Automatic Test Equipment Market

Automatic Test Equipment Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708703 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

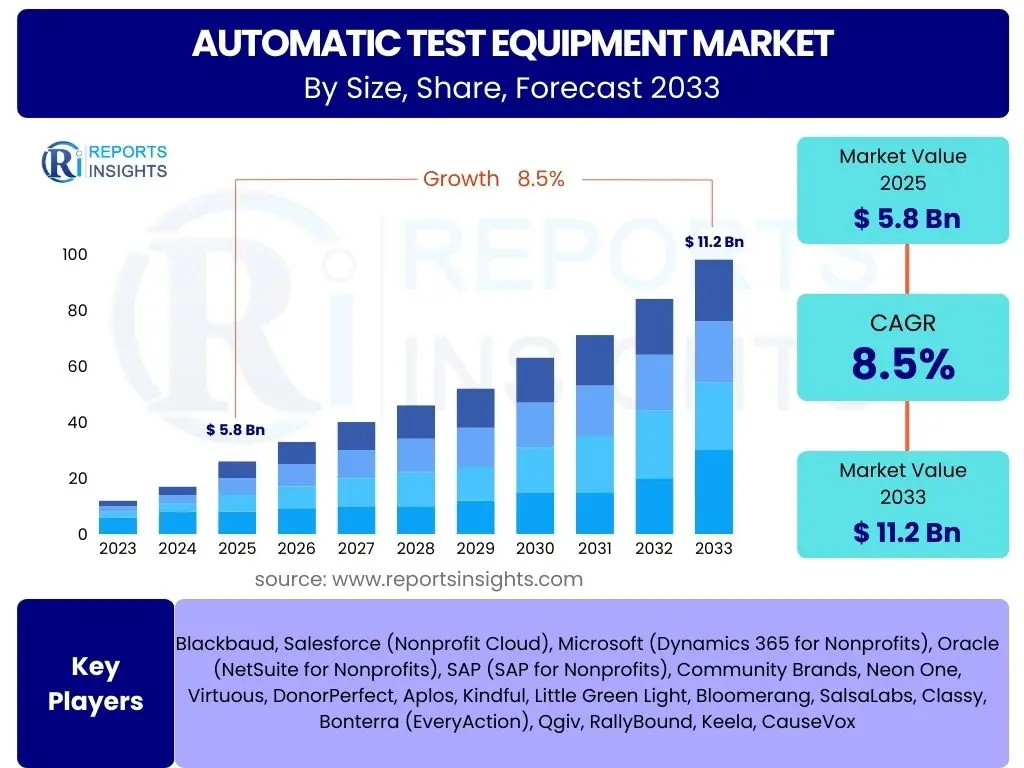

Automatic Test Equipment Market Size

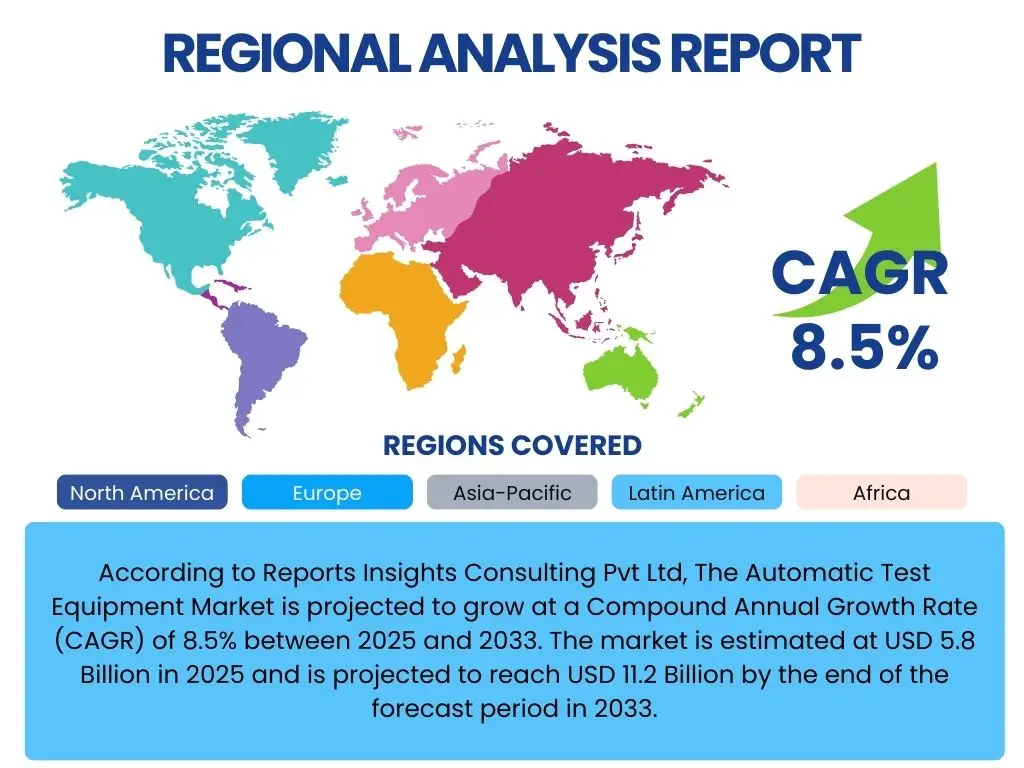

According to Reports Insights Consulting Pvt Ltd, The Automatic Test Equipment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2025 and 2033. The market is estimated at USD 5.8 Billion in 2025 and is projected to reach USD 11.2 Billion by the end of the forecast period in 2033.

Key Automatic Test Equipment Market Trends & Insights

User queries regarding Automatic Test Equipment (ATE) market trends frequently highlight the increasing complexity of electronic components and the accelerating pace of technological innovation. There is significant interest in how ATE solutions are evolving to address the demands of advanced semiconductor manufacturing, particularly in areas like heterogeneous integration, System-on-Chip (SoC) designs, and the testing of specialized components for emerging applications. Furthermore, users are keen to understand the shift towards more flexible, scalable, and software-defined testing platforms that can adapt to rapid product cycles and diverse testing requirements.

Another prominent theme in user questions revolves around the integration of advanced connectivity standards and the proliferation of smart devices. Inquiries often focus on how ATE is adapting to test 5G-enabled devices, Internet of Things (IoT) modules, and high-speed data communication interfaces. The automotive sector, with its rapid adoption of advanced driver-assistance systems (ADAS) and electric vehicles (EVs), also generates substantial interest in specialized ATE solutions designed for robust and safety-critical component testing. These trends collectively underscore a market moving towards higher precision, greater adaptability, and more comprehensive testing capabilities to support the next generation of electronic innovation.

- Miniaturization and increasing complexity of electronic devices drive demand for advanced ATE.

- Proliferation of 5G technology and high-speed communication standards necessitates specialized testing.

- Rapid growth in IoT and connected devices expands the application scope for ATE.

- Surge in automotive electronics, including ADAS and EVs, fuels demand for robust ATE solutions.

- Shift towards modular, scalable, and software-defined ATE architectures for enhanced flexibility.

- Emphasis on parallel testing and higher test coverage to improve efficiency and reduce time-to-market.

AI Impact Analysis on Automatic Test Equipment

Common user questions regarding AI's impact on Automatic Test Equipment (ATE) center on its potential to revolutionize test processes, enhance efficiency, and reduce costs. Users are particularly interested in how AI can facilitate more intelligent test pattern generation, optimize test sequences, and improve fault detection capabilities, especially for highly complex devices. The ability of AI to learn from vast datasets of test results and identify subtle anomalies or patterns that might be missed by traditional methods is a key area of inquiry, suggesting an expectation for more proactive and predictive testing methodologies.

Furthermore, there is significant interest in AI's role in predictive maintenance for ATE systems themselves, reducing downtime and optimizing equipment utilization. Users also explore how AI can contribute to data analytics, transforming raw test data into actionable insights for manufacturing process improvement and product design optimization. While excitement about AI's potential is high, questions also arise about the practical implementation challenges, data privacy concerns, and the need for specialized skills to effectively integrate and leverage AI within existing ATE infrastructures, highlighting both the promise and the complexities of this technological convergence.

- AI-driven optimization of test plan generation and sequencing for improved efficiency.

- Enhanced fault detection and diagnosis through machine learning algorithms, identifying subtle anomalies.

- Predictive maintenance for ATE systems, reducing downtime and extending equipment lifespan.

- Advanced data analytics using AI to transform test data into actionable manufacturing and design insights.

- Automation of complex decision-making processes in test flows, reducing human intervention.

- Potential for self-learning test systems that adapt to new device complexities and failure modes.

Key Takeaways Automatic Test Equipment Market Size & Forecast

User inquiries about key takeaways from the Automatic Test Equipment (ATE) market size and forecast consistently highlight the robust growth trajectory driven by the relentless advancement of electronics across various sectors. There is a strong emphasis on understanding the primary factors contributing to this growth, such as the increasing demand for high-performance computing, the proliferation of connected devices, and the automotive industry's digital transformation. Users are keenly interested in identifying the segments and regions poised for the most significant expansion, seeking to pinpoint lucrative investment opportunities and strategic focus areas.

Another crucial aspect frequently explored in user questions pertains to the long-term sustainability of ATE market growth, considering technological shifts and potential market saturation points. Queries often touch upon the impact of emerging technologies like AI and advanced packaging on the forecast, and how these innovations might reshape the competitive landscape. Overall, the key takeaways sought by users revolve around understanding the core drivers, significant market opportunities, and the strategic implications of the forecasted growth for stakeholders across the entire electronics value chain, underscoring the dynamic nature of this critical industry segment.

- The ATE market is experiencing substantial growth, primarily fueled by innovations in semiconductors and consumer electronics.

- Digital transformation across industries like automotive, telecom, and healthcare is a significant growth catalyst.

- Asia Pacific is expected to remain the dominant region due to robust manufacturing and R&D activities.

- Investment in advanced testing methodologies, including AI integration, is crucial for competitive advantage.

- The market presents significant opportunities for companies offering flexible, high-speed, and cost-effective testing solutions.

Automatic Test Equipment Market Drivers Analysis

The Automatic Test Equipment (ATE) market is fundamentally propelled by the relentless innovation and expansion within the global electronics industry. As electronic devices become more sophisticated, complex, and miniaturized, the need for precise, efficient, and comprehensive testing solutions intensifies. This complexity is evident in advanced semiconductor designs, System-on-Chip (SoC) integration, and heterogeneous packaging, all of which require state-of-the-art ATE to ensure reliability and performance. The proliferation of these advanced components across a diverse range of end-user applications directly translates into heightened demand for sophisticated testing capabilities.

Key drivers also include the widespread adoption of next-generation communication technologies, such as 5G, and the exponential growth of the Internet of Things (IoT). These technologies demand rigorous testing for high-frequency signals, low power consumption, and robust connectivity, creating significant impetus for ATE market expansion. Furthermore, the automotive industry's rapid shift towards electric vehicles (EVs) and advanced driver-assistance systems (ADAS) mandates incredibly stringent testing for safety-critical components, thereby serving as a major growth engine. The convergence of these factors creates a dynamic environment where ATE is indispensable for maintaining product quality, accelerating time-to-market, and driving technological progress.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Complexity of Electronic Devices and SoCs | +2.1% | Global (Strongest in APAC, North America) | Long-term |

| Proliferation of 5G Technology and Advanced Connectivity | +1.8% | APAC, North America, Europe | Medium-term |

| Growth of IoT and Connected Devices Ecosystem | +1.5% | Global | Medium-term |

| Expansion of Automotive Electronics (ADAS, EVs, Infotainment) | +1.9% | Europe, North America, APAC | Long-term |

| Rising Demand for High-Performance Computing (HPC) and Data Centers | +1.2% | North America, Europe, APAC | Medium-to-Long term |

Automatic Test Equipment Market Restraints Analysis

Despite the robust growth prospects, the Automatic Test Equipment (ATE) market faces several significant restraints that could temper its expansion. One primary challenge is the substantial upfront capital investment required for acquiring and deploying advanced ATE systems. These systems are highly specialized and incorporate cutting-edge technology, making them expensive to purchase, install, and maintain. This high cost can be a barrier for smaller manufacturers or those operating in emerging markets with limited capital, potentially slowing the adoption of the latest testing methodologies.

Another critical restraint is the rapid pace of technological obsolescence inherent in the electronics industry. As new semiconductor architectures, communication standards, and device functionalities emerge quickly, ATE systems can become outdated within relatively short periods. This necessitates frequent upgrades or complete replacements, incurring additional costs and R&D expenditures for ATE manufacturers, which can then be passed on to end-users. Furthermore, the increasing complexity of devices and test requirements demands a highly skilled workforce for operating, programming, and maintaining ATE, and a shortage of such expertise can limit efficient deployment and utilization of these advanced systems globally.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Capital Investment and Ownership Cost | -1.2% | Emerging Markets, SMEs Globally | Medium-term |

| Rapid Technological Obsolescence of Test Equipment | -1.0% | Global | Short-to-Medium term |

| Shortage of Skilled Workforce for ATE Operation and Maintenance | -0.8% | Global (Varies by Region) | Long-term |

| Complexity of Integrating Diverse Test Environments and Standards | -0.7% | Global | Short-to-Medium term |

Automatic Test Equipment Market Opportunities Analysis

The Automatic Test Equipment (ATE) market is ripe with opportunities driven by several transformative shifts in technology and industry. The burgeoning demand for electric vehicles (EVs) and autonomous driving systems presents a significant avenue for growth, as these vehicles rely on a vast array of sophisticated electronic components that require rigorous and specialized testing for safety and performance. This includes power electronics, battery management systems, and advanced sensor arrays, all of which necessitate tailored ATE solutions. The expansion of smart cities infrastructure, coupled with the ongoing deployment of 5G networks, further creates demand for robust testing of communication modules, IoT devices, and complex network hardware.

Another major opportunity lies in the development and adoption of advanced semiconductor packaging technologies, such as 2.5D/3D integration and chiplets. These innovations introduce new testing challenges that traditional ATE solutions may not fully address, creating a market for highly advanced, high-density, and versatile test platforms. Furthermore, the trend towards modular and software-defined ATE systems offers flexibility and scalability, enabling manufacturers to adapt more quickly to evolving test requirements and reducing the total cost of ownership over time. Expanding into niche markets like medical devices, industrial automation, and aerospace and defense, where precision and reliability are paramount, also provides substantial growth prospects for specialized ATE providers.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand for Electric Vehicles (EVs) and Autonomous Driving Systems | +1.7% | Global (Europe, APAC, North America) | Long-term |

| Development of Advanced Semiconductor Packaging (2.5D/3D, Chiplets) | +1.5% | APAC, North America | Medium-to-Long term |

| Expansion into Niche Markets (Medical Devices, Aerospace & Defense) | +1.0% | North America, Europe | Long-term |

| Adoption of Modular and Software-Defined ATE Architectures | +1.3% | Global | Medium-term |

| Increasing Investments in Smart Manufacturing and Industry 4.0 | +0.9% | Global | Medium-to-Long term |

Automatic Test Equipment Market Challenges Impact Analysis

The Automatic Test Equipment (ATE) market faces formidable challenges that stem directly from the very innovations it seeks to enable. The increasing complexity and miniaturization of electronic components, particularly in advanced integrated circuits, create significant hurdles for test engineers. Designing ATE capable of accurately testing billions of transistors on a single chip, often with mixed-signal capabilities and high-frequency requirements, demands continuous and costly research and development. This complexity not only drives up R&D expenses for ATE manufacturers but also necessitates highly sophisticated programming and diagnostic tools, increasing the learning curve and operational complexity for end-users.

Furthermore, the sheer volume of data generated during the testing process presents another substantial challenge. As test coverage expands and device complexity grows, the amount of data collected can become overwhelming, requiring advanced analytics and storage solutions. Managing, analyzing, and deriving actionable insights from this big data efficiently is crucial for optimizing manufacturing processes and identifying subtle defects. Cybersecurity concerns also loom large, particularly as ATE systems become more connected and integrated into factory networks. Protecting sensitive intellectual property and ensuring the integrity of test data from cyber threats is a growing challenge that demands robust security measures and continuous vigilance within the ATE ecosystem.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Complexity and Miniaturization of Devices Under Test (DUTs) | -1.3% | Global | Ongoing |

| High Cost of Research and Development for Advanced ATE Systems | -1.1% | Global | Long-term |

| Managing and Analyzing Vast Amounts of Test Data (Big Data) | -0.9% | Global | Medium-term |

| Ensuring Interoperability Across Diverse Test Environments and Standards | -0.8% | Global | Short-to-Medium term |

| Supply Chain Disruptions and Geopolitical Instabilities | -0.7% | Global | Short-to-Medium term |

Automatic Test Equipment Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the Automatic Test Equipment (ATE) market, offering a detailed understanding of its current landscape, future projections, and the underlying factors influencing its trajectory. The scope encompasses a thorough examination of market size and growth forecast, key trends, drivers, restraints, opportunities, and challenges that shape the industry. It further delves into a detailed segmentation analysis by type, application, and component, alongside an extensive regional assessment to highlight variations in market dynamics. The report also profiles leading industry players, offering insights into their strategic initiatives and market positioning, providing stakeholders with critical intelligence for informed decision-making and strategic planning.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 5.8 Billion |

| Market Forecast in 2033 | USD 11.2 Billion |

| Growth Rate | 8.5% |

| Number of Pages | 255 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Advantest Corporation, Teradyne Inc., National Instruments Corporation, Cohu Inc., Chroma ATE Inc., LTX-Credence (Xcerra), Astronics Corporation, Aemulus Holdings Bhd, Acculogic Inc., Marvin Test Solutions Inc., Keysight Technologies Inc., Rohde & Schwarz GmbH & Co. KG, STAr Technologies Inc., SPEA S.p.A., Fuji Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Automatic Test Equipment (ATE) market is meticulously segmented to provide a granular understanding of its diverse components and application areas. This segmentation allows for a detailed analysis of market dynamics, growth drivers, and opportunities within specific niches, enabling stakeholders to identify high-potential areas and tailor their strategies effectively. The primary segmentation categories typically include Type, Application, and Component, each with further sub-segmentations that reflect the intricate nature of the electronics testing landscape. Understanding these segments is crucial for recognizing how different industry sectors and technological advancements influence demand for specific ATE solutions.

For instance, the segmentation by Type distinguishes between ATE for semiconductors, board-level testing, and solutions for electronic manufacturing services, highlighting the varied requirements across the production chain. Application-based segmentation provides insights into the end-user industries driving ATE demand, such as consumer electronics, automotive, and telecommunications, each with unique performance and compliance standards. Component-wise segmentation breaks down the ATE system into its core elements like testers, probers, handlers, and accompanying software, offering a view into the technological intricacies and market shares of each part. This multi-faceted segmentation framework ensures a comprehensive market assessment, reflecting the complexity and evolving needs of the global ATE industry.

- By Type: Semiconductor ATE, Board-Level ATE, Electronic Manufacturing Services (EMS) ATE, Others.

- By Application: Consumer Electronics, Automotive, Aerospace & Defense, Telecommunications, Industrial, Medical, Others.

- By Component: Testers (Digital, Mixed-Signal, RF, Analog, Power), Probers, Handlers, Software & Services, Integrated Systems.

Regional Highlights

- Asia Pacific (APAC): Dominates the ATE market due to a high concentration of semiconductor manufacturing facilities, robust electronics production, and increasing investments in advanced technologies like 5G and IoT, particularly in countries like China, Taiwan, South Korea, and Japan.

- North America: A significant market driven by strong R&D activities, the presence of major technology innovators, and high demand from aerospace, defense, and high-performance computing sectors. Early adoption of cutting-edge testing methodologies and focus on advanced packaging also contribute to its growth.

- Europe: Characterized by a strong automotive industry and a growing emphasis on industrial automation and medical electronics. Countries like Germany and the UK are key contributors, focusing on precision engineering and high-reliability testing for specialized applications.

- Latin America: An emerging market with growing electronics manufacturing capabilities and increasing investments in telecommunications infrastructure, presenting future growth opportunities though from a smaller base.

- Middle East & Africa (MEA): Shows potential with rising investments in digital infrastructure and diversification efforts in technology, but currently represents a smaller share of the global ATE market compared to other regions.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Automatic Test Equipment Market.- Advantest Corporation

- Teradyne Inc.

- National Instruments Corporation

- Cohu Inc.

- Chroma ATE Inc.

- LTX-Credence (Xcerra)

- Astronics Corporation

- Aemulus Holdings Bhd

- Acculogic Inc.

- Marvin Test Solutions Inc.

- Keysight Technologies Inc.

- Rohde & Schwarz GmbH & Co. KG

- STAr Technologies Inc.

- SPEA S.p.A.

- Fuji Corporation

- ATE Systems Ltd.

- Test Research, Inc. (TRI)

- JTAG Technologies B.V.

- Yokogawa Electric Corporation

- VIAVI Solutions Inc.

Frequently Asked Questions

Analyze common user questions about the Automatic Test Equipment market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is Automatic Test Equipment (ATE) and why is it important?

Automatic Test Equipment (ATE) refers to computer-controlled systems designed to test electronic components and systems quickly and efficiently. It is crucial for ensuring product quality, reliability, and performance by detecting defects, verifying specifications, and reducing the time-to-market for complex electronic devices across various industries like semiconductors, automotive, and consumer electronics.

What key factors are driving the growth of the Automatic Test Equipment market?

The ATE market growth is primarily driven by the increasing complexity and miniaturization of electronic devices, the rapid expansion of 5G and IoT technologies, rising demand for automotive electronics (ADAS, EVs), and the continuous innovation in semiconductor manufacturing processes. These factors necessitate advanced testing solutions to maintain product integrity and accelerate development cycles.

How is Artificial Intelligence (AI) impacting the Automatic Test Equipment industry?

AI is transforming the ATE industry by enabling more intelligent test pattern generation, optimizing test sequences, and enhancing fault detection capabilities through machine learning. It also facilitates predictive maintenance for ATE systems, improves data analytics for actionable insights, and contributes to the automation of complex decision-making processes, leading to greater efficiency and accuracy.

What are the major challenges facing the Automatic Test Equipment market?

Key challenges include the high initial capital investment required for advanced ATE systems, the rapid technological obsolescence of equipment due to fast-paced innovation, the shortage of a skilled workforce capable of operating and maintaining complex ATE, and the complexities associated with managing and analyzing the vast amounts of test data generated.

Which regions are leading the Automatic Test Equipment market in terms of growth and adoption?

Asia Pacific (APAC) currently dominates the ATE market, driven by its robust semiconductor and electronics manufacturing hubs in countries like China, Taiwan, South Korea, and Japan. North America and Europe also represent significant markets, characterized by strong R&D activities, early technology adoption, and high demand from specialized sectors like aerospace, defense, and automotive electronics.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted