Welding Robot Market

Welding Robot Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703777 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

Welding Robot Market Size

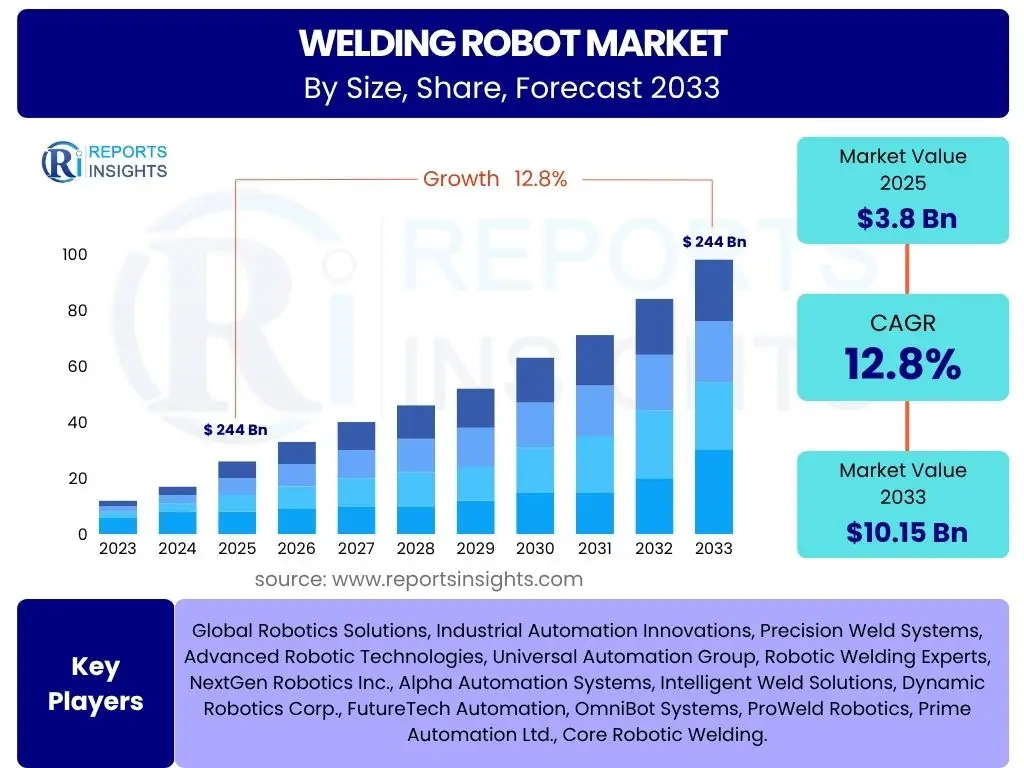

According to Reports Insights Consulting Pvt Ltd, The Welding Robot Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.8% between 2025 and 2033. The market is estimated at USD 3.8 billion in 2025 and is projected to reach USD 10.15 billion by the end of the forecast period in 2033.

Key Welding Robot Market Trends & Insights

The global welding robot market is undergoing significant transformation, driven by advancements in automation, increasing demand for manufacturing efficiency, and the integration of smart technologies. Users frequently inquire about the emerging technologies and shifts shaping the industry. A prominent trend is the widespread adoption of collaborative robots (cobots), which are designed to work safely alongside human operators, thereby lowering entry barriers for small and medium-sized enterprises (SMEs). This collaborative capability enhances flexibility and addresses labor shortages, making automation accessible to a broader range of industries beyond traditional heavy manufacturing.

Furthermore, the market is witnessing a surge in demand for highly intelligent and connected welding solutions. This includes the integration of advanced sensors, vision systems, and artificial intelligence, enabling robots to perform complex welds with greater precision, adapt to variations in materials, and conduct real-time quality checks. The push towards Industry 4.0 and smart factories is accelerating this trend, as manufacturers seek to create highly automated and data-driven production environments. These interconnected systems allow for predictive maintenance, optimized production flows, and reduced material waste, contributing significantly to operational cost savings and improved output quality.

Another critical insight is the growing emphasis on customization and versatility. Manufacturers are looking for welding robot solutions that can be easily reprogrammed and reconfigured for different tasks and production batches. This shift away from rigid, single-purpose automation towards more adaptable systems is crucial for industries facing diverse product lines and fluctuating market demands. The development of modular robotic systems and intuitive programming interfaces is facilitating this flexibility, ensuring that investments in welding automation remain relevant and productive over extended periods.

- Increased adoption of collaborative robots (cobots) for enhanced human-robot interaction.

- Integration of advanced sensing and vision systems for improved precision and quality.

- Rising demand for intelligent, AI-powered welding solutions for adaptive control.

- Emphasis on modular and flexible robotic systems for rapid retooling and diverse applications.

- Growing penetration of Industry 4.0 principles, including data analytics and predictive maintenance.

- Shift towards automation in new industries beyond traditional automotive and heavy machinery.

AI Impact Analysis on Welding Robot

The integration of Artificial Intelligence (AI) is fundamentally reshaping the capabilities and applications of welding robots, addressing common user questions regarding enhanced autonomy, efficiency, and quality control. AI algorithms enable robots to learn from diverse welding parameters, optimizing weld quality and consistency by adaptively adjusting to variations in material thickness, joint configuration, and environmental conditions. This cognitive capability allows for a significant reduction in human intervention, minimizing errors and rework, and consequently, lowering overall production costs. AI also facilitates advanced path planning, where robots can autonomously determine the most efficient and precise welding trajectories, further boosting operational speed and accuracy.

Beyond direct welding operations, AI plays a crucial role in predictive maintenance and quality assurance. By analyzing sensor data in real-time, AI models can detect early signs of equipment malfunction, predicting potential failures before they occur. This proactive approach minimizes downtime, extends the lifespan of robotic systems, and ensures continuous production. For quality control, AI-powered vision systems can inspect welds with unparalleled accuracy, identifying defects that might be missed by human inspection or traditional automated systems. This ensures higher product quality and compliance with stringent industry standards, which is a major concern for manufacturers.

Furthermore, AI is driving the development of more intuitive human-robot interfaces, making it easier for operators to program and manage complex welding tasks. Natural language processing and machine learning algorithms are enabling robots to understand verbal commands and learn from demonstrations, democratizing access to advanced automation. This addresses user concerns about the complexity of deploying robotic systems, fostering broader adoption across various industries, including those with limited prior automation experience. The long-term impact of AI on welding robots points towards fully autonomous, self-optimizing welding cells capable of handling diverse production requirements with minimal human oversight.

- Enhanced adaptive control for consistent weld quality across varying conditions.

- Optimized path planning and real-time adjustment for increased precision and speed.

- Predictive maintenance capabilities reducing downtime and extending equipment lifespan.

- Advanced defect detection and quality assurance through AI-powered vision systems.

- Simplified human-robot interaction and programming via machine learning and natural language processing.

- Potential for fully autonomous welding operations requiring minimal human supervision.

Key Takeaways Welding Robot Market Size & Forecast

Analyzing common user questions about the future trajectory of the welding robot market reveals a strong consensus on sustained growth, driven by an urgent need for manufacturing efficiency and automation across diverse sectors. The projected growth from USD 3.8 billion in 2025 to USD 10.15 billion by 2033, at a CAGR of 12.8%, underscores a robust market expansion. This significant increase highlights the increasing reliance of industries on automated welding solutions to overcome challenges such as skilled labor shortages, rising production costs, and the imperative for higher quality and faster output. The forecast indicates that welding robots are no longer just a niche solution for large enterprises but are becoming an integral part of modern manufacturing strategies for businesses of all sizes.

A crucial insight from the market forecast is the evolving role of welding robots from mere tools to intelligent, integrated systems. This evolution is propelled by technological advancements, particularly in AI, machine vision, and collaborative robotics, which are making these systems more versatile, precise, and user-friendly. The substantial market expansion suggests that industries are increasingly prioritizing investments in these sophisticated solutions to gain a competitive edge. This shift also reflects a growing understanding among manufacturers that automation is key to achieving consistency, reducing waste, and improving workplace safety, directly impacting their profitability and sustainability goals.

Furthermore, the geographic distribution of this growth indicates strong adoption rates in traditionally industrialized regions, alongside rapid expansion in emerging economies. The market forecast implies that as global supply chains continue to evolve and localized manufacturing gains traction, the demand for adaptable and efficient welding automation will only intensify. This makes the welding robot market a highly attractive sector for technology providers, investors, and manufacturers looking to modernize their operations and meet the demands of a rapidly changing global economy. The consistent double-digit growth rate signals a profound and lasting transformation in industrial production methodologies worldwide.

- Significant market expansion from USD 3.8 billion in 2025 to USD 10.15 billion by 2033.

- Consistent double-digit CAGR of 12.8% indicates strong and sustained adoption.

- Automation imperative driven by skilled labor shortages and efficiency demands.

- Technological advancements in AI and collaborative robotics are key growth enablers.

- Increasing integration of welding robots into comprehensive Industry 4.0 frameworks.

- Strong investment opportunities across developed and emerging economies for automation solutions.

Welding Robot Market Drivers Analysis

The welding robot market is propelled by a confluence of powerful drivers, each contributing significantly to its accelerated growth. A primary factor is the global shortage of skilled welders, compelling manufacturers to invest in automation to maintain production levels and quality standards. Robotic welding systems offer a consistent, high-quality alternative that mitigates reliance on increasingly scarce human expertise. This demographic shift in the labor force, particularly in industrialized nations, makes robotic solutions an indispensable part of future manufacturing strategies. Manufacturers are actively seeking ways to bridge this skills gap, leading to sustained demand for automated welding.

Another crucial driver is the relentless pursuit of increased manufacturing efficiency and productivity. Welding robots operate with superior speed, precision, and repeatability compared to manual methods, leading to higher throughput, reduced cycle times, and lower material waste. The ability to perform continuous operations without fatigue enables factories to optimize production schedules and meet demanding output targets. Additionally, the enhanced quality and consistency achieved through robotic welding result in fewer defects and less rework, directly translating to significant cost savings and improved customer satisfaction. This efficiency imperative is universally relevant across manufacturing sectors, driving widespread adoption.

Furthermore, the growing emphasis on workplace safety and compliance with stringent industrial regulations acts as a significant catalyst. Manual welding involves exposure to hazardous conditions such as intense heat, UV radiation, fumes, and sparks, posing considerable health risks to human operators. Deploying welding robots removes personnel from these dangerous environments, thereby enhancing worker safety, reducing occupational injuries, and lowering associated healthcare costs and liability. This commitment to creating safer working conditions is a key motivator for industrial automation, aligning with corporate responsibility initiatives and regulatory mandates globally.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Acute shortage of skilled welders globally | +3.5% | North America, Europe, Asia Pacific (China, Japan) | 2025-2033 (Long-term) |

| Increasing demand for enhanced manufacturing efficiency and productivity | +3.0% | Global (esp. Automotive, Metal Fabrication, Electronics) | 2025-2033 (Ongoing) |

| Rising focus on workplace safety and compliance with regulations | +2.5% | North America, Europe, Developed Asia Pacific | 2025-2033 (Continuous) |

| Technological advancements and integration of AI/IoT | +2.0% | Global (esp. Technology-forward regions) | 2025-2030 (Mid-term) |

| Growth in automotive, electronics, and general manufacturing industries | +1.8% | Asia Pacific (China, India), Europe, North America | 2025-2033 (Long-term) |

Welding Robot Market Restraints Analysis

Despite robust growth, the welding robot market faces several significant restraints that could impede its full potential. A primary hurdle is the high initial capital investment required for purchasing and implementing robotic welding systems. This includes not only the cost of the robot itself but also expenditures for peripheral equipment, safety enclosures, specialized tooling, and software. For small and medium-sized enterprises (SMEs) with limited budgets, this upfront cost can be prohibitive, acting as a major barrier to adoption even when the long-term benefits are clear. The return on investment (ROI) period can also be perceived as too long by some decision-makers, especially in volatile economic conditions.

Another key restraint is the complexity associated with the integration and programming of welding robots. Implementing these advanced systems often requires significant technical expertise in robotics, automation, and specific welding processes. Companies may struggle to find or train qualified personnel capable of programming, operating, and maintaining these robots, leading to higher operational costs or delays in full utilization. The learning curve for new robotic systems can be steep, and the need for specialized knowledge can deter potential adopters who lack the necessary internal resources or prefer simpler, less capital-intensive solutions.

Furthermore, economic downturns and fluctuations in industrial production can significantly impact market growth. During periods of economic uncertainty, businesses tend to scale back on capital expenditures and delay investments in new automation technologies. Industries heavily reliant on welding, such as automotive, construction, and heavy machinery, are particularly susceptible to economic cycles. A slowdown in these key end-user sectors directly translates to reduced demand for welding robots, as companies prioritize cost-cutting measures over long-term automation projects. This external economic volatility introduces an element of unpredictability to market forecasts and adoption rates.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High initial capital investment and integration costs | -2.5% | Global (esp. SMEs, developing economies) | 2025-2033 (Ongoing) |

| Complexity of programming and lack of skilled operators | -2.0% | Global (esp. regions with less automation expertise) | 2025-2030 (Mid-term) |

| Economic slowdowns and geopolitical uncertainties | -1.8% | Global (region-dependent) | Short-term (cyclical) |

| Perceived inflexibility for highly customized, low-volume production | -1.2% | Various (Custom fabrication, niche markets) | 2025-2033 (Long-term) |

| Cybersecurity concerns related to interconnected systems | -0.8% | Developed regions (High industrial digitization) | 2025-2033 (Emerging) |

Welding Robot Market Opportunities Analysis

The welding robot market is ripe with opportunities that promise to accelerate its growth trajectory and expand its application across diverse industries. A significant avenue for expansion lies in the burgeoning demand for automation in emerging economies. As countries in Asia Pacific, Latin America, and Africa industrialize and modernize their manufacturing infrastructure, they are increasingly seeking efficient and cost-effective production solutions. These regions often face challenges similar to developed nations, such as labor shortages and the need for improved quality, making welding robots an attractive investment for rapid industrial scaling and competitive positioning in the global market. The lower labor costs in these regions are gradually being offset by the benefits of consistency and speed that automation offers.

The continuous evolution of collaborative robots (cobots) presents another substantial opportunity. Cobots are designed to be more affordable, easier to program, and safer to operate alongside humans, making them highly suitable for small and medium-sized enterprises (SMEs) that traditionally found industrial robots too complex or expensive. This segment of the market represents an untapped potential, as SMEs look to adopt automation incrementally without massive upfront investments or extensive factory reconfigurations. The simplified deployment and enhanced flexibility of cobots are lowering the barriers to entry, enabling a wider range of businesses to integrate robotic welding into their operations, fostering market penetration across previously underserved segments.

Furthermore, the increasing integration of welding robots with advanced manufacturing technologies like additive manufacturing (3D printing) and smart factory ecosystems (Industry 4.0) opens up new application possibilities. Robotic systems can be utilized for post-processing of 3D-printed metal parts, enhancing their structural integrity and surface finish. The broader Industry 4.0 movement facilitates seamless data exchange, predictive analytics, and remote monitoring of welding processes, maximizing efficiency and enabling new levels of customization and quality control. This convergence of technologies creates demand for highly sophisticated, interconnected welding solutions that offer significant competitive advantages and drive innovation within the manufacturing landscape.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing demand from emerging economies for automation | +3.0% | Asia Pacific (India, Southeast Asia), Latin America, MEA | 2025-2033 (Long-term) |

| Development and increasing adoption of collaborative robots (cobots) | +2.5% | Global (esp. SMEs, general manufacturing) | 2025-2030 (Mid-term) |

| Integration with Industry 4.0, IoT, and smart factory initiatives | +2.0% | Developed economies, tech-forward industries | 2025-2033 (Ongoing) |

| Expansion into new application areas (e.g., construction, aerospace, shipbuilding) | +1.5% | Global (Diversified industries) | 2025-2033 (Long-term) |

| Customization and modularity for tailored solutions | +1.0% | Global (Niche markets, complex fabrication) | 2025-2030 (Mid-term) |

Welding Robot Market Challenges Impact Analysis

The welding robot market, while growing, faces specific challenges that require strategic navigation to ensure sustained expansion. One significant hurdle is the persistent lack of standardized global safety regulations and interoperability protocols. The absence of universally accepted standards can lead to fragmentation in product design and integration, making it difficult for manufacturers to develop universally compatible solutions. This also complicates cross-border deployment and can increase costs associated with adapting systems to varying national safety requirements. Harmonization of these standards is crucial for streamlining market entry and encouraging broader adoption, particularly for global enterprises.

Another major challenge lies in the rapid pace of technological change and the potential for obsolescence. As new advancements in robotics, AI, and materials science emerge, existing robotic welding systems can quickly become outdated. This creates pressure on manufacturers to continuously invest in research and development to stay competitive, while end-users face the dilemma of investing in expensive equipment that might have a shorter technological lifespan than anticipated. The need for constant upgrades and compatibility issues with legacy systems can deter potential buyers or lead to higher total cost of ownership over time, especially for businesses with long-term investment horizons.

Furthermore, the public perception and potential societal impact, particularly concerning job displacement, present a delicate challenge. While automation brings efficiency and safety benefits, concerns about robots replacing human workers are prevalent, especially in regions with high unemployment or strong labor unions. Addressing these concerns requires clear communication about the creation of new, higher-skilled jobs in robot operation, maintenance, and programming, as well as the overall economic benefits of increased productivity. Overcoming this perception challenge through effective workforce retraining programs and policy initiatives is vital for ensuring societal acceptance and fostering a conducive environment for automation adoption.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Lack of standardized global safety and interoperability regulations | -1.5% | Global (cross-border operations) | 2025-2033 (Long-term) |

| Rapid technological advancements leading to obsolescence | -1.0% | Global (especially developed markets) | 2025-2030 (Mid-term) |

| Public perception and concerns about job displacement | -0.8% | Global (varying by economic conditions and labor policies) | 2025-2033 (Ongoing) |

| High maintenance and operational costs post-installation | -0.7% | Global (SMEs, cost-sensitive industries) | 2025-2033 (Long-term) |

| Integration complexity with existing legacy systems | -0.5% | Established manufacturing regions | 2025-2030 (Mid-term) |

Welding Robot Market - Updated Report Scope

This comprehensive market report offers an in-depth analysis of the global welding robot market, providing stakeholders with critical insights into market dynamics, segmentation, and regional trends. It covers historical data from 2019 to 2023, establishes 2024 as the base year, and projects market performance through 2033, enabling a strategic outlook on industry growth and opportunities. The report's scope encompasses a detailed examination of market size and forecast, key drivers, restraints, opportunities, and challenges influencing market trajectory. Furthermore, it provides an extensive segmentation analysis, breaking down the market by various dimensions to offer granular insights into different product types, applications, and end-user industries.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 3.8 billion |

| Market Forecast in 2033 | USD 10.15 billion |

| Growth Rate | 12.8% |

| Number of Pages | 250 |

| Key Trends | |

| Segments Covered | |

| Key Companies Covered | Global Robotics Solutions, Industrial Automation Innovations, Precision Weld Systems, Advanced Robotic Technologies, Universal Automation Group, Robotic Welding Experts, NextGen Robotics Inc., Alpha Automation Systems, Intelligent Weld Solutions, Dynamic Robotics Corp., FutureTech Automation, OmniBot Systems, ProWeld Robotics, Prime Automation Ltd., Core Robotic Welding. |

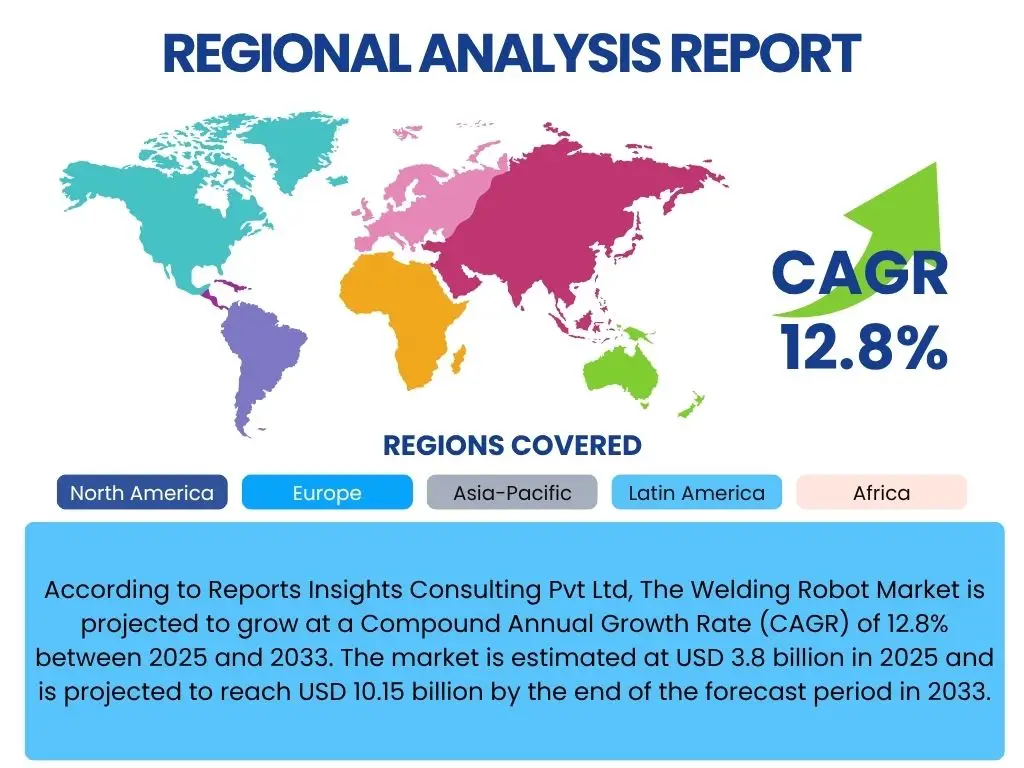

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The global welding robot market is meticulously segmented to provide a comprehensive understanding of its diverse facets and varying dynamics across different product types, applications, and end-user industries. This granular breakdown allows stakeholders to identify specific growth opportunities and tailor strategies for targeted market segments. The segmentation by type typically includes major categories such as arc welding robots, spot welding robots, and laser welding robots, each catering to distinct welding processes and material requirements. Understanding the market share and growth rates within these types is crucial for technology developers and robot manufacturers.

Further segmentation by application highlights the dominant industries adopting welding robots, with the automotive sector historically leading in integration due to its high-volume, precision manufacturing needs. However, the market is increasingly expanding into general manufacturing, heavy machinery, electronics, and construction, driven by the broader imperative for automation. Analyzing these application segments helps in identifying emerging consumer bases and areas where robotic solutions can provide the most significant impact on productivity and quality. The expansion into new applications signifies the growing versatility and adaptability of modern welding robots beyond traditional industrial strongholds.

Moreover, the market is segmented by components, detailing the various parts that constitute a complete robotic welding system, including the robot arm, controller, power source, and advanced vision systems. This component-level analysis provides insights into the supply chain, key technology providers, and areas of future innovation. Finally, end-user industry segmentation offers a vertical perspective, detailing how different industrial sectors are leveraging welding robots to meet their unique production challenges and operational goals. This holistic segmentation approach ensures a thorough and actionable understanding of the intricate market landscape.

- By Type: Arc Welding Robots, Spot Welding Robots, Laser Welding Robots, Resistance Welding Robots, Other Welding Robots.

- By Application: Automotive, Heavy Machinery, General Manufacturing, Electronics & Electrical, Construction, Shipbuilding, Aerospace & Defense, Others.

- By Component: Robot Arm, Controller, Power Source, Welding Gun/Torch, Sensors & Vision Systems, Software, Other Peripherals.

- By End User Industry: Automotive & Transportation, Metal Fabrication & Machinery, Electronics & Semiconductors, Construction & Infrastructure, Energy, Aerospace, Others.

- By Robot Type: Articulated Robots, SCARA Robots, Cartesian Robots, Collaborative Robots (Cobots), Cylindrical Robots.

Regional Highlights

- Asia Pacific (APAC): Dominates the market due to robust manufacturing growth, high adoption in automotive and electronics, increasing labor costs, and government initiatives supporting industrial automation in countries like China, Japan, South Korea, and India.

- Europe: A mature market characterized by advanced technological adoption, emphasis on Industry 4.0, skilled labor shortages, and strong presence of automotive and machinery industries, with Germany, Italy, and Scandinavia as key contributors.

- North America: Significant growth driven by reshoring initiatives, increasing demand for automation to boost competitiveness, and investments in advanced manufacturing technologies, particularly in the automotive, aerospace, and general manufacturing sectors across the United States and Canada.

- Latin America: Emerging market with increasing industrialization, particularly in Brazil and Mexico, witnessing growing adoption of welding robots to enhance efficiency and product quality in manufacturing sectors.

- Middle East and Africa (MEA): Nascent but rapidly growing market, spurred by diversification efforts away from oil economies, infrastructure development, and investments in manufacturing capabilities, though adoption rates vary by country.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Welding Robot Market.- Global Robotic Solutions

- Industrial Automation Innovations

- Precision Weld Systems

- Advanced Robotic Technologies

- Universal Automation Group

- Robotic Welding Experts

- NextGen Robotics Inc.

- Alpha Automation Systems

- Intelligent Weld Solutions

- Dynamic Robotics Corp.

- FutureTech Automation

- OmniBot Systems

- ProWeld Robotics

- Prime Automation Ltd.

- Core Robotic Welding

- Automated Weld Systems

- Smart Robot Welders

- Integrated Robotics Co.

- Premier Automation Solutions

- Quantum Robotics

Frequently Asked Questions

What is the projected growth of the Welding Robot Market?

The Welding Robot Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 12.8% between 2025 and 2033, expanding from USD 3.8 billion in 2025 to USD 10.15 billion by 2033.

How does AI impact welding robot capabilities?

AI significantly enhances welding robot capabilities through adaptive control for consistent quality, optimized path planning, predictive maintenance, advanced defect detection via vision systems, and simplified human-robot interaction for easier programming and operation.

What are the primary drivers for the Welding Robot Market?

Key drivers include the global shortage of skilled welders, increasing demand for manufacturing efficiency and productivity, and a growing focus on workplace safety and regulatory compliance. Technological advancements in AI and IoT also play a significant role.

What are the main restraints to market growth?

Major restraints include the high initial capital investment required for robotic systems, the complexity associated with programming and integration, and the lack of readily available skilled operators. Economic slowdowns and technological obsolescence also pose challenges.

Which regions are leading in welding robot adoption?

Asia Pacific (especially China, Japan, South Korea), Europe (Germany, Italy), and North America (United States) are leading regions in welding robot adoption, driven by strong manufacturing bases and ongoing automation initiatives.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted