Water Treatment Equipment in Power Market

Water Treatment Equipment in Power Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704541 | Last Updated : August 11, 2025 |

Format : ![]()

![]()

![]()

![]()

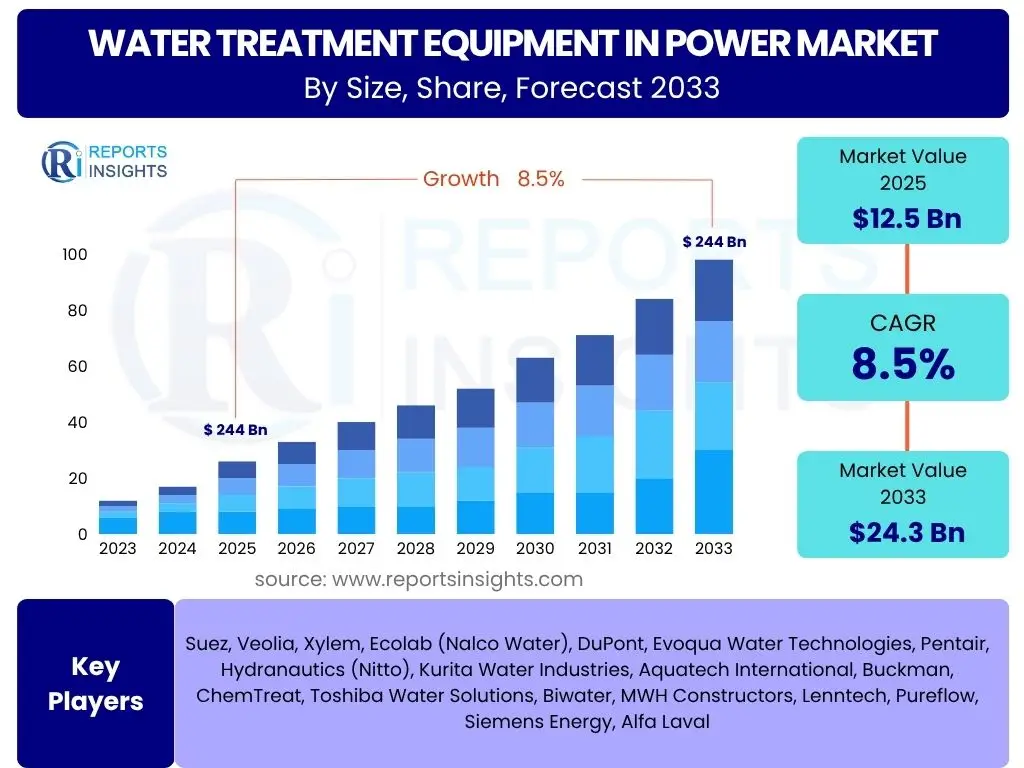

Water Treatment Equipment in Power Market Size

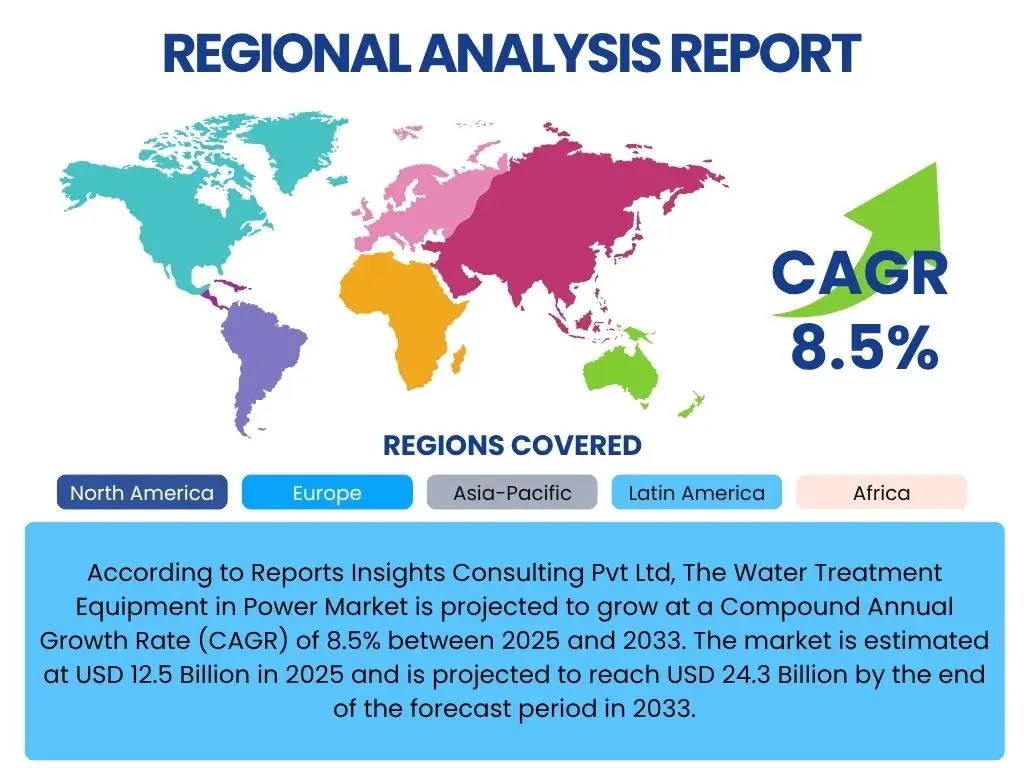

According to Reports Insights Consulting Pvt Ltd, The Water Treatment Equipment in Power Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2025 and 2033. The market is estimated at USD 12.5 Billion in 2025 and is projected to reach USD 24.3 Billion by the end of the forecast period in 2033.

Key Water Treatment Equipment in Power Market Trends & Insights

The Water Treatment Equipment in Power Market is significantly influenced by global efforts towards energy transition and the increasing stringency of environmental regulations. As power generation shifts towards more sustainable and efficient methods, the demand for advanced water treatment solutions intensifies to ensure operational purity, reduce water consumption, and minimize environmental discharge. This includes a growing emphasis on managing complex wastewater streams from diverse power plant types, from conventional thermal to emerging renewable energy facilities.

Key market trends underscore a move towards integrated and intelligent water management systems. Digital transformation, encompassing IoT sensors, data analytics, and automation, is becoming pivotal for real-time monitoring, predictive maintenance, and optimized process control. Furthermore, the imperative for water conservation is driving the adoption of Zero Liquid Discharge (ZLD) systems and advanced recycling technologies, especially in regions facing acute water scarcity, thereby transforming wastewater into a valuable resource rather than a waste product.

- Stringent environmental regulations demanding higher purity and reduced discharge.

- Increasing adoption of Zero Liquid Discharge (ZLD) and water reuse technologies.

- Integration of digitalization, IoT, and automation for enhanced operational efficiency.

- Growing demand for water treatment solutions in renewable energy power plants.

- Shift towards modular and decentralized water treatment systems for flexibility.

AI Impact Analysis on Water Treatment Equipment in Power

Artificial intelligence (AI) is poised to revolutionize the Water Treatment Equipment in Power Market by transforming operational efficiency, predictive capabilities, and resource management. Users anticipate AI will significantly enhance the accuracy of process control, enabling optimal chemical dosing, filtration rates, and energy consumption. This leads to more stable operations, reduced downtime, and lower overall operational costs by minimizing human error and maximizing system performance through continuous learning and adaptation.

Moreover, AI's application in predictive maintenance is a major area of focus, allowing power plant operators to anticipate equipment failures before they occur, thus scheduling maintenance proactively and extending the lifespan of critical assets. AI-powered analytics also facilitate deeper insights into water quality parameters, helping identify anomalies, predict treatment efficacy, and ensure compliance with environmental standards. This data-driven approach promises to make water treatment processes in power generation more resilient, sustainable, and economically viable.

- Predictive maintenance for water treatment equipment, reducing unscheduled downtime.

- Real-time process optimization through AI-driven control and automation.

- Enhanced chemical dosing accuracy and efficiency, leading to chemical savings.

- Improved energy efficiency in treatment processes via intelligent algorithms.

- Advanced anomaly detection and fault diagnosis for rapid issue resolution.

Key Takeaways Water Treatment Equipment in Power Market Size & Forecast

The Water Treatment Equipment in Power Market is characterized by a robust growth trajectory, primarily driven by the escalating global demand for energy, the pervasive challenge of water scarcity, and increasingly stringent environmental regulations. Power plants, regardless of their energy source, are critically dependent on effective water treatment for their operational integrity, efficiency, and compliance. This necessitates continuous investment in advanced technologies and solutions to manage diverse water quality challenges.

The forecast indicates sustained expansion, fueled by ongoing technological innovations aimed at improving treatment efficiency, reducing operational footprints, and promoting water reuse. Opportunities abound in the development of smart, digitally integrated systems and in emerging markets where new power infrastructure is being established. Addressing the nexus of energy generation and water management remains a paramount concern, driving both market growth and the imperative for sustainable practices.

- Consistent market expansion driven by global energy demand and environmental mandates.

- Critical role of water treatment in ensuring operational efficiency and regulatory compliance for power plants.

- Significant potential for technological advancements in intelligent and sustainable water solutions.

- Growing investment opportunities in regions with expanding power sectors and water stress.

- Increasing focus on water conservation and the circular economy within power generation.

Water Treatment Equipment in Power Market Drivers Analysis

The Water Treatment Equipment in Power Market is propelled by several fundamental drivers that underscore the critical role of water management in energy production. A primary driver is the burgeoning global demand for electricity, necessitating the expansion and modernization of power generation infrastructure across various energy sources. This expansion, particularly in emerging economies, directly translates to increased requirements for efficient water treatment systems to support new and existing plants.

Furthermore, the escalating global concern over water scarcity and the widespread implementation of stringent environmental regulations are compelling power plants to adopt advanced water treatment technologies. These regulations mandate higher discharge quality, limit water intake, and promote water reuse, pushing operators towards solutions like Zero Liquid Discharge (ZLD). Technological advancements, including innovations in membrane filtration, automation, and smart systems, also act as significant drivers, enhancing the efficiency and cost-effectiveness of treatment processes, thereby encouraging their adoption.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Global Energy Demand and Power Plant Expansion | +2.1% | Asia Pacific, North America, Europe | Short to Long-term |

| Stringent Environmental Regulations and Water Quality Standards | +1.8% | Europe, North America, China, India | Mid to Long-term |

| Growing Focus on Water Scarcity and Zero Liquid Discharge (ZLD) | +1.5% | Middle East, India, China, South Africa | Mid to Long-term |

| Technological Advancements in Water Treatment Solutions | +1.2% | Global | Short to Mid-term |

| Aging Power Plant Infrastructure and Need for Upgrades | +0.9% | North America, Europe | Mid-term |

Water Treatment Equipment in Power Market Restraints Analysis

Despite significant growth drivers, the Water Treatment Equipment in Power Market faces several restraints that can impede its expansion. A major restraint is the substantial capital expenditure required for installing advanced water treatment systems. The initial investment for technologies like Zero Liquid Discharge (ZLD) or large-scale membrane filtration can be prohibitive for some power plant operators, particularly smaller entities or those facing tight budget constraints, leading to slower adoption rates.

Furthermore, the operational and maintenance costs associated with these systems, including energy consumption, chemical usage, and disposal of concentrates and sludge, can also be considerable. The complexity of treating highly variable wastewater compositions from different power generation processes, along with the need for specialized technical expertise, presents ongoing challenges. Additionally, a scarcity of skilled personnel capable of operating and maintaining sophisticated water treatment technologies can limit the effective deployment and optimization of these systems, especially in developing regions.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Expenditure and Operational Costs | -1.5% | Global | Short to Mid-term |

| Complexity of Wastewater Composition and Treatment | -1.0% | Global | Ongoing |

| Lack of Skilled Workforce for Advanced Systems | -0.8% | Developing Economies | Mid to Long-term |

| Energy Consumption of Water Treatment Processes | -0.7% | Global | Ongoing |

Water Treatment Equipment in Power Market Opportunities Analysis

Significant opportunities exist within the Water Treatment Equipment in Power Market, driven by evolving technological landscapes and increasing sustainability imperatives. The growing adoption of smart and digital water treatment solutions, including IoT-enabled monitoring, predictive analytics, and AI-driven process control, presents a vast area for innovation and market expansion. These technologies promise enhanced efficiency, reduced operational costs, and improved regulatory compliance, appealing to power plant operators seeking to optimize their water management strategies.

The global shift towards renewable energy sources also creates new avenues for growth. As solar, wind, and geothermal power plants expand, so does the need for specialized water treatment equipment tailored to their unique operational requirements, which often include managing cooling water, process water, and wastewater. Furthermore, increasing investments in infrastructure development, particularly in developing economies, coupled with a heightened focus on water reuse and recycling initiatives, provide fertile ground for market players to introduce advanced and sustainable water treatment solutions, moving towards a circular water economy in the power sector.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Adoption of Smart and Digital Water Treatment Solutions | +1.7% | Global, particularly developed regions | Short to Long-term |

| Increasing Demand from Renewable Energy Power Plants | +1.4% | Asia Pacific, Europe, North America | Mid to Long-term |

| Growing Investments in Developing Economies | +1.3% | Asia Pacific, Latin America, MEA | Mid to Long-term |

| Water Reuse and Recycling Initiatives | +1.1% | Global, particularly water-stressed regions | Ongoing |

Water Treatment Equipment in Power Market Challenges Impact Analysis

The Water Treatment Equipment in Power Market encounters several challenges that require innovative solutions and strategic adaptation. One significant challenge is the effective management and disposal of sludge, brine, and other concentrates generated during the treatment process. As environmental regulations become stricter, the costs and complexities associated with the safe and sustainable disposal of these by-products continue to rise, urging the development of technologies that minimize waste volume or facilitate resource recovery.

Another major hurdle involves the high energy intensity of certain advanced water treatment technologies, such as reverse osmosis and thermal evaporation. While these technologies are highly effective, their substantial energy consumption can offset some of the environmental benefits and add to operational costs, pushing for innovations in energy-efficient processes. Additionally, adapting to the diverse and often rapidly changing composition of raw water sources, coupled with the emerging threat of cybersecurity risks for increasingly connected and automated treatment systems, poses ongoing challenges for ensuring reliable and secure water management in power plants.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Management and Disposal of Sludge and Concentrates | -1.2% | Global | Ongoing |

| Meeting Evolving Regulatory Requirements | -0.9% | Global | Ongoing |

| High Energy Intensity of Advanced Technologies | -0.8% | Global | Ongoing |

| Cybersecurity Risks for Connected Systems | -0.7% | Global | Short to Mid-term |

Water Treatment Equipment in Power Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the Water Treatment Equipment in Power Market, offering critical insights into its current landscape and future trajectory. It encompasses a detailed examination of market size, growth drivers, restraints, opportunities, and challenges across various segments and key geographical regions. The report leverages extensive data to present a holistic view of the market's dynamics, supporting strategic decision-making for stakeholders involved in the power generation and water treatment industries.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 12.5 Billion |

| Market Forecast in 2033 | USD 24.3 Billion |

| Growth Rate | 8.5% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Suez, Veolia, Xylem, Ecolab (Nalco Water), DuPont, Evoqua Water Technologies, Pentair, Hydranautics (Nitto), Kurita Water Industries, Aquatech International, Buckman, ChemTreat, Toshiba Water Solutions, Biwater, MWH Constructors, Lenntech, Pureflow, Siemens Energy, Alfa Laval |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Water Treatment Equipment in Power Market is comprehensively segmented to provide a granular understanding of its diverse components and their respective market dynamics. This segmentation facilitates a detailed analysis of specific technologies, types of equipment, and their applications across various power generation facilities. Understanding these segments is crucial for identifying key growth areas, competitive landscapes, and strategic opportunities within the broader market.

- By Type: This segment includes filtration technologies such as membrane filtration (encompassing RO, UF, NF), sand, activated carbon, and multi-media filtration, which are essential for removing suspended solids and impurities. Ion exchange systems, crucial for demineralization and condensate polishing, are also covered. Disinfection methods like UV, chlorination, and ozonation, along with clarification processes such as coagulation, flocculation, and sedimentation, are vital for water quality control. Chemical treatments, including scale inhibitors, corrosion inhibitors, and biocides, address specific water chemistry challenges.

- By Technology: Key technologies like Reverse Osmosis (RO), Ultrafiltration (UF), Nanofiltration (NF), and Electrodeionization (EDI) represent advanced membrane and electrochemical processes for high-purity water production. Zero Liquid Discharge (ZLD) systems are a critical technology for minimizing wastewater discharge.

- By Application/End-use: This segment categorizes the market based on the type of power plant, including thermal power plants (coal-fired, gas-fired, oil-fired), nuclear power plants, and a growing segment of renewable energy power plants (hydroelectric, geothermal, biomass).

Regional Highlights

- Asia Pacific (APAC): The largest and fastest-growing market due to rapid industrialization, increasing energy demand, and significant investments in new power generation capacities, particularly in countries like China, India, and Southeast Asian nations. Stringent environmental regulations and a growing focus on water scarcity also drive the adoption of advanced treatment solutions.

- North America: A mature market characterized by stringent environmental regulations, a strong emphasis on industrial water reuse, and the modernization of aging power infrastructure. The region shows high adoption of advanced water treatment technologies and digital solutions for operational efficiency.

- Europe: Focuses heavily on sustainable water management, energy efficiency, and compliance with strict EU environmental directives. The market is driven by the transition to cleaner energy sources and the continuous upgrade of existing power plants to meet higher water quality and discharge standards.

- Latin America: An emerging market with significant potential, driven by growing energy demands, infrastructure development, and increasing awareness of environmental protection. Investments in new power projects and the need for reliable water sources contribute to market growth.

- Middle East and Africa (MEA): Characterized by acute water scarcity, making advanced water treatment technologies, especially desalination and ZLD, highly critical for power generation. The region is witnessing substantial investments in power infrastructure development, particularly in GCC countries, driving demand for innovative water solutions.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Water Treatment Equipment in Power Market.- Suez

- Veolia

- Xylem

- Ecolab (Nalco Water)

- DuPont

- Evoqua Water Technologies

- Pentair

- Hydranautics (Nitto)

- Kurita Water Industries

- Aquatech International

- Buckman

- ChemTreat

- Toshiba Water Solutions

- Biwater

- MWH Constructors

- Lenntech

- Pureflow

- Siemens Energy

- Alfa Laval

Frequently Asked Questions

What is water treatment equipment in the power market?

Water treatment equipment in the power market refers to a range of technologies and systems used by power plants (thermal, nuclear, renewable) to purify incoming water, manage process water, treat cooling tower water, and treat wastewater before discharge or reuse, ensuring operational efficiency, safety, and environmental compliance.

Why is water treatment crucial for power plants?

Water treatment is crucial for power plants to prevent scaling, corrosion, fouling, and microbiological growth in boilers, turbines, and cooling systems, which can lead to equipment damage, reduced efficiency, and unscheduled downtime. It also ensures compliance with environmental discharge regulations and promotes water conservation.

What technologies are dominant in this market?

Dominant technologies include various filtration methods (membrane filtration like Reverse Osmosis and Ultrafiltration), ion exchange, disinfection, clarification, and chemical treatment. Zero Liquid Discharge (ZLD) systems and advanced digital monitoring solutions are rapidly gaining prominence.

What are the key drivers for the Water Treatment Equipment in Power Market?

Key drivers include increasing global energy demand, stringent environmental regulations on water quality and discharge, growing concerns over water scarcity, the need for operational efficiency and asset protection in power plants, and continuous technological advancements in water treatment.

How does AI impact the Water Treatment Equipment in Power Market?

AI impacts the market by enabling predictive maintenance for equipment, optimizing treatment processes in real-time, improving chemical dosing accuracy, enhancing energy efficiency, and providing data-driven insights for better decision-making, thereby increasing overall plant performance and sustainability.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted