Weighing and Inspection Equipment Market

Weighing and Inspection Equipment Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702808 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

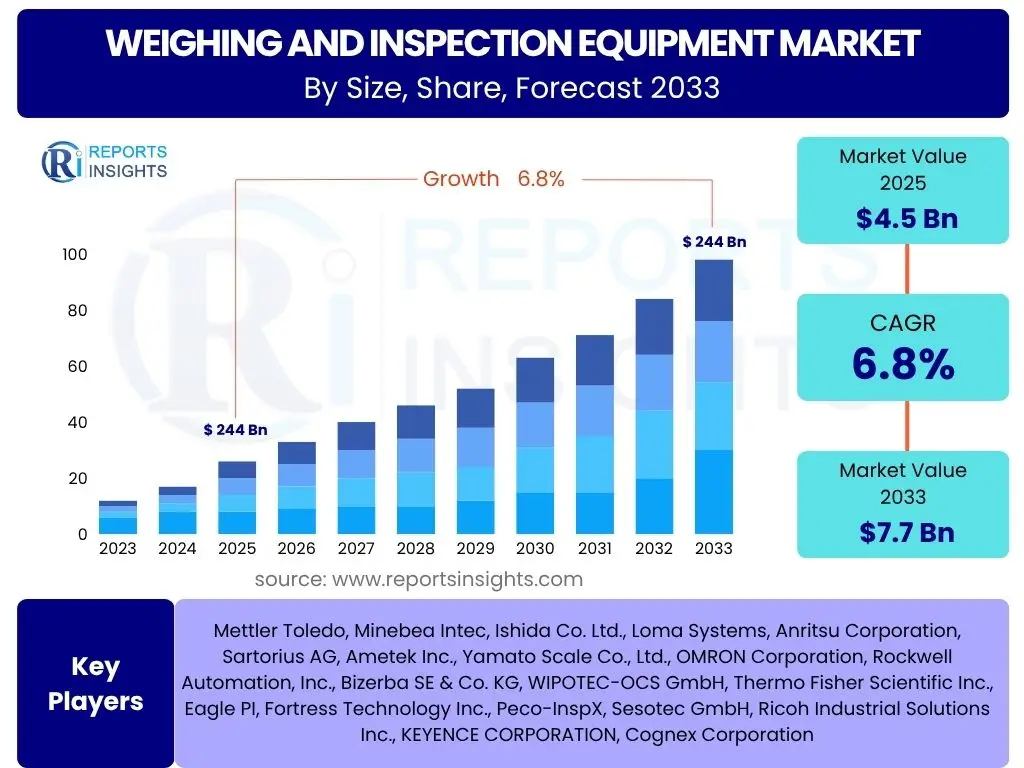

Weighing and Inspection Equipment Market Size

According to Reports Insights Consulting Pvt Ltd, The Weighing and Inspection Equipment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 4.5 Billion in 2025 and is projected to reach USD 7.7 Billion by the end of the forecast period in 2033. This growth is primarily fueled by increasing automation across various industries, stringent regulatory frameworks demanding higher quality control, and the expanding global manufacturing sector's need for precision and efficiency.

The market's expansion is also influenced by the accelerating pace of technological innovation, including the integration of advanced sensors, IoT, and artificial intelligence into weighing and inspection systems. These advancements enhance accuracy, speed, and overall operational efficiency, making them indispensable for modern production lines. Furthermore, the rising consumer awareness regarding product safety and quality, particularly in the food and pharmaceutical sectors, continues to drive demand for sophisticated inspection solutions.

Key Weighing and Inspection Equipment Market Trends & Insights

The Weighing and Inspection Equipment market is undergoing significant transformation, driven by a confluence of technological advancements and evolving industry demands. Users frequently inquire about the impact of Industry 4.0, the rise of smart factories, and the growing emphasis on sustainability and product safety. The market is witnessing a strong shift towards highly integrated, automated, and data-driven solutions that offer enhanced precision, real-time monitoring capabilities, and reduced human intervention. This reflects a broader industry push for operational excellence, waste reduction, and compliance with increasingly stringent global standards.

Another prominent trend is the increasing adoption of multi-functional systems that combine various inspection technologies, such as checkweighing with metal detection or X-ray inspection, into a single unit. This integration optimizes factory floor space, streamlines processes, and reduces capital expenditure for manufacturers. Furthermore, the demand for equipment capable of handling diverse product types and packaging formats is growing, fueled by the diversification of consumer goods and the expansion of e-commerce. The focus on predictive maintenance and remote diagnostics through connected devices is also gaining traction, promising improved uptime and lower total cost of ownership for end-users.

- Industry 4.0 and IoT Integration: Seamless connectivity and data exchange for smart manufacturing.

- Increased Automation and Robotics: Reducing manual labor and improving consistency and speed.

- Advanced Sensor Technology: Enhancing detection capabilities for minute defects and foreign objects.

- Artificial Intelligence and Machine Learning: Enabling predictive maintenance, anomaly detection, and self-optimization.

- Miniaturization and Portability: Development of compact and mobile inspection solutions for flexible deployment.

- Sustainability Focus: Energy-efficient designs and reduced material waste during production and inspection.

- Stricter Regulatory Compliance: Driving demand for high-accuracy and verifiable inspection systems, especially in food, pharma, and medical devices.

- Growth of E-commerce and Logistics: Increasing need for efficient parcel weighing and dimensioning systems.

AI Impact Analysis on Weighing and Inspection Equipment

Common user inquiries regarding AI's impact on Weighing and Inspection Equipment often revolve around its potential to enhance accuracy, improve efficiency, and enable predictive capabilities. Users are keen to understand how AI can automate complex decision-making, reduce false positives, and contribute to overall operational intelligence within manufacturing and logistics environments. The pervasive sentiment is that AI holds the key to unlocking new levels of performance and cost-effectiveness, moving beyond traditional rule-based systems to more adaptive and intelligent inspection processes.

Artificial intelligence is profoundly transforming the weighing and inspection equipment landscape by enabling unprecedented levels of precision, speed, and analytical depth. AI-powered vision systems can identify intricate defects at high throughputs that might be invisible or too time-consuming for human operators. Machine learning algorithms contribute to predictive maintenance by analyzing equipment performance data to anticipate failures, thereby minimizing downtime and extending asset lifespan. Furthermore, AI facilitates real-time process optimization, allowing systems to autonomously adjust parameters based on incoming data, ensuring consistent product quality and reducing waste. While adoption requires initial investment in data infrastructure and skilled personnel, the long-term benefits in terms of enhanced efficiency, reduced operational costs, and superior product integrity are substantial.

- Enhanced Anomaly Detection: AI algorithms can identify subtle deviations and defects with higher accuracy than traditional methods.

- Predictive Maintenance: Analyzing equipment data to anticipate failures, reducing downtime and optimizing service schedules.

- Automated Calibration and Self-Optimization: AI enables systems to adapt and calibrate autonomously, maintaining optimal performance.

- Reduced False Rejects: Machine learning improves the differentiation between actual defects and benign variations, minimizing product waste.

- Real-time Data Analysis and Reporting: Providing actionable insights for process improvement and quality control.

- Improved Throughput: AI-driven systems can process and inspect products at higher speeds without compromising accuracy.

- Adaptive Inspection Protocols: AI allows systems to learn from new data and adjust inspection criteria for evolving product lines or standards.

Key Takeaways Weighing and Inspection Equipment Market Size & Forecast

User questions about key takeaways from the Weighing and Inspection Equipment market size and forecast consistently highlight the market's robust growth trajectory, driven by an increasing global emphasis on automation, product quality, and regulatory compliance. The primary insight is that this market is not merely expanding in volume but also evolving in sophistication, with technological advancements such as AI and IoT integration playing a pivotal role in shaping its future. The forecast indicates sustained demand across diverse industries, cementing the equipment's essential role in modern supply chains and manufacturing processes.

The market's resilience is further demonstrated by its critical function in ensuring consumer safety and adherence to international standards, particularly in sectors like food and pharmaceuticals. The long-term outlook remains positive, underpinned by continuous investment in research and development, which introduces more efficient, accurate, and integrated solutions. Companies that prioritize innovation and strategic partnerships to address specific industry needs are well-positioned to capitalize on these growth opportunities. Overall, the market is poised for significant expansion, making it a crucial area for investment and technological development.

- Strong Growth Trajectory: Projected substantial increase in market size from 2025 to 2033.

- Technological Integration is Key: Adoption of Industry 4.0, AI, and IoT solutions drives market value.

- Automation as a Core Driver: Increasing demand for automated systems across manufacturing and logistics.

- Regulatory Compliance Imperative: Stringent quality and safety regulations boost equipment demand.

- Diversification Across Industries: Growth observed beyond traditional sectors into new applications.

- Focus on Efficiency and Accuracy: End-users prioritize solutions that enhance operational effectiveness and product integrity.

Weighing and Inspection Equipment Market Drivers Analysis

The Weighing and Inspection Equipment market is propelled by several robust drivers, primarily the escalating global emphasis on industrial automation and the pervasive need for stringent quality control across diverse manufacturing sectors. The increasing adoption of smart factory concepts and the advent of Industry 4.0 necessitate advanced and integrated weighing and inspection solutions that can operate autonomously and provide real-time data. This push for automation enhances production efficiency, reduces human error, and ensures consistent product quality, making these systems indispensable.

Furthermore, the continuous rise in consumer awareness regarding product safety and quality, particularly in sensitive sectors such as food, pharmaceuticals, and medical devices, compels manufacturers to invest in state-of-the-art inspection technologies. Regulatory bodies worldwide are also implementing stricter guidelines and standards for product manufacturing and packaging, mandating the use of precise weighing and inspection equipment to ensure compliance and prevent product recalls. The expansion of global trade and e-commerce also contributes significantly, requiring efficient and accurate weighing and dimensioning solutions for logistics and packaging operations.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Industrial Automation and Industry 4.0 Adoption | +2.5% | Global, particularly North America, Europe, Asia Pacific | Long-term (2025-2033) |

| Stringent Regulatory Compliance and Quality Standards | +1.8% | Global, especially highly regulated markets like EU, US, Japan | Ongoing (2025-2033) |

| Growing Demand for Food & Pharmaceutical Safety | +1.5% | Global | Ongoing (2025-2033) |

| Expansion of E-commerce and Logistics Sector | +1.0% | Global, with strong growth in Asia Pacific | Mid-term (2025-2030) |

Weighing and Inspection Equipment Market Restraints Analysis

Despite robust growth drivers, the Weighing and Inspection Equipment market faces several restraints that could temper its expansion. One significant challenge is the substantial initial capital investment required for acquiring advanced weighing and inspection systems. High-precision equipment, especially those integrated with AI and sophisticated imaging technologies, can be prohibitively expensive for small and medium-sized enterprises (SMEs), potentially limiting broader market penetration and adoption rates across all business scales.

Another key restraint involves the complexities associated with integrating new, high-tech weighing and inspection systems into existing legacy manufacturing infrastructures. Many older production lines may not be readily compatible with modern, networked equipment, requiring significant modifications, software upgrades, and potential downtime, which can deter adoption. Furthermore, a shortage of skilled labor capable of operating, maintaining, and troubleshooting these advanced systems poses an ongoing challenge, particularly in regions where industrial automation expertise is less developed. Data security and privacy concerns, especially with the rise of connected IoT devices transmitting sensitive operational data, also present a hurdle for wider acceptance and deployment of smart inspection solutions.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Capital Investment and Total Cost of Ownership | -1.2% | Developing Economies, SMEs globally | Ongoing (2025-2033) |

| Integration Complexities with Legacy Systems | -0.8% | Established Industrial Regions (North America, Europe) | Mid-term (2025-2030) |

| Shortage of Skilled Labor for Advanced Systems | -0.5% | Global | Long-term (2025-2033) |

| Data Security and Privacy Concerns | -0.3% | Global | Ongoing (2025-2033) |

Weighing and Inspection Equipment Market Opportunities Analysis

The Weighing and Inspection Equipment market is ripe with opportunities, particularly stemming from the accelerating digital transformation across industries and the increasing demand for data-driven manufacturing. The growing trend towards smart factories and the adoption of Industrial Internet of Things (IIoT) technologies create significant avenues for integrating advanced weighing and inspection systems that offer real-time monitoring, predictive analytics, and remote diagnostic capabilities. This connectivity allows for greater efficiency, reduced downtime, and enhanced decision-making, providing a competitive edge for manufacturers.

Moreover, emerging economies, especially in Asia Pacific and Latin America, present substantial untapped market potential. Rapid industrialization, increasing foreign direct investment in manufacturing, and a rising focus on quality assurance in these regions are driving the demand for modern inspection solutions. The ongoing research and development in areas such as artificial intelligence, machine learning, and advanced sensor technologies also create opportunities for developing innovative and highly specialized equipment tailored to niche applications. Furthermore, the global shift towards sustainable manufacturing practices and waste reduction offers opportunities for solutions that minimize material loss through precise weighing and efficient rejection of non-conforming products.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Smart, Connected Devices (IoT & IIoT Integration) | +1.5% | Global | Long-term (2025-2033) |

| Expansion into Emerging Economies (e.g., APAC, LATAM, MEA) | +1.3% | Asia Pacific, Latin America, Middle East & Africa | Long-term (2025-2033) |

| Increased R&D in AI, ML, and Advanced Sensing Technologies | +1.0% | Global | Long-term (2025-2033) |

| Demand for Customized Solutions for Niche Applications | +0.7% | Global, particularly specialized industries | Ongoing (2025-2033) |

Weighing and Inspection Equipment Market Challenges Impact Analysis

The Weighing and Inspection Equipment market faces several formidable challenges that require strategic navigation from market participants. Rapid technological evolution is a double-edged sword; while it creates opportunities, it also poses the challenge of keeping pace with advancements. Manufacturers must continually invest in research and development to avoid technological obsolescence, which can be resource-intensive and lead to shorter product life cycles. The complexity of integrating new, advanced systems with existing, often disparate, manufacturing execution systems (MES) or enterprise resource planning (ERP) platforms also presents significant technical and operational hurdles for end-users.

Supply chain disruptions, as experienced recently with global events, represent another critical challenge. The reliance on specialized electronic components and sensors, often sourced globally, makes the production of weighing and inspection equipment vulnerable to material shortages, logistical bottlenecks, and price volatility, impacting manufacturing timelines and costs. Furthermore, intense market competition, characterized by a mix of established global players and agile niche providers, pushes companies to innovate constantly while maintaining competitive pricing. Ensuring data security and protecting intellectual property in an increasingly connected environment also remain persistent concerns for both equipment manufacturers and end-users, requiring robust cybersecurity measures and compliance frameworks.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Technological Obsolescence and Need for Continuous R&D | -0.9% | Global | Ongoing (2025-2033) |

| Supply Chain Volatility and Component Shortages | -0.7% | Global | Short-to-Mid Term (2025-2028) |

| High Competition and Price Sensitivity | -0.5% | Global | Ongoing (2025-2033) |

| Data Security and Interoperability Concerns | -0.4% | Global | Ongoing (2025-2033) |

Weighing and Inspection Equipment Market - Updated Report Scope

This comprehensive report offers an in-depth analysis of the global Weighing and Inspection Equipment Market, providing a detailed understanding of its current landscape, historical performance, and future growth projections. It encapsulates critical market dynamics, including key trends, drivers, restraints, opportunities, and challenges, providing a holistic view for stakeholders. The report segments the market extensively by product type, application, end-use industry, technology, and component, offering granular insights into specific market niches and growth segments. Furthermore, it includes a robust regional analysis, highlighting growth patterns and market characteristics across major geographical areas. The inclusion of a competitive landscape section profiles leading market players, offering insights into their strategies, product portfolios, and market positioning, enabling a comprehensive assessment of the market's competitive intensity.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | $4.5 Billion |

| Market Forecast in 2033 | $7.7 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Mettler Toledo, Minebea Intec, Ishida Co. Ltd., Loma Systems, Anritsu Corporation, Sartorius AG, Ametek Inc., Yamato Scale Co., Ltd., OMRON Corporation, Rockwell Automation, Inc., Bizerba SE & Co. KG, WIPOTEC-OCS GmbH, Thermo Fisher Scientific Inc., Eagle PI, Fortress Technology Inc., Peco-InspX, Sesotec GmbH, Ricoh Industrial Solutions Inc., KEYENCE CORPORATION, Cognex Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Weighing and Inspection Equipment market is comprehensively segmented to provide granular insights into its diverse components and applications. This segmentation allows for a detailed understanding of specific growth drivers, market sizes, and competitive landscapes within each category, enabling stakeholders to identify precise opportunities. The market is broadly divided by product type, reflecting the different types of equipment available, ranging from highly specialized inspection systems to general-purpose weighing scales. Further segmentation by application highlights the specific tasks or functions these machines perform, such as foreign object detection or precise dosing.

Moreover, the market is analyzed based on end-use industry, providing a clear picture of demand from sectors like food & beverages, pharmaceuticals, and logistics, each with unique regulatory and operational requirements. Technology-based segmentation differentiates between manual, semi-automatic, and fully automatic systems, showcasing the trend towards automation. Finally, the component-based segmentation breaks down the market into hardware, software, and services, offering insights into the value chain and technological advancements that drive the market. This multi-faceted segmentation ensures a thorough and actionable market analysis.

- By Product Type:

- Checkweighers

- Metal Detectors

- X-ray Inspection Systems

- Vision Inspection Systems

- Weighing Scales (Industrial Scales, Retail Scales, Laboratory Scales, Bench Scales, Floor Scales, Pallet Scales, Crane Scales)

- Dosing & Filling Systems

- Combination Systems

- Others (e.g., Load Cells, Controllers)

- By Application:

- Weight Control

- Foreign Object Detection

- Quality Control

- Product Integrity

- Dosing & Batching

- Counting

- Dimensioning

- Over/Under Fill Detection

- By End-Use Industry:

- Food & Beverages (Meat, Poultry & Seafood, Dairy Products, Bakery & Confectionery, Fruits & Vegetables, Beverages, Prepared Foods)

- Pharmaceuticals & Healthcare (Tablets, Capsules, Powders, Liquids, Medical Devices)

- Chemicals

- Packaging

- Logistics & Transportation

- Automotive

- Manufacturing & Industrial (General Manufacturing, Electronics, Textiles)

- Cosmetics & Personal Care

- Mining & Construction

- Retail

- By Technology:

- Manual

- Semi-Automatic

- Automatic

- By Component:

- Hardware (Sensors, Cameras, Load Cells, Conveyors, Processors)

- Software (Control Software, Data Analytics Software, HMI Software)

- Services (Installation, Maintenance, Calibration, Training, Consulting)

Regional Highlights

- North America: Characterized by a high adoption rate of advanced automation technologies and stringent regulatory frameworks, particularly in the food and pharmaceutical sectors. The region's mature industrial base and significant investments in smart manufacturing drive consistent demand for sophisticated weighing and inspection solutions.

- Europe: Driven by strong emphasis on product quality, consumer safety, and adherence to rigorous EU directives. European countries are pioneers in sustainable manufacturing, fostering demand for energy-efficient and highly accurate inspection equipment. Innovation in R&D and a focus on integrating AI and IoT are also key regional trends.

- Asia Pacific (APAC): Projected to be the fastest-growing market due to rapid industrialization, expanding manufacturing sectors (especially in China, India, and Southeast Asia), and increasing awareness regarding product quality and safety standards. Rising disposable incomes and the growth of e-commerce further fuel the demand for efficient weighing and inspection equipment in this region.

- Latin America: An emerging market experiencing growth due to increasing foreign investments in manufacturing, improving economic conditions, and a growing focus on food processing and packaging industries. Infrastructure development and a gradual shift towards automation contribute to market expansion, albeit at a slower pace compared to APAC.

- Middle East & Africa (MEA): Growth in this region is primarily driven by diversification efforts away from oil-dependent economies, leading to investments in manufacturing, food processing, and logistics. Increasing consumer awareness and developing regulatory environments are gradually creating demand for modern weighing and inspection solutions.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Weighing and Inspection Equipment Market.- Mettler Toledo

- Minebea Intec

- Ishida Co. Ltd.

- Loma Systems

- Anritsu Corporation

- Sartorius AG

- Ametek Inc.

- Yamato Scale Co., Ltd.

- OMRON Corporation

- Rockwell Automation, Inc.

- Bizerba SE & Co. KG

- WIPOTEC-OCS GmbH

- Thermo Fisher Scientific Inc.

- Eagle PI

- Fortress Technology Inc.

- Peco-InspX

- Sesotec GmbH

- Ricoh Industrial Solutions Inc.

- KEYENCE CORPORATION

- Cognex Corporation

Frequently Asked Questions

What is the primary driver of the Weighing and Inspection Equipment market growth?

The primary driver is the increasing adoption of industrial automation and Industry 4.0 initiatives globally, coupled with stringent regulatory requirements for quality control and product safety across various manufacturing sectors.

How is AI transforming weighing and inspection processes?

AI is transforming processes by enabling enhanced anomaly detection, predictive maintenance, automated calibration, and real-time data analysis, leading to improved accuracy, efficiency, and reduced operational costs.

Which industries are the largest consumers of weighing and inspection equipment?

The largest consumers are the Food & Beverages, Pharmaceuticals & Healthcare, and Packaging industries, driven by high production volumes, critical safety standards, and strict regulatory compliance needs.

What are the main challenges facing the Weighing and Inspection Equipment market?

Key challenges include high initial capital investment costs, complexities in integrating new systems with existing infrastructure, a shortage of skilled personnel, and potential vulnerabilities related to data security in connected systems.

Which region offers the most significant growth opportunities in this market?

The Asia Pacific region offers the most significant growth opportunities, propelled by rapid industrialization, expanding manufacturing bases, increasing consumer awareness of product quality, and rising investments in automation across countries like China and India.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted