Wafer Carrier Market

Wafer Carrier Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702223 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

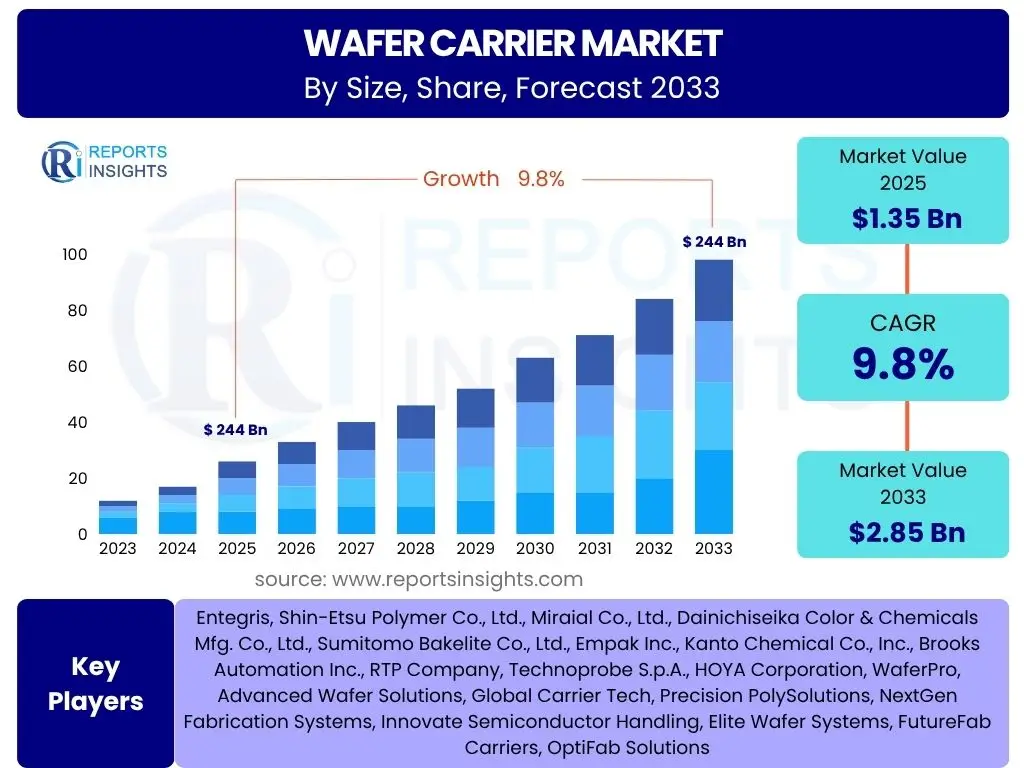

Wafer Carrier Market Size

According to Reports Insights Consulting Pvt Ltd, The Wafer Carrier Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.8% between 2025 and 2033. The market is estimated at USD 1.35 Billion in 2025 and is projected to reach USD 2.85 Billion by the end of the forecast period in 2033.

Key Wafer Carrier Market Trends & Insights

The wafer carrier market is experiencing dynamic shifts driven by advancements in semiconductor technology and manufacturing processes. Key trends indicate a strong emphasis on improving purity, enhancing structural integrity for smaller nodes, and integrating smart features to optimize fab automation. The increasing complexity of chip designs, including 3D ICs and advanced packaging techniques, necessitates carriers that can precisely protect and transport delicate wafers throughout the fabrication process, often under ultra-clean conditions. This pushes manufacturers to innovate in material science and design.

Furthermore, the global expansion of semiconductor manufacturing capacity, particularly in Asia Pacific, is a significant driver. New fab constructions and the upgrading of existing facilities are directly increasing the demand for high-performance wafer carriers. Manufacturers are also focusing on sustainable practices, exploring reusable or recyclable materials, and optimizing their production processes to reduce environmental impact, aligning with broader industry goals for green manufacturing.

The industry is also witnessing a surge in demand for specialized carriers for emerging materials like Silicon Carbide (SiC) and Gallium Nitride (GaN), which are critical for power electronics and high-frequency applications. These materials have different thermal and mechanical properties compared to traditional silicon, requiring bespoke carrier solutions that can withstand varying process conditions without compromising wafer integrity. This customization trend adds another layer of complexity and innovation to the market.

- Miniaturization and advanced packaging techniques demanding higher precision carriers.

- Rising adoption of EUV lithography requiring specialized, ultra-low particle contamination carriers.

- Growing investment in new fab construction and capacity expansion globally.

- Increasing focus on automation and smart carriers with integrated sensors for real-time tracking.

- Development of carriers for emerging semiconductor materials such as SiC and GaN.

- Emphasis on sustainable and reusable carrier solutions to reduce environmental impact.

- Integration of advanced materials to improve durability and chemical resistance.

AI Impact Analysis on Wafer Carrier

The integration of Artificial Intelligence (AI) and machine learning (ML) within semiconductor manufacturing is profoundly influencing the design, production, and utilization of wafer carriers. Users frequently inquire about AI's role in predictive maintenance for carrier lifespan, optimizing carrier logistics within automated fabs, and enhancing quality control to minimize wafer contamination. AI algorithms can analyze vast datasets from manufacturing lines to identify patterns indicative of potential carrier degradation, thereby enabling proactive replacement and reducing costly production interruptions.

Beyond maintenance, AI is crucial for optimizing the flow of wafer carriers through complex fabrication processes. By leveraging AI-powered scheduling and routing, fabs can improve throughput, reduce idle times, and prevent bottlenecks, directly impacting overall operational efficiency. This includes dynamic allocation of carriers based on real-time production demands and equipment availability. The ability of AI to process and interpret sensor data from smart carriers also facilitates enhanced traceability and inventory management, ensuring the right carrier is at the right place at the right time.

Furthermore, AI-driven inspection systems are revolutionizing quality control for wafer carriers. These systems can quickly and accurately detect microscopic defects, particles, or scratches on carrier surfaces that might otherwise compromise wafer integrity. This not only improves the overall quality of carriers but also contributes to higher yield rates in chip manufacturing by preventing contamination or damage during transport. The predictive capabilities of AI can even extend to optimizing carrier design for specific process steps, learning from past performance data to inform future material and structural improvements.

- AI-driven predictive maintenance for wafer carriers, extending lifespan and reducing downtime.

- Optimization of carrier logistics and routing within highly automated semiconductor fabs using AI algorithms.

- Enhanced quality control and defect detection on carrier surfaces through AI-powered vision systems.

- Real-time monitoring and data analysis from smart carriers for improved traceability and inventory management.

- AI-assisted design and material selection for new generation wafer carriers based on performance data.

- Improved production yield rates by mitigating carrier-related contamination or damage via AI insights.

Key Takeaways Wafer Carrier Market Size & Forecast

Common inquiries regarding the wafer carrier market's future center on its sustained growth trajectory, driven by an insatiable global demand for semiconductors. The market's expansion is intrinsically linked to investments in new fabrication plants and the continuous technological advancements in chip design and manufacturing processes. This consistent demand underpins the positive forecast, highlighting wafer carriers as indispensable components in the semiconductor ecosystem, critical for both protection and efficient handling of delicate silicon wafers.

A significant takeaway is the market's resilience and adaptability to evolving industry standards. As chip geometries shrink and new materials emerge, carrier manufacturers are compelled to innovate, offering solutions that meet increasingly stringent purity, structural, and automation requirements. This continuous innovation, coupled with the capital-intensive nature of semiconductor manufacturing, ensures a steady demand for high-performance and specialized carriers, reinforcing the market's long-term growth prospects.

Furthermore, the strategic importance of regional manufacturing hubs, particularly in Asia Pacific, is a key insight. Countries like Taiwan, South Korea, China, and Japan continue to lead in semiconductor production, directly influencing the demand for wafer carriers. This regional concentration not only drives market growth but also fosters intense competition and innovation among local and international suppliers, shaping the competitive landscape and technological direction of the wafer carrier market.

- The Wafer Carrier Market exhibits robust growth, projected to more than double by 2033, fueled by escalating global semiconductor demand.

- Continuous innovation in carrier design, materials, and smart features is essential to meet the evolving requirements of advanced chip manufacturing.

- Significant investments in new semiconductor fabrication facilities worldwide directly translate into increased demand for wafer carriers.

- Asia Pacific remains the dominant regional market, driven by the presence of major foundries and IDMs.

- The market is characterized by a strong emphasis on ultra-purity, structural integrity, and automation compatibility to safeguard high-value wafers.

Wafer Carrier Market Drivers Analysis

The wafer carrier market is propelled by several fundamental drivers stemming from the global semiconductor industry's robust growth and technological evolution. Increasing demand for electronic devices across various sectors, coupled with the continuous miniaturization of semiconductor components and the adoption of advanced packaging technologies, necessitates highly specialized and reliable wafer carriers. These carriers are indispensable for the safe and efficient transport of wafers throughout the complex and sensitive fabrication process, driving consistent demand.

Significant investments by leading semiconductor manufacturers in expanding their production capacities and establishing new fabrication plants globally are also key drivers. As fabs become more automated and sophisticated, the demand for smart, contamination-resistant, and durable carriers that can seamlessly integrate into advanced manufacturing environments continues to rise. This capital expenditure in new infrastructure directly translates into a higher volume requirement for wafer carriers, making them a critical component of factory modernization and expansion initiatives.

Furthermore, the advent of new material substrates like Silicon Carbide (SiC) and Gallium Nitride (GaN), critical for power electronics, EVs, and 5G infrastructure, presents a burgeoning market for specialized carriers. These materials often require carriers with enhanced thermal and chemical resistance properties, distinct from those used for traditional silicon wafers. The push for higher yield rates and reduced defects in advanced manufacturing also elevates the importance of high-quality, ultra-clean wafer carriers, encouraging innovation in material science and design within the market.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Semiconductor Industry & Advanced Packaging | +1.5% | Global, particularly Asia Pacific (Taiwan, South Korea, China), North America | Long-term (5+ years) |

| Increased Investments in New Fabrication Plants (Fabs) | +1.0% | Asia Pacific, North America, Europe | Mid-term (3-5 years) |

| Miniaturization of Chip Geometries & EUV Lithography Adoption | +0.8% | Global, especially advanced manufacturing regions | Short-to-Mid-term (1-5 years) |

| Rising Demand for Specialized Carriers for SiC/GaN Wafers | +0.7% | North America, Europe, Japan, China | Mid-term (3-5 years) |

| Focus on Fab Automation & Smart Manufacturing | +0.5% | Global | Short-term (1-3 years) |

Wafer Carrier Market Restraints Analysis

Despite robust growth, the wafer carrier market faces several restraints that can impede its expansion. One primary concern is the high cost associated with advanced wafer carriers, particularly those designed for ultra-low particle contamination and specific wafer sizes (e.g., 300mm). The use of high-purity, specialized materials and precision manufacturing processes drives up production costs, which can become a significant capital expenditure for semiconductor manufacturers, especially smaller foundries or those with older facilities seeking upgrades.

Another significant restraint is the stringent quality control and material compatibility requirements. Wafer carriers must maintain extremely low particle generation and outgassing properties to prevent contamination of delicate wafers, which are highly susceptible to defects. Meeting these rigorous purity standards often necessitates complex manufacturing environments and expensive testing protocols. Any failure in material compatibility or cleanliness can lead to significant yield losses for semiconductor manufacturers, making them hesitant to adopt new, unproven carrier technologies quickly.

Furthermore, the market can be constrained by global supply chain vulnerabilities and geopolitical tensions, which can disrupt the supply of critical raw materials or specialized components required for carrier manufacturing. Given the highly concentrated nature of the semiconductor supply chain, any regional instability or trade disputes can have ripple effects, leading to price volatility or delays in carrier delivery. The need for precise customization for various fabrication processes also limits economies of scale for some specialized carrier types, contributing to higher unit costs.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Manufacturing Costs of Advanced Carriers | -0.4% | Global | Long-term (5+ years) |

| Stringent Quality & Contamination Control Requirements | -0.3% | Global | Mid-term (3-5 years) |

| Supply Chain Vulnerabilities & Geopolitical Risks | -0.2% | Global, particularly Asia Pacific, North America | Short-to-Mid-term (1-5 years) |

| Limited Customization Options for Niche Applications | -0.15% | Global | Mid-term (3-5 years) |

| High Research & Development Investments | -0.1% | Global | Long-term (5+ years) |

Wafer Carrier Market Opportunities Analysis

The wafer carrier market is poised for significant opportunities driven by the accelerating pace of technological innovation in the semiconductor industry. The burgeoning demand for advanced memory solutions, high-performance computing (HPC), and artificial intelligence (AI) chips creates a need for carriers capable of handling ever more delicate wafers with increased precision. This translates into opportunities for developing next-generation carriers that can support smaller process nodes, higher wafer densities, and novel materials, driving innovation in design and functionality.

Emerging markets and new applications also present substantial growth avenues. Countries like China and India are rapidly expanding their domestic semiconductor manufacturing capabilities, leading to a surge in demand for all fab equipment, including wafer carriers. Beyond traditional computing, the proliferation of the Internet of Things (IoT), automotive electronics, and specialized industrial applications also generates a diverse range of requirements for wafer carriers, opening doors for custom solutions and niche market penetration.

Furthermore, the focus on sustainable manufacturing practices and the integration of smart technologies offer compelling opportunities. The development of eco-friendly, reusable, or recyclable carrier materials addresses environmental concerns and provides long-term cost benefits for fabs. Simultaneously, incorporating advanced sensors, RFID tags, and data analytics into carriers can transform them into "smart carriers," enabling real-time tracking, environmental monitoring, and predictive maintenance within automated factory environments, enhancing operational efficiency and yield management.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Smart Carriers with Integrated Sensors | +0.9% | Global, particularly North America, Europe, Japan | Mid-term (3-5 years) |

| Expansion into New & Emerging Semiconductor Markets | +0.8% | China, India, Southeast Asia | Long-term (5+ years) |

| Adoption of Sustainable & Recyclable Materials | +0.6% | Global, driven by corporate sustainability goals | Mid-to-Long-term (3-7 years) |

| Growth in Specialty Application Segments (e.g., MEMS, Photonics) | +0.5% | North America, Europe, Japan | Long-term (5+ years) |

| Strategic Partnerships for Integrated Fab Solutions | +0.4% | Global | Short-to-Mid-term (1-5 years) |

Wafer Carrier Market Challenges Impact Analysis

The wafer carrier market faces several significant challenges that demand continuous innovation and adaptation. One major hurdle is the relentless demand for higher purity and lower particle contamination in carriers as semiconductor manufacturing progresses to smaller nodes and more sensitive processes. Achieving and maintaining ultra-cleanliness throughout the carrier's lifecycle, from manufacturing to usage in the fab, is incredibly complex and costly, requiring advanced material science and stringent environmental controls. Any failure in this regard can lead to significant wafer defects and yield losses, impacting profitability for chip manufacturers.

Another critical challenge involves material compatibility and thermal stability. As new semiconductor materials like SiC and GaN become prevalent, and as processing temperatures vary, carriers must be designed to withstand diverse chemical and thermal environments without degradation or outgassing. Ensuring that carrier materials do not interact negatively with wafer surfaces or process chemistries, while maintaining structural integrity under extreme conditions, presents complex engineering problems that require substantial research and development investments. This constant need for material innovation can slow down product development cycles.

Furthermore, the rapid pace of technological change within the semiconductor industry means that wafer carrier designs can quickly become obsolete. Investments in specialized tooling and manufacturing lines for one generation of carriers might not be easily transferable to the next, posing a financial risk for manufacturers. The intense competitive landscape also puts pressure on pricing, forcing companies to balance high R&D costs with the need to offer competitive solutions. Navigating intellectual property rights and maintaining supply chain resilience in a globally interconnected yet sensitive industry also present ongoing operational and strategic challenges.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Maintaining Ultra-High Purity & Contamination Control | -0.5% | Global | Long-term (5+ years) |

| Material Compatibility & Thermal Stability for New Substrates | -0.4% | Global | Mid-term (3-5 years) |

| Rapid Technological Obsolescence & High R&D Costs | -0.3% | Global | Short-to-Mid-term (1-5 years) |

| Intellectual Property Protection & Counterfeit Products | -0.2% | Asia Pacific, North America | Mid-term (3-5 years) |

| Price Pressure & Intense Competition | -0.1% | Global | Short-term (1-3 years) |

Wafer Carrier Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global Wafer Carrier Market, offering valuable insights into its current landscape, future projections, and the key factors influencing its trajectory. The scope covers detailed market segmentation, competitive analysis of leading players, and regional dynamics. It aims to equip stakeholders with critical data and strategic recommendations to navigate the evolving demands of the semiconductor industry and capitalize on emerging opportunities.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.35 Billion |

| Market Forecast in 2033 | USD 2.85 Billion |

| Growth Rate | 9.8% |

| Number of Pages | 267 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Entegris, Shin-Etsu Polymer Co., Ltd., Miraial Co., Ltd., Dainichiseika Color & Chemicals Mfg. Co., Ltd., Sumitomo Bakelite Co., Ltd., Empak Inc., Kanto Chemical Co., Inc., Brooks Automation Inc., RTP Company, Technoprobe S.p.A., HOYA Corporation, WaferPro, Advanced Wafer Solutions, Global Carrier Tech, Precision PolySolutions, NextGen Fabrication Systems, Innovate Semiconductor Handling, Elite Wafer Systems, FutureFab Carriers, OptiFab Solutions |

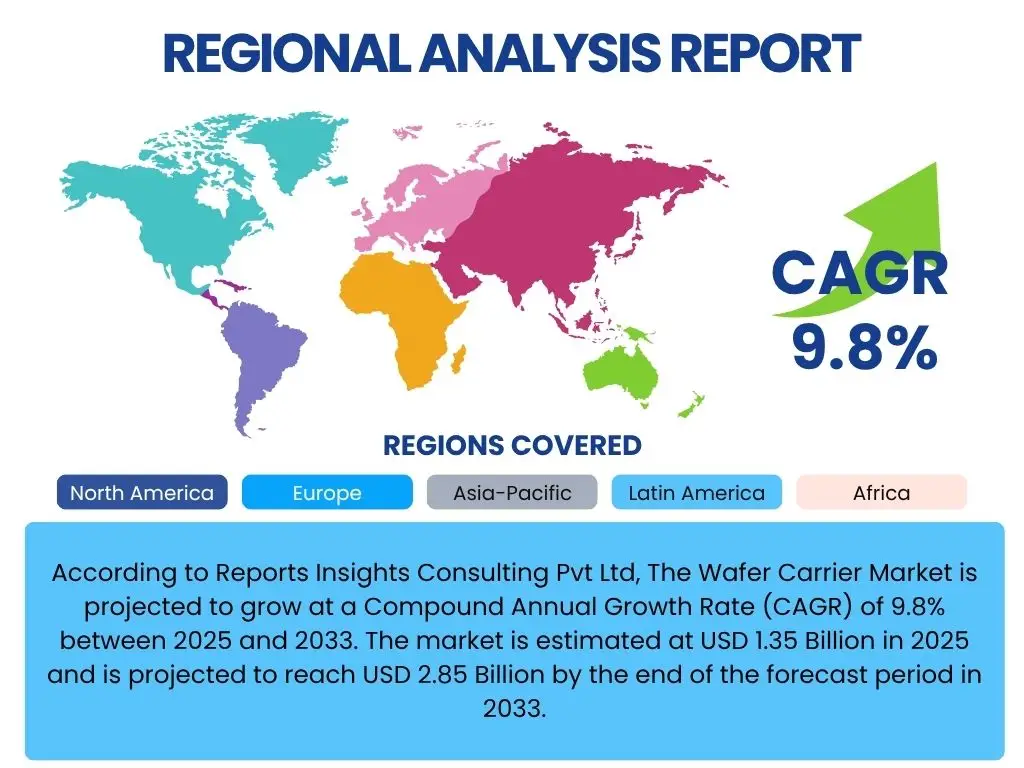

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The wafer carrier market is extensively segmented to provide a granular view of its diverse applications and product types, reflecting the varied requirements of the semiconductor manufacturing ecosystem. These segmentations are critical for understanding market dynamics, identifying specific growth opportunities, and tailoring solutions to meet the precise needs of different industry players. The market is primarily broken down by carrier type, material composition, wafer size compatibility, application within the semiconductor value chain, and the ultimate end-use industry.

- By Type:

- Front Opening Unified Pod (FOUP): Dominant for 300mm wafers, offering contamination control and automation compatibility.

- Front Opening Shipping Box (FOSB): Used primarily for shipping and transport of wafers between facilities.

- Open Cassette: Older technology, still used for smaller wafer sizes and less stringent cleanroom environments.

- Specialty Carriers: Custom solutions for unique processes, specific wafer shapes, or emerging materials.

- By Material:

- Polycarbonate: Cost-effective and widely used, offering good optical clarity and impact resistance.

- Polyether Ether Ketone (PEEK): High-performance polymer, known for excellent chemical and thermal resistance, suitable for harsh environments.

- Quartz: Provides superior purity and thermal stability, critical for high-temperature processes.

- Stainless Steel: Utilized in specific applications where robust mechanical properties and some chemical resistance are required.

- Advanced Polymers: Emerging materials offering enhanced properties like reduced outgassing or improved chemical resistance.

- Others (e.g., Ceramic Composites): Niche materials for highly specialized or experimental applications.

- By Wafer Size:

- 300mm: The largest segment, driven by advanced chip manufacturing.

- 200mm: Continues to be significant for mature technologies and specialty devices.

- 150mm & Below: Used for older technologies, MEMS, and niche applications.

- By Application:

- Integrated Device Manufacturers (IDMs): Companies that design, manufacture, and sell their own chips.

- Foundries: Companies that manufacture chips for other fabless companies.

- Outsourced Semiconductor Assembly and Test (OSAT): Providers of post-fabrication services, including assembly, packaging, and testing.

- Memory Manufacturers: Specialized companies producing memory chips like DRAM and NAND.

- Other Semiconductor Fabricators: Includes research institutions, academic labs, and smaller specialty producers.

- By End-Use Industry:

- Consumer Electronics: Smartphones, laptops, wearables, TVs.

- Automotive: Infotainment, ADAS, power electronics, sensors.

- Healthcare & Medical Devices: Diagnostic equipment, medical implants, imaging systems.

- Industrial & Automation: Robotics, industrial control systems, power management.

- IT & Telecommunication: Data centers, networking equipment, 5G infrastructure.

- Aerospace & Defense: Avionics, communication systems, ruggedized electronics.

Regional Highlights

- Asia Pacific (APAC): APAC dominates the wafer carrier market due to its position as the global hub for semiconductor manufacturing. Countries like Taiwan, South Korea, China, and Japan house the world's largest foundries, IDMs, and OSATs, driving immense demand for wafer carriers. Ongoing investments in new fab construction and expansion, particularly in China and Southeast Asia, further solidify the region's market leadership. The rapid adoption of advanced packaging and 300mm wafer technology also contributes significantly to this region's growth.

- North America: This region holds a substantial share of the wafer carrier market, propelled by significant investments in advanced research and development, particularly in leading-edge process technologies and AI chip development. The presence of major semiconductor equipment manufacturers and innovative fabless companies, coupled with government initiatives to strengthen domestic chip manufacturing capabilities, ensures steady demand for high-performance and specialty carriers.

- Europe: The European market for wafer carriers is characterized by strong emphasis on automotive electronics, industrial applications, and specialized semiconductor research. Countries like Germany, France, and the Netherlands are key players, with continuous investments in smart manufacturing and sustainable technologies. While not as large in volume as APAC, the region focuses on high-value, niche applications requiring advanced and custom wafer carrier solutions.

- Latin America, Middle East, and Africa (MEA): These regions represent emerging markets for wafer carriers, with nascent but growing semiconductor manufacturing capabilities. While smaller in market size currently, increasing digitalization, industrialization, and foreign direct investment in technology infrastructure are expected to drive gradual growth in demand for basic and advanced wafer carriers in the long term. Local fab developments and government support for high-tech industries will be crucial for their market expansion.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Wafer Carrier Market.| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted