and fostering rapid market expansion. The declining cost of manufacturing 3D display components also contributes to their increased affordability and wider adoption.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing demand for immersive entertainment and gaming experiences. | +5.5% | North America, Asia Pacific, Europe | Short to Medium Term (2025-2029) |

| Advancements in glasses-free 3D (autostereoscopic) technologies. | +4.8% | Global | Medium to Long Term (2027-2033) |

| Increasing adoption in professional applications (medical, automotive, industrial). | +4.2% | North America, Europe, Japan | Medium Term (2026-2031) |

| Rising investments in virtual and augmented reality ecosystems. | +3.0% | Global | Short to Medium Term (2025-2030) |

| Decline in manufacturing costs and increased accessibility. | +2.5% | Asia Pacific, Emerging Economies | Medium to Long Term (2028-2033) |

3D Display Market Restraints Analysis

Despite its significant growth potential, the 3D Display market faces several notable restraints that could temper its expansion. One major hurdle is the relatively high cost of advanced 3D display technologies, particularly for larger screens or highly specialized professional applications, which can deter widespread consumer adoption. This cost barrier is compounded by the perception among some consumers that the benefits of 3D viewing do not always outweigh the added expense, especially for non-autostereoscopic solutions that require cumbersome eyewear.

Another significant restraint is the limited availability of high-quality, native 3D content across various platforms. While the entertainment industry has seen some successes, the broader content ecosystem for everyday use, educational materials, or general broadcasting still predominantly relies on 2D formats. This scarcity of compelling content reduces the incentive for consumers and businesses to invest in 3D display hardware. Furthermore, lingering concerns about potential eye strain, motion sickness, or visual discomfort associated with prolonged 3D viewing, particularly for traditional stereoscopic displays, remain a psychological barrier for some potential users, requiring continuous technological improvements to mitigate these issues.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High initial cost of advanced 3D display hardware. | -3.5% | Global | Short to Medium Term (2025-2029) |

| Limited availability of native 3D content across diverse platforms. | -3.0% | Global | Medium Term (2026-2031) |

| Concerns regarding eye strain and visual fatigue for users. | -2.0% | Global | Short to Medium Term (2025-2029) |

| Interoperability issues and lack of standardized formats. | -1.5% | Global | Medium Term (2026-2030) |

3D Display Market Opportunities Analysis

The 3D Display market is ripe with opportunities that can significantly accelerate its growth trajectory. A prime opportunity lies in the continued advancements and commercialization of autostereoscopic (glasses-free) 3D technology. As these technologies mature and become more cost-effective, they promise to remove the primary barrier to widespread consumer adoption, opening up vast markets in consumer electronics, public displays, and digital signage. The comfort and convenience offered by glasses-free solutions will likely drive a new wave of demand previously untapped by traditional stereoscopic displays.

Furthermore, the expanding ecosystem of the metaverse and immersive virtual environments presents a monumental opportunity for 3D displays. As individuals and enterprises increasingly engage in virtual worlds for work, entertainment, and social interaction, the demand for displays that can render truly spatial and interactive content will surge. This includes specialized displays for virtual reality arcades, collaborative design studios, and virtual classrooms. Beyond the metaverse, opportunities are emerging in niche but high-value applications such as holographic advertising, advanced medical training simulators, and sophisticated automotive cockpit displays, where the benefits of 3D visualization offer clear competitive advantages and improved user experiences.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Commercialization of advanced autostereoscopic (glasses-free) displays. | +4.0% | Global, particularly North America, Asia Pacific | Medium to Long Term (2027-2033) |

| Emergence of the Metaverse and demand for immersive virtual environments. | +3.5% | Global | Medium to Long Term (2028-2033) |

| Expansion into specialized professional applications (medical, defense, education). | +3.0% | North America, Europe, Asia Pacific | Short to Medium Term (2025-2030) |

| Development of 3D displays for automotive infotainment and HUDs. | +2.5% | Europe, North America, Japan | Medium Term (2026-2032) |

| Growth in 3D content creation tools and platforms leveraging AI. | +2.0% | Global | Short to Medium Term (2025-2030) |

3D Display Market Challenges Impact Analysis

The 3D Display market faces several significant challenges that require innovative solutions to ensure sustained growth and widespread adoption. A primary challenge is the persistent issue of limited and fragmented 3D content. Despite advancements in display technology, the dearth of compelling, diverse, and easily accessible 3D content across various platforms continues to hinder consumer uptake. Content creators often face technical complexities and high production costs when developing native 3D experiences, leading to a bottleneck in content availability.

Another critical challenge is overcoming user discomfort, such as eye strain, headaches, and motion sickness, which are often associated with prolonged viewing of certain 3D display types, particularly stereoscopic ones. While autostereoscopic technologies aim to mitigate these issues, achieving a truly comfortable and immersive viewing experience for all users remains a complex engineering challenge. Additionally, the lack of universal standards for 3D content formats, display specifications, and interoperability across devices creates friction in the ecosystem, complicating content distribution and hardware compatibility for both consumers and manufacturers. Addressing these challenges through robust R&D and industry collaboration will be crucial for the market to realize its full potential.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Scarcity and high cost of producing compelling 3D content. | -4.0% | Global | Short to Medium Term (2025-2030) |

| Technical complexities in achieving comfortable, high-quality glasses-free 3D. | -3.0% | Global | Medium Term (2026-2031) |

| Lack of industry-wide standardization for 3D content and hardware. | -2.5% | Global | Medium to Long Term (2027-2033) |

| High power consumption and processing requirements for advanced 3D rendering. | -1.5% | Global | Short to Medium Term (2025-2029) |

3D Display Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global 3D Display market, offering detailed insights into market size, growth trends, competitive landscape, and future projections. The scope covers various display technologies, applications, and regional dynamics, providing stakeholders with critical information to make informed strategic decisions. It delves into the impact of emerging technologies like AI and the metaverse, alongside a thorough examination of market drivers, restraints, opportunities, and challenges affecting the industry from 2019 to 2033.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 12.85 Billion |

| Market Forecast in 2033 | USD 59.72 Billion |

| Growth Rate | 21.7% |

| Number of Pages | 255 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Samsung Display, LG Display, Sony Corporation, Sharp Corporation, Panasonic Corporation, Toshiba Corporation, Vuzix Corporation, Ostendo Technologies Inc., RealD Inc., Dolby Laboratories Inc., Leia Inc., Looking Glass Factory, Dimenco, Seecube Inc., Innolux Corporation, AU Optronics Corp., Acer Inc., Apple Inc., NVIDIA Corporation, Canon Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The 3D Display market is meticulously segmented to provide a granular understanding of its diverse components and their individual growth trajectories. This segmentation allows for precise analysis of market dynamics across various technological approaches, product categories, and application verticals, catering to different end-user needs and preferences. Understanding these segments is crucial for stakeholders to identify high-potential areas and tailor their strategies accordingly.

The segmentation by technology differentiates between conventional stereoscopic methods requiring eyewear and the more advanced autostereoscopic solutions that offer glasses-free viewing, reflecting the industry's shift towards greater user convenience. Product type segmentation provides insights into the adoption rates across devices such as 3D TVs, smartphones, head-mounted displays, and specialized volumetric displays. Application-based segmentation highlights the primary revenue-generating sectors, from consumer entertainment to specialized industrial and medical uses. These detailed breakdowns facilitate a comprehensive market assessment and enable targeted strategic planning.

- By Technology: Stereoscopic (Anaglyph, Polarized, Active Shutter), Autostereoscopic (Lenticular Lens, Parallax Barrier, Light Field, Holographic)

- By Product Type: Volumetric Displays, Head-Mounted Displays (HMDs), Projectors, Smart TVs, Smartphones, Monitors

- By Application: Entertainment (Gaming, Film, Broadcasting), Healthcare (Medical Imaging, Surgical Training), Automotive (HUDs, Infotainment), Industrial Design & Manufacturing, Education & Training, Retail & Advertising, Military & Defense, Others

- By End-User: Consumer, Commercial, Industrial, Medical, Government & Defense

- By Display Size: Up to 50 Inches, 50-100 Inches, Above 100 Inches

Regional Highlights

- North America: This region is a leading adopter of 3D display technologies, driven by a robust entertainment industry, significant investments in AR/VR, and increasing demand from the healthcare and automotive sectors. Early adoption of advanced consumer electronics and strong research and development capabilities contribute to its market dominance. The presence of key technology developers and a high disposable income further support market growth.

- Europe: Europe demonstrates strong growth in the 3D Display market, particularly in professional and industrial applications such as automotive design, engineering, and medical visualization. Countries like Germany and the UK are at the forefront of adopting 3D displays for manufacturing and specialized training. The region's emphasis on innovation and advanced manufacturing processes fuels the demand for high-fidelity 3D visualization solutions.

- Asia Pacific (APAC): APAC is expected to exhibit the highest growth rate during the forecast period, primarily due to the rapid expansion of the consumer electronics manufacturing base, increasing disposable incomes, and a burgeoning gaming and entertainment industry in countries like China, Japan, and South Korea. Government initiatives promoting smart cities and digital transformation also contribute to the adoption of 3D displays in public spaces and retail.

- Latin America: This region is experiencing steady growth, driven by increasing internet penetration, rising consumer awareness, and growing investments in digital infrastructure. While relatively smaller than other regions, the demand for immersive entertainment and educational content is gradually boosting the adoption of 3D display technologies. Brazil and Mexico are key markets within this region.

- Middle East and Africa (MEA): The MEA region is an emerging market for 3D displays, propelled by diversifying economies, investments in tourism and entertainment infrastructure, and increasing adoption of advanced technologies in sectors like healthcare and defense. The region's focus on smart city development and large-scale public projects also presents opportunities for 3D display integration.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the 3D Display Market.- Samsung Display

- LG Display

- Sony Corporation

- Sharp Corporation

- Panasonic Corporation

- Toshiba Corporation

- Vuzix Corporation

- Ostendo Technologies Inc.

- RealD Inc.

- Dolby Laboratories Inc.

- Leia Inc.

- Looking Glass Factory

- Dimenco

- Seecube Inc.

- Innolux Corporation

- AU Optronics Corp.

- Acer Inc.

- Apple Inc.

- NVIDIA Corporation

- Canon Inc.

Frequently Asked Questions

What is the projected growth rate of the 3D Display Market?

The 3D Display Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 21.7% between 2025 and 2033, reaching an estimated value of USD 59.72 Billion by 2033.

What are the primary drivers for the 3D Display Market?

Key drivers include increasing demand for immersive entertainment, advancements in glasses-free (autostereoscopic) 3D technology, and growing adoption in professional applications such as medical imaging, automotive, and industrial design.

How is AI impacting the 3D Display industry?

AI is revolutionizing 3D display technology by optimizing content creation, enhancing real-time rendering, enabling personalized viewing experiences through eye-tracking, and developing solutions to minimize eye strain and discomfort.

What are the main challenges facing the 3D Display Market?

Major challenges include the scarcity and high cost of producing compelling 3D content, technical complexities in achieving comfortable glasses-free 3D, and the lack of industry-wide standardization for content and hardware.

Which regions are expected to be key growth markets for 3D Displays?

Asia Pacific (APAC) is anticipated to be the fastest-growing region due to strong consumer electronics manufacturing and increasing disposable incomes, while North America and Europe will maintain significant market shares due to high R&D investments and professional application adoption.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted