Viscose Fiber Market

Viscose Fiber Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_707369 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

Viscose Fiber Market Size

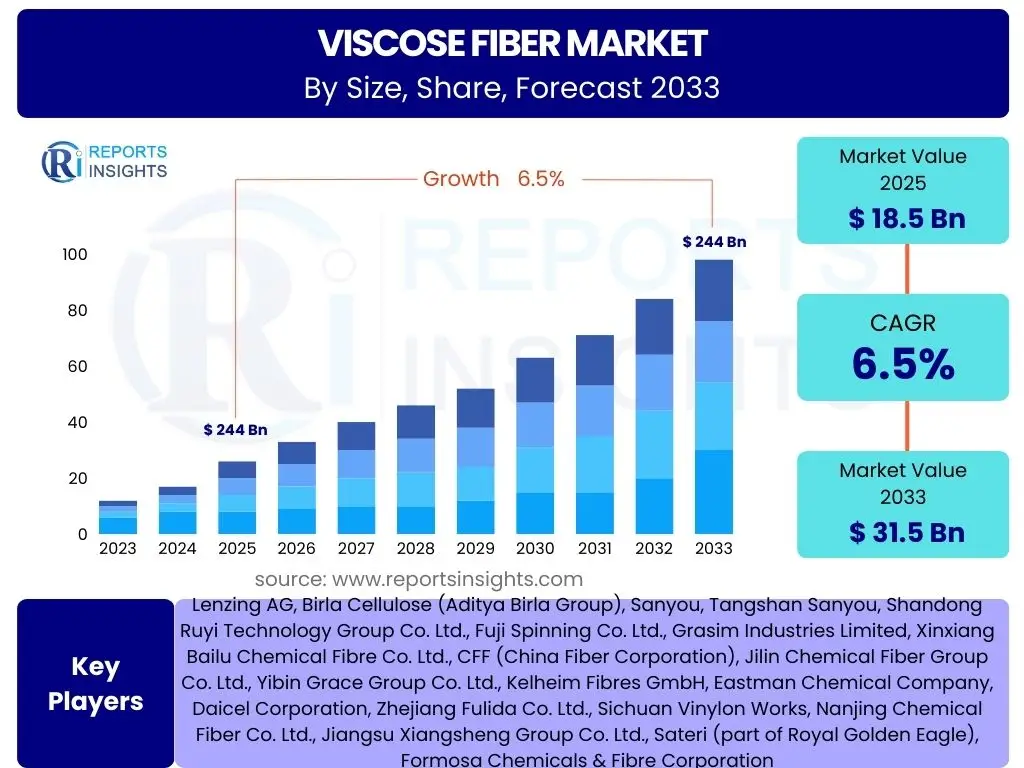

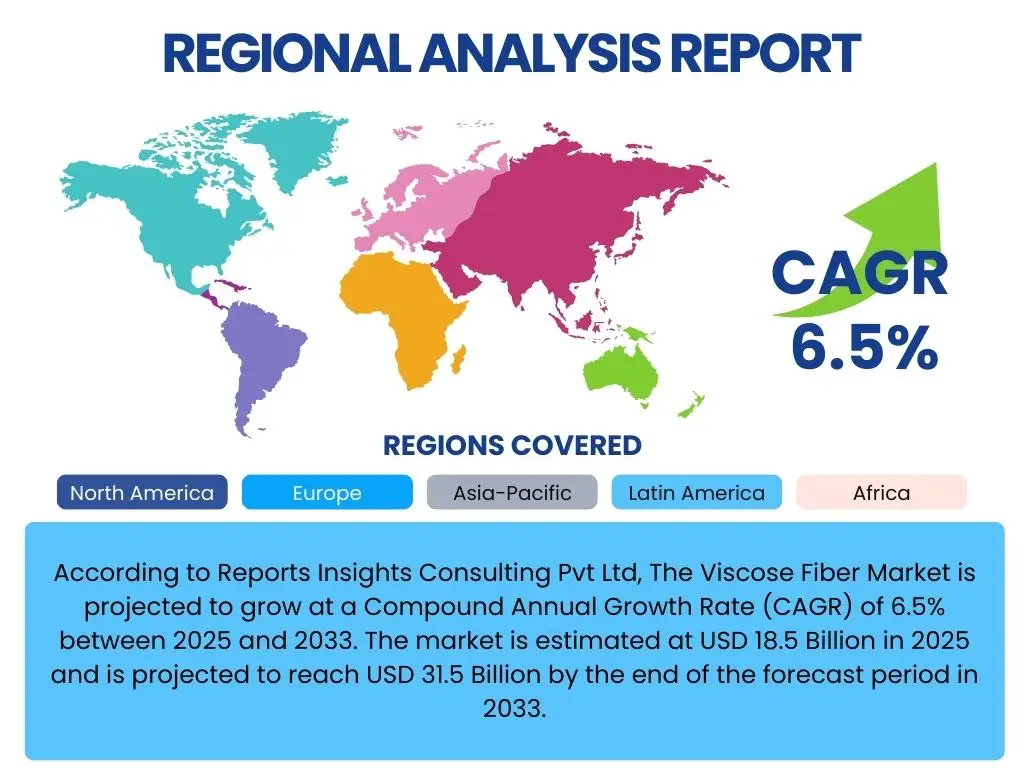

According to Reports Insights Consulting Pvt Ltd, The Viscose Fiber Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2025 and 2033. The market is estimated at USD 18.5 Billion in 2025 and is projected to reach USD 31.5 Billion by the end of the forecast period in 2033.

Key Viscose Fiber Market Trends & Insights

The Viscose Fiber market is currently shaped by a strong global shift towards sustainable and eco-friendly textile solutions. Consumers and brands are increasingly prioritizing materials that minimize environmental impact, driving demand for viscose variants produced through more responsible methods, such as closed-loop systems and certified wood pulp sources. This trend is not merely a niche preference but a mainstream movement influencing supply chains and product development across the apparel, home textiles, and non-woven sectors.

Technological advancements in viscose production are also playing a pivotal role, focusing on improving process efficiency, reducing chemical consumption, and enhancing the fiber's performance characteristics. Innovations leading to stronger, softer, and more durable viscose fibers are expanding their application scope beyond traditional clothing into sportswear, activewear, and specialized industrial textiles. The ability to blend viscose seamlessly with other natural and synthetic fibers to create composite materials with superior properties further amplifies its market appeal and utility.

Moreover, the expansion of the non-woven industry, particularly in hygiene products, medical textiles, and wipes, represents a significant growth area for viscose fiber due to its absorbency, biodegradability, and softness. Emerging economies, driven by rising disposable incomes and rapid urbanization, are experiencing a surge in demand for affordable yet quality textile products, which viscose fiber, with its versatile properties, is well-positioned to meet. The circular economy model is increasingly influencing the industry, pushing for the development of viscose fibers derived from textile waste, further bolstering its sustainable credentials and market viability.

- Growing emphasis on sustainable and eco-friendly textile solutions.

- Increased adoption of closed-loop production systems for reduced environmental footprint.

- Rising demand for viscose in activewear and performance textiles.

- Expansion of non-woven applications in hygiene and medical sectors.

- Technological innovations enhancing fiber properties and production efficiency.

- Strategic blending of viscose with other fibers for enhanced fabric characteristics.

- Shift towards circular economy models, utilizing textile waste as feedstock.

- Increasing disposable incomes in emerging economies driving textile consumption.

AI Impact Analysis on Viscose Fiber

Artificial intelligence is beginning to exert a transformative influence across various stages of the Viscose Fiber industry value chain, from raw material sourcing to manufacturing and demand forecasting. AI-driven analytics can optimize forest management for sustainable wood pulp sourcing, ensuring traceability and compliance with environmental standards. In the manufacturing process, AI algorithms can monitor and control complex variables such as temperature, chemical concentrations, and flow rates in real-time, leading to improved process efficiency, reduced waste, and enhanced product consistency. This precision translates into higher yields, lower operational costs, and superior fiber quality, directly impacting the profitability and competitiveness of viscose producers.

Furthermore, AI significantly enhances supply chain management and logistics within the viscose fiber market. Predictive analytics, powered by machine learning, can forecast demand fluctuations with greater accuracy, enabling manufacturers to optimize production schedules and inventory levels, thereby minimizing overproduction or stock shortages. This capability is crucial in managing the global supply of raw materials and finished products, reducing lead times, and improving overall responsiveness to market shifts. AI also facilitates more efficient distribution networks, identifying optimal routes and transportation methods to reduce carbon emissions and logistical costs, aligning with the industry's broader sustainability goals.

Beyond operational efficiencies, AI's role extends into research and development, accelerating the innovation cycle for new viscose fiber types and applications. Machine learning models can analyze vast datasets of material properties and performance characteristics, guiding the development of novel fibers with specific attributes, such as enhanced flame retardancy, moisture-wicking capabilities, or improved biodegradability. While the initial investment in AI infrastructure can be substantial, and the integration requires specialized expertise, the long-term benefits in terms of cost savings, increased productivity, improved sustainability, and competitive advantage are poised to make AI an indispensable tool for the future of the viscose fiber industry.

- Optimization of raw material sourcing and forest management for sustainability.

- Real-time process control and quality enhancement in manufacturing.

- Predictive analytics for accurate demand forecasting and inventory management.

- Improved supply chain efficiency and logistical optimization.

- Acceleration of research and development for novel fiber properties.

- Enhanced energy efficiency and waste reduction in production.

- Potential for automated quality inspection and defect detection.

Key Takeaways Viscose Fiber Market Size & Forecast

The Viscose Fiber market is poised for robust growth, driven by an escalating global demand for sustainable and versatile textile materials. The forecast demonstrates a clear trajectory of expansion, underpinned by shifting consumer preferences towards eco-conscious products and significant advancements in production technologies that address historical environmental concerns. This sustained growth is a testament to viscose's unique combination of natural origins, comfort, and performance attributes, which continue to make it a preferred choice across various end-use applications, from fashion apparel to specialized industrial uses.

A crucial takeaway is the industry's proactive response to environmental scrutiny, with significant investments in green technologies like closed-loop systems and the utilization of certified, sustainably managed forests. This commitment not only mitigates ecological impact but also enhances the fiber's market appeal and regulatory compliance, positioning it as a frontrunner in the sustainable fashion and textile movement. Furthermore, the diversification of viscose fiber into high-growth segments such as non-wovens, sportswear, and blended fabrics represents a strategic expansion that promises to unlock new revenue streams and strengthen market resilience against potential shifts in traditional textile markets.

- Projected steady market growth at a CAGR of 6.5% through 2033.

- Significant market value increase from USD 18.5 Billion in 2025 to USD 31.5 Billion by 2033.

- Sustainability initiatives are central to market expansion and acceptance.

- Technological advancements are enhancing production efficiency and environmental performance.

- Diversification of applications across textiles, non-wovens, and industrial sectors.

- Strong demand from emerging economies contributing substantially to growth.

- Increased focus on circular economy practices and textile waste recycling.

Viscose Fiber Market Drivers Analysis

The increasing global emphasis on sustainable and eco-friendly materials is a primary driver for the Viscose Fiber market. As environmental awareness grows among consumers and regulatory bodies worldwide, there is a distinct shift away from synthetic fibers that have a high carbon footprint or are non-biodegradable. Viscose, being derived from renewable natural resources like wood pulp, offers a compelling alternative that aligns with green consumer preferences and corporate sustainability mandates. This demand is further amplified by the fashion industry's push for more responsible sourcing and manufacturing practices, leading many apparel brands to significantly increase their use of cellulosic fibers.

The robust growth of the global textile and apparel industry, particularly in emerging economies, significantly contributes to the demand for viscose fiber. Rapid urbanization, rising disposable incomes, and evolving fashion trends in regions such as Asia Pacific are fueling a surge in textile consumption. Viscose fiber's desirable properties, including softness, breathability, vibrant dye absorption, and affordability, make it highly attractive for a wide range of clothing applications, from everyday wear to high-fashion garments. Its versatility allows it to be used standalone or blended with other fibers, expanding its utility and market penetration in diverse textile segments.

Furthermore, the expanding application scope of viscose fiber beyond traditional apparel into non-woven products and specialized industrial uses is a crucial market driver. In the non-woven sector, viscose is highly valued for its excellent absorbency, softness, and biodegradability, making it ideal for disposable wipes, hygiene products (e.g., feminine hygiene, baby diapers), and medical textiles. Simultaneously, ongoing technological advancements in viscose production are improving fiber strength, durability, and performance characteristics, enabling its adoption in industrial applications such like tire cords and filtration media, thereby broadening its market base and sustaining its growth trajectory.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand for Sustainable & Biodegradable Fibers | +1.5% | Global, particularly Europe & North America | Short to Mid-term (2025-2029) |

| Increasing Demand from Textile & Apparel Industry | +1.0% | Asia Pacific, Emerging Economies | Mid-term (2026-2030) |

| Expanding Applications in Non-Woven Products | +0.8% | North America, Europe, Asia Pacific | Mid to Long-term (2027-2033) |

| Technological Advancements in Production Processes | +0.7% | Global | Long-term (2028-2033) |

| Rising Disposable Income & Changing Lifestyles | +0.5% | Emerging Economies | Mid-term (2026-2031) |

Viscose Fiber Market Restraints Analysis

One of the primary restraints on the Viscose Fiber market has historically been environmental concerns associated with conventional production methods. Traditional viscose manufacturing processes can be chemical-intensive, involving the use of carbon disulfide, which can lead to air and water pollution if not properly managed. This has resulted in scrutiny from environmental organizations and consumers, potentially deterring some brands and end-users despite the fiber's natural origin. While significant strides have been made in developing more eco-friendly processes like the Lyocell method or closed-loop systems, the perception of environmental impact from older production technologies can still influence market adoption and regulatory pressures, particularly in developed regions with stringent environmental standards.

Another significant restraint is the volatility in raw material prices, primarily wood pulp. The cost of wood pulp is subject to fluctuations driven by factors such as forest management practices, climate change impacts, energy costs, and global demand-supply dynamics. As wood pulp constitutes a substantial portion of the production cost for viscose fiber, price instability can directly impact profit margins for manufacturers and lead to unpredictable pricing for consumers. This volatility can make long-term planning challenging for producers and potentially shift demand towards more price-stable synthetic alternatives, especially in cost-sensitive markets where slight price increases can significantly affect competitiveness.

Furthermore, intense competition from alternative fibers, both natural and synthetic, poses a considerable restraint. The market for textile fibers is highly competitive, with cotton, wool, silk, polyester, nylon, and acrylic offering various price points and performance characteristics. While viscose offers a unique blend of comfort and absorbency, synthetic fibers like polyester are often more durable, less prone to wrinkling, and generally more cost-effective to produce at scale. Natural fibers like cotton benefit from strong consumer recognition and established supply chains. Viscose must continuously innovate and emphasize its sustainable advantages and performance benefits to differentiate itself effectively and maintain its market share against a diverse range of competitors.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Environmental Concerns of Traditional Production Methods | -1.2% | Europe, North America, Global | Short to Mid-term (2025-2029) |

| Volatility in Raw Material (Wood Pulp) Prices | -0.9% | Global | Short-term (2025-2027) |

| Intense Competition from Synthetic & Other Natural Fibers | -0.7% | Global | Mid-term (2026-2030) |

| High Capital Investment for Eco-Friendly Technologies | -0.5% | Global | Long-term (2028-2033) |

Viscose Fiber Market Opportunities Analysis

A significant opportunity for the Viscose Fiber market lies in the continuous development and widespread adoption of advanced, eco-friendly production technologies. Innovations such as the Lyocell process, which utilizes a closed-loop solvent system, and other next-generation cellulosic fiber technologies are addressing the environmental drawbacks of traditional methods, offering a more sustainable and resource-efficient production pathway. Investing in these greener processes allows manufacturers to meet stringent environmental regulations, enhance their brand image, and cater to the growing segment of environmentally conscious consumers and brands. This technological leap represents a substantial competitive advantage, opening doors to partnerships with sustainable fashion brands and premium textile markets.

Another promising opportunity involves the expansion of viscose fiber into novel and high-performance application areas beyond traditional apparel. While fashion remains a core market, there is increasing potential in technical textiles, medical textiles, and specialized industrial uses. For instance, viscose's absorbency and softness make it highly suitable for advanced wound care products, surgical drapes, and high-performance filtration media. Furthermore, its excellent blending capabilities allow for the creation of innovative composite materials with enhanced properties like flame retardancy, moisture management, or microbial resistance, catering to the specific demands of these niche, high-value segments. This diversification reduces reliance on single market segments and opens up new revenue streams.

Moreover, the increasing focus on circular economy initiatives presents a transformative opportunity for the viscose fiber market. The development of technologies that can extract cellulose from textile waste, agricultural residues, or other non-wood sources to produce new viscose fibers is gaining traction. This "fiber-to-fiber" recycling approach not only minimizes waste but also reduces the reliance on virgin wood pulp, further enhancing the sustainability profile of viscose. Such initiatives align perfectly with global efforts to create a more circular textile industry, attracting investment, fostering innovation, and positioning viscose as a key player in the transition towards a truly sustainable material economy. Collaborations across the value chain, from waste collection to fiber regeneration, will be crucial for capitalizing on this opportunity.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development & Adoption of Eco-friendly Production Technologies | +1.8% | Global, especially Europe & North America | Mid to Long-term (2027-2033) |

| Expansion into New & High-Performance Applications | +1.0% | North America, Europe, Asia Pacific | Mid-term (2026-2030) |

| Growing Demand for Blended Fabrics & Smart Textiles | +0.8% | Asia Pacific, Global | Short to Mid-term (2025-2029) |

| Leveraging Circular Economy & Textile-to-Fiber Recycling | +0.7% | Europe, Global | Long-term (2028-2033) |

| Increasing Investments in Research & Development | +0.6% | Global | Long-term (2029-2033) |

Viscose Fiber Market Challenges Impact Analysis

A significant challenge facing the Viscose Fiber market is the imperative to achieve scalable and truly sustainable production practices. While advancements in closed-loop systems and responsible forest management are notable, the industry faces the complex task of ensuring these methods are adopted uniformly across all manufacturing facilities globally, particularly within smaller or less regulated markets. The demand for transparency and traceability throughout the supply chain, from forest to fiber, adds pressure. Ensuring that all raw materials are sourced from sustainably managed plantations and that production processes meet stringent environmental and social standards consistently is a formidable undertaking, requiring significant investment and continuous auditing to overcome greenwashing perceptions and maintain consumer trust.

Another key challenge is managing supply chain volatility and geopolitical risks. The global supply chain for viscose fiber relies on the availability of wood pulp from specific regions, which can be affected by natural disasters, political instability, trade disputes, or economic downturns. Such disruptions can lead to raw material shortages, increased logistics costs, and delays in production, impacting the reliability and cost-effectiveness of viscose fiber for end-users. Furthermore, rising energy costs, labor costs, and transportation expenses in various regions can put pressure on manufacturing margins, especially for a product that often competes on price with other fibers. Diversifying sourcing and building resilient supply networks are critical but complex solutions.

Lastly, overcoming price sensitivity in emerging markets and innovating to stay competitive against well-established and cheaper alternatives remains a persistent challenge. While consumers in developed markets are increasingly willing to pay a premium for sustainable products, price remains a significant determinant in large, growing markets like India and China. Here, viscose must compete not only with synthetic fibers but also with traditional natural fibers like cotton, which often have lower price points. Continuous innovation in fiber properties, such as enhanced durability or specific performance features, and optimizing production costs are essential to maintain competitiveness and expand market share in these critical growth regions. The challenge lies in balancing the cost of sustainable production with market price expectations.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Achieving Scalable & Consistent Sustainable Production | -1.0% | Global | Long-term (2029-2033) |

| Managing Supply Chain Volatility & Geopolitical Risks | -0.8% | Global | Short to Mid-term (2025-2028) |

| Price Sensitivity in Emerging Markets | -0.6% | Asia Pacific, Latin America | Mid-term (2026-2030) |

| Stringent Regulatory Compliance & Standards Evolution | -0.4% | Europe, North America | Short to Mid-term (2025-2029) |

Viscose Fiber Market - Updated Report Scope

This comprehensive report on the Viscose Fiber Market provides an in-depth analysis of market size, trends, drivers, restraints, opportunities, and challenges across various segments and key geographies. It incorporates a detailed competitive landscape, profiling leading market players and offering strategic insights into market dynamics from 2019 to 2033.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 18.5 Billion |

| Market Forecast in 2033 | USD 31.5 Billion |

| Growth Rate | 6.5% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Lenzing AG, Birla Cellulose (Aditya Birla Group), Sanyou, Tangshan Sanyou, Shandong Ruyi Technology Group Co. Ltd., Fuji Spinning Co. Ltd., Grasim Industries Limited, Xinxiang Bailu Chemical Fibre Co. Ltd., CFF (China Fiber Corporation), Jilin Chemical Fiber Group Co. Ltd., Yibin Grace Group Co. Ltd., Kelheim Fibres GmbH, Eastman Chemical Company, Daicel Corporation, Zhejiang Fulida Co. Ltd., Sichuan Vinylon Works, Nanjing Chemical Fiber Co. Ltd., Jiangsu Xiangsheng Group Co. Ltd., Sateri (part of Royal Golden Eagle), Formosa Chemicals & Fibre Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Viscose Fiber market is extensively segmented by type, application, and end-use industry, reflecting the fiber's remarkable versatility and diverse utility across a multitude of sectors. This granular segmentation provides critical insights into specific growth pockets and demand patterns, allowing stakeholders to tailor their strategies effectively. Understanding these segments is paramount for identifying key consumer preferences, technological requirements, and market penetration opportunities that drive the overall expansion of the viscose fiber landscape.

By type, the market differentiates between conventional Rayon, Modal (known for softness and dimensional stability), Lyocell (recognized for its eco-friendly closed-loop production), Cupro (silky texture, breathability), and HWM (High Wet Modulus) Viscose (enhanced strength when wet). Each type possesses distinct properties making it suitable for particular applications, from luxurious apparel to durable industrial materials. This diversification of types caters to a broad spectrum of performance needs and sustainability preferences, allowing manufacturers to innovate and differentiate their product offerings based on specific market demands and regulatory considerations.

The application and end-use industry segments highlight the broad utility of viscose fiber. In apparel, it spans everything from everyday clothing and activewear to lingerie and formal garments due to its comfort and aesthetic appeal. The non-woven sector, including hygiene products and medical textiles, leverages viscose's absorbency and biodegradability. Furthermore, its increasing adoption in home textiles (bedding, upholstery) and industrial applications (tire cords, filters) underscores its expanding utility. This widespread adoption across diverse industries is a testament to viscose's adaptability and its increasing role as a sustainable alternative to traditional materials, driving robust growth across its varied end-use segments.

- By Type:

- Rayon

- Modal

- Lyocell (Tencel)

- Cupro

- HWM Viscose

- Others

- By Application:

- Apparel

- Clothing

- Sportswear

- Lingerie

- Formalwear

- Home Textiles

- Bedding

- Upholstery

- Towels

- Curtains

- Non-Woven

- Wipes

- Hygiene Products

- Medical Textiles

- Filtration

- Industrial

- Tire Cords

- Industrial Filters

- Ropes

- Belts

- Other applications (including technical textiles)

- Apparel

- By End-Use Industry:

- Textile & Apparel Industry

- Automotive Industry

- Healthcare & Hygiene Industry

- Personal Care Industry

- Building & Construction

- Others

Regional Highlights

Asia Pacific is unequivocally the largest and fastest-growing market for Viscose Fiber, driven by its expansive manufacturing base for textiles and apparel, coupled with a rapidly increasing consumer population. Countries like China, India, and Southeast Asian nations are at the forefront of this growth, benefiting from rising disposable incomes, rapid urbanization, and a burgeoning middle class that fuels demand for diverse textile products. The region's substantial investments in textile manufacturing infrastructure, combined with its role as a global sourcing hub, solidify its dominance. Furthermore, increasing awareness and adoption of sustainable practices within these economies are further accelerating the shift towards viscose fiber as a preferred material.

Europe stands as a key market distinguished by its strong emphasis on sustainability, innovation, and stringent environmental regulations. While not the largest in terms of sheer volume, European demand for premium, eco-friendly viscose fibers, particularly those produced via closed-loop processes like Lyocell, is very high. The region is a hub for research and development in advanced textile materials and sustainable fashion, pushing the boundaries of viscose fiber performance and environmental credentials. Brands and consumers in Europe are highly sensitive to the ecological footprint of their products, driving manufacturers to invest heavily in certifications and transparent supply chains, thereby favoring responsibly produced viscose.

North America demonstrates a steady demand for viscose fiber, particularly in its applications within sportswear, activewear, and the non-woven sector. The region's consumers are increasingly seeking comfortable, breathable, and sustainable apparel, aligning well with viscose's inherent properties. Growth in the non-woven segment, driven by demand for wipes, hygiene products, and medical textiles, further contributes to market expansion. While textile manufacturing has shifted globally, North America retains significant R&D capabilities and a strong consumer market that appreciates value-added, performance-oriented, and sustainably produced textile products, influencing global trends and driving demand for advanced viscose fiber types.

Latin America, the Middle East, and Africa represent emerging markets with significant growth potential for viscose fiber. Latin America's textile and apparel industries are gradually expanding, supported by a growing consumer base and increasing urbanization. In the Middle East and Africa, rising disposable incomes and changing fashion preferences are stimulating demand for comfortable and versatile clothing materials. While these regions currently have a smaller market share compared to Asia Pacific, the increasing awareness of sustainable products, coupled with developing manufacturing capabilities and a growing retail sector, suggests a promising future for viscose fiber adoption in these geographies.

- Asia Pacific: Dominates the market due to robust textile manufacturing, high population density, and rising disposable incomes. Countries like China and India lead in production and consumption.

- Europe: Focuses on premium, sustainable, and technologically advanced viscose fibers, driven by stringent environmental regulations and eco-conscious consumer demand.

- North America: Exhibits consistent demand, especially in non-woven applications and performance apparel, with a growing preference for sustainable textile options.

- Latin America: Emerging market with growing textile industries and increasing consumer awareness of sustainable materials.

- Middle East & Africa: Demonstrates nascent but growing demand, influenced by urbanization and evolving fashion trends, offering future growth opportunities.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Viscose Fiber Market.- Lenzing AG

- Birla Cellulose (Aditya Birla Group)

- Sanyou

- Tangshan Sanyou

- Shandong Ruyi Technology Group Co. Ltd.

- Fuji Spinning Co. Ltd.

- Grasim Industries Limited

- Xinxiang Bailu Chemical Fibre Co. Ltd.

- CFF (China Fiber Corporation)

- Jilin Chemical Fiber Group Co. Ltd.

- Yibin Grace Group Co. Ltd.

- Kelheim Fibres GmbH

- Eastman Chemical Company

- Daicel Corporation

- Zhejiang Fulida Co. Ltd.

- Sichuan Vinylon Works

- Nanjing Chemical Fiber Co. Ltd.

- Jiangsu Xiangsheng Group Co. Ltd.

- Sateri (part of Royal Golden Eagle)

- Formosa Chemicals & Fibre Corporation

Frequently Asked Questions

What is viscose fiber and how is it produced?

Viscose fiber, also known as rayon, is a semi-synthetic cellulosic fiber made from regenerated cellulose, typically sourced from wood pulp (like spruce, pine, or eucalyptus). The production process involves dissolving cellulose pulp in a chemical solution to form a viscous liquid, which is then extruded through spinnerets into a coagulating bath. This process regenerates the cellulose into solid filaments, which are then spun into fibers. While traditional methods can be chemical-intensive, modern advancements focus on more sustainable, closed-loop systems to minimize environmental impact and recover chemicals.

What are the primary applications of viscose fiber?

Viscose fiber boasts extensive applications across various industries due to its versatility and desirable properties. Its primary uses are in the textile and apparel sector, where it is favored for clothing, sportswear, lingerie, and formalwear due to its softness, breathability, and excellent drape. It is also widely used in home textiles for bedding, upholstery, and towels. Beyond traditional textiles, viscose is crucial in the non-woven industry for products like wipes, hygiene items (diapers, feminine hygiene products), and medical textiles (surgical gowns, bandages) owing to its absorbency and biodegradability. Industrial applications include tire cords, filtration media, and ropes.

Is viscose fiber considered a sustainable material?

The sustainability of viscose fiber is a nuanced topic. As it is derived from natural, renewable resources (wood pulp), it is inherently biodegradable. However, traditional production methods have faced environmental criticisms due to water and chemical usage. In response, the industry has made significant strides in sustainability, with many manufacturers adopting advanced eco-friendly processes like closed-loop systems (e.g., Lyocell production) that recover and reuse solvents, significantly reducing emissions and waste. Sourcing wood pulp from sustainably managed forests certified by organizations like FSC (Forest Stewardship Council) or PEFC (Programme for the Endorsement of Forest Certification) further enhances its environmental credentials, positioning modern viscose as a more sustainable choice.

What factors are driving the growth of the viscose fiber market?

Several key factors are propelling the growth of the viscose fiber market. Foremost among these is the escalating global demand for sustainable and biodegradable textile materials, driven by increasing consumer environmental awareness and brand commitments to eco-friendliness. The robust growth of the textile and apparel industry, particularly in emerging economies with rising disposable incomes, further fuels demand. Additionally, the expanding applications of viscose in the non-woven sector, including hygiene and medical products, contribute significantly. Continuous technological advancements that improve production efficiency and enhance fiber performance characteristics also play a crucial role in widening its market appeal and driving its growth trajectory.

How does AI impact the viscose fiber industry?

Artificial intelligence is beginning to revolutionize the viscose fiber industry by enhancing efficiency, sustainability, and innovation. AI-driven analytics optimize raw material sourcing, ensuring sustainable forest management and traceability. In manufacturing, AI algorithms provide real-time control over production parameters, improving quality consistency, reducing waste, and optimizing resource consumption. Furthermore, predictive AI models enable more accurate demand forecasting and streamlined supply chain management, leading to optimized inventory and reduced logistical costs. AI also accelerates R&D by analyzing complex data for developing novel fiber properties. These applications contribute to more sustainable, cost-effective, and competitive production processes.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted