Whole Blood Transfusion Filter Market

Whole Blood Transfusion Filter Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_706261 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

Whole Blood Transfusion Filter Market Size

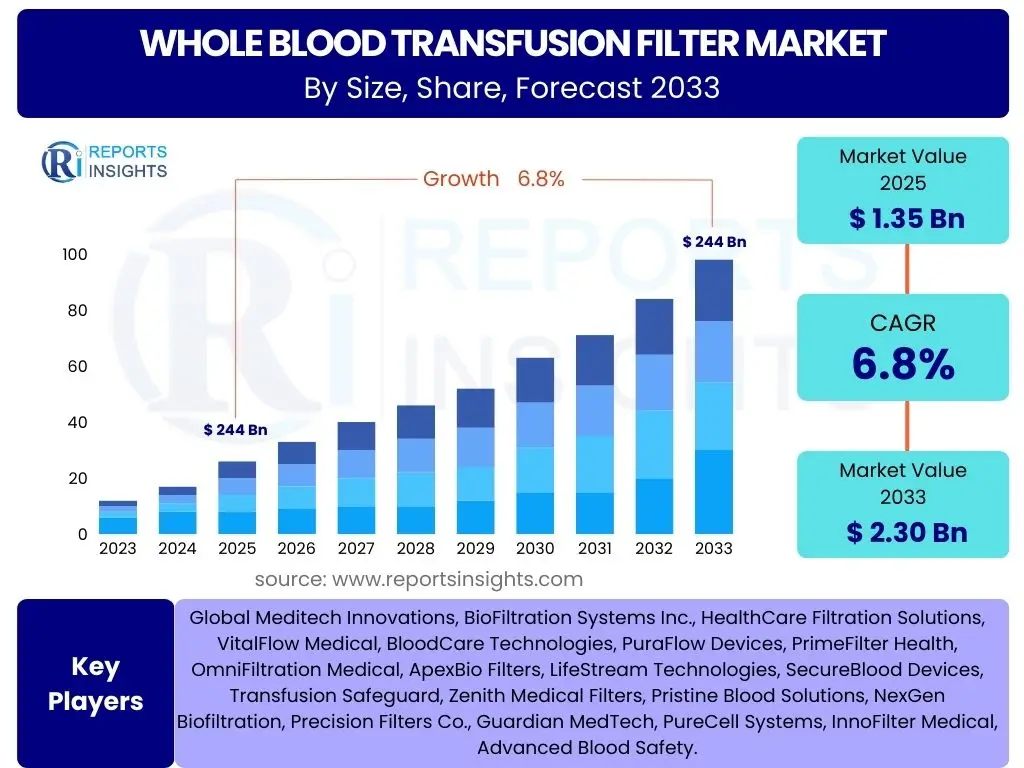

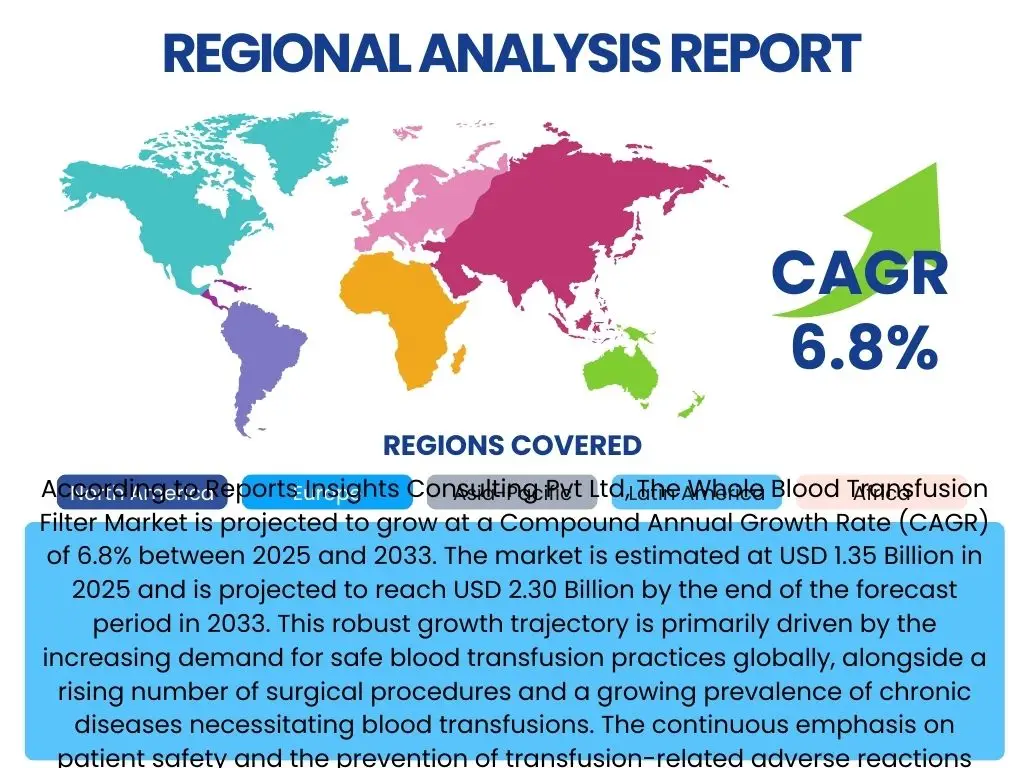

According to Reports Insights Consulting Pvt Ltd, The Whole Blood Transfusion Filter Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 1.35 Billion in 2025 and is projected to reach USD 2.30 Billion by the end of the forecast period in 2033. This robust growth trajectory is primarily driven by the increasing demand for safe blood transfusion practices globally, alongside a rising number of surgical procedures and a growing prevalence of chronic diseases necessitating blood transfusions. The continuous emphasis on patient safety and the prevention of transfusion-related adverse reactions are pivotal factors contributing to the market's expansion.

The market's valuation reflects the significant investment in healthcare infrastructure and advanced medical technologies across both developed and emerging economies. The projected increase in market size underscores the critical role that whole blood transfusion filters play in modern healthcare, ensuring the quality and safety of blood products before administration. This growth is also fueled by innovations in filtration technology, including the development of more efficient and biocompatible materials, which enhance the efficacy of these filters in removing harmful components like leukocytes, microaggregates, and pathogens from blood.

Key Whole Blood Transfusion Filter Market Trends & Insights

User inquiries about the Whole Blood Transfusion Filter market frequently revolve around emerging technologies, evolving regulatory landscapes, and the shifting preferences in blood processing. Common questions highlight concerns about improving filtration efficiency, reducing costs, and adapting to new medical guidelines. There is also a keen interest in the adoption of automated systems and the integration of smart technologies in blood management. These questions collectively point to a market striving for enhanced safety, operational efficiency, and broader accessibility of advanced filtration solutions.

The market is experiencing a significant shift towards more sophisticated filtration technologies designed to address specific transfusion-related complications, such as febrile non-hemolytic transfusion reactions and transfusion-related acute lung injury. Innovations are not only focused on improving the removal of residual leukocytes but also on ensuring the preservation of essential blood components. Furthermore, the increasing global awareness of blood-borne pathogens and the need for stricter blood safety protocols are accelerating the adoption of advanced filtration methods, influencing product development and market dynamics. This sustained focus on safety and efficacy is expected to continue driving technological advancements and market growth over the forecast period.

- Increased adoption of leukocyte reduction filters: Driven by guidelines advocating for their use to prevent transfusion-related complications.

- Technological advancements in filter materials and pore sizes: Leading to higher filtration efficiency and better preservation of blood components.

- Shift towards pre-storage leukocyte reduction: Becoming the standard practice in many blood banks to enhance safety and shelf life.

- Growing demand for bedside filtration: For specific patient populations or critical care scenarios requiring immediate filtration.

- Rise of integrated blood processing systems: Combining filtration with other blood component separation techniques for streamlined operations.

- Emphasis on cost-effectiveness and sustainability: Driving innovation in reusable or more environmentally friendly filter designs.

AI Impact Analysis on Whole Blood Transfusion Filter

Common user questions regarding AI's impact on the Whole Blood Transfusion Filter market often center on its potential to revolutionize blood inventory management, enhance donor screening processes, and improve the predictive capabilities for transfusion reactions. Users are curious about how AI can contribute to greater precision in blood component separation, reduce human error in laboratory settings, and optimize the overall blood supply chain. Concerns also include data privacy, the ethical implications of AI in healthcare, and the need for robust validation protocols to ensure AI-driven decisions are reliable and safe for patient outcomes. These inquiries highlight a collective anticipation for AI to bring efficiency and intelligence to traditional blood management practices.

The integration of Artificial intelligence (AI) is poised to significantly transform various facets of the blood transfusion ecosystem, indirectly influencing the demand and application of transfusion filters. AI algorithms can analyze vast datasets from donor histories, patient profiles, and transfusion outcomes to identify patterns that might indicate a higher risk of adverse reactions, thereby guiding more personalized transfusion protocols. This predictive capability could lead to more targeted use of filters, ensuring they are deployed where they offer the most benefit. Moreover, AI-driven solutions for optimizing inventory management in blood banks can minimize waste and ensure the availability of appropriate blood products, indirectly enhancing the overall efficiency of the transfusion process where filters are an integral part.

Furthermore, AI can play a crucial role in quality control and automation within blood processing centers. By employing machine vision and deep learning, AI systems can inspect filtered blood products for anomalies or incomplete filtration, providing real-time feedback that improves process consistency and reduces manual inspection errors. This enhanced oversight contributes to higher safety standards for filtered blood, potentially increasing trust and demand for filtered products. While AI may not directly manufacture filters, its pervasive influence on the operational efficiency, safety protocols, and predictive analytics in the blood transfusion sector will undoubtedly shape the market dynamics for transfusion filters by optimizing their deployment and underscoring their importance in a technologically advanced healthcare landscape.

- Enhanced donor screening and blood suitability assessment: AI algorithms can analyze complex donor data to predict potential risks and optimize blood donation collection, indirectly affecting the demand for specific filtration needs.

- Optimized blood inventory management: AI can predict demand and supply fluctuations, reducing waste and ensuring timely availability of filtered blood products.

- Predictive analytics for adverse transfusion reactions: AI can identify patient risk factors, leading to more targeted and safer transfusion practices, potentially increasing the demand for highly effective filters.

- Automated quality control and process monitoring: AI-powered systems can inspect filtration processes for efficacy and detect anomalies, ensuring high-quality filtered blood components.

- Personalized blood component therapy: AI could help tailor blood product selection and filtration requirements based on individual patient needs and genetic profiles.

Key Takeaways Whole Blood Transfusion Filter Market Size & Forecast

User queries regarding the key takeaways from the Whole Blood Transfusion Filter market size and forecast often focus on understanding the primary growth drivers, the most promising investment areas, and the critical challenges that could impede market progression. There's significant interest in identifying which regions offer the highest growth potential and how regulatory changes or technological innovations might reshape the competitive landscape. These questions underscore a desire for actionable insights to inform strategic decisions for stakeholders ranging from manufacturers to healthcare providers and investors.

The market is poised for sustained growth, largely driven by the imperative to enhance blood safety and the increasing volume of medical procedures globally that require blood transfusions. Innovations in filtration technology, particularly those that offer improved leukocyte reduction and broader pathogen inactivation capabilities, will be central to this growth. Additionally, the expansion of healthcare infrastructure in emerging economies presents substantial opportunities for market penetration. However, challenges related to the high cost of advanced filters and the need for greater awareness in certain regions will require strategic approaches to ensure widespread adoption. Overall, the market's trajectory is firmly upward, propelled by an unwavering commitment to patient well-being and advanced medical practices.

- Strong growth trajectory: Driven by increasing surgical procedures, rising chronic disease incidence, and growing demand for blood safety.

- Technological innovation as a key differentiator: Advanced filter materials and designs are crucial for market competitiveness.

- Regulatory landscape influence: Stricter guidelines for blood product safety are compelling broader adoption of filtration technologies.

- Emerging markets as significant growth avenues: Asia Pacific and Latin America present substantial untapped potential due to improving healthcare access.

- Patient safety at the forefront: The primary driver for end-user adoption and investment in high-quality filtration solutions.

Whole Blood Transfusion Filter Market Drivers Analysis

The Whole Blood Transfusion Filter market is significantly propelled by an escalating global demand for safe and high-quality blood products. A primary driver is the rising number of surgical procedures performed worldwide, including complex cardiovascular surgeries, organ transplants, and trauma-related interventions, all of which frequently necessitate blood transfusions. As these procedures become more common and accessible, the concomitant need for effective blood filtration to prevent transfusion-related complications, such as febrile non-hemolytic transfusion reactions, alloimmunization, and viral transmission, also increases, thereby boosting filter adoption.

Furthermore, the growing prevalence of chronic diseases like cancer, kidney failure, and various blood disorders, which often require regular blood transfusions for patient management, contributes substantially to market expansion. The increasing geriatric population, a demographic particularly susceptible to such conditions and requiring more frequent medical interventions, further amplifies the demand for safe blood products. Concurrently, stringent regulatory guidelines imposed by health authorities globally, emphasizing the importance of leukocyte reduction and pathogen inactivation in blood components, are compelling blood banks and hospitals to adopt advanced filtration technologies, ensuring compliance and enhancing patient safety.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Incidence of Chronic Diseases and Surgeries | +1.5% | Global, particularly North America, Europe, Asia Pacific | Short to Long-term (2025-2033) |

| Growing Awareness and Emphasis on Blood Safety | +1.2% | Global, particularly Developed Economies | Short to Mid-term (2025-2030) |

| Aging Population Requiring Transfusions | +0.8% | North America, Europe, Japan, China | Mid to Long-term (2027-2033) |

| Technological Advancements in Filtration Materials | +0.7% | Global, especially R&D Hubs | Mid-term (2027-2031) |

| Stringent Regulatory Guidelines for Blood Products | +0.6% | Europe, North America, Japan | Short-term (2025-2028) |

Whole Blood Transfusion Filter Market Restraints Analysis

Despite the robust growth drivers, the Whole Blood Transfusion Filter market faces several significant restraints that could temper its expansion. One prominent challenge is the relatively high cost associated with advanced filtration technologies, particularly for leukocyte reduction and pathogen removal filters. This cost can be prohibitive for healthcare facilities and blood banks in developing regions or those operating with limited budgets, potentially hindering widespread adoption, despite the clear clinical benefits. The economic burden is further compounded by the single-use nature of most filters, leading to ongoing operational expenses for healthcare providers.

Another crucial restraint is the inherent complexity and logistical challenges associated with maintaining a consistent and safe blood supply chain. Fluctuations in blood donor rates, difficulties in donor recruitment, and the need for highly specialized personnel to handle and process blood products can indirectly impact the demand and efficient utilization of filters. Furthermore, the risk of human error during the filtration process, despite technological advancements, and the potential for device malfunctions or integrity issues can lead to safety concerns, requiring constant vigilance and robust quality control measures that add to operational complexities and costs for healthcare providers.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Cost of Advanced Filtration Devices | -0.9% | Developing Economies, Budget-Constrained Facilities Globally | Short to Long-term (2025-2033) |

| Logistical Challenges in Blood Supply Management | -0.5% | Global, particularly Regions with Limited Infrastructure | Mid-term (2027-2031) |

| Lack of Awareness in Underdeveloped Regions | -0.4% | Africa, Parts of Asia, Latin America | Long-term (2029-2033) |

| Regulatory Hurdles and Compliance Complexities | -0.3% | Europe, North America | Short to Mid-term (2025-2030) |

| Alternative Treatment Options (e.g., Blood Substitutes Research) | -0.2% | Global, especially Research-Active Regions | Long-term (2030-2033) |

Whole Blood Transfusion Filter Market Opportunities Analysis

The Whole Blood Transfusion Filter market presents significant opportunities for growth, particularly through expansion into emerging economies. Countries in the Asia Pacific, Latin America, and Middle East & Africa regions are rapidly improving their healthcare infrastructure and increasing healthcare spending. This creates a burgeoning demand for advanced medical technologies, including blood transfusion filters, as these regions strive to elevate their blood safety standards to match those of developed nations. Strategic market entry and localized product development can unlock substantial untapped potential in these areas.

Furthermore, continuous innovation in filter technology offers a promising avenue for market expansion. The development of more efficient, cost-effective, and versatile filters, such as those capable of broad-spectrum pathogen inactivation or integrated multi-functional systems, can address current market gaps and create new demand. Opportunities also lie in fostering strategic collaborations between filter manufacturers, blood banks, and research institutions to develop next-generation solutions that are more patient-centric and adaptable to evolving clinical needs. The increasing focus on personalized medicine and targeted therapies may also drive demand for highly specialized filters designed for specific blood components or patient conditions, opening new niche markets within the broader transfusion filter landscape.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into Emerging Economies (APAC, LatAm, MEA) | +1.8% | Asia Pacific, Latin America, Middle East & Africa | Mid to Long-term (2027-2033) |

| Development of Advanced and Multi-Functional Filters | +1.5% | Global, especially Developed Markets | Short to Mid-term (2025-2030) |

| Strategic Collaborations and Partnerships | +1.0% | Global | Short to Mid-term (2025-2029) |

| Growing Demand for Point-of-Care Transfusion | +0.7% | North America, Europe | Mid-term (2028-2032) |

| Increasing Investment in Healthcare Infrastructure | +0.6% | China, India, Brazil, UAE | Long-term (2029-2033) |

Whole Blood Transfusion Filter Market Challenges Impact Analysis

The Whole Blood Transfusion Filter market faces several formidable challenges that could impede its growth and widespread adoption. One significant challenge is the ongoing intense competition from generic and low-cost filter manufacturers, particularly in price-sensitive markets. This pressure can erode profit margins for companies offering premium, technologically advanced filters, making it difficult to recoup substantial R&D investments. Ensuring product differentiation and demonstrating superior clinical outcomes becomes paramount in such a competitive landscape, requiring continuous innovation and robust marketing efforts.

Another critical challenge involves the complex and evolving regulatory landscape surrounding medical devices. Obtaining necessary approvals from diverse regulatory bodies across different countries can be a time-consuming and costly process, delaying market entry for new products. Additionally, maintaining compliance with stringent quality and safety standards, which are subject to frequent updates, demands significant resources and continuous monitoring from manufacturers. Furthermore, managing the logistical complexities of global supply chains for specialized medical devices, including issues like raw material procurement, manufacturing capacity, and distribution across varied geographical regions with distinct infrastructure challenges, poses an operational hurdle. These factors collectively require manufacturers to invest heavily in regulatory affairs, quality assurance, and resilient supply chain management to navigate the market effectively.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Competition from Generic/Low-Cost Filters | -0.8% | Global, especially Price-Sensitive Markets | Short to Long-term (2025-2033) |

| Stringent Regulatory Approval Processes | -0.6% | North America, Europe, Japan | Short to Mid-term (2025-2030) |

| Ethical and Safety Concerns Related to Transfusions | -0.5% | Global | Ongoing (2025-2033) |

| Maintaining Sterility and Efficacy Across Supply Chain | -0.4% | Global | Ongoing (2025-2033) |

| Disposal of Medical Waste and Environmental Impact | -0.3% | Global, particularly Developed Economies | Mid to Long-term (2028-2033) |

Whole Blood Transfusion Filter Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Whole Blood Transfusion Filter Market, covering market size estimations, growth forecasts, key trends, drivers, restraints, opportunities, and challenges. It offers a detailed segmentation analysis, regional insights, and profiles of leading market players, aiming to provide stakeholders with actionable intelligence for strategic decision-making in the dynamic healthcare sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.35 Billion |

| Market Forecast in 2033 | USD 2.30 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 265 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Meditech Innovations, BioFiltration Systems Inc., HealthCare Filtration Solutions, VitalFlow Medical, BloodCare Technologies, PuraFlow Devices, PrimeFilter Health, OmniFiltration Medical, ApexBio Filters, LifeStream Technologies, SecureBlood Devices, Transfusion Safeguard, Zenith Medical Filters, Pristine Blood Solutions, NexGen Biofiltration, Precision Filters Co., Guardian MedTech, PureCell Systems, InnoFilter Medical, Advanced Blood Safety. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Whole Blood Transfusion Filter market is intricately segmented to provide a comprehensive understanding of its diverse applications and technological nuances. This segmentation allows for a granular analysis of market dynamics across various product types, materials, end-user applications, and the specific blood components being filtered. Understanding these segments is crucial for identifying key growth areas, tailoring product development, and devising targeted marketing strategies that cater to the distinct needs of different healthcare settings and clinical requirements.

The segmentation highlights the specialization within the market, emphasizing the evolving demands for specific filtration characteristics. For instance, the distinction between leukocyte reduction filters and microaggregate filters reflects different primary clinical objectives, while segmentation by application (RBCs, Platelets, Plasma) underscores the varied processing requirements for each blood component. Analyzing these segments provides valuable insights into how technological advancements are addressing precise clinical challenges and how different end-users are adopting these solutions to enhance patient safety and optimize transfusion practices.

- By Type:

- Leukocyte Reduction Filters: Designed to remove white blood cells to prevent complications like febrile non-hemolytic transfusion reactions.

- Microaggregate Filters: Used to remove cellular debris and fibrin clots that form during blood storage.

- Bedside Filters: Applied at the patient's bedside immediately prior to transfusion.

- Pre-storage Filters: Used by blood banks to filter blood components before storage.

- Others: Including specialized filters for specific pathogens or unique clinical needs.

- By Material:

- Polyester: Commonly used for its filtration properties and biocompatibility.

- Polypropylene: Valued for its strength, chemical resistance, and wide applicability.

- Polyurethane: Utilized for its flexibility and specific filtration characteristics.

- Others: Encompassing advanced polymer blends and novel membrane materials.

- By Application:

- Red Blood Cells (RBCs): The most commonly filtered blood component.

- Platelets: Filtered to remove leukocytes and prevent alloimmunization.

- Plasma: Filtered to remove cellular debris and improve purity.

- Whole Blood: Filtration before separation or direct transfusion.

- By End-User:

- Hospitals: The largest end-user segment due to the high volume of transfusions.

- Blood Banks: Integral for large-scale processing and storage of filtered blood products.

- Ambulatory Surgical Centers (ASCs): Growing segment due to increasing outpatient surgical procedures.

- Specialty Clinics: Including oncology centers and dialysis centers requiring specific transfusion needs.

Regional Highlights

- North America: Dominates the market due to advanced healthcare infrastructure, high healthcare expenditure, increasing prevalence of chronic diseases, and stringent blood safety regulations. The presence of key market players and a strong focus on R&D also contribute to its leading position. The U.S. and Canada are significant contributors to regional growth, driven by high adoption rates of advanced filtration technologies and robust regulatory frameworks.

- Europe: Represents a substantial market share, driven by a well-established healthcare system, an aging population, and a high volume of surgical procedures. Strict European Union directives on blood safety and quality necessitate the widespread use of transfusion filters. Countries like Germany, France, and the UK are key contributors, emphasizing patient safety and continuous technological upgrades in blood management.

- Asia Pacific (APAC): Expected to witness the highest CAGR during the forecast period. This growth is attributed to improving healthcare infrastructure, rising disposable incomes, increasing awareness about blood safety, and a large patient pool. Emerging economies such as China, India, and Japan are experiencing a rapid expansion in their healthcare sectors, leading to increased adoption of modern blood transfusion practices and filters. Investments in public health and a growing medical tourism industry further bolster regional demand.

- Latin America: Shows promising growth potential, driven by increasing government initiatives to improve healthcare access and quality, alongside a rising number of medical facilities. Countries like Brazil and Mexico are investing in upgrading their blood processing capabilities, leading to higher adoption of transfusion filters. However, economic instability and varying regulatory landscapes present both opportunities and challenges.

- Middle East and Africa (MEA): Projected for steady growth, primarily fueled by increasing healthcare expenditure, a rising incidence of chronic diseases, and efforts to modernize healthcare infrastructure in key countries such as Saudi Arabia, UAE, and South Africa. While market penetration is currently lower compared to developed regions, growing awareness and international collaborations are expected to drive future adoption of blood transfusion filters.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Whole Blood Transfusion Filter Market.- Global Meditech Innovations

- BioFiltration Systems Inc.

- HealthCare Filtration Solutions

- VitalFlow Medical

- BloodCare Technologies

- PuraFlow Devices

- PrimeFilter Health

- OmniFiltration Medical

- ApexBio Filters

- LifeStream Technologies

- SecureBlood Devices

- Transfusion Safeguard

- Zenith Medical Filters

- Pristine Blood Solutions

- NexGen Biofiltration

- Precision Filters Co.

- Guardian MedTech

- PureCell Systems

- InnoFilter Medical

- Advanced Blood Safety

Frequently Asked Questions

What is a whole blood transfusion filter and why is it used?

A whole blood transfusion filter is a medical device designed to remove unwanted components from blood before or during transfusion. It is primarily used to remove leukocytes (white blood cells), microaggregates, and other particulate matter that can cause adverse reactions in patients, thereby enhancing transfusion safety and efficacy.

What are the primary types of whole blood transfusion filters?

The primary types include leukocyte reduction filters, which remove white blood cells; microaggregate filters, which remove small clots and cellular debris; and pre-storage or bedside filters, depending on when they are used in the blood processing or transfusion pipeline. Each type serves a specific purpose in improving blood product quality.

How do whole blood transfusion filters improve patient safety?

These filters significantly improve patient safety by reducing the risk of transfusion-related adverse events such as febrile non-hemolytic transfusion reactions, alloimmunization, and the transmission of certain viruses (e.g., CMV). By removing harmful components, they minimize inflammatory responses and enhance the therapeutic benefits of the transfusion.

What factors are driving the growth of the whole blood transfusion filter market?

Key growth drivers include the increasing number of surgical procedures requiring blood transfusions, the rising prevalence of chronic diseases, a growing aging population, and increasingly stringent regulatory guidelines for blood safety worldwide. Technological advancements in filtration materials also contribute significantly to market expansion.

What is the future outlook for the whole blood transfusion filter market?

The market is projected for robust growth, driven by continuous innovation in filtration technology, increasing demand for enhanced blood safety, and expanding healthcare infrastructure in emerging economies. The focus on preventing transfusion-related complications will continue to underscore the essential role of these filters in modern healthcare.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted