Wafer Inspection Equipment Market

Wafer Inspection Equipment Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709383 | Last Updated : December 08, 2025 |

Format : ![]()

![]()

![]()

![]()

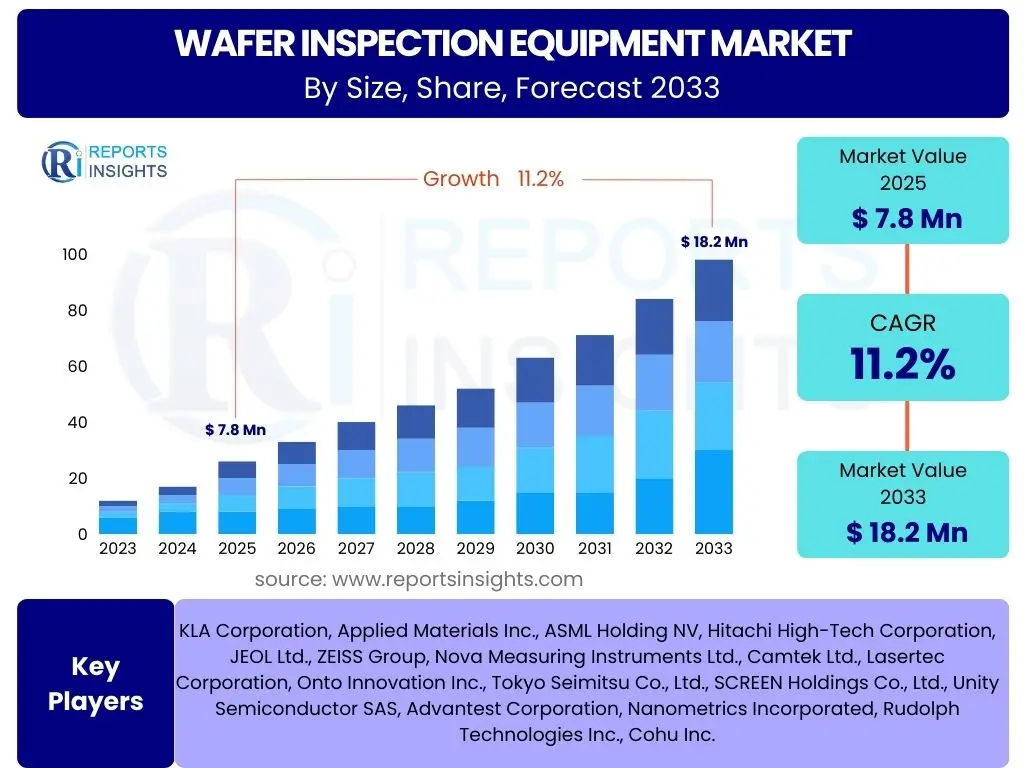

Wafer Inspection Equipment Market Size

According to Reports Insights Consulting Pvt Ltd, The Wafer Inspection Equipment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 11.2% between 2025 and 2033. The market is estimated at USD 7.8 Billion in 2025 and is projected to reach USD 18.2 Billion by the end of the forecast period in 2033.

Key Wafer Inspection Equipment Market Trends & Insights

The wafer inspection equipment market is undergoing significant transformation, driven by an escalating demand for advanced semiconductor devices across various industries. Key user inquiries frequently highlight the impact of miniaturization, the adoption of advanced packaging technologies, and the imperative for higher yield rates in complex manufacturing processes. These factors collectively push manufacturers towards more sophisticated and high-speed inspection solutions capable of detecting increasingly smaller and more intricate defects. Furthermore, the integration of automation and data analytics is a prominent trend, as companies seek to enhance efficiency and predictive capabilities within their inspection workflows.

Another critical insight is the growing emphasis on in-line and in-situ inspection methodologies. Traditional off-line inspection processes, while effective, can be time-consuming and may not provide immediate feedback for process optimization. The shift towards real-time monitoring and analysis allows for quicker identification of anomalies, leading to reduced waste and improved overall manufacturing throughput. Users are keenly interested in how these advancements contribute to cost reduction and accelerate time-to-market for next-generation chips, particularly in high-volume production environments where even minor defects can lead to substantial financial losses and reputational damage.

- Increasing demand for advanced semiconductor devices across consumer electronics, automotive, and data centers.

- Miniaturization of electronic components driving the need for higher resolution and precision inspection.

- Shift towards advanced packaging technologies requiring more stringent and diverse inspection capabilities.

- Integration of artificial intelligence and machine learning for enhanced defect detection and classification.

- Growing adoption of in-line and in-situ inspection systems for real-time process monitoring.

- Emphasis on yield management and process control optimization in semiconductor manufacturing.

AI Impact Analysis on Wafer Inspection Equipment

The integration of Artificial Intelligence (AI) and Machine Learning (ML) is fundamentally transforming the wafer inspection equipment landscape, directly addressing common user questions related to automation, accuracy, and operational efficiency. Users are primarily concerned with how AI can enhance the speed and reliability of defect detection, reduce human error, and enable predictive maintenance. AI algorithms are proving instrumental in processing vast amounts of image data generated during inspection, allowing for faster and more accurate identification of subtle defects that might be missed by conventional methods or human operators. This capability is critical for complex integrated circuits (ICs) where defect patterns are intricate and varied.

Furthermore, AI's influence extends to enabling smarter decision-making and process optimization. By analyzing historical inspection data, AI models can learn to predict potential failure points, classify defects with higher precision, and even suggest corrective actions to manufacturing processes. This predictive power is a significant area of interest for users looking to move beyond reactive quality control to proactive yield management. The expectation is that AI will not only improve defect detection but also contribute significantly to reducing false positives and false negatives, thereby optimizing throughput and minimizing the need for costly re-inspections or scrapped wafers, leading to substantial cost savings and improved production cycles.

- Enhanced defect detection accuracy and speed through intelligent image processing and pattern recognition.

- Reduction in false positives and false negatives, leading to improved throughput and reduced re-inspection costs.

- Automated defect classification and root cause analysis, streamlining quality control processes.

- Predictive maintenance capabilities for inspection equipment, minimizing downtime and optimizing operational efficiency.

- Development of adaptive inspection algorithms that can learn from new defect types and evolving wafer designs.

- Facilitation of big data analytics from inspection results for comprehensive process optimization and yield improvement.

Key Takeaways Wafer Inspection Equipment Market Size & Forecast

The Wafer Inspection Equipment Market is poised for robust growth, reflecting the escalating demands of the semiconductor industry. Key user inquiries consistently revolve around understanding the core drivers behind this expansion, the primary regions contributing to market acceleration, and the enduring impact of technological advancements on future market trajectory. A significant takeaway is the strong correlation between increased semiconductor capital expenditure globally and the sustained investment in advanced inspection solutions. This indicates that as manufacturers expand production capabilities and introduce more complex chip designs, the need for sophisticated and reliable inspection equipment will only intensify, making it a critical bottleneck in the production chain.

Another crucial insight is the long-term viability and strategic importance of investing in technologies that support both current and future semiconductor manufacturing nodes. The market's projected growth rate of 11.2% CAGR and its substantial increase in valuation from USD 7.8 Billion in 2025 to USD 18.2 Billion by 2033 highlight a resilient sector driven by continuous innovation. This growth is not merely incremental but reflective of a fundamental shift towards higher performance, greater efficiency, and more rigorous quality assurance in chip production. The market's trajectory underscores the indispensable role of advanced inspection in enabling the next generation of computing, communication, and intelligent systems, making it a pivotal sector for stakeholders.

- Strong growth projected at 11.2% CAGR, indicating a high-potential market.

- Market valuation expected to more than double from USD 7.8 Billion in 2025 to USD 18.2 Billion by 2033.

- Growth is driven by increasing demand for advanced semiconductors and stricter quality control.

- Technological innovation, particularly in AI and advanced optics, will be critical for market leadership.

- Asia Pacific will remain a dominant region due to concentration of semiconductor manufacturing.

- The market offers significant opportunities for companies providing high-precision, automated, and intelligent inspection solutions.

Wafer Inspection Equipment Market Drivers Analysis

The rapid advancement in semiconductor technology, characterized by device miniaturization and increasing circuit density, stands as a primary driver for the wafer inspection equipment market. As feature sizes shrink to nanometer scales, the detection of even microscopic defects becomes paramount to ensure functionality and reliability. This relentless pursuit of smaller, more powerful, and energy-efficient chips in devices like smartphones, IoT gadgets, and high-performance computing systems directly fuels the demand for ultra-precise and sensitive inspection tools. Manufacturers are continuously upgrading their facilities and processes, necessitating inspection equipment capable of handling increasingly complex wafer structures and materials with higher throughput and accuracy.

Another significant driver is the global expansion of semiconductor manufacturing capacities, particularly in Asia Pacific. Countries like Taiwan, South Korea, China, and Japan are heavily investing in new foundries and fabrication plants to meet the burgeoning demand for semiconductors. This expansion inherently increases the volume of wafers requiring inspection at various stages of the manufacturing process, from raw wafer inspection to patterned wafer and final die inspection. Additionally, the proliferation of advanced packaging technologies, such as 3D ICs, fan-out wafer-level packaging (FOWLP), and system-in-package (SiP), introduces new inspection challenges that traditional methods cannot address, thus creating a strong impetus for the development and adoption of specialized inspection equipment.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Miniaturization & Increasing Device Complexity | +3.5% | Global, particularly APAC (Taiwan, South Korea) | Short-to-Mid Term (2025-2029) |

| Growth in Semiconductor Manufacturing Capacity | +2.8% | APAC (China, South Korea, Taiwan), North America | Mid-to-Long Term (2027-2033) |

| Rising Demand for Advanced Packaging | +2.2% | Global, especially automotive & high-end consumer electronics sectors | Mid-to-Long Term (2026-2033) |

| Increasing Adoption of IoT & AI Technologies | +1.7% | North America, Europe, APAC | Mid Term (2025-2030) |

| Stricter Quality Control & Yield Management | +1.0% | Global, all major semiconductor producing regions | Ongoing (2025-2033) |

Wafer Inspection Equipment Market Restraints Analysis

One primary restraint for the wafer inspection equipment market is the exceptionally high capital investment required for these advanced systems. Cutting-edge inspection tools, especially those utilizing electron beam or deep ultraviolet (DUV) technologies, involve substantial upfront costs for acquisition, installation, and maintenance. This high barrier to entry can limit adoption, particularly for smaller foundries or integrated device manufacturers (IDMs) operating on tighter budgets. Furthermore, the rapid pace of technological obsolescence in the semiconductor industry means that equipment purchased today may require significant upgrades or replacement within a relatively short timeframe, adding to the total cost of ownership and posing financial challenges for market participants.

Another significant restraint is the increasing complexity and technical expertise required to operate and maintain these sophisticated inspection systems. The shortage of skilled engineers and technicians proficient in advanced semiconductor manufacturing and metrology processes can hinder the efficient deployment and utilization of wafer inspection equipment. Companies often face challenges in finding and retaining talent capable of interpreting complex inspection data, performing intricate calibrations, and troubleshooting highly specialized machinery. This skill gap, coupled with the intricate nature of defect characterization at advanced nodes, can slow down production cycles and impact the overall effectiveness of inspection processes, thereby constraining market growth to some extent.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Investment & Cost of Ownership | -2.5% | Global, particularly smaller fabs and new entrants | Ongoing (2025-2033) |

| Technological Complexity & Skilled Labor Shortage | -1.8% | North America, Europe, parts of APAC | Mid-to-Long Term (2026-2033) |

| Cyclical Nature of Semiconductor Industry | -1.2% | Global, impacting market stability | Short-to-Mid Term (2025-2028) |

| Data Management & Security Concerns | -0.8% | Global, especially for highly integrated systems | Mid Term (2027-2032) |

| Trade Tensions & Supply Chain Disruptions | -0.7% | Global, impacting equipment availability and cost | Short-to-Mid Term (2025-2029) |

Wafer Inspection Equipment Market Opportunities Analysis

The burgeoning demand from emerging markets and the increasing governmental support for domestic semiconductor manufacturing present significant opportunities for the wafer inspection equipment market. Countries in Southeast Asia, India, and parts of Eastern Europe are actively looking to establish or expand their semiconductor ecosystems to reduce reliance on existing hubs and ensure supply chain resilience. This geopolitical drive to localize chip production translates into new fabrication plant constructions and capacity expansions, thereby opening fresh avenues for inspection equipment sales and service contracts. Suppliers can leverage these new market entries by offering tailored solutions, including more cost-effective options or comprehensive support packages, to capture market share in these developing regions.

Furthermore, continuous innovation in inspection technologies, particularly the integration of advanced optics, AI/ML, and quantum sensing, offers substantial growth opportunities. The development of next-generation inspection tools capable of detecting sub-nanometer defects, performing faster in-line analysis, and providing more predictive insights into manufacturing processes creates significant competitive advantages. Companies investing heavily in R&D to enhance resolution, speed, and automation in their inspection platforms are well-positioned to capitalize on the industry's evolving needs. Moreover, the expansion into non-traditional semiconductor applications, such as medical devices, advanced sensors, and quantum computing components, which demand highly specialized inspection protocols, represents an untapped market segment for specialized wafer inspection solutions.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion in Emerging Semiconductor Manufacturing Hubs | +3.0% | Southeast Asia, India, Eastern Europe | Mid-to-Long Term (2027-2033) |

| Advanced R&D in AI-powered & Novel Inspection Technologies | +2.5% | Global, particularly North America, APAC (Japan, South Korea) | Ongoing (2025-2033) |

| Demand from New Application Areas (e.g., Medical, Quantum Computing) | +2.0% | Global, niche high-tech industries | Long Term (2029-2033) |

| Strategic Partnerships & Collaborations | +1.5% | Global, between equipment vendors and fabs | Mid Term (2026-2031) |

| Focus on Software-defined Inspection & Analytics | +1.0% | Global, particularly advanced manufacturing regions | Short-to-Mid Term (2025-2029) |

Wafer Inspection Equipment Market Challenges Impact Analysis

One of the foremost challenges facing the wafer inspection equipment market is the relentless pace of technological evolution in semiconductor manufacturing. As chip designs become increasingly complex and feature sizes continue to shrink, existing inspection technologies quickly become inadequate. This necessitates continuous and costly research and development efforts to create new equipment capable of detecting ever-smaller defects with higher speed and accuracy. The challenge lies in staying ahead of the curve, as the development cycles for new inspection tools often lag behind the rapid advancements in fabrication processes, creating a technology gap that can impact yield rates and time-to-market for chip manufacturers.

Another significant challenge pertains to the massive data generation and effective management required by advanced inspection systems. Modern wafer inspection tools generate terabytes of data per day, encompassing high-resolution images, spectral analyses, and metrology measurements. Processing, storing, and analyzing this vast amount of data in real-time to extract actionable insights presents a formidable hurdle. Companies face challenges in developing robust data infrastructure, implementing advanced analytics, and ensuring data security and integrity. Furthermore, the integration of diverse inspection systems from multiple vendors into a cohesive data analysis platform adds another layer of complexity, demanding interoperability and standardized data formats for comprehensive defect management and process control.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Technological Obsolescence & R&D Intensity | -2.0% | Global, particularly leading-edge fabs | Ongoing (2025-2033) |

| Massive Data Generation & Analytics Complexity | -1.5% | Global, all advanced semiconductor manufacturers | Mid-to-Long Term (2026-2033) |

| Ensuring Cost-Effectiveness for Small/Mid-Sized Fabs | -1.0% | Emerging markets, niche players | Ongoing (2025-2033) |

| Supply Chain Vulnerabilities for Critical Components | -0.8% | Global, impacting equipment manufacturers | Short-to-Mid Term (2025-2029) |

| Maintaining High Throughput with Increased Resolution | -0.7% | Global, high-volume production facilities | Mid Term (2027-2032) |

Wafer Inspection Equipment Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global Wafer Inspection Equipment Market, covering historical data, current market trends, and future growth projections. The report offers a detailed segmentation analysis, regional insights, competitive landscape, and the impact of emerging technologies like Artificial Intelligence. It is designed to assist stakeholders in understanding market dynamics, identifying growth opportunities, and making informed strategic decisions within the evolving semiconductor industry.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 7.8 Billion |

| Market Forecast in 2033 | USD 18.2 Billion |

| Growth Rate | 11.2% |

| Number of Pages | 265 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | KLA Corporation, Applied Materials Inc., ASML Holding NV, Hitachi High-Tech Corporation, JEOL Ltd., ZEISS Group, Nova Measuring Instruments Ltd., Camtek Ltd., Lasertec Corporation, Onto Innovation Inc., Tokyo Seimitsu Co., Ltd., SCREEN Holdings Co., Ltd., Unity Semiconductor SAS, Advantest Corporation, Nanometrics Incorporated, Rudolph Technologies Inc., Cohu Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The wafer inspection equipment market is segmented across various critical dimensions to provide a granular view of its structure and dynamics. These segmentations are designed to help stakeholders understand distinct market behaviors based on technology type, wafer dimensions, specific application areas within semiconductor manufacturing, and the diverse end-use industries that drive demand for integrated circuits. Each segment possesses unique requirements for precision, throughput, and defect detection capabilities, influencing the adoption rates and technological preferences of different market participants. Analyzing these segments in detail reveals the nuanced competitive landscape and the specific areas of growth and innovation.

The market is primarily divided by the type of inspection technology, with optical and e-beam systems forming the dominant categories due to their complementary strengths in defect detection and metrology. Further differentiation by wafer size reflects the industry's progression towards larger wafers, which require specialized handling and inspection tools. Application-based segmentation distinguishes between the needs of pure-play foundries and integrated device manufacturers (IDMs), each having distinct operational models and inspection priorities. Finally, the breakdown by end-use industry highlights how sectors like consumer electronics, automotive, and healthcare dictate the demand for specific types of semiconductors and, consequently, the inspection technologies required to ensure their quality and reliability.

- By Type:

- Optical Wafer Inspection Systems

- E-beam Wafer Inspection Systems

- Others (e.g., X-ray, Acoustic)

- By Wafer Size:

- 150 mm

- 200 mm

- 300 mm and Above

- By Application:

- Foundry

- IDM (Integrated Device Manufacturer)

- By End-Use Industry:

- Consumer Electronics

- Automotive

- Healthcare

- Telecommunication

- Industrial

- Others

Regional Highlights

- Asia Pacific (APAC): Dominates the global wafer inspection equipment market due to the high concentration of semiconductor manufacturing facilities, including major foundries and IDMs, particularly in Taiwan, South Korea, China, and Japan. Significant government investments and a robust electronics manufacturing ecosystem drive continuous demand.

- North America: A key region for advanced R&D and leading-edge technology development in semiconductors. The presence of major equipment suppliers and high-tech chip designers ensures a steady demand for innovative inspection solutions, especially for next-generation nodes.

- Europe: Demonstrates steady growth, supported by a strong automotive electronics sector and increasing investments in advanced manufacturing processes. The focus on domestic chip production through initiatives like the European Chips Act is expected to boost regional market expansion.

- Latin America & Middle East and Africa (MEA): Emerging regions with nascent but growing semiconductor industries. While currently smaller, these regions represent future growth opportunities as global semiconductor supply chains diversify and manufacturing capabilities expand.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Wafer Inspection Equipment Market.- KLA Corporation

- Applied Materials Inc.

- ASML Holding NV

- Hitachi High-Tech Corporation

- JEOL Ltd.

- ZEISS Group

- Nova Measuring Instruments Ltd.

- Camtek Ltd.

- Lasertec Corporation

- Onto Innovation Inc.

- Tokyo Seimitsu Co., Ltd.

- SCREEN Holdings Co., Ltd.

- Unity Semiconductor SAS

- Advantest Corporation

- Nanometrics Incorporated

- Rudolph Technologies Inc.

- Cohu Inc.

Frequently Asked Questions

What is wafer inspection equipment?

Wafer inspection equipment refers to advanced systems used in semiconductor manufacturing to detect defects, contaminants, and structural anomalies on silicon wafers. These tools ensure the quality and reliability of integrated circuits by identifying issues at various stages of production, from raw wafer to patterned wafer and final die inspection, crucial for maintaining high manufacturing yields.

Why is wafer inspection important in semiconductor manufacturing?

Wafer inspection is critically important because even microscopic defects can lead to significant device failures, impacting overall chip performance and reliability. By detecting defects early, manufacturers can improve yield rates, reduce waste, optimize production processes, and ensure that only high-quality chips proceed to final packaging, saving substantial costs and accelerating time-to-market.

What are the main types of wafer inspection technologies?

The primary types of wafer inspection technologies include optical inspection systems, which use light-based methods to detect surface and patterned defects, and e-beam (electron beam) inspection systems, which offer ultra-high resolution for detecting smaller, sub-nanometer defects that optical methods might miss. Other emerging technologies include X-ray and acoustic inspection for specific applications.

How does AI impact the wafer inspection equipment market?

AI significantly enhances wafer inspection by enabling faster and more accurate defect detection, classification, and analysis. AI-powered systems can process vast amounts of image data, reduce false positives, facilitate predictive maintenance for equipment, and contribute to overall process optimization by identifying trends and potential failure points, leading to higher efficiency and improved yields.

What is the growth outlook for the Wafer Inspection Equipment Market?

The Wafer Inspection Equipment Market is projected for robust growth, with a Compound Annual Growth Rate (CAGR) of 11.2% between 2025 and 2033, reaching USD 18.2 Billion by 2033. This growth is primarily driven by increasing demand for advanced semiconductors, miniaturization trends, the expansion of global manufacturing capacities, and continuous technological innovations in inspection methodologies.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted