Waveguide Filter Market

Waveguide Filter Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709788 | Last Updated : December 17, 2025 |

Format : ![]()

![]()

![]()

![]()

Waveguide Filter Market Size

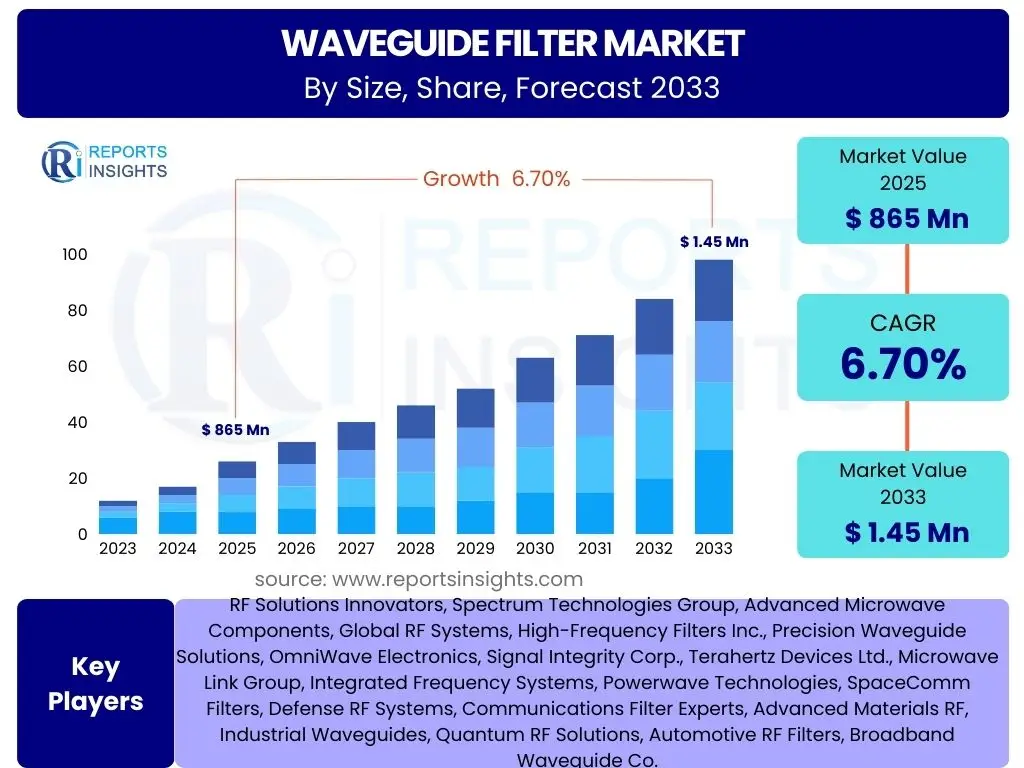

According to Reports Insights Consulting Pvt Ltd, The Waveguide Filter Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.7% between 2025 and 2033. The market is estimated at USD 865 Million in 2025 and is projected to reach USD 1.45 Billion by the end of the forecast period in 2033. This growth is primarily fueled by the accelerating global deployment of advanced communication technologies, including 5G and nascent 6G networks, alongside significant investments in aerospace, defense, and satellite communication systems. The demand for highly precise and reliable filtering solutions in these high-frequency applications is a core driver for market expansion.

The consistent expansion reflects the critical role waveguide filters play in ensuring signal integrity and managing electromagnetic interference across a multitude of high-frequency applications. As digital transformation accelerates and new communication standards emerge, the inherent advantages of waveguide filters, such as low insertion loss and high power handling capabilities, become increasingly indispensable. Emerging applications in autonomous vehicles, quantum computing, and advanced radar systems are also contributing to the market's robust trajectory.

Key Waveguide Filter Market Trends & Insights

The waveguide filter market is experiencing dynamic shifts driven by technological advancements and evolving application requirements. A primary trend involves the relentless pursuit of miniaturization and weight reduction, essential for integration into compact electronic systems in aerospace, satellite, and portable communication devices. This trend is accompanied by an increasing demand for filters capable of operating at higher frequency bands, specifically in the millimeter-wave (mmWave) and sub-terahertz (sub-THz) spectrum, to support advanced wireless communication and radar systems.

Another significant insight points to the growing adoption of new manufacturing techniques, such as additive manufacturing (3D printing), which enables the creation of complex filter geometries with enhanced performance characteristics and reduced lead times. This innovation facilitates rapid prototyping and customization, addressing specific client needs more efficiently. Furthermore, there is a clear trend towards integrating waveguide filters with other passive and active components to create more compact and functional modules, streamlining system design and improving overall efficiency.

The market also observes a strong emphasis on developing filters with enhanced power handling capabilities and improved thermal stability, crucial for high-power radar and satellite communication systems. The drive towards energy efficiency and spectral purity further underscores the need for high-performance filters that can operate reliably under demanding environmental conditions. This holistic approach to filter design and manufacturing is shaping the competitive landscape and technological roadmap for the industry.

- Miniaturization and weight reduction for compact integration.

- Expansion into higher frequency bands (mmWave, sub-THz).

- Adoption of advanced manufacturing techniques like additive manufacturing.

- Increased demand for filters with enhanced power handling and thermal stability.

- Integration of waveguide filters into multi-component modules.

- Focus on improved spectral purity and energy efficiency.

- Development of tunable and reconfigurable filter solutions.

AI Impact Analysis on Waveguide Filter

Artificial Intelligence (AI) is poised to significantly impact the waveguide filter market by revolutionizing design, optimization, and manufacturing processes. Users frequently inquire about how AI can accelerate the complex design cycles inherent in these highly specialized components. AI-driven simulation and optimization tools can explore a vast design space far more efficiently than traditional methods, allowing engineers to quickly converge on optimal filter configurations that meet stringent performance specifications for insertion loss, return loss, and rejection ratios. This capability reduces both time-to-market and development costs, enhancing innovation speed across the industry.

Beyond initial design, AI is also expected to play a crucial role in predicting the performance of waveguide filters under various operating conditions and identifying potential manufacturing defects through advanced analytics. Machine learning algorithms can analyze vast datasets from simulations and physical tests to predict how material variations or subtle manufacturing imperfections might affect filter performance. This predictive capability enables proactive adjustments in manufacturing processes, improving yield rates and product quality, which are critical for high-reliability applications in aerospace and defense.

Furthermore, AI-powered automation in manufacturing, including robotic assembly and automated quality control, stands to enhance precision and consistency in the production of waveguide filters. By continuously monitoring and adjusting production parameters, AI systems can minimize human error and ensure that each filter meets exact specifications. This integration of AI not only streamlines production but also opens avenues for more complex and intricate filter designs that were previously challenging to manufacture, pushing the boundaries of what is technically feasible in high-frequency signal processing.

- Accelerated design and optimization cycles using AI-driven simulation.

- Predictive performance analysis and defect detection in manufacturing.

- Enhanced automation and quality control in production lines.

- Enabling the realization of more complex and intricate filter geometries.

- Reduction in development costs and time-to-market.

- Improved yield rates and consistent product quality through intelligent process control.

- Facilitation of rapid prototyping and customization.

Key Takeaways Waveguide Filter Market Size & Forecast

A central insight from the waveguide filter market analysis is its robust and sustained growth trajectory, primarily fueled by the insatiable demand for high-speed data transmission and secure communication across global infrastructures. The market's expansion is not merely incremental but represents a foundational shift towards more sophisticated, higher-frequency filtering solutions necessitated by the advent of 5G, upcoming 6G, and burgeoning satellite communication networks. This indicates that waveguide filters are not just niche components but critical enablers of the next generation of digital connectivity.

Another key takeaway underscores the dual importance of technological innovation and strategic market positioning. While traditional applications in defense and aerospace remain vital, significant growth opportunities are emerging in new sectors such as autonomous vehicles, quantum computing, and advanced industrial IoT, which demand superior signal integrity and resilience in harsh environments. Companies that invest in research and development to produce compact, high-performance, and cost-effective filters will be best positioned to capture these evolving market segments.

Furthermore, regional dynamics play a pivotal role, with strong growth anticipated in Asia Pacific due to rapid telecommunications infrastructure development, while North America and Europe continue to lead in defense and space applications. Understanding these regional nuances and tailoring product offerings to specific market requirements, alongside fostering strong partnerships within the supply chain, will be crucial for navigating the competitive landscape and capitalizing on the projected market expansion through 2033.

- Sustained growth driven by 5G, 6G, and satellite communication deployments.

- Increasing demand for high-frequency, high-performance filtering solutions.

- Emerging applications in autonomous vehicles, quantum computing, and advanced radar.

- Technological innovation in miniaturization and manufacturing processes is critical for market success.

- Asia Pacific leading in telecom infrastructure, while North America and Europe excel in defense and space.

- Strategic partnerships and customized product development are key competitive advantages.

Waveguide Filter Market Drivers Analysis

The waveguide filter market is propelled by several robust drivers, each contributing significantly to its anticipated growth. The global rollout of 5G and future 6G communication networks stands as a primary catalyst, demanding high-performance, low-loss filters for enhanced data rates and spectral efficiency in millimeter-wave bands. Concurrently, the burgeoning satellite communication sector, including Low Earth Orbit (LEO) constellations, requires highly reliable and radiation-hardened filters for earth-to-space and inter-satellite links, expanding the application scope for waveguide technology.

Furthermore, increasing global defense expenditures and modernization initiatives, particularly in radar systems and electronic warfare, drive the demand for sophisticated waveguide filters capable of operating under extreme conditions with high precision. These systems rely on advanced filtering to manage complex electromagnetic environments and ensure secure, interference-free operations. The proliferation of IoT devices and the development of autonomous vehicles, which utilize advanced radar sensors for navigation and safety, also contribute to the growing market, as these applications require robust and reliable signal filtering to prevent interference and maintain system integrity.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global 5G and 6G Network Deployments | +2.1% | Global, particularly Asia Pacific, North America, Europe | Short to Mid-term (2025-2030) |

| Expansion of Satellite Communication (LEO/MEO) | +1.8% | Global, major spacefaring nations (USA, China, Europe) | Mid to Long-term (2027-2033) |

| Increasing Defense Spending & Modernization | +1.5% | North America, Europe, Middle East, specific APAC countries | Consistent (2025-2033) |

| Growth in Automotive Radar Systems | +0.9% | Europe, North America, Japan, China | Mid-term (2026-2032) |

Waveguide Filter Market Restraints Analysis

Despite its robust growth, the waveguide filter market faces several significant restraints that could temper its expansion. One primary challenge is the relatively high manufacturing cost associated with these components, particularly for custom-designed filters and those requiring extreme precision or exotic materials. The intricate fabrication processes and the need for specialized equipment often result in higher unit costs compared to other filter technologies, which can limit adoption in price-sensitive applications or smaller-scale deployments.

Furthermore, the physical bulk and weight of traditional waveguide filters can be a considerable restraint, especially in applications where space and mass are critical, such as small satellites, drones, and portable communication devices. While miniaturization efforts are ongoing, achieving significant size and weight reductions without compromising performance remains a complex engineering challenge. This inherent physical characteristic can sometimes make alternative, more compact filtering solutions (e.g., planar filters) more attractive for certain system designs, even if they offer slightly lower performance.

Another factor limiting market growth is the design complexity and the specialized expertise required for both the design and implementation of waveguide filters. The need for highly skilled engineers proficient in electromagnetic theory and high-frequency design tools can create bottlenecks in development cycles and increase lead times. This specialized knowledge requirement, coupled with the capital investment needed for advanced manufacturing, acts as a barrier to entry for new players and can slow down innovation in the broader market.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Manufacturing Costs & Complexity | -1.2% | Global, impacts emerging markets more significantly | Consistent (2025-2033) |

| Physical Size and Weight Limitations | -0.8% | Aerospace, Portable Communications, UAVs | Consistent (2025-2033) |

| Availability of Alternative Filter Technologies | -0.7% | Consumer Electronics, High-Volume Commercial | Mid to Long-term (2027-2033) |

Waveguide Filter Market Opportunities Analysis

Significant opportunities abound within the waveguide filter market, particularly driven by emerging technological frontiers. The accelerating pace of space exploration and commercialization, including ambitious projects for lunar and Martian missions, presents a robust demand for highly reliable, radiation-hardened waveguide filters for spacecraft communication and scientific instrumentation. These applications require components capable of withstanding extreme environmental conditions while delivering uncompromising performance, areas where waveguide filters inherently excel.

Furthermore, the advent of quantum computing and advanced research in terahertz (THz) frequency applications is opening new avenues for specialized waveguide filters. These cutting-edge fields necessitate filters with unprecedented precision and minimal signal loss at extremely high frequencies, pushing the boundaries of current technology. As quantum technologies mature and THz communication or imaging systems become more prevalent, the demand for highly customized and innovative waveguide filter solutions will surge, creating a niche market for advanced manufacturers.

The continuous development of autonomous driving technologies and advanced driver-assistance systems (ADAS) also offers a burgeoning opportunity. High-resolution automotive radar systems, which operate in millimeter-wave bands, increasingly rely on sophisticated waveguide filters to ensure clear signal reception and rejection of interference, critical for safety and reliability. As autonomous vehicle penetration increases globally, the need for robust and dependable radar components, including waveguide filters, will escalate, representing a substantial volume opportunity for manufacturers.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Space Exploration & Commercialization | +1.5% | USA, Europe, China, India, Japan | Mid to Long-term (2027-2033) |

| Advancements in Quantum Computing & THz Tech | +1.2% | Global, major research hubs | Long-term (2030-2033) |

| Expansion of Autonomous Driving & ADAS Radar | +1.0% | Europe, North America, Asia Pacific | Mid-term (2026-2032) |

| Non-telecom mmWave Applications (e.g., Industrial, Medical) | +0.8% | Global | Mid to Long-term (2027-2033) |

Waveguide Filter Market Challenges Impact Analysis

The waveguide filter market, despite its strong growth prospects, faces several critical challenges that require concerted efforts from manufacturers and innovators. A significant hurdle is the escalating demand for extreme miniaturization without compromising performance. As electronic systems become smaller and more integrated, there is persistent pressure to reduce the physical size and weight of waveguide filters, which can be inherently bulky. Achieving this while maintaining low insertion loss, high selectivity, and power handling capabilities presents complex engineering and manufacturing challenges, often requiring novel materials and advanced fabrication techniques.

Another substantial challenge revolves around thermal management, particularly for high-power applications. Waveguide filters used in radar, satellite uplinks, and high-power communication systems generate heat, which can degrade performance, alter frequency response, and even lead to component failure if not effectively dissipated. Designing filters that efficiently manage thermal loads while maintaining their electrical characteristics across a wide temperature range is a critical design and material science problem that demands innovative solutions, often adding to manufacturing complexity and cost.

Furthermore, the global supply chain for specialized materials and components required for waveguide filter manufacturing remains vulnerable to disruptions. Geopolitical tensions, trade restrictions, and unforeseen global events can impact the availability and cost of critical raw materials, such as specific metals, ceramics, and high-frequency substrates. This volatility can lead to increased production costs, extended lead times, and potential delays in product delivery, posing a significant operational challenge for market players reliant on a stable and efficient supply chain.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Extreme Miniaturization & Integration Demands | -1.0% | Global, affects all high-tech applications | Consistent (2025-2033) |

| Thermal Management in High-Power Applications | -0.9% | Defense, Satellite, High-Power Telecom | Consistent (2025-2033) |

| Volatile Supply Chain for Specialized Materials | -0.6% | Global, impacts all manufacturers | Short to Mid-term (2025-2030) |

| Skilled Workforce Shortage in RF Engineering | -0.5% | North America, Europe | Long-term (2028-2033) |

Waveguide Filter Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global waveguide filter market, offering detailed insights into its current landscape, key trends, drivers, restraints, opportunities, and challenges. It covers market sizing and forecasting, segmented analysis by type, application, and frequency band, along with a thorough regional breakdown. The report aims to equip stakeholders with critical information to make informed strategic decisions, identify growth avenues, and understand the competitive dynamics shaping the industry over the forecast period.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 865 Million |

| Market Forecast in 2033 | USD 1.45 Billion |

| Growth Rate | 6.7% CAGR |

| Number of Pages | 265 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | RF Solutions Innovators, Spectrum Technologies Group, Advanced Microwave Components, Global RF Systems, High-Frequency Filters Inc., Precision Waveguide Solutions, OmniWave Electronics, Signal Integrity Corp., Terahertz Devices Ltd., Microwave Link Group, Integrated Frequency Systems, Powerwave Technologies, SpaceComm Filters, Defense RF Systems, Communications Filter Experts, Advanced Materials RF, Industrial Waveguides, Quantum RF Solutions, Automotive RF Filters, Broadband Waveguide Co. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The waveguide filter market is extensively segmented to provide a granular understanding of its diverse components and application areas. These segmentations are crucial for identifying specific market niches, understanding competitive dynamics, and tailoring product development strategies. The market is primarily categorized by type, which includes various configurations such as rectangular, circular, ridged, planar, coaxial, and dielectric resonator filters, each suited for different performance requirements and integration challenges.

Further segmentation by application highlights the broad utility of waveguide filters across key industries. Telecommunications, encompassing the rapidly evolving 5G/6G networks and satellite communication, represents a dominant segment. Aerospace and defense, driven by sophisticated radar and electronic warfare systems, also form a critical application area. Emerging applications in automotive (ADAS), medical, industrial, and scientific research are progressively contributing to market growth, demonstrating the versatility and indispensability of these specialized components in high-frequency domains.

Additionally, the market is segmented by the frequency band of operation, ranging from C-band to millimeter-wave and sub-terahertz frequencies, reflecting the increasing shift towards higher frequency spectrums for advanced communication and sensing. Material type also constitutes a significant segmentation, distinguishing between metallic, dielectric, ceramic, and composite filters, each offering distinct advantages in terms of performance, weight, and environmental resilience, catering to specific demands of diverse end-use sectors.

- By Type: Rectangular Waveguide Filters, Circular Waveguide Filters, Ridged Waveguide Filters, Planar Waveguide Filters, Coaxial Waveguide Filters, Dielectric Resonator Filters, Others.

- By Application: Telecommunications (5G/6G, Satellite), Aerospace & Defense (Radar, Electronic Warfare), Medical, Industrial, Automotive (ADAS, Autonomous Driving), Scientific Research, Broadcasting, Others.

- By Frequency Band: C-Band, X-Band, Ku-Band, Ka-Band, V-Band, W-Band, MmWave and Sub-THz.

- By Material: Metallic (Aluminum, Copper, Brass), Dielectric, Ceramic, Composite.

Regional Highlights

- North America: Expected to hold a significant market share due to substantial investments in defense and aerospace sectors, coupled with early adoption of advanced 5G technologies. The presence of key market players and a robust research and development ecosystem further bolsters regional growth.

- Europe: A key region driven by stringent regulatory standards for telecommunications, strong presence of automotive industry for ADAS radar, and ongoing modernization of defense capabilities. Significant R&D initiatives in advanced materials and manufacturing also contribute to market expansion.

- Asia Pacific (APAC): Projected to witness the highest growth rate, primarily attributed to aggressive 5G infrastructure deployment, increasing government spending on space programs, and a booming electronics manufacturing base in countries like China, Japan, South Korea, and India.

- Latin America: An emerging market with growing investments in telecommunications infrastructure and increasing adoption of satellite communication services. Economic development and urbanization are driving demand for advanced connectivity solutions.

- Middle East and Africa (MEA): Characterized by significant defense spending, particularly in the Middle East, and increasing investments in telecommunication infrastructure. The expansion of satellite services and efforts to diversify economies are key growth drivers in this region.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Waveguide Filter Market.- RF Solutions Innovators

- Spectrum Technologies Group

- Advanced Microwave Components

- Global RF Systems

- High-Frequency Filters Inc.

- Precision Waveguide Solutions

- OmniWave Electronics

- Signal Integrity Corp.

- Terahertz Devices Ltd.

- Microwave Link Group

- Integrated Frequency Systems

- Powerwave Technologies

- SpaceComm Filters

- Defense RF Systems

- Communications Filter Experts

- Advanced Materials RF

- Industrial Waveguides

- Quantum RF Solutions

- Automotive RF Filters

- Broadband Waveguide Co.

Frequently Asked Questions

What is a waveguide filter and how does it function?

A waveguide filter is an electrical filter that uses waveguide structures to pass specific frequencies of electromagnetic waves while attenuating others. It functions by creating resonant cavities within the waveguide, which selectively allow or block signals based on their wavelength, ensuring signal integrity in high-frequency systems.

What are the primary applications of waveguide filters?

Waveguide filters are predominantly used in high-frequency applications such as telecommunications (5G/6G, satellite communication), aerospace and defense (radar, electronic warfare), broadcasting, and increasingly in emerging fields like automotive radar and scientific research requiring precise signal management.

How does 5G technology impact the demand for waveguide filters?

5G technology significantly boosts demand for waveguide filters by requiring operation at higher frequency bands (millimeter-wave), where their low insertion loss, high power handling, and excellent selectivity are crucial for ensuring reliable and efficient high-speed data transmission and managing spectral congestion.

What are the key advantages of waveguide filters over other filter technologies?

Waveguide filters offer several advantages, including very low insertion loss, high power handling capability, superior out-of-band rejection, and excellent thermal stability. These characteristics make them ideal for demanding high-frequency, high-power, and harsh environment applications where signal purity is paramount.

What trends are shaping the future of the waveguide filter market?

Future trends include continued miniaturization for integration into compact systems, expansion into sub-terahertz frequencies, adoption of additive manufacturing for complex geometries, enhanced thermal management solutions for high-power applications, and the development of tunable and reconfigurable filters to meet evolving system demands.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted