Wired Telecommunication Carrier Market

Wired Telecommunication Carrier Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704225 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

Wired Telecommunication Carrier Market Size

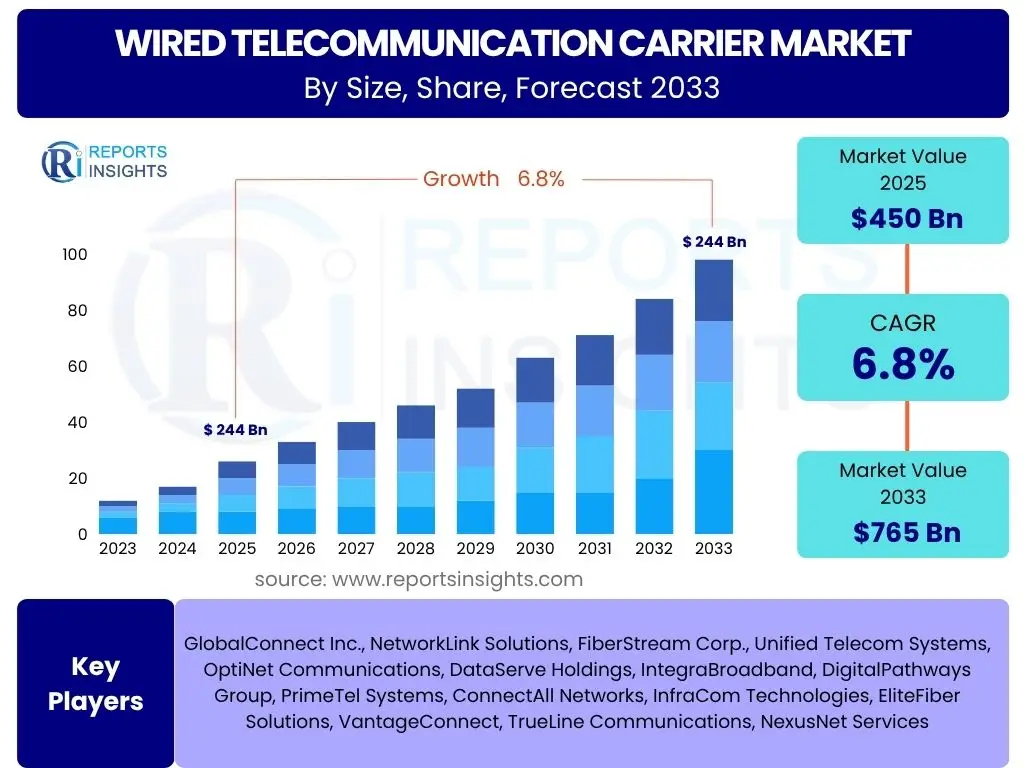

According to Reports Insights Consulting Pvt Ltd, The Wired Telecommunication Carrier Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 450 Billion in 2025 and is projected to reach USD 765 Billion by the end of the forecast period in 2033.

Key Wired Telecommunication Carrier Market Trends & Insights

The wired telecommunication carrier market is currently undergoing a significant transformation driven by escalating data demands, technological advancements, and evolving consumer and business needs. A primary trend involves the widespread deployment of fiber optic infrastructure, which is replacing legacy copper networks to support higher bandwidth requirements for residential and commercial customers. This fiberization is critical for delivering advanced services such as 4K/8K video streaming, cloud computing, and robust connectivity for the Internet of Things (IoT). Furthermore, the convergence of fixed and mobile networks is blurring traditional boundaries, with wired infrastructure serving as the essential backhaul for 5G deployments and future wireless technologies, ensuring seamless connectivity and high-speed data transmission across diverse environments.

Another pivotal trend is the increasing adoption of network virtualization technologies, including Software-Defined Networking (SDN) and Network Function Virtualization (NFV). These technologies enable carriers to create more flexible, scalable, and programmable networks, reducing operational costs and accelerating the deployment of new services. The shift towards edge computing is also a notable trend, pushing data processing closer to the source of generation, thereby reducing latency and improving application performance for critical services like autonomous vehicles and augmented reality. Moreover, the demand for dedicated, high-security enterprise solutions, such as private networks and managed SD-WAN services, is fostering new revenue streams and strategic partnerships within the wired telecommunication sector.

- Extensive Fiber-to-the-X (FTTX) deployments to enhance bandwidth and network reliability.

- Integration of wired networks as critical backhaul infrastructure for 5G and beyond.

- Increased adoption of Software-Defined Networking (SDN) and Network Function Virtualization (NFV) for agile service delivery.

- Growth in edge computing infrastructure to minimize latency and optimize performance.

- Rising demand for secure, high-capacity enterprise solutions and private networks.

- Convergence of fixed and mobile services, offering integrated communication solutions.

- Focus on network slicing and disaggregation for customized service offerings.

AI Impact Analysis on Wired Telecommunication Carrier

The integration of Artificial Intelligence (AI) into wired telecommunication networks is fundamentally reshaping operational paradigms, service delivery, and strategic decision-making. Users frequently inquire about how AI can optimize network performance, enhance security, and improve customer experience. AI-driven solutions are being deployed to automate complex network management tasks, predict potential network failures, and dynamically allocate resources based on real-time traffic patterns. This leads to significantly improved network efficiency, reduced downtime, and lower operational expenditures for carriers. The ability of AI to analyze vast datasets also enables more effective capacity planning and infrastructure investment strategies.

Beyond operational efficiencies, AI is transforming customer interactions and cybersecurity within the wired telecommunications landscape. Users are keen to understand how AI contributes to personalized customer services, predictive maintenance, and robust threat detection. AI-powered chatbots and virtual assistants are streamlining customer support, providing instant responses and resolving common issues, thereby enhancing customer satisfaction. In terms of security, AI algorithms can identify anomalous network behavior indicative of cyber threats, enabling proactive defense mechanisms against sophisticated attacks. Furthermore, AI facilitates the development of innovative services, such as smart home solutions, intelligent traffic management, and AI-optimized data centers, creating new revenue opportunities and solidifying the competitive position of wired carriers in the digital economy.

- Automated network operations and orchestration through AI algorithms.

- Predictive maintenance for infrastructure, minimizing downtime and optimizing resource allocation.

- Enhanced cybersecurity measures, including real-time threat detection and anomaly identification.

- Personalized customer service and support via AI-powered chatbots and virtual assistants.

- Optimized network planning and capacity management for efficient resource utilization.

- Development of new AI-driven services and smart applications leveraging network capabilities.

- Improved energy efficiency through AI-managed power consumption in network infrastructure.

Key Takeaways Wired Telecommunication Carrier Market Size & Forecast

The Wired Telecommunication Carrier Market is poised for consistent growth, driven by an insatiable global demand for high-speed data and reliable connectivity. Key user inquiries frequently revolve around the sustainability of this growth, the primary factors influencing market expansion, and the strategic implications for both established carriers and new entrants. The market's projected expansion from USD 450 Billion in 2025 to USD 765 Billion by 2033, at a CAGR of 6.8%, signifies robust investment in next-generation infrastructure, particularly fiber optics and backhaul solutions for advanced wireless technologies like 5G and future 6G networks. This growth is fundamentally underpinned by digital transformation initiatives across industries, the proliferation of connected devices, and the increasing reliance on cloud-based services.

A critical takeaway is the escalating importance of network quality, resilience, and latency, which are becoming key differentiators in a highly competitive landscape. Carriers are increasingly focusing on enhancing network intelligence through AI and automation to deliver superior performance and more agile service provisioning. While significant capital expenditure remains a challenge, the long-term opportunities arising from enterprise digitalization, smart city initiatives, and the expansion into underserved rural areas present compelling growth avenues. The market is evolving into a more diversified ecosystem where traditional connectivity services are augmented by value-added offerings such as cybersecurity, edge computing, and managed IT services, ensuring sustained relevance and revenue growth for wired telecommunication carriers.

- The market is set for steady growth, driven by increasing data consumption and digitalization.

- Significant investment in fiber infrastructure and 5G/6G backhaul is essential for future growth.

- Network quality, low latency, and reliability are paramount for competitive differentiation.

- AI and automation are critical for operational efficiency and service innovation.

- New revenue streams are emerging from value-added services beyond traditional connectivity.

- Strategic partnerships and mergers will likely shape the competitive landscape.

- Expansion into enterprise solutions and underserved regions presents substantial opportunities.

Wired Telecommunication Carrier Market Drivers Analysis

The wired telecommunication carrier market is significantly propelled by several fundamental drivers that underscore the necessity for robust and high-capacity network infrastructure. The escalating global demand for data, fueled by the proliferation of smartphones, smart devices, and bandwidth-intensive applications such as video streaming, online gaming, and cloud services, forms the primary catalyst. This persistent increase in data traffic necessitates continuous upgrades and expansion of wired networks, particularly fiber optics, to ensure seamless connectivity and prevent network congestion. Furthermore, the accelerating pace of digital transformation across various industries, including healthcare, education, manufacturing, and finance, mandates dependable high-speed internet connections for cloud adoption, remote work, and digital operations, driving enterprise demand for advanced wired solutions.

Another significant driver is the global deployment of 5G networks, which, despite being wireless, heavily rely on high-capacity wired backhaul infrastructure. Fiber optic cables are indispensable for connecting 5G small cells and base stations to the core network, ensuring the low latency and high throughput capabilities that 5G promises. Urbanization and the development of smart cities also contribute substantially to market growth, as intelligent urban environments require pervasive wired connectivity to support IoT sensors, smart grids, traffic management systems, and public services. Government initiatives and funding programs aimed at bridging the digital divide and expanding broadband access to rural and underserved areas further stimulate investment in wired infrastructure, ensuring broader market penetration and socioeconomic benefits.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Surging Data Consumption | +2.5% | Global | 2025-2033 |

| Digital Transformation Initiatives | +1.8% | North America, Europe, APAC | 2025-2033 |

| 5G Network Backhaul Demand | +1.5% | Global, particularly developed regions | 2025-2030 |

| Smart City Development | +1.2% | APAC, Europe, Middle East | 2027-2033 |

| Government Broadband Initiatives | +1.0% | Underserved Rural Areas Globally | 2025-2033 |

Wired Telecommunication Carrier Market Restraints Analysis

Despite the robust growth drivers, the wired telecommunication carrier market faces significant restraints that can impede its expansion. One of the most prominent challenges is the exceptionally high capital expenditure (CAPEX) required for building and maintaining extensive wired infrastructure, particularly fiber optic networks. The costs associated with deploying fiber, acquiring rights-of-way, and upgrading legacy systems are substantial, often necessitating long payback periods and making it challenging for smaller players to compete. This high upfront investment can limit the pace of network modernization and expansion, especially in economically sensitive regions or areas with low population density. Moreover, the extensive regulatory frameworks and permitting processes involved in infrastructure deployment across various jurisdictions add layers of complexity and cost, often leading to project delays.

Another critical restraint is the intensifying competition from wireless technologies, particularly advanced cellular networks (e.g., 5G FWA - Fixed Wireless Access) and satellite internet providers. While wired networks offer superior bandwidth and stability, wireless alternatives are becoming increasingly viable for last-mile connectivity in certain areas, potentially eroding a segment of the traditional wired customer base. This competition compels wired carriers to continuously innovate and invest, placing further pressure on profitability. Furthermore, the shortage of skilled labor for deploying, maintaining, and operating complex fiber optic and network virtualization technologies poses a significant bottleneck. The specialized expertise required for these tasks is not readily available in all regions, leading to increased labor costs and potential delays in project execution, thereby impacting the overall efficiency and expansion capabilities of carriers.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Expenditure (CAPEX) | -1.8% | Global | 2025-2033 |

| Intense Competition from Wireless Alternatives | -1.5% | North America, Europe | 2025-2033 |

| Complex Regulatory & Permitting Processes | -1.2% | Europe, Asia Pacific (certain countries) | 2025-2033 |

| Shortage of Skilled Labor | -0.9% | Global, particularly developed economies | 2025-2030 |

Wired Telecommunication Carrier Market Opportunities Analysis

The wired telecommunication carrier market is presented with numerous opportunities that can significantly contribute to its future growth and diversification. One significant avenue lies in the expansion of enterprise solutions, particularly for dedicated private networks, Software-Defined Wide Area Networks (SD-WAN), and secure cloud connectivity. As businesses continue their digital transformation journeys, they require robust, reliable, and secure wired infrastructure to support their mission-critical applications, data centers, and multi-cloud environments. This provides carriers with opportunities to offer premium, customized services beyond basic internet access, fostering stronger B2B relationships and higher average revenue per user (ARPU).

Another substantial opportunity exists in the burgeoning field of edge computing infrastructure development. As the demand for low-latency processing grows with the proliferation of IoT, AI, and real-time applications, wired carriers are uniquely positioned to leverage their extensive network footprint to deploy and manage edge data centers. This enables new service offerings such as localized content delivery, AI inferencing at the edge, and industrial IoT solutions. Furthermore, partnerships with hyperscale cloud providers and content delivery networks can create synergistic opportunities for wired carriers to host and deliver specialized services. Lastly, the ongoing efforts to bridge the digital divide in rural and underserved areas, often supported by government subsidies and public-private partnerships, present significant market expansion opportunities for wired broadband deployment, particularly in developing regions, ensuring universal access and new subscriber growth.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion of Enterprise Solutions (e.g., SD-WAN, Private Networks) | +2.0% | Global | 2025-2033 |

| Development of Edge Computing Infrastructure | +1.7% | North America, Europe, APAC | 2026-2033 |

| Partnerships with Hyperscale Cloud Providers & CDNs | +1.3% | Global | 2025-2033 |

| Rural Broadband Expansion & Digital Divide Initiatives | +1.0% | Developing Regions, Underserved Areas | 2025-2033 |

| Smart City and IoT Infrastructure Enablement | +0.8% | APAC, Middle East, Europe | 2027-2033 |

Wired Telecommunication Carrier Market Challenges Impact Analysis

The wired telecommunication carrier market faces several formidable challenges that necessitate strategic planning and innovative solutions. One of the primary concerns is the relentless evolution of technology, demanding continuous and often costly upgrades to existing infrastructure. Legacy networks require significant investment to modernize and keep pace with increasing bandwidth demands and emerging service requirements, leading to high capital expenditures and a constant need for re-investment cycles. Additionally, the complex issue of cybersecurity threats poses a pervasive challenge. Wired networks are vulnerable to sophisticated cyberattacks, including denial-of-service (DoS) attacks, data breaches, and ransomware, which can compromise network integrity, customer data, and service availability, leading to severe reputational and financial damage. Protecting vast and interconnected infrastructure from these evolving threats requires continuous investment in advanced security solutions and skilled personnel.

Another significant challenge is the increasing energy consumption of network infrastructure. As data traffic grows and more complex technologies are deployed, the energy footprint of wired networks expands, leading to higher operational costs and environmental concerns. Carriers are under pressure to adopt more energy-efficient technologies and sustainable practices. Furthermore, regulatory hurdles and policy uncertainties across different regions can complicate network deployment and market entry. Varying regulations concerning spectrum allocation, net neutrality, data privacy, and infrastructure sharing can create fragmented market conditions and impose compliance burdens on carriers. Lastly, the fierce competition from both traditional rivals and new entrants, including over-the-top (OTT) service providers, constantly pressures pricing and profit margins, requiring carriers to innovate and differentiate their offerings to maintain market share.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Requirements for Infrastructure Upgrades | -1.5% | Global | 2025-2033 |

| Evolving Cybersecurity Threats | -1.3% | Global | 2025-2033 |

| Intense Market Competition | -1.0% | North America, Europe | 2025-2033 |

| Increasing Energy Consumption of Networks | -0.8% | Global | 2025-2033 |

| Regulatory Hurdles and Policy Changes | -0.7% | Europe, Asia Pacific (certain countries) | 2025-2033 |

Wired Telecommunication Carrier Market - Updated Report Scope

This report provides an in-depth analysis of the global Wired Telecommunication Carrier market, offering a comprehensive overview of its current state, historical performance, and future growth prospects. The scope encompasses detailed market sizing, trend identification, impact analysis of key drivers, restraints, opportunities, and challenges. It also includes a thorough examination of AI's transformative impact on the sector. The report segments the market by technology, service type, application, and end-user, providing granular insights into each category's dynamics and regional contributions. Furthermore, it features profiles of key market players, competitive landscape analysis, and an outlook on future market developments, designed to support strategic decision-making for stakeholders.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 450 Billion |

| Market Forecast in 2033 | USD 765 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | GlobalConnect Inc., NetworkLink Solutions, FiberStream Corp., Unified Telecom Systems, OptiNet Communications, DataServe Holdings, IntegraBroadband, DigitalPathways Group, PrimeTel Systems, ConnectAll Networks, InfraCom Technologies, EliteFiber Solutions, VantageConnect, TrueLine Communications, NexusNet Services |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Wired Telecommunication Carrier Market is analyzed across various strategic segmentations to provide a granular understanding of its dynamics and growth trajectories. These segmentations enable stakeholders to identify specific market opportunities, competitive landscapes, and consumer behaviors within distinct categories. The segmentation by service type delineates revenue streams from voice, data, video, and managed services, reflecting the evolving portfolio of offerings by carriers. Data services, particularly broadband internet, continue to dominate due to increasing digital consumption and enterprise needs. Segmentation by end-user differentiates demand from residential, commercial (small, medium, and large enterprises), and government sectors, highlighting the varying requirements and growth patterns across customer groups.

Further analysis is conducted based on the underlying technology, distinguishing between traditional copper-based DSL, cable modem, T-carrier/E-carrier systems, and the increasingly dominant fiber optic infrastructure. Fiber optics represent the future of wired telecommunications due to their superior speed, reliability, and capacity. The market is also segmented by application, including broadband internet, telephony, television services, and specialized applications such as data center connectivity and cloud connectivity. This allows for a detailed examination of where network capacity and services are most critically consumed, guiding future investment and development strategies for wired telecommunication carriers. Each segment's growth rate, market share, and future outlook are meticulously assessed to offer comprehensive market insights.

- By Service Type:

- Voice Services

- Data Services

- Video Services

- Managed Services

- By End-User:

- Residential

- Commercial

- Small and Medium Businesses (SMB)

- Large Enterprise

- Government

- By Technology:

- Fiber Optics

- Digital Subscriber Line (DSL)

- Cable Modem

- T-carrier/E-carrier

- Others

- By Application:

- Broadband Internet

- Telephony

- Television

- Data Center Connectivity

- Cloud Connectivity

Regional Highlights

- North America: Characterized by early adoption of advanced wired technologies, significant investment in fiber optic networks, and strong demand from both residential and enterprise sectors. High penetration of broadband services and robust competitive landscape.

- Europe: Focus on digital infrastructure upgrades, strong regulatory influence, and initiatives to expand gigabit connectivity. Varying levels of fiber deployment across countries with strong emphasis on smart city development.

- Asia Pacific (APAC): Represents the fastest-growing region, driven by massive urbanization, rapid digitalization, and government-led initiatives for broadband expansion, particularly in emerging economies like India and Southeast Asia. China and Japan lead in fiber adoption and 5G backhaul.

- Latin America: Growing demand for high-speed internet, increasing investment in fiber infrastructure, and government efforts to improve connectivity in underserved areas. Market is characterized by potential for significant growth, albeit with economic volatility in some countries.

- Middle East and Africa (MEA): Significant investment in digital infrastructure driven by economic diversification efforts and smart city projects, particularly in the Gulf Cooperation Council (GCC) countries. Africa is seeing gradual but accelerating broadband penetration and leapfrogging older technologies with fiber and 5G.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Wired Telecommunication Carrier Market.- GlobalConnect Inc.

- NetworkLink Solutions

- FiberStream Corp.

- Unified Telecom Systems

- OptiNet Communications

- DataServe Holdings

- IntegraBroadband

- DigitalPathways Group

- PrimeTel Systems

- ConnectAll Networks

- InfraCom Technologies

- EliteFiber Solutions

- VantageConnect

- TrueLine Communications

- NexusNet Services

- BroadPath Services

- CoreLink Systems

- Universal Fibercom

- TeleMesh Group

- Quantum Wired Solutions

Frequently Asked Questions

What is the projected growth rate of the Wired Telecommunication Carrier Market?

The Wired Telecommunication Carrier Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033, driven by increasing data demand and infrastructure development.

How is AI impacting the Wired Telecommunication Carrier sector?

AI is significantly impacting the wired telecommunication sector by enabling automated network operations, predictive maintenance, enhanced cybersecurity, and personalized customer services, leading to greater efficiency and new service offerings.

What are the primary drivers for the Wired Telecommunication Carrier Market?

Key drivers include surging data consumption, global digital transformation initiatives, increasing demand for 5G network backhaul, and the expansion of smart city developments and government broadband programs.

What are the main challenges faced by wired telecommunication carriers?

Major challenges include high capital expenditure for infrastructure upgrades, intense competition from wireless alternatives, evolving cybersecurity threats, increasing network energy consumption, and complex regulatory landscapes.

Which region is expected to lead the growth in the Wired Telecommunication Carrier Market?

The Asia Pacific (APAC) region is expected to lead the growth due to rapid urbanization, extensive digitalization efforts, and significant government investments in broadband infrastructure across its emerging and developed economies.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted