Tablet and Notebook Display Market

Tablet and Notebook Display Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703068 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

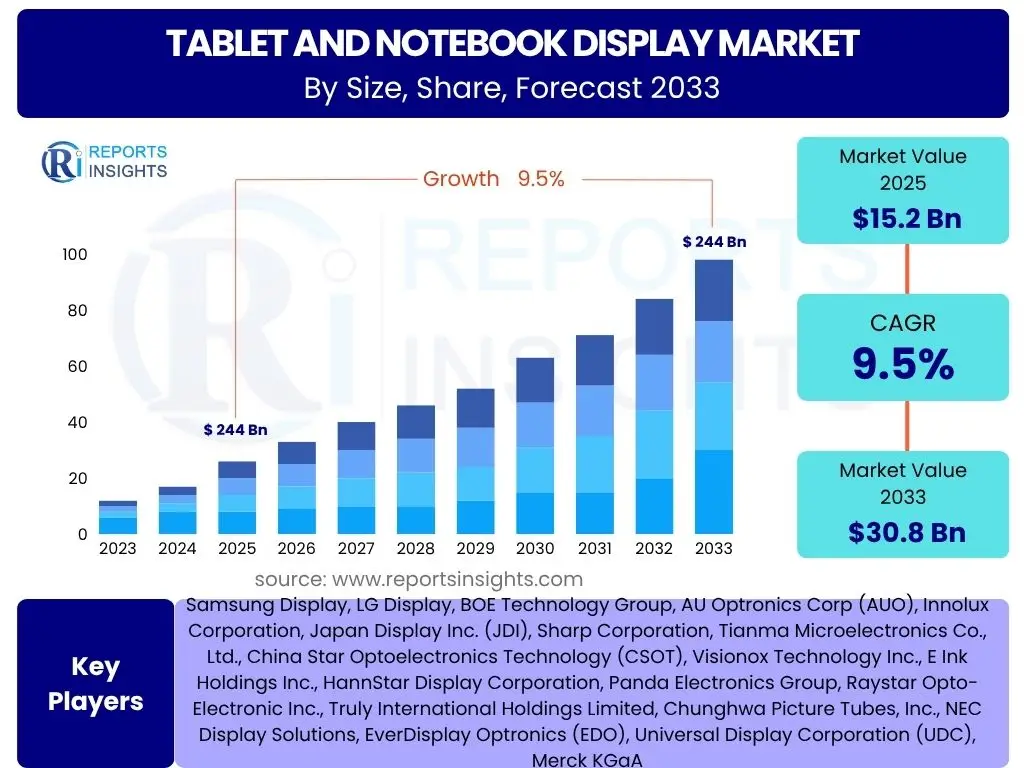

Tablet and Notebook Display Market Size

According to Reports Insights Consulting Pvt Ltd, The Tablet and Notebook Display Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.5% between 2025 and 2033. The market is estimated at USD 15.2 Billion in 2025 and is projected to reach USD 30.8 Billion by the end of the forecast period in 2033.

Key Tablet and Notebook Display Market Trends & Insights

Common inquiries regarding the Tablet and Notebook Display market frequently revolve around the evolution of display technologies, their impact on user experience, and the sustainability of manufacturing processes. Users are keenly interested in understanding which display types are gaining traction, how performance metrics such as refresh rates and resolution are advancing, and the broader implications of these developments for both consumers and enterprises. This segment explores the significant technological and market shifts defining the current landscape and future trajectory of tablet and notebook displays.

The market is witnessing a profound shift towards more immersive and power-efficient display solutions. Consumer demand for higher fidelity visuals, combined with the increasing adoption of tablets and notebooks for professional and creative tasks, is driving innovation. This includes advancements in panel structures, backlighting technologies, and integration with input methods, which collectively enhance the overall utility and appeal of these devices in a diverse range of environments.

- Increased adoption of OLED and Mini-LED display technologies for superior contrast and brightness.

- Rising demand for higher refresh rates (120Hz and above) in gaming and professional notebooks.

- Growth in touch-enabled and stylus-supported displays for enhanced interactivity and productivity.

- Focus on thinner bezels and higher screen-to-body ratios for more immersive viewing experiences.

- Development of energy-efficient display panels to extend battery life in portable devices.

- Emergence of foldable and rollable display prototypes for future form factors.

- Growing emphasis on eye-care features, including low blue light and anti-glare coatings.

- Integration of advanced display security features such as privacy filters.

- Expansion of sustainable manufacturing practices and use of recycled materials in display components.

AI Impact Analysis on Tablet and Notebook Display

User questions frequently address how artificial intelligence (AI) is transforming display technology, particularly concerning image quality, user interaction, and manufacturing efficiency. There is significant interest in understanding AI's role in enhancing visual processing, enabling personalized display experiences, and optimizing the production of display panels. Users seek insights into AI-driven improvements in display performance and the potential for smart, adaptive screens.

AI's influence is expanding across various facets of the tablet and notebook display ecosystem. In terms of user experience, AI algorithms are being leveraged for real-time image and video enhancement, adjusting display parameters such as brightness, contrast, and color temperature based on ambient lighting and content. This leads to more dynamic and visually appealing content consumption. Furthermore, AI is crucial in optimizing power consumption, intelligently managing backlight units and pixels to extend battery life without compromising visual fidelity.

Beyond the end-user experience, AI plays a pivotal role in the manufacturing and quality control of display panels. AI-powered inspection systems can detect micro-defects with greater precision and speed than traditional methods, leading to higher yield rates and reduced production costs. Predictive maintenance for manufacturing equipment, enabled by AI, further enhances operational efficiency. The long-term trajectory suggests AI could also influence adaptive material design and the development of next-generation display architectures, paving the way for truly intelligent and responsive screens.

- Enhanced image processing: AI-driven upscaling, noise reduction, and dynamic range optimization for superior visual quality.

- Adaptive display settings: Real-time adjustment of brightness, color temperature, and contrast based on ambient light and content type using AI.

- Power optimization: AI algorithms manage display power consumption to extend battery life through intelligent pixel and backlight control.

- Manufacturing efficiency: AI-powered defect detection and quality control systems in panel production lines, improving yield rates.

- Personalized user experience: AI learns user preferences to customize display profiles and content presentation.

- Content awareness: AI can analyze on-screen content to apply optimal display modes for different applications (e.g., gaming, reading, video).

- Predictive maintenance: AI monitors display components for early signs of failure, reducing repair costs and downtime.

- New material discovery: AI assists in the research and development of novel display materials with enhanced properties.

- Generative design: AI tools aid in optimizing display panel layouts and circuitry for performance and efficiency.

Key Takeaways Tablet and Notebook Display Market Size & Forecast

User questions frequently probe the core conclusions and future outlook of the Tablet and Notebook Display market, seeking to understand the most impactful factors influencing its growth and competitive dynamics. There's a strong interest in identifying the primary drivers of market expansion, the significant technological shifts, and the critical challenges that could impede progress. This summary addresses these inquiries by highlighting the essential insights derived from the market size and forecast data, providing a condensed view of the market's trajectory.

The market is poised for sustained growth, underpinned by continuous technological innovation and evolving consumer preferences for higher-quality, more versatile display solutions. The increasing convergence of work, education, and entertainment on portable devices further solidifies the demand for advanced displays. While economic fluctuations and supply chain vulnerabilities present ongoing challenges, the industry's focus on premiumization, energy efficiency, and novel form factors is expected to drive significant value creation over the forecast period.

- The Tablet and Notebook Display market is projected for robust growth, driven by technological advancements and rising demand for high-performance devices.

- OLED and Mini-LED technologies are set to be primary growth catalysts, commanding premium pricing and expanding market share.

- The shift towards hybrid work models and remote education continues to fuel demand for larger, higher-resolution, and more ergonomic displays.

- Energy efficiency and sustainable manufacturing practices are emerging as key competitive differentiators and consumer preferences.

- Asia-Pacific is anticipated to remain the dominant market, driven by its manufacturing prowess and large consumer base, while North America and Europe will lead in adoption of premium displays.

- Supply chain resilience and managing raw material price volatility will be crucial factors influencing market profitability.

- The competitive landscape is intensifying, with manufacturers investing heavily in R&D to introduce next-generation display solutions and capture market share.

Tablet and Notebook Display Market Drivers Analysis

The Tablet and Notebook Display market is propelled by a confluence of factors, ranging from technological innovation to shifting consumer behavior and evolving work paradigms. A primary driver is the incessant demand for higher resolution, refresh rates, and color accuracy, particularly from segments like professional content creation, gaming, and multimedia consumption. This pushes manufacturers to continually enhance display panel capabilities. The global transition towards remote work and e-learning further amplifies the need for reliable, high-quality display solutions in portable devices.

Furthermore, advancements in display technologies, such as the increasing commercial viability and adoption of OLED and Mini-LED panels, are significant market accelerators. These technologies offer superior contrast, deeper blacks, and better power efficiency, appealing to a broad spectrum of users. The growing integration of touch functionality, stylus support, and foldable form factors in notebooks and tablets also expands their utility, driving new product cycles and market demand. Economic factors, including the increasing affordability of advanced display technologies due to scaling production, contribute to their wider market penetration.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for High-Resolution and Advanced Displays | +2.5% | Global, particularly North America, Europe, APAC | Short to Mid-term (2025-2030) |

| Proliferation of Remote Work and E-learning | +2.0% | Global, especially Developed Economies | Mid-term (2025-2031) |

| Technological Advancements in Display Panels (OLED, Mini-LED) | +2.3% | Global, with Manufacturing Hubs in APAC | Short to Long-term (2025-2033) |

| Growth in Gaming and Multimedia Consumption | +1.8% | North America, Europe, APAC (China, South Korea, Japan) | Mid-term (2026-2032) |

| Rising Affordability of Premium Display Technologies | +0.9% | Emerging Markets, Global | Long-term (2028-2033) |

Tablet and Notebook Display Market Restraints Analysis

Despite robust growth prospects, the Tablet and Notebook Display market faces several significant restraints that could temper its expansion. One prominent challenge is the vulnerability of the global supply chain, which can be easily disrupted by geopolitical tensions, natural disasters, or public health crises. Such disruptions lead to shortages of critical components, raw material price volatility, and increased production costs, ultimately affecting the final product pricing and availability for consumers. The market's reliance on a few key suppliers for certain advanced display components also exacerbates this vulnerability.

Another major restraint is the intense price competition within the display manufacturing sector. The commoditization of standard LCD panels, coupled with a large number of players, exerts downward pressure on profit margins. While premium technologies like OLED offer higher margins, increasing production capacities and competition are slowly eroding these advantages. Furthermore, economic slowdowns and inflationary pressures can lead to reduced consumer spending on discretionary items like new tablets and notebooks, impacting overall market demand. The mature state of some regional markets also limits significant new growth, shifting focus towards replacement cycles rather than new user acquisition.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Supply Chain Disruptions and Component Shortages | -1.5% | Global | Short to Mid-term (2025-2029) |

| Intense Price Competition and Margin Pressure | -1.2% | Global, particularly Asia Pacific | Mid to Long-term (2027-2033) |

| Economic Downturns and Reduced Consumer Spending | -1.0% | Global, especially Developed Economies | Short-term (2025-2027) |

| Market Saturation in Mature Regions | -0.8% | North America, Europe, Japan | Mid to Long-term (2028-2033) |

Tablet and Notebook Display Market Opportunities Analysis

Significant opportunities abound in the Tablet and Notebook Display market, driven by evolving technological paradigms and expanding application areas. The advent of novel form factors, such as foldable and rollable displays, represents a substantial avenue for innovation and market expansion. These technologies promise to redefine the user experience by offering greater versatility and portability, potentially creating new product categories and stimulating demand. Manufacturers investing in these cutting-edge solutions stand to gain a first-mover advantage and capture premium market segments.

Another key opportunity lies in the development and adoption of more sustainable and eco-friendly display manufacturing processes and materials. As environmental concerns gain prominence, consumers and regulations increasingly favor products with a lower carbon footprint. Companies that can innovate in green display technologies, from production to recycling, will differentiate themselves and appeal to a growing segment of environmentally conscious consumers. Furthermore, the expansion into specialized niche applications, such as medical displays, industrial control panels, and automotive infotainment systems, offers lucrative growth paths beyond traditional consumer electronics, leveraging the advanced capabilities of modern display technology.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of Foldable and Rollable Display Technologies | +1.8% | Global, with R&D in APAC, North America | Mid to Long-term (2027-2033) |

| Expansion into Niche and Specialized Applications | +1.5% | Global | Mid to Long-term (2026-2033) |

| Development of Sustainable and Eco-friendly Display Solutions | +1.0% | Europe, North America, Japan | Long-term (2028-2033) |

| Integration of Advanced Sensing and Haptic Feedback | +0.8% | Global | Mid to Long-term (2027-2033) |

Tablet and Notebook Display Market Challenges Impact Analysis

The Tablet and Notebook Display market faces several critical challenges that demand strategic responses from manufacturers and stakeholders. Fluctuations in raw material costs, particularly for rare earth elements and specialized chemicals essential for display production, pose a significant hurdle. These volatilities directly impact manufacturing costs and, consequently, product pricing and profitability. Managing these cost pressures while maintaining competitive pricing is a constant balancing act for market players, requiring robust procurement strategies and potential vertical integration.

Another substantial challenge is the rapid pace of technological obsolescence. The display market is characterized by continuous innovation, where new display technologies and features emerge frequently. This rapid evolution can quickly render existing products and manufacturing lines outdated, necessitating substantial and continuous investment in research and development, as well as capital expenditure for equipment upgrades. Companies that fail to keep pace risk losing market share to more innovative competitors. Additionally, the increasing complexity of intellectual property rights and patent disputes within the display technology sector adds legal and financial risks, particularly for new entrants or those seeking to license advanced technologies.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Fluctuations in Raw Material Costs | -1.3% | Global, particularly Asia Pacific (Manufacturing Hubs) | Short to Mid-term (2025-2029) |

| Rapid Technological Obsolescence | -1.1% | Global | Short to Mid-term (2025-2030) |

| Intensifying Intellectual Property Disputes | -0.7% | North America, Europe, APAC | Mid-term (2026-2031) |

| Stringent Environmental Regulations and Disposal | -0.6% | Europe, North America | Long-term (2028-2033) |

Tablet and Notebook Display Market - Updated Report Scope

This report provides an in-depth analysis of the Tablet and Notebook Display market, offering a comprehensive overview of its current size, historical performance, and future growth projections. It delves into key market trends, identifies prominent drivers and restraints, highlights emerging opportunities, and evaluates critical challenges shaping the industry. The scope encompasses detailed segmentation analysis by display technology, screen size, application, and end-user, complemented by a thorough regional breakdown to provide a holistic understanding of market dynamics.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 15.2 Billion |

| Market Forecast in 2033 | USD 30.8 Billion |

| Growth Rate | 9.5% |

| Number of Pages | 255 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Samsung Display, LG Display, BOE Technology Group, AU Optronics Corp (AUO), Innolux Corporation, Japan Display Inc. (JDI), Sharp Corporation, Tianma Microelectronics Co., Ltd., China Star Optoelectronics Technology (CSOT), Visionox Technology Inc., E Ink Holdings Inc., HannStar Display Corporation, Panda Electronics Group, Raystar Opto-Electronic Inc., Truly International Holdings Limited, Chunghwa Picture Tubes, Inc., NEC Display Solutions, EverDisplay Optronics (EDO), Universal Display Corporation (UDC), Merck KGaA |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Tablet and Notebook Display market is extensively segmented to provide a granular understanding of its diverse components and drivers. This segmentation allows for precise analysis of various technologies, screen dimensions, application scenarios, and end-user demographics. By breaking down the market into these distinct categories, the report illuminates specific growth pockets, technological preferences, and evolving consumer and enterprise demands, offering a comprehensive view of the industry's landscape. Understanding these segments is crucial for strategic planning and product development within the display ecosystem.

- By Display Technology: This segment includes LCD (comprising IPS LCD, TN LCD, and VA LCD variants, each offering distinct viewing angles and color reproduction), OLED (dominated by AMOLED and PMOLED, known for their superior contrast and true blacks), Mini-LED (an emerging backlight technology providing improved brightness and contrast control), Micro-LED (a next-generation technology with potential for ultra-high brightness and efficiency), and Other technologies such as E-Paper, used for specialized applications.

- By Screen Size: Categorization based on diagonal screen dimensions, including Less than 11 inches (typically for smaller tablets), 11-13 inches (common for versatile tablets and compact notebooks), 13-15 inches (standard for most notebooks and larger tablets), and 15 inches and above (for larger notebooks, gaming laptops, and specialized professional devices).

- By Application: Differentiated by the device type, covering Notebooks (including Consumer Notebooks, high-performance Gaming Notebooks, Business Notebooks for corporate use, and Ultrabooks focused on portability) and Tablets (categorized into Consumer Tablets for general use, Professional Tablets for creative and business tasks, and Education Tablets for learning environments).

- By Resolution: Segmented by pixel density and clarity, encompassing HD (High Definition), Full HD (1920x1080), QHD (Quad HD), 4K (Ultra HD), and emerging 8K resolutions, reflecting the market's move towards sharper visual experiences.

- By Backlight Technology: Distinguishes between Edge-lit (LEDs placed along the edges), Direct-lit (LEDs placed directly behind the panel for better uniformity), and Self-Emissive displays (like OLED, where each pixel generates its own light).

- By Panel Type: Separated into Rigid panels (traditional flat displays) and Flexible panels (enabling curved, foldable, and rollable form factors).

- By End-User: Divided into Commercial (including Enterprise for business use, Education for institutional deployment, and Government for public sector applications) and Consumer (individual buyers for personal use).

Regional Highlights

- North America: This region is characterized by high adoption rates of premium devices and advanced display technologies, driven by a strong focus on innovation, a robust gaming industry, and significant enterprise demand for high-performance notebooks and tablets. The presence of major technology companies and a high disposable income contribute to the early adoption of new display features and higher resolution screens. Demand for devices supporting hybrid work models remains strong.

- Europe: The European market demonstrates a strong preference for energy-efficient and sustainably manufactured display solutions, aligning with regional environmental regulations and consumer consciousness. Western European countries lead in the adoption of professional and high-end consumer devices. The region also exhibits steady growth in the education sector, driving demand for tablets and notebooks with durable displays.

- Asia Pacific (APAC): APAC represents the largest and fastest-growing market, primarily due to its vast manufacturing capabilities for display panels and electronic devices, coupled with a massive consumer base. Countries like China, South Korea, Japan, and Taiwan are at the forefront of display technology innovation and production. Rapid urbanization, increasing disposable incomes, and the widespread adoption of digital technologies in emerging economies within this region are significant growth drivers.

- Latin America: This region is an emerging market for tablet and notebook displays, characterized by increasing internet penetration and growing digital literacy. Affordability plays a crucial role in market adoption, leading to higher demand for cost-effective display solutions. Government initiatives in digital education and increasing commercial investments are expected to fuel future growth.

- Middle East and Africa (MEA): The MEA region is experiencing gradual growth, driven by increasing smartphone and internet penetration, along with government-led digital transformation initiatives. Investment in educational technology and enterprise IT infrastructure is contributing to the demand for tablets and notebooks, albeit at a slower pace compared to developed regions. Future growth is tied to economic diversification and improved digital access.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Tablet and Notebook Display Market.- Samsung Display

- LG Display

- BOE Technology Group

- AU Optronics Corp (AUO)

- Innolux Corporation

- Japan Display Inc. (JDI)

- Sharp Corporation

- Tianma Microelectronics Co., Ltd.

- China Star Optoelectronics Technology (CSOT)

- Visionox Technology Inc.

- E Ink Holdings Inc.

- HannStar Display Corporation

- Panda Electronics Group

- Raystar Opto-Electronic Inc.

- Truly International Holdings Limited

- Chunghwa Picture Tubes, Inc.

- NEC Display Solutions

- EverDisplay Optronics (EDO)

- Universal Display Corporation (UDC)

- Merck KGaA

Frequently Asked Questions

Analyze common user questions about the Tablet and Notebook Display market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the projected growth rate of the Tablet and Notebook Display Market?

The Tablet and Notebook Display Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.5% between 2025 and 2033, reaching an estimated USD 30.8 Billion by 2033.

Which display technologies are driving market growth?

OLED and Mini-LED display technologies are key drivers of market growth due to their superior contrast, brightness, and energy efficiency, increasingly adopted in high-end tablets and notebooks.

How is remote work impacting the Tablet and Notebook Display Market?

The widespread adoption of remote work and e-learning models has significantly boosted demand for tablets and notebooks, particularly for devices featuring larger, higher-resolution, and more ergonomic displays suitable for extended use.

What are the main challenges facing the Tablet and Notebook Display Market?

Key challenges include global supply chain disruptions, intense price competition, fluctuations in raw material costs, and the rapid pace of technological obsolescence, which necessitate continuous innovation and strategic procurement.

Which region holds the largest share in the Tablet and Notebook Display Market?

Asia Pacific (APAC) currently holds the largest market share, driven by its extensive display panel manufacturing capabilities and a large, growing consumer base for electronic devices.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted